There is hardly a company that does not require printing out any document, putting a signature on it or making a note - all of these actions require the presence of stationery at the enterprise. Sometimes you need a lot of them, sometimes very little, but in any case you need to be able to properly conduct accounting in relation to them. In this article we will talk about postings for writing off paper and stationery, and give an example of drawing up a write-off act.

Stationery supplies are purchased through an accountable person of the company or directly from the supplier. They are accounted for as inventories (inventories) and are reflected in accounts at the purchase price plus delivery costs, VAT is excluded. You also need to write off office supplies according to the rules.

What can be classified as office supplies?

This usually includes all devices that are intended for writing, designing and printing documentation.

Among the main copies:

- pens and pencils;

- felt-tip pens, markers, highlighters;

- paper, white and colored;

- cardboard;

- notebooks, notepads.

Separately, it is worth considering the fastening parts:

- paper clips, staples;

- glue;

- folders, cases, binders.

It is difficult to imagine an enterprise without devices. Among organizational and mechanical equipment:

- typewriters;

- calculators;

- scanner;

- hole puncher;

- stapler

Also, we must not forget about the cabinets in which all this will be stored, about school bags and other types of products that can be attributed to this.

This category contains promotional products that are issued to employees for distribution and use. Everything that is on the balance sheet and has actually already been spent should be written off.

To what account should I post office supplies? - posting

In practice, accounting for office supplies is not a very pleasant process in the accounting department, since it requires painstaking and time-consuming work, with relatively small amounts in receipt documents.

How to properly capitalize office supplies, in what account should they be accounted for, and how to write them off as cost? We will try to consider all these questions in the article, taking into account already established practice.

Option 1. Posting of stationery by quantity and amount

The most reliable way to reflect information, which is at the same time the most labor-intensive, is accounting for each unit of goods. Those. As it is written in the invoices, we register the goods: in quantity and amount.

For this accounting option, accounting account 10 “Materials” is used. Here you can create a group “Stationery”, where the name of the product is indicated by name: “binder”, “folder with ties”, etc.

Which subaccount should I include the accounting of stationery?

D-t 10 K-t 60.71, etc. In which subaccount should stationery be accounted for in this case? In principle, there is no big difference here, but it is important to consolidate this position in the accounting policy.

The first option is very appropriate if you buy a large number of office supplies, and then gradually issue them to employees as needed. Stationery is issued according to an invoice or request, the form of which must be fixed in the accounting policy of your company (analogous to form No. M-11).

This option for accounting for stationery supplies is the most reliable. It allows you to track the company's needs for a certain type of stationery at some point in time. For example, during the reporting period, the company’s needs for paper and pens increase. This is economically justified, and the tax authorities will not have any questions.

Option 2. We bring the whole party as a unit

With this option, all office supplies indicated in the receipt documents are received in the quantity of one unit, and are also written off. For this method of accounting, an order is issued, on the basis of which office supplies are received and simultaneously transferred for use.

How to receive stationery in this case? In this case, a copy of the delivery note (or similar document) of the supplier is attached to the receipt order in order to track the received stationery by name. To write off office supplies, employee requests are attached to the invoice (demand or similar document).

What are the pros and cons of this accounting option? Plus, the accounting method is very simple. But in this case, tax authorities may have questions.

Option 3. Capitalization by quantity

Another option for accounting for office supplies is to post them by quantity rather than by name. Those. in the accounting it will be written: “Stationery 15 pcs.” Those. the number of units indicated in the receipt documents will be the quantity of stationery.

In this case, the accountant cannot be blamed for the unreliability of the accounting reflection: after all, according to the documents, 15 pieces were actually received. Just as for the nomenclature, inspectors may have questions here. Still, a chair, for example, is also a thing, but it doesn’t cost as much as a standard ballpoint pen.

Questions in this case may also arise from the head of the company. If you show him, for example, that you purchased and wrote off 300 pieces of office supplies, this may raise additional questions: did you collect too much?

Option 4. Accounting for stationery without using account 10

Sometimes in practice, accountants receive office supplies without recording them in account 10 “Materials”. This method is often chosen if the purchased stationery is immediately written off for the needs of the company. Moreover, these expenses come as services immediately to expense accounts (25, 26, 44, etc.) and are recorded in accounting entries

Dt 25,26, 44, etc. K-60.71, etc. At the same time, these expenses are not included in inventories.

If the amounts are insignificant, tax authorities may not have any questions in this accounting option. But if the amounts are significant and permanent, then the error can be significant. Therefore, this method is very fraught with negative consequences.

A problem may also arise when deducting input VAT. Thus, the main point of accepting VAT for deduction is the acceptance of materials (goods) for accounting, and this rule was not followed.

Also, a problem may arise when rationing the costs of office supplies by type and location of operation, since you will not be able to give a clear answer as to exactly what office supplies are required by shop floor workers or administration employees. Although, according to accounting rules, each MP unit must be accounted for at the place of its operation.

Business Solutions

- shops clothing, shoes, groceries, toys, cosmetics, appliances Read more

- warehouses

material, in-production, sales and transport organizations Read more

- marking

tobacco, shoes, consumer goods, medicines Read more

- production

meat, procurement, machining, assembly and installation Read more

- rfid

radio frequency identification of inventory items More details

- egais

automation of accounting operations with alcoholic beverages Read more

Write-off act for office supplies

If the office was purchased with the company's money, then over time it is necessary to write it off in order to buy a new one. The main thing is to fill out this document correctly and comply with all the standards established by the company. Completing this paper is a mandatory part of the procedure; it is a primary accounting form.

Who has the right to use

This is a common form of deregistration, which is actively used by small, medium and large businesses alike, since every enterprise needs to write off office supplies. The tax system does not play a role here.

Why register it?

Quite often, companies that regularly purchase “stationery” classify it as an expense at the time they purchase it. But this is the wrong decision, because the tax service may issue a fine, since in this case the income tax becomes higher. The inspector does not recognize this as expenses that relate to the main activity for no reason.

It is the drawn up document that becomes the reason that justifies the removal of inventory items from the register and allows the amount to be added to the expenses of the enterprise. With its help, it becomes possible to officially reduce the tax base for all expenses of this kind.

Reasons and grounds for writing off office supplies in the act - sample and examples

Many accountants believe that it is easier to carry out such an operation immediately after purchasing a CT scanner. That is, they are brought to the company, the production is noted and immediately attributed to the expenses of the main activity. On the one hand, this way the specialist does not forget to indicate the expenses. But on the other hand, periodic acquisition and constant withdrawal on the same day becomes a violation.

When the inspector conducts an audit of activities, he will recognize this method as incorrect, recalculate and redistribute the balance so that a large amount will have to be paid due to changes in the level of profit.

Therefore, it is worth acting differently. How to write off an office - remove materials according to a pre-planned schedule, which will be established by special order. Another option is to create a manager’s order, in accordance with which responsible persons carry out an inventory.

At what point is it compiled and who will apply it?

This procedure assumes that records were kept from the acquisition of materials to removal from the balance sheet of the enterprise. Therefore, all operations must take place and it is necessary that they follow a certain algorithm.

How this is done:

1. Inventory and materials are received from a supplier or a traveling employee - written by PKO according to f. No. 4;

2. If it is necessary to send goods to a specific department, then indicate the requirement-invoice (form No. 11), which contains the purpose and quantity of products;

3. A document is drawn up and signed, preceded by a management order.

Each enterprise can use such paper for general taxation and for “simplified” taxes. That is, they can remove items from the balance that they previously placed there. But it is important that the CT scans are in a volume that is greater than what is written off. At the time of inventory before drawing up the act, they must also be on the accounts.

It is not advisable to leave all this to chance, since if you do not control the quantities and do not receive inventory items upon receipt, then problems will appear later at the time of write-off, since there is no reason for this. Even if it seems that the cost of the purchased pens is small, it gradually accumulates and it will no longer be possible to remove it from the balance with one operation. The shortages will grow every month. However, reporting will not be possible.

Now there are many different orders and recommendations from the Government that relate to the deregistration of fixed assets and inventory items. Note that it reveals two applications:

1. Reflects the status of the accounts on which the calculation will be carried out;

2. Shows how the budget tool can be used.

In addition, each organization must draw up its own internal regulations, which help regulate the features and order of movement of CT.

Recognize expense

If the acquired assets are used for production purposes, then their cost relates to expenses for ordinary activities (clause 5, clause 7 of PBU 10/99 “Expenses of the organization”) and is taken into account in cost accounts (20, 23, 25, 26, 44). These expenses are recognized in accounting in the reporting period in which they occurred (clauses 16, 17, 18 of PBU 10/99).

When calculating income tax, the cost of stationery is taken into account as part of other expenses associated with production and sales (subclause 24, clause 1, article 264 of the Tax Code of the Russian Federation).

Often, the cost of refilling a cartridge is taken into account by accountants as part of the cost of “office supplies”.

However, in letters of the Ministry of Finance of the Russian Federation dated February 8, 2007 No. 03-11-04/2/26, UMNS for Moscow dated December 1, 2004 No. 21-09/77274, such costs are proposed to be taken into account as part of material costs on the basis of subparagraph 2 paragraph 1 of Article 254 of the Tax Code of the Russian Federation. Example

In March 2011, an organization purchased office supplies from Skrepka+ LLC in the amount of 17,700 rubles, including VAT - 2,700 rubles.

The materials were received by the organization in full. Documents received from the supplier: waybill TORG-12, invoice. Materials were paid for by bank transfer. During the same period, the accountable person purchased stationery in a retail store in the amount of 1,416 rubles. A sales receipt is attached to the advance report; VAT in the amount of 216 rubles is highlighted on the cash receipt as a separate line. All purchased materials were put into operation. The accountant will make the following entries in accounting: Debit 10.9 Credit 60 - 15,000 rubles. – materials were received from Skrepka+ LLC (documentation: form No. M-4); Debit 19 Credit 60 – 2,700 rub. – VAT on purchased materials is taken into account; Debit 60 Credit 51 – 17,700 rub. – paid for materials from the current account (documentation: payment order, bank statement); Debit 68 Credit 19 – 2,700 rub. – input VAT is accepted for deduction (documentation: supplier invoice); Debit 60 Credit 71 – 1,416 rub. – an advance report was received and processed (documentation: a/o); Debit 10 Credit 60 – 1,200 rub. – materials have been capitalized (documentation: form No. M-4); Debit 19 Credit 60 – 216 rub. – VAT on purchased materials is taken into account; Debit 68 Credit 19 – 216 rub. – input VAT is accepted for deduction (documentation: check with the allocated VAT amount); Debit 26 (44) Credit 10 – 16,200 rub.

– office supplies were put into operation (documentation: Form No. M-11). For profit tax purposes, the cost of office supplies transferred to production is taken into account by the organization as part of the taxpayer’s other expenses associated with production and (or) sales in accordance with subparagraph 24 of paragraph 1 of Article 264 of the Tax Code of the Russian Federation.

Business Solutions

- the shops

clothes, shoes, products, toys, cosmetics, appliances Read more

- warehouses

material, in-production, sales and transport organizations Read more

- marking

tobacco, shoes, consumer goods, medicines Read more

- production

meat, procurement, machining, assembly and installation Read more

- rfid

radio frequency identification of inventory items More details

- egais

automation of accounting operations with alcoholic beverages Read more

How to write off office supplies: documentation in a budget institution

It is important here to check what is deregistered and in what quantity, because the tax office will definitely raise questions about 10 calculators every month, which are used by a department of 2 people.

More often, small CTs are purchased for cash or by bank transfer; in the first case, this is usually purchased by an accountable person; in the second, it is transferred to a bank account in favor of the supplier.

It doesn’t matter whether they will be transferred to the warehouse or immediately used by employees, they should be recorded in accounting. For this procedure, a specialist will need:

- invoice;

- cash and sales receipts.

Based on the first document, the accountant will draw up a PQR, which will indicate the names of all CTs that were purchased. Units of measurement and quantities of purchased items are also specified. Enter the financially responsible person who made the purchase and the one to whose warehouse the goods are credited.

The header of the statement will look like this:

| № | Employee's full name | Unit change | Volume | Signature |

It is filled out by the MOL when it is issued from warehouses to people for use. At the end of the month, he closes it, checks actual availability with virtual balances, and transfers it to the accounting department. These papers may be closed at another period if this is established by internal regulations.

Based on this file, the accountant draws up a demand invoice for writing off office supplies. It reflects the general CT issued and is filed with the rest of the documents of the month.

It is worth remembering that if the organization is small and there are not many employees who use CT, then the statement is not required. When the office movement is small, you can immediately use the demand invoice and write off on this basis. In addition, an act is drawn up.

The manager checks the completion and number of specified copies of the CT, looks at the availability of documentation in accounting. If everything is correct, then the costs are included in expenses and are considered written off.

The procedure for writing off office supplies

When transferring office supplies and accessories from the warehouse to the company's structural divisions, unified forms are drawn up:

- limit-fence card (form No. M-8);

- requirement-invoice form M-11;

- invoice according to the standard interindustry form M-15.

Important: some accountants include the costs of refilling cartridges as expenses for office supplies. This approach is incorrect, as evidenced by paragraph 2 of paragraph 1 of Article 254 of the Tax Code of the Russian Federation. These costs must be attributed to the company’s material expenses.

If the office supply has expired, the receiving unit draws up a corresponding act to write it off. Among the mandatory information in this document, the following information can be noted:

- Name and quantity;

- Registration price and amount for all items;

- Where is the material consumption facility spent?

- If so, the consumption standard;

- Other information at the discretion of the compilers.

An example of an entry in synthetic accounting accounts when writing off office supplies for general business needs:

| Account debit | Account credit | Wiring Description | A document base |

| 10.01 | Paper and pens written off for accounting needs | Request-invoice |

The company approves the form of the write-off act and the composition of the commission by local regulations (orders, regulations, etc.). Some accountants modify f. No. M-11, supplementing it with the necessary details, they use a modified document to write off office supplies after their service life has expired.

Important: the demand invoice form is approved by the company’s accounting policy for use and for writing off materials.

Written-off stationery - documentation in the Republic of Belarus (budget discrepancies)

To carry out this operation correctly, you need to enter the following information:

- name of the insurance company;

- the date on which the products were shipped;

- the number of the telephone message indicating that the sender was called, and the date on which it was composed;

- volume of seats;

- what does the packaging look like?

- units in which the measurement is carried out;

- passport ID.

It is worth noting that the contract can specify other papers that will be drawn up if deviations are detected.

What wiring should be

First you need to determine where the materials could go. There are many such paths in every organization; there is always the opportunity to write them off somewhere:

- as a basis for production;

- will become packaging for GP;

- one of the auxiliary consumables for the manufacture of the final product;

- promotes the liquidation of out-of-service fixed assets;

- used by the administration in their activities;

- useful for OS construction.

Depending on what a certain number of handles or cabinets were used for, the wiring data changes:

- Dt 20 – Kt 10 – when raw materials are sent to the production workshop;

- Dt 25 – Kt 10 – materials transferred to the repair department;

- Dt 26 – Dt 10 – the accounting department received office paper;

- Dt 44 – Kt 10 – containers for GP were issued;

- Dt 91-2 – Kt 10 – office supplies are allocated for the liquidation of a certain fixed asset;

- Dt 94 – Kt 10 – the missing (shortage) CTs were written off.

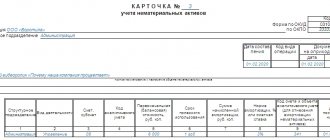

Accounting

In accounting, consider stationery as part of the materials on account 10-9 “Inventory and household supplies.” Document the purchase of stationery and reflect it in accounting in the usual manner prescribed for materials. For more information about this, see How to reflect the receipt of materials in accounting.

Situation: is it necessary to include stationery products with a useful life exceeding 12 months in accounting as part of fixed assets? For example, scissors, calculators, etc.

Stationery, the cost of which does not exceed the limit established in the accounting policy, can be recorded on account 10 “Materials” and written off at a time when put into operation.

Assets that meet all the characteristics of fixed assets and the cost of which does not exceed 40,000 rubles can be taken into account as part of the inventory (clause 5 of PBU 6/01). If an organization decides to exercise such a right, it must record this in its accounting policies for accounting purposes. In this case, you need to select a specific limit on the cost of objects with a useful life of more than a year, which will be taken into account as inventory. When setting such a limit, please note that its amount cannot exceed 40,000 rubles. (clause 5 of PBU 6/01).

When releasing office supplies from the warehouse, simultaneously with drawing up a demand invoice in Form No. M-11 or an act (report), make the following entries:

Debit 23 (25, 26, 29, 44...) Credit 10-9

– the cost of consumed stationery is included in expenses.

This is stated in paragraphs 90, 93, 97 and 98 of the Methodological Instructions, approved by order of the Ministry of Finance of Russia dated December 28, 2001 No. 119n.

What are the stages of purchasing office supplies?

The whole procedure consists of several sequential steps:

- First, a product is purchased, and a cash receipt and sales receipt must be obtained.

- A PKO is drawn up, without which it will not be possible to capitalize the “stationery”.

- Then the purchased items are sent to the warehouse or, in some cases, directly to the requesting department. If the actions were carried out through a warehouse, then a standard form is first drawn up. No. 4, then everything is issued upon request - an invoice with a mandatory mark in the statement.

- The last action of the life of the CT on the territory of the company will be the act of writing off and attributing it to the expenses of the enterprise. Remember that the document can be compiled in free form, this is not a unified paper. But it is better if a template is drawn up within the company according to which everything will happen every time.

We looked at how to correctly write off office supplies so as not to raise questions from the tax authorities and to correctly keep records of all purchased CTs in the organization.

This is necessary to avoid unnecessary losses and costs, because even if it seems that the amount spent on office supplies is minimal, it still needs to be taken into account. Gradually, it accumulates and turns out to be a serious expense item, so we advise you to keep an eye on it. Number of impressions: 15101

To what account should stationery be written off in accounting - accounting and examples

Stationery is accepted for accounting on the basis of the supplier's invoice in the Torg-12 form. If office supplies are purchased at retail by an accountable person, then the stationery is accepted for accounting on the basis of an advance report with a sales or cash receipt attached to it, which indicates the name of the product.

Accounting and documentation of the acquisition and use of office supplies

Purchased office supplies are accepted for accounting as such an object of material and industrial inventories (MPI), as materials, at the actual cost equal to the amount of actual costs for their acquisition (clauses 2, 5, 6 of the Accounting Regulations “Accounting for Materials and Materials”). production inventories" PBU 5/01, approved by Order of the Ministry of Finance of Russia dated 06/09/2001 N 44n). Stationery can be received in any of two options (clause 3 of PBU 5/01):

- or for each position (for example, a blue ballpoint pen, A4 paper, photo paper, a simple pencil, a folder-registrator, a folder-binder);

- or homogeneous groups (for example, writing instruments, paper, folders).

The chosen method should be fixed in the Accounting Policy. When transferring purchased office supplies to the financially responsible person (to the warehouse), you must do the following (clause 49 of the Methodology for accounting for inventories):

- or draw up a receipt order (form M-4);

- or put a stamp on the supplier’s invoice containing the name of the organization, the date of receipt of the stationery by the financially responsible person and the next receipt order number. In this case, a separate receipt order is not drawn up. The financially responsible person must sign the supplier's invoice.

On the date of transfer of office supplies for their intended use, their actual cost is recognized as an expense for ordinary activities (clauses 5, 8, 16 of the Accounting Regulations “Organizational Expenses” PBU 10/99, approved by Order of the Ministry of Finance of Russia dated May 6, 1999 N 33n ).

Stationery supplies are written off as expenses when transferred to the employees who use them, based on the invoice requirement (form M-11) (clause 93 of the Guidelines for accounting for inventories).

Accounting records for the transactions under consideration are made in accordance with the Instructions for the application of the Chart of Accounts for accounting of financial and economic activities of organizations, approved by Order of the Ministry of Finance of Russia dated October 31, 2000 N 94n, and are shown in the table of transactions:

| Wiring | Operation |

| D 10 - K 60 (71) | Stationery goods have been received |

| D 26 (44) - K 10 | Stationery supplied to employees |

Value added tax (VAT)

In general, organizations have the right to deduct VAT amounts presented by sellers of goods (works, services) on the basis of paragraphs 1, 2 of Art. 171 of the Tax Code of the Russian Federation in the manner established by paragraph 1 of Art. 172 of the Tax Code of the Russian Federation.

The submitted VAT amounts are highlighted as a separate line in settlement documents, primary accounting documents and in invoices (clause 4 of Article 168 of the Tax Code of the Russian Federation). The deduction of “input” VAT is made on the basis of an invoice issued by the seller (clause 1 of Article 172 of the Tax Code of the Russian Federation).

Corporate income tax

The cost of office supplies is included in other expenses on the date of their transfer to employees (clause 24, clause 1, article 264 of the Tax Code of the Russian Federation).

Example

In May 2015, the employee was given cash from the cash register for reporting purposes in the amount of 2,000 rubles. for purchasing office supplies.

On the same day, the employee submitted an advance report to the organization’s accounting department with the attachment of a cash register receipt and a sales receipt confirming the costs of purchasing office supplies in the amount of 2,006 rubles. (including VAT 306 rubles). An invoice is also attached to the advance report. The following entries must be made in accounting:

| Debit | Credit | Amount, rub. | Primary document | |

| Funds were issued on account for the purchase of office supplies | 71 “Settlements with accountable persons” | 50 "Cashier" | 2 006 | Account cash warrant |

| Office supplies accepted for accounting (2006 - 306) | 10 "Materials" | 71 “Settlements with accountable persons” | 1 700 | Advance report, Receipt order in form M-4 |

| The amount of VAT on purchased office supplies is reflected | 19 “Value added tax on acquired assets” | 71 “Settlements with accountable persons” | 306 | Invoice |

| VAT amount accepted for deduction | 68/VAT | 19 “Value added tax on acquired assets” | 306 | Invoice |

Tax paid when applying the simplified tax system

An organization applying the simplified tax system reduces the income received by the expenses provided for in paragraph 1 of Art. 346. 16 of the Tax Code of the Russian Federation, which, in particular, includes expenses for office supplies, provided they meet the criteria of paragraph 1 of Art. 252 of the Tax Code of the Russian Federation and in the manner provided for in paragraphs. 24 clause 1 art. 264 of the Tax Code of the Russian Federation (clause 17 clause 1, paragraph 1, 2 clause 2 of article 346. 16 of the Tax Code of the Russian Federation).

VAT amounts paid to the supplier when purchasing stationery, the cost of which is subject to inclusion in expenses in accordance with Art. 346.16 and 346.17 of the Tax Code of the Russian Federation are also included in expenses on the basis of paragraphs. 8 clause 1 art. 346. 16 Tax Code of the Russian Federation.

In this case, the amount of VAT paid by the organization to the supplier of office supplies is reflected as a separate line in gr. Section 5 I book of accounting of income and expenses of organizations and individual entrepreneurs using a simplified taxation system, the form of which was approved by Order of the Ministry of Finance of Russia dated October 22, 2012 N 135n.

Thus, the cost of office supplies and VAT on them (if there is an invoice) are recognized as expenses after they are paid (clause 17, clause 1, article 346.16 of the Tax Code of the Russian Federation).

In May 2015, the organization purchased stationery (folders, pens, buttons, pencils, etc.) for a total amount of 40,000 rubles. (including VAT).

Payments to the supplier are made non-cash. Stationery supplies were paid for in the month of their purchase and transferred for use in the production activities of the organization. The organization is on a simplified taxation regime. The following entries must be made in accounting:

| Debit | Credit | Amount, rub. | Primary document | |

| Costs for the purchase of stationery are reflected (including VAT) | 10 "Materials" | 60 “Settlements with suppliers and contractors” | 40 000 | Supplier shipping documents, Receipt order in form M-4 |

| Payment for stationery was transferred to the supplier | 60 “Settlements with suppliers and contractors” | 51 “Current account” | 40 000 | Bank account statement |

| The transfer of stationery for its intended use is reflected | 20, 25, 26,44, etc. | 10 "Materials" | 40 000 | Requirement-invoice in form M-11 |

Writing off the cost of office supplies directly as expenses, without reflecting them on account 10 “Materials”

In practice, Organizations often write off the cost of office supplies directly as expenses, without reflecting them on account 10 “Materials”. We draw your attention to the fact that this method is not correct for the following reasons: In this case, the requirements of clauses 5, 16 of PBU 5/01 are violated, according to which inventories are accepted for accounting and released into production according to established standards.

The absence of a necessary component of accounting makes it possible to qualify these transactions as incorrect reflection of transactions and material assets in the accounting accounts, which, in accordance with Article 120 of the Tax Code of the Russian Federation, is considered a gross violation of the rules for accounting for income and (or) expenses and (or) taxable items and, accordingly, entails a fine of 10,000 rubles. 30,000 rub.

A gross violation of the rules for accounting for income and expenses and objects of taxation means incorrect reflection of transactions and material assets not only in accounting accounts, but also in tax accounting registers.

In addition, problems may arise with the right to deduct “input” VAT, since, according to Art. 172 of the Tax Code of the Russian Federation, tax can be deducted after goods (work, services) are registered.

In this case, the tax authorities may come to the conclusion that the office supplies were not accepted for registration by the taxpayer and deny the Organization the right to deduct value added tax on office supplies from the budget.

![My business [CPS] RU](https://belovocity.ru/wp-content/uploads/moe-delo-cps-ru-330x140.jpg)