Documents to confirm the zero VAT rate

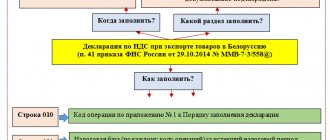

To confirm the zero VAT rate when exporting goods, the following documents are required (clause 1 of Article 165 of the Tax Code of the Russian Federation):

- a contract (a copy thereof) with a foreign person for the supply of goods outside the Customs Union;

- customs declaration (its copy) with the corresponding marks of the customs authorities;

- copies of transport, shipping and (or) other documents with appropriate marks from customs authorities.

This list of documents is exhaustive.

The Office reminds you of the possibility of submitting registers of customs declarations in electronic form

Date of publication: 02/29/2016 12:27 (archive)

In accordance with paragraph 15 of Article 165 of the Tax Code of the Russian Federation, the taxpayer-exporter is given the right, to confirm the validity of the application of the tax rate of 0 percent for VAT when selling goods provided for in subparagraph 1 of paragraph 1 of Article 164 of the Tax Code of the Russian Federation, to submit to the tax authority in electronic form:

- register of customs declarations (full customs declarations) provided for in subparagraphs 3 and 5 of paragraph 1 of Article 165 of the Tax Code of the Russian Federation, indicating in it the registration numbers of the relevant declarations instead of copies of these declarations;

- register of customs declarations (full customs declarations), as well as transport, shipping and (or) other documents provided for in subparagraphs 3 and 4 of paragraph 1 (except for the cases provided for in paragraph five of subparagraph 3, paragraph eight of subparagraph 4 of paragraph 1) of Article 165 of the Tax Code RF, instead of copies of these documents.

The forms and procedure for filling out the registers provided for in paragraph 15 of Article 165 of the Tax Code of the Russian Federation, as well as the formats and procedure for submitting registers in electronic form, were approved by Order of the Federal Tax Service of Russia dated September 30, 2015 No. ММВ-7-15/427.

To justify the application of a tax rate of 0 percent for VAT, the exporting taxpayer has the right to submit either the documents provided for in Article 165 of the Tax Code of the Russian Federation on paper or the Registers of information in electronic form.

According to paragraphs eleven, thirteen and fourteen of paragraph 15 of Article 165 of the Tax Code of the Russian Federation, the tax authority conducting a desk tax audit has the right to request from the taxpayer documents, information from which is included in the Registers of Information. Copies of these documents are submitted by the taxpayer within 20 calendar days from the date (day) of receipt of the relevant request from the tax authority. These documents must comply with the requirements stipulated by Article 165 of the Tax Code of the Russian Federation, including containing the appropriate marks of the Russian customs authority.

In accordance with paragraph sixteen of paragraph 15 of Article 165 of the Tax Code of the Russian Federation, if the taxpayer fails to provide, at the request of the tax authority, the above documents, information from which is included in the Registers of Information, the validity of applying a tax rate of 0 percent in the relevant part is considered unconfirmed.

Registers of customs declarations

Starting from the fourth quarter of 2015, instead of transport and shipping documents, exporters can submit their electronic registers to the tax inspectorates. The forms, formats and procedure for compiling such registers are approved by Order of the Federal Tax Service of Russia dated September 30, 2015 No. MMV-7-15/427 (hereinafter referred to as the Order) (Part 4 of Article 3 of Federal Law dated December 29, 2014 No. 452-FZ).

“Electronic” registers do not replace all documents that must be submitted to confirm the application of the zero VAT rate. In particular, a contract with a foreign company for the supply of goods must be submitted on paper (Clause 19, Article 165 of the Tax Code of the Russian Federation).

In addition, during a desk audit, the tax inspectorate has the right to request transportation documents, information from which is included in the registers. And also request the necessary documents if the information on export operations received from customs authorities does not correspond to the data contained in the “electronic” registers. Documents will need to be submitted within 20 calendar days after receiving the request. They must have Russian customs marks (clauses 15–18 of Article 165 of the Tax Code of the Russian Federation). If the exporter has not fulfilled the inspection requirement (in whole or in part), the justification for applying a 0 percent tax rate in the relevant part is considered unconfirmed.

At the moment, 14 registers have been approved, depending on the type of export transactions performed (clause 15 of article 165 of the Tax Code of the Russian Federation, clause 1 of the Order). Each register is “linked” to the corresponding subparagraph or paragraph of Article 165 of the Tax Code of the Russian Federation, as one of the documents confirming the right to apply the zero VAT rate.

The “electronic” register must contain information about the size of the tax base to which the zero VAT rate applies. The tax base is determined for each transaction, confirmed by documents, the details of which are reflected in the register.

Electronic registers of VAT documents for exporters

To confirm the validity of applying a 0 percent tax rate and VAT deductions, exporters must submit copies of customs declarations, shipping, shipping and other documents to the tax office. The entire list is listed in Article 165 of the Tax Code of the Russian Federation. From October 1, 2015, exporters received the right to reduce the number of papers - paragraph 15 of Article 165 of the Tax Code of the Russian Federation allows, instead of copies of documents, to send their electronic registers to the Federal Tax Service (Federal Law dated December 29, 2014 No. 452-FZ). The forms and formats of the registers were approved by order of the Federal Tax Service of Russia dated September 30, 2015 No. ММВ-7-15/427 (came into force on November 17, 2015).

Registers of documents confirming the 0% VAT rate have been added to the regulated reporting forms “1C: Accounting 8” starting with version 3.0.42.87. For information on the timing of support for forms and formats of document registers to confirm the 0% VAT rate in other 1C:Enterprise solutions, see “Monitoring Legislative Changes.”

Register No. 5

Registry form No. 5 is given in Appendix No. 5 to the Order. Here is the tabular part of the register:

| N p/p | Registration number of the customs declaration (full customs declaration) | Tax base for the corresponding transaction for the sale of goods (works, services), the validity of applying a tax rate of 0 percent for which is documented (in rubles and kopecks) | Code of the type of vehicle by which goods were imported into the territory of the Russian Federation or exported from the territory of the Russian Federation | Transport, shipping and (or) other document confirming the export of goods outside the Russian Federation or the import of goods into the territory of the Russian Federation | Note | ||

| Document type | Number | date | |||||

| 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 |

Section VI of Appendix No. 15 to the Order is devoted to filling out register No. 5. The following information is indicated in register columns No. 5:

- in column 1 - the serial number of the corresponding operation for the sale of goods (works, services);

- in column 2 - registration number of the customs declaration (full customs declaration) for the corresponding operation for the sale of goods (work, services);

- in column 3 - the tax base for the sale of goods (work, services), the validity of applying a tax rate of 0 percent for VAT for which is documented;

- in column 4 - codes of types of vehicles by which goods were imported into the territory of the Russian Federation or exported from the territory of the Russian Federation;

- in column 5 - types of transport, shipping or other documents (CMR, bill of lading, railway waybill, air waybill, TIR Carnet, shipping order, sea waybill, other document) confirming the export of goods outside the Russian Federation or the import of goods into the territory of the Russian Federation for the corresponding sale goods (works, services);

- in column 6 - the numbers of the documents indicated in column 5. If the number is missing, “b/n” is indicated;

- in column 7 - the dates of the documents indicated in column 5;

- in column 8 - other information related to the transaction, the details of the documents for which are reflected in register line No. 5. This is the type, number and date of the document submitted simultaneously with the VAT return, with the exception of the documents specified in columns 2, 5 - 7 For example, agreement (contract) No. 5-VAM-1991 dated May 21, 2015. If several documents are indicated, column 8 reflects the type, number and date of each document, separated by the sign “;”.

Registry information

Filling out information in the registry begins by adding the code of the operation for which the registry is being created. The required code is selected from the corresponding directory and the following information is indicated:

- serial number of the transaction for the sale of goods (works, services);

- registration number of the customs declaration for the relevant operation;

- the tax base for the relevant transaction, the validity of applying a 0% tax rate for which is documented;

- other information related to the transaction is indicated as a note (for example, the number and date of the agreement (contract) with a foreign partner).

In the "Total"

The total amount of the tax base for the corresponding transaction is automatically calculated.

This line is generated according to the transaction code and must correspond to the total amount of indicators in lines 020

of section 4 of the VAT tax return for the corresponding operation.

How to fill out column 4

Column 4 of register No. 5 indicates the codes of the types of vehicles with which goods were exported from the territory of the Russian Federation, by type of transport in accordance with Appendix No. 3 of the Decision of the Customs Union Commission dated September 20, 2010 No. 378.

In addition, in the declaration for goods in the first subsection of column 25 “Mode of transport at the border” the code of the type of vehicle is indicated in accordance with the classifier of types of transport and transportation of goods (subclause 25, clause 15 of section II of the Instructions for filling out customs declarations and customs declaration forms , approved by the Decision of the Customs Union Commission dated May 20, 2010 No. 257). That is, when filling out column 4, you can use the information from column 25 of the goods declaration “Mode of transport at the border”.

New registers have been approved to confirm the zero VAT rate for exporters

The Federal Tax Service has approved new forms and formats of registers for exporters to confirm the application of the 0% VAT rate. Order No. ED-7-15/ [email protected] has been officially published and will come into force on January 1, 2021.

New forms are being introduced:

- Register of customs declarations (full customs declarations) provided for in subparagraphs 3, 5 and 6 of paragraph 1, subparagraph 3 of paragraph 3.2, subparagraph 3 of paragraph 3.3, subparagraph 3 of paragraph 3.6, subparagraph 3 of paragraph 4 of Article 165 of the Tax Code of the Russian Federation (KND 1155110);

- Register of documents confirming the provision of services for the transportation of oil and petroleum products by pipeline transport, provided for in subparagraph 3 of paragraph 3.2 of Article 165 of the Tax Code of the Russian Federation (in the event that customs declaration is not provided for by the customs legislation of the Customs Union or is not carried out) KND 1155119;

- Register of documents confirming the provision of services for organizing transportation (transportation services in the case of import into the territory of the Russian Federation) of natural gas by pipeline transport, provided for in subparagraph 3 of paragraph 3.3 of Article 165 of the Tax Code of the Russian Federation (in the event that customs declaration is not provided for by the law of the EAEU or is not performed) KND 1155121;

- Register of complete customs declarations or documents confirming the provision of services for the transportation of oil and petroleum products by pipeline transport, as well as transport, shipping and (or) other documents provided for in subparagraphs 3 and 4 of paragraph 3.2 of Article 165 of the Tax Code of the Russian Federation (KND 1155120);

- Register of customs declarations (full customs declarations), as well as transport, shipping and (or) other documents provided for in subparagraphs 3 and 4 of paragraph 3.6, subparagraphs 3 and 4 of paragraph 4 of Article 165 of the Tax Code of the Russian Federation (KND 1155111);

- Register of declarations for goods provided for in paragraph 5 of subparagraph 3 of paragraph 1 of Article 165 of the Tax Code of the Russian Federation, or transport, shipping and (or) other documents provided for in subparagraph 4 of paragraph 1 of Article 165 of the Tax Code of the Russian Federation (KND 1155117);

- Register of transport, shipping and (or) other documents provided for in subparagraph 3 of paragraph 3.1 and subparagraph 3 of paragraph 3.7 of Article 165 of the Tax Code of the Russian Federation (when transporting goods by rail) KND 1155112;

- Register of transport, shipping and (or) other documents provided for in subparagraph 3 of paragraph 3.1 of Article 165 of the Tax Code of the Russian Federation (when transporting goods by road) KND 1155113;

- Register of transport, shipping and (or) other documents provided for in subparagraph 3 of paragraph 3.1 of Article 165 of the Tax Code of the Russian Federation (when transporting goods by air) KND 1155114;

- Register of transport, shipping and (or) other documents provided for in subparagraph 3 of paragraph 3.1, subparagraph 3 of paragraph 3.5, subparagraph 3 of paragraph 3.8, subparagraph 2 of paragraph 14 of Article 165 of the Tax Code of the Russian Federation (when transporting goods by sea or river vessels, mixed vessels (river-sea ) swimming) KND 1155115;

- Register of transportation documents provided for in paragraph 4.1 of Article 165 of the Tax Code of the Russian Federation (KND 1155122);

- Register of transportation, shipping or other documents provided for in paragraph 3.9 of Article 165 of the Tax Code of the Russian Federation (KND 1155123);

- Register of transportation documents provided for in paragraphs 5 (except for the fifth paragraph) and 5.1 of Article 165 of the Tax Code of the Russian Federation (KND 1155116);

- Register of transportation documents provided for in paragraph five of clause 5 and clauses 5.3, 6, 6.1, 6.2, 6.4 of Article 165 of the Tax Code of the Russian Federation (KND 1155118).

Order of the Federal Tax Service of Russia dated September 30, 2015 No. ММВ-7-15/427 “On approval of the forms and procedure for filling out registers provided for in paragraph 15 of Article 165 of the Tax Code of the Russian Federation, as well as formats and procedure for submitting registers in electronic form” will become invalid from January 1 2021

How to fill out columns 6 and 7

Column 6 of Register No. 5 indicates the numbers of transport, shipping or other documents confirming the export of goods outside the Russian Federation for the corresponding sale of goods (work, services). Column 7 indicates the dates of these documents. Regardless of the type of transport, if there is no number on the document, “b/n” is indicated in the register.

International waybill

With regard to filling out columns 6 and 7 of the international consignment note (hereinafter referred to as CMR), the Federal Tax Service of Russia notes the following.

The consignment note must contain the place and date of its preparation (Article 6 of the Convention on the Contract for the International Carriage of Goods by Road (CMR), concluded in Geneva on May 19, 1956, hereinafter referred to as the Convention). However, the Convention does not provide for a universal form of CMR. The CMR number can be indicated in the upper right corner, and the date of its completion (registration) and the name of the locality where the CMR was compiled can be indicated in column 21 “Compiled on/date”.

Railway consignment note

In the column “Consignment note No.” the shipment number assigned by the carrier is indicated (clause 3.3 of the Rules for filling out transportation documents for the transportation of goods by rail, approved by order of the Ministry of Railways of Russia dated June 18, 2003 No. 39 (hereinafter referred to as the Rules). In the column “Calendar stamps, documentation acceptance of cargo for transportation" on the reverse side of the original waybill and waybill, as well as on the front side of the spine of the waybill and receipt of cargo acceptance, a calendar stamp "Documentary registration of acceptance of cargo for transportation" is affixed, which indicates the date of documentary registration of acceptance of cargo for transportation (p 3.10 of the Rules) The consignment note must also contain the shipment number and the date of conclusion of the contract of carriage (Article 15 of the Agreement on International Rail Freight Transport of November 1, 1951).

In this regard, the register should indicate the shipment number and either the date of documentary registration of acceptance of the cargo for transportation, or the date of conclusion of the contract of carriage.

Shipping order and bill of lading

In column 7, when exporting goods by sea, river, mixed (river-sea) transport, the date of the transport, shipping or other document (bill of lading, sea waybill or any other document) confirming the fact of acceptance of the goods for transportation and the order for shipment is indicated.

The bill of lading must include the time and place of issue of the bill of lading, as well as the date of acceptance of the cargo by the carrier at the port of loading (Article 144 of the Merchant Shipping Code of the Russian Federation dated April 30, 1999 No. 81-FZ). Appendix 8 to Order No. 182 of the Ministry of Transport of Russia dated July 09, 2014 provides a recommended sample of an order for the shipment of export cargo, which contains the columns “Date of loading” and “Date of issue of the order.” Therefore, if there is no date on the document confirming the fact of acceptance of the goods for transportation, or in the order for shipment, the date of acceptance of the goods for transportation is indicated in column 7 of register No. 5.

Registers of documents for confirmation of VAT 0%

To confirm the VAT rate is 0%

for export, a package of documents is provided to the Federal Tax Service (Article 165 of the Tax Code of the Russian Federation).

Documents can be submitted entirely on paper or in a more convenient form - on paper and electronically using

a special register:

- contract (copy) with a foreign buyer;

- registers of customs declarations

(full customs declarations) of transport, shipping and (or) other documents in electronic form (clause 15 of article 165 of the Tax Code of the Russian Federation).

Registers of customs declarations, transport, shipping and other documents:

- Appendix No. 1;

- Appendix No. 2;

- Appendix No. 3;

- …

- Appendix No. 14.

Registers of documents provided for in paragraph 15 of Art. 165 Tax Code of the Russian Federation (from 3.0.78.68):

- procedures for filling out and submitting Registers to tax authorities in electronic form;

- XSD schemes (Letter of the Federal Tax Service of the Russian Federation dated May 15, 2020 N EA-4-15/ [email protected] ).

To automatically fill out the VAT Register: Appendix

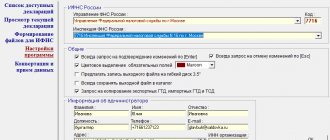

01

, you must first enter the document:

- Customs declaration (export).

This document can be created based on the document Sales of goods and class=”aligncenter” width=”1307″ height=”312″[/img]

Reports – Regular reports – Create – All tab – Tax reporting folder – VAT Register: Appendix 01 – Fill in

Data from documents is reflected:

- Customs declaration (export);

- Confirmation of zero VAT rate.

- the register number depends on the type of transactions for which the VAT rate of 0% is confirmed;

- registers are submitted together with the VAT return;

- first the declaration is sent, and thenafter receiving a receipt from the Federal Tax Service, there is already a register

Register No. 1

Registers

of declarations for goods for retail

, updated and approved by Order of the Federal Tax Service of the Russian Federation dated August 20, 2020 N ED-7-15 / [email protected] (valid from 2021):

- Register of declarations for goods or customs declarations CN 23, provided for in paragraphs. 7 clause 1 art. 165 of the Tax Code of the Russian Federation (KND 1155126);

- Register of declarations for goods for express cargo, provided for in paragraphs. 8 clause 1 art. 165 of the Tax Code of the Russian Federation (KND 1155128).

Enterprise accounting, version 3.0 – planned 3.0.86 from 12/18/2020.

Uploading in Federal Tax Service formats (from 3.0.82):

- Register No. 2, KND 1155119;

- Register No. 3, KND 1155121;

- Register No. 14, KND 1155118;

- Register for goods for express cargo, KND 1155128 (Letter of the Federal Tax Service of the Russian Federation dated 08/06/2020 N EA-4-15/ [email protected] ).

https://service.nalog.ru/customchk/?t=1602662325282

https://service.nalog.ru/blr1.do

Useful links. Services for foreign trade

| Address | Information |

| https://www.nalog.ru/rn77/service/traceability/ | Service for checking the traceability of goods, check the registration number of a consignment of goods (RNPT), check the processing status of a notification about the movement of goods subject to traceability to EAEU member states |

| https://service.nalog.ru/blr1.do | Obtain information about the import of goods and payment of indirect taxes. Valid for the Russian Federation and EAEU importing countries |

| https://service.nalog.ru/customchk/ | Online service of the Federal Tax Service for checking the correctness of customs declaration numbers. Allows you to check the fact of receipt from the Federal Customs Service of Russia of information on the documents necessary to confirm the validity of the application of the tax rate of 0 percent VAT |

See also:

- [10/16/2020 entry] VAT return for the 3rd quarter of 2021 in 1C

- Is the statistical form of the Federal Customs Service when working with the EAEU in 1C automatically generated only when importing?

- Submission of a statistical report to the Federal Customs Service in electronic form

- New rules for maintaining trade statistics with EAEU countries have been approved

- Import of goods from the EAEU. Prepayment in foreign currency 50%

- VAT register Appendix 01 to confirm the 0% rate

- Is it our responsibility to submit registers when confirming exports, or can we not submit them?

Did the article help?

Get another secret bonus and full access to the BukhExpert8 help system for 14 days free of charge

Related publications

- VAT register: Appendix 05 is not filled out...

- Incorrect code in the VAT Register: Appendix 5...

- Which register should I submit to the Federal Tax Service in 2021? ...

- VAT register Appendix 01 to confirm the 0% rate...

Registers of customs declarations instead of customs declarations

The Russian Ministry of Finance has developed and posted on its website a draft order approving the Procedure for submitting registers of customs declarations to the tax authorities to confirm the legality of applying the zero VAT rate when selling goods exported under the customs export regime.

The reason for the appearance of the document was the norm included on January 1, 2009 in Chapter 21 of the Tax Code of the Russian Federation, which gives the taxpayer the right to confirm the zero VAT rate when exporting goods, instead of customs declarations, submit registers of customs declarations (subclause 3 of clause 1 of Article 165 of the Tax Code of the Russian Federation ).

Obviously, the submission of registers instead of declarations will simplify the procedure in cases where the taxpayer has a significant number of customs declarations, despite the fact that the tax authority only needs to confirm the date of actual export of the goods. In addition, the tax office will be deprived of the opportunity to refuse to apply the zero rate, citing shortcomings in the registration of the customs declaration.

The Ministry of Finance proposes to introduce the following rules. If the goods are exported under the customs export regime, the taxpayer can, instead of the customs declaration, submit a register of declarations with marks from the border customs authority of the Russian Federation. If the goods are exported under the customs regime of export to the territory of a member state of the Customs Union, where customs control is abolished, or exported by pipeline transport or via power lines, instead of a customs declaration, a register with marks from the customs authority of the Russian Federation confirming the fact of placing the goods under the customs regime of export can be submitted.

At the same time, a number of issues arise, the resolution of which is no longer within the competence of the Ministry of Finance, but of the Federal Customs Service of Russia. First of all, is the register of customs declarations suitable as a document confirming the export of goods under current legislation?

The register form is given in the appendix to the letter of the Federal Customs Service of Russia dated July 2, 2010 No. 04-45/32583, from which it follows that it is intended for use by the customs authority as an internal departmental document. At the same time, customs legislation does not give taxpayers the right to use the register as a document confirming the actual export of goods.

The procedure for confirming the actual export of goods is determined by Order No. 1327 of the Federal Customs Service of Russia dated December 18, 2006. In accordance with it, the fact of export is certified, which can be affixed to the customs declaration (copy), transport or shipping document. Registers of customs declarations are not listed among the documents on which export notes can be made.

Thus, it is logical to expect that during the approval by the Federal Customs Service of the Procedure for submitting registers of customs declarations to the tax authorities proposed by the Ministry of Finance, customs officers will have to concern themselves with introducing changes to customs legislation.