Liquidation commission

To make a decision on partial liquidation of a fixed asset, create a commission that should:

- determine the possibility and feasibility of restoring part of the fixed asset that is subject to liquidation;

- determine the possibility of using individual components, parts, materials of the retiring part of the fixed asset.

The commission should include the chief accountant, employees responsible for the safety of fixed assets, and other employees appointed by order of the head of the organization. The decision on partial liquidation of a fixed asset made by the commission is approved by order of the head of the organization. After the liquidation of part of the fixed asset, an act is drawn up. The commission can draw up an act on partial liquidation of a fixed asset using form No. OS-4 or No. OS-4a.

This procedure follows from paragraph 77 of the Methodological Instructions, approved by Order of the Ministry of Finance of Russia dated October 13, 2003 No. 91n.

Certificate of write-off of fixed assets

A prerequisite after all activities is the preparation of appropriate documentation. First of all, the act of writing off a fixed asset is considered, which indicates the reasons for the procedure and its consequences for the legal entity.

Leasing, as well as transfer on gratuitous terms, sale require the presence of an acceptance certificate. Wear and other reasons leading to the impossibility of operation require the existence of a liquidation act.

There is no standard form of completed documentation, but all details must be reflected without fail:

- name of the item;

- inventory number. You can learn more about the procedure for conducting an inventory of fixed assets;

- initial cost;

- the amount reached by wear;

- reasons for liquidation and lack of possibility for further exploitation;

- liquidation costs (costs of additional work for specialists, disassembly and dismantling);

- income (the cost of products that were sold or the price of materials that can be used in the future, despite the liquidation of the main facility);

- result of the procedure.

All documentation must be completed in accordance with current requirements.

Partial liquidation of the building

When a building (structure) is partially liquidated, its total area and other characteristics that were originally indicated during its state registration are reduced. For example, number of floors. Therefore, new characteristics of the building (structure) must be registered in the state register (clause 68 of the Rules, approved by order of the Ministry of Economic Development of Russia dated December 23, 2013 No. 765). In this case, the building (structure) is not re-registered, but only an entry is made in the register about changes in its characteristics.

To register changes, you need to submit to the territorial office of Rosreestr:

- application for amendments to the state register of rights to real estate and transactions with it;

- documents confirming changes in the relevant information previously entered into the state register (for example, a certificate from the BTI);

- payment order for payment of state duty in the amount of 1000 rubles. (Subclause 27, Clause 1, Article 333.33 of the Tax Code of the Russian Federation).

This is stated in paragraphs 4 and 5.1.1 of the Regulations approved by Decree of the Government of the Russian Federation dated June 1, 2009 No. 457, Section IX of the Methodological Instructions approved by Order of the Ministry of Justice of Russia dated July 1, 2002 No. 184.

Compound

The commission is needed to identify the need to write off property. Only certain people can confirm that the OS cannot be used further due to wear and tear or transfer under a contract to another owner.

The composition includes middle-level managers. For example, chief engineer. Accountants are also often members of the commission.

It is required that the composition include specialists from various fields. This will help determine the need to write off fixed assets from different points of view.

The recommended number of members is at least three people. Additionally, the head appoints a chairman.

To approve the commission, the head issues a special order.

How to issue an order for creation?

To issue an order to create a commission, you can use a regular sheet of format A - 4 or the company’s letterhead.

The document may be written by hand or printed on a computer or other printing equipment.

You cannot make mistakes or typos in the order. Otherwise, the document cannot be recognized as valid.

Also, the order is not recognized as valid without the approving signature of the head of the company.

At the top of the sheet it is indicated:

- the name of the company in which the order to create the commission is issued;

- Title of the document;

- document number, date and city of its publication;

- a short sentence about what the order is about;

- reason for publication.

Below is the word “I ORDER” and the manager’s orders are listed point by point, in particular on the creation of a commission of three people. Positions and full names are listed. members. The chairman stands out separately.

In addition to the composition of the commission, the order contains specific responsibilities of the members.

The commission is not only obliged to identify unusable operating systems, but also to establish the reason for write-off. To do this, she draws up the necessary documents. One of them is the act.

Additionally, the order approves the employee responsible for the execution of orders and familiarization of all persons specified in the document.

A separate paragraph in the order indicates a list of fixed assets that are subject to deregistration, and also indicates the time frame within which the property must be inspected.

The order contains the signature of the director and the visas of all persons designated in the order. Transcripts of signed signatures must be present.

After approval of the document, the commission can begin its immediate responsibilities: inspect the designated objects, draw up inspection reports and other accompanying documentation if necessary.

The document must comply with the basic rules for preparing business documentation.

An example of drawing up an order to appoint a commission for writing off fixed assets – word.

Responsibilities of Members

The commission approved by the head must perform the following duties:

- study and thorough inspection of assets subject to write-off;

- determining the reasons for deregistration: wear and tear, reconstruction, violation of operating rules, accident, disaster, long-term use, etc.;

- identifying whether it is possible in the future to use the property or its individual parts for its intended purpose;

- preparation of documentation directly related to the write-off of objects: technical, commercial, accounting;

- identification of those responsible for the malfunction of the fixed asset. If there are any, then involving employees in compensation for damage (a memo is drawn up addressed to the manager), the results are displayed in the property inspection report;

- compiling a list of parts of a fixed asset that can be used in the future, their evaluation;

- responsibility for dismantling individual parts of the decommissioned OS;

- drawing up a protocol for writing off fixed assets;

- execution of inspection and write-off acts (form OS-4, OS-4a, OS-4b).

Additionally, it is expected to draw up a conclusion on write-off. The form of this document is not approved at the legislative level.

Therefore, it must be filled out in any form, but with the obligatory indication of the company details.

All duties of the commission members are specifically prescribed in the order for its creation and must be carried out properly.

Accounting: partial liquidation

The organization is obliged to keep records of fixed assets according to the degree of their use:

- in operation;

- in stock (reserve);

- in the stage of partial liquidation, etc.

This is stated in paragraph 20 of the Methodological Instructions, approved by order of the Ministry of Finance of Russia dated October 13, 2003 No. 91n.

Accounting for fixed assets by degree of use can be carried out with or without reflection on account 01 (03). Thus, fixed assets that have been in the stage of partial liquidation for a long time should be accounted for in a separate subaccount “Fixed assets in the stage of partial liquidation.” This approach is consistent with paragraph 20 of the Methodological Instructions, approved by Order of the Ministry of Finance of Russia dated October 13, 2003 No. 91n.

Debit 01 (03) subaccount “Fixed assets in the stage of partial liquidation” Credit 01 (03) subaccount “Fixed assets in operation”

– work has begun on the partial liquidation of fixed assets.

Upon completion of partial liquidation, make the following entry:

Debit 01 (03) subaccount “Fixed assets in operation” Credit 01 (03) subaccount “Fixed assets in the stage of partial liquidation”

– work on the partial liquidation of fixed assets has been completed.

This procedure follows from paragraph 2 of clause 14 of PBU 6/01 and the Instructions for the chart of accounts (account 01).

How to reflect in 1C

When writing off a fixed asset item in 1C 8.2 and 8.3, you will need to carry out several basic procedures:

- calculate depreciation recorded for the last month of equipment operation;

- write off the original cost of this property to account 01.09;

- write off the total amount of depreciation that was accrued during the period of operation (also written off to the account 01.09);

- write off the difference between the original price of the property and the calculated depreciation to account 91.02).

For all these purposes, a specialized document “Write-off of OS” is created. Simply create a new document and indicate the reason for the write-off, then select the company, the write-off account and the corresponding expense item, which must be indicated in accordance with the established rules.

In addition, you will also need to indicate the relevant information in the “Location of fixed assets” section, indicating in it the division to which the written-off property belongs after it has been accepted for accounting. If this detail is left blank or the data is entered incorrectly, the program will simply generate an error and the document will not be posted.

Certificate of write-off of fixed assets

Accounting: depreciation during partial liquidation

Do not suspend depreciation on fixed assets that are in the stage of partial liquidation. There is an exception to this rule - if the liquidation of part of the fixed asset is carried out as part of reconstruction for more than 12 months (clause 23 of PBU 6/01, clause 63 of the Methodological Instructions approved by Order of the Ministry of Finance of Russia dated October 13, 2003 No. 91n). For more information about this, see How to reflect the reconstruction of fixed assets in accounting.

Upon receipt of the act of partial liquidation, adjust the value of the fixed asset (paragraph 2, clause 14 of PBU 6/01). Calculate the monthly amount of depreciation after partial liquidation based on the adjusted initial (residual) value of the fixed asset and the previous depreciation rate.

Do not revise the useful life of a fixed asset. An exception to this rule is the partial liquidation of a fixed asset carried out as part of reconstruction. Reconstruction work can lead to an increase in the useful life of the fixed asset. In this case, for accounting purposes, the remaining useful life of the reconstructed fixed asset must be revised. For more information about this, see How to reflect the reconstruction of fixed assets in accounting.

This procedure follows from paragraph 20 of PBU 6/01 and paragraph 60 of the Methodological Instructions, approved by Order of the Ministry of Finance of Russia dated October 13, 2003 No. 91n.

Situation: how to determine at the end of the partial liquidation of a fixed asset the amount by which its initial cost should be reduced and the amount of accrued depreciation?

The procedure for reducing the value of a fixed asset after its partial liquidation is not established by law. Therefore, the organization must develop it independently.

The best way is to determine the initial cost of the liquidated part of the fixed asset using accounting data. For example, if in the primary documents submitted by the supplier when purchasing a fixed asset, the cost of the liquidated part is highlighted as a separate line, in this case the amount of depreciation charges attributable to the liquidated part can be calculated using the formula:

| Depreciation charges attributable to the liquidated part of the fixed asset | = | Initial cost of the liquidated part of the fixed asset | : | Initial cost of the entire fixed asset | × | Accrued depreciation at the end of liquidation |

If it is impossible to determine the initial cost of the liquidated part of the fixed asset based on accounting data, it can be calculated:

- a commission created from employees of the organization;

- independent appraiser.

In this case, the share of liquidated property must be determined as a percentage of any physical indicator characterizing the fixed asset. Taking into account this share, the cost and amount of depreciation attributable to the liquidated property are calculated.

For example, for buildings (structures), the initial cost and depreciation charges attributable to the liquidated part can be determined by calculation:

| Initial cost attributable to the liquidated part of the building (structure) | = | Area of the liquidated part of the building (structure) | : | Total area of the building (structure) before liquidation | × | Initial cost of the building (structure) |

| Depreciation charges attributable to the liquidated part of the building (structure) | = | Area of the liquidated part of the building (structure) | : | Total area of the building (structure) before liquidation | × | Accrued depreciation at the end of liquidation |

The applied option for adjusting the initial cost and the amount of accrued depreciation after partial liquidation of a fixed asset should be fixed in the accounting policy for accounting and tax purposes.

After partial liquidation, depreciation on the fixed asset continues to be calculated based on its value adjusted to the cost of the liquidated part.

This procedure is confirmed by letter of the Ministry of Finance of Russia dated August 27, 2008 No. 03-03-06/1/479. Although this letter contains references to the old version of the Tax Code of the Russian Federation, the conclusions drawn in it can still be applied now, as amended by the current rules of law.

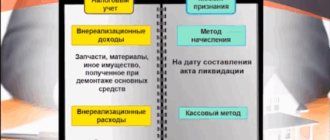

The amount of underaccrued depreciation on fixed assets subject to partial liquidation, with linear depreciation, can be included in non-operating expenses. With the non-linear method, it is not possible to write off amounts at a time. Recently, officials explained all these issues in detail. Partial liquidation means the disposal of part of a fixed asset from its composition. A fixed asset will not lose its properties upon disposal of any part of it if it is a complex of structurally articulated objects *(1). This could be a building, a machine, a car, a computer and other similar objects.

Not a complete disposal of a fixed asset, but the withdrawal of a part of it is possible if: - its disassembly does not affect the economic feasibility of use; — disassembly does not prevent it from being used for its original purpose; — the functional purpose of the retiring part is not an integral part; — the object continues to function as a single separate complex.

Note that when accounting for the fact of economic life, the partial liquidation of a fixed asset should be distinguished from the disposal of part of it due to repair or reconstruction (modernization). When repairing property, a part that has become unusable during use is replaced with a new one of the same type.

The accounting life of the fixed asset after repair does not change, as well as its residual value; depreciation continues to be accrued in the current order. The cost of the old spare part is charged to current expenses, and the new one continues to function as part of the fixed asset.

During reconstruction (modernization), the retired part is replaced with a new one, not similar to the old one. It has fundamentally new characteristics that improve the operation of the fixed asset and give it new properties * (2). And the residual value of the fixed asset, as a rule, increases. Depreciation is calculated taking into account the changed value and useful life.

In case of partial liquidation, the disposed part of the fixed asset is not replaced by anything.

This happens when there is no demand for the use of such a part in the complex of a particular object and under certain operating conditions. For example, an unused porch of a building was dismantled, components and parts of a machine that were not needed were removed, or an unused webcam was disconnected from the computer. In case of partial liquidation of a fixed asset, parts, assemblies, assemblies and other items or materials can be used in the further economic life of the company, if they are suitable. In this case, the accountant should accept them for accounting and reflect income at the current market value of the received accounting items *(3).

Documentation of partial liquidation

To document partial liquidation, employees of the financial department recommend creating a commission. She is appointed by order of the head of the organization. The commission should include competent specialists, the chief accountant and employees responsible for the safety of fixed assets in the company.

During public consultations, tax officials strongly recommend including technical specialists in the commission, on whose knowledge both the accountant and the tax inspector can rely. The role of the chief accountant, in our opinion, in assessing the condition of a fixed asset is not decisive and comes down to control over the execution of documents. The chief accountant can also assess the economic feasibility of operating a fixed asset after part of it has been disposed of, but even in this case he will need the advice of a technical expert. Employees responsible for storing fixed assets do not necessarily have to be financially responsible persons. The list of jobs and categories of employees is approved by the Government of the Russian Federation. The manager, in agreement with the chief accountant, within the framework of the internal control system, can appoint responsible persons from among the company’s employees who monitor the provision of proper storage conditions, the provision of information on internal movement and changes in the status of fixed assets. It is enough to issue an order or instruction. The regulation on the procedure for accounting for fixed assets, approved by the manager, can also determine the responsibility of the employee within the framework of his official duties.

The competence of the commission includes:

— inspection of an object subject to write-off; — use of the necessary technical documentation to assess the technical feasibility of disposing of part of the fixed asset; — use of accounting data to assess the economic feasibility of writing off part of a fixed asset and its further operation; — determination of the share of the liquidated part of the fixed asset as a percentage of the cost of the depreciable object; — establishing the reasons for writing off fixed assets; — the possibility of using individual components, parts, materials of retired fixed assets and their assessment based on the current market value; — drawing up an act for writing off part of the object.

The act contains the following information:

— date of acceptance of the object for accounting; — year of manufacture, time of commissioning; — useful life; — initial cost and amount of accrued depreciation; — revaluations and repairs carried out; — reasons for departure with their justification; — condition of the main parts, parts, assemblies, structural elements; — the share of the liquidated part of the fixed asset in percentage and monetary terms.

The act of writing off fixed assets is approved by the head of the company. There is no unified primary document for registering the partial liquidation of a fixed asset. In our opinion, to document this operation, you can use the act of writing off a fixed asset item (form N OS-4, form N OS-4, KS-10KS-10 - for buildings).

Underaccrued depreciation

Recently, officials from the financial department clarified the procedure for reflecting in tax accounting expenses for depreciation of fixed assets during partial liquidation * (4).

The essence of the answer boils down to the following: - with the linear method, the amount of underaccrued depreciation on the liquidated part of the fixed asset is included in non-operating expenses as other reasonable expenses * (5); — with the non-linear method of writing off an object, the company cannot simultaneously take into account the residual value of the liquidated part as part of expenses. The cost of the object will continue to be depreciated as part of the total balance of the depreciation group to which the object was included * (6).

Additional liquidation costs

During the liquidation of property, costs may arise associated with dismantling, disassembly, loading, expert assessment, and others. These expenses do not increase the cost of the fixed asset, but are included in non-operating expenses, as well as underaccrued depreciation * (7).

This is explained by the fact that the fixed asset continues to be used, and only part of it is retired. Let us recall that, as a general rule, when disposing of fixed assets, additional expenses are taken into account as non-operating expenses for liquidation * (8).

The initial cost of a fixed asset can be increased by the amount of additional expenses only in the case of the acquisition or creation of depreciable property, completion, additional equipment, reconstruction, modernization, technical re-equipment. The list of situations in which the initial cost increases is given in paragraph 5 of Article 270, paragraph 5 of Article 270 of the Tax Code and is closed. The fact of partial liquidation of a fixed asset is not indicated in the list.

Thus, in the case of partial liquidation, tax legislation provides only one option for accounting for additional expenses, namely as part of non-operating expenses as other reasonable expenses.

Accounting

In accounting, partial liquidation is one of the special cases of disposal of fixed assets and is reflected in accounting in the general manner under account 01, account 01 “Fixed assets” using subaccount 01 “Disposal of fixed assets”. Depreciation is accounted for in account 02, account 02. Expenses in the amount of underaccrued depreciation are reflected as other expenses in account 91-2account 91-2.

Example The initial cost of a machine is 600,000 rubles, accrued depreciation is 400,000 rubles, the residual value is 200,000 rubles. According to the commission's conclusion, the share of the liquidated part of the fixed asset was 10%. Taking into account the share, the initial cost of the liquidated part is 60,000 rubles, the residual value is 20,000 rubles, accrued depreciation is 40,000 rubles.

Debit 0101 subaccount “Disposal of fixed assets” Credit 01-01 - 60,000 rubles. — the disposal of the part being liquidated is reflected; Debit 02-0102-01 Credit 0101 subaccount “Disposal of fixed assets” - 40,000 rubles. — the write-off of depreciation of the liquidated part is reflected; Debit 91-0291-02 Credit 0101 subaccount “Disposal of fixed assets” - 20,000 rubles. — the residual value of the liquidated part is written off as expenses.

Depreciation relating to the part of the fixed asset remaining in operation, both in accounting and tax accounting, is accrued at the rates determined before the moment of partial liquidation. The moment of partial liquidation can be considered the date of approval by the manager of the act on disposal of part of the fixed asset.

With the straight-line depreciation method, the amount of monthly depreciation expenses for the remaining part of the fixed asset will decrease in proportion to the share of partial liquidation determined by the commission. This rule is true for both accounting and tax accounting. Depreciation on an item of fixed assets should be calculated from the 1st day of the month following the month of completion of its partial liquidation until the cost of this item is fully repaid or it is written off from accounting.

With the non-linear method of calculating depreciation, the amount of monthly depreciation expenses in tax accounting will not change. The cost of the object in full (including the liquidated part) will continue to be depreciated as part of the total balance sheet of the depreciation group to which this object was included before the liquidation of its part * (9).

If the cost of the remaining part does not exceed 40,000 rubles, depreciation on such an object is calculated in accounting and tax accounting until its cost is completely written off as expenses. The accounting rules do not provide grounds for subsequent reclassification of already capitalized assets. If an asset has been accepted for accounting as a fixed asset, it must continue to be accounted for in the same capacity until the end of its operation *(10).

Let us note the situation related to the depreciation bonus taken into account when purchasing a fixed asset. In our opinion, it does not need to be restored. Tax Code The Tax Code prescribes its restoration only if the fixed asset is sold earlier than five years from the date of its commissioning * (11). But in this case there is no implementation. This position is confirmed by employees of the financial department * (12).

Accounting: cost adjustment

In accounting, reflect the adjustment in the value of a fixed asset after its partial liquidation with the following entries:

Debit 01 (03) subaccount “Retirement of fixed assets” Credit 01 (03) subaccount “Fixed assets in operation”

– the initial (replacement) cost of the liquidated part of the fixed asset is taken into account;

Debit 02 Credit 01 (03) subaccount “Disposal of fixed assets”

– the amount of depreciation charges attributable to the liquidated part of the fixed asset is written off;

Debit 91-2 Credit 01 (03) subaccount “Disposal of fixed assets”

– the residual value of the liquidated part of the fixed asset is written off.

This procedure follows from the Instructions for the chart of accounts (account 01).

The amount by which the initial value of the fixed asset was adjusted after partial liquidation is reflected in the inventory record card in form No. OS-6 (No. OS-6a) or in the inventory book in form No. OS-6b (used by small enterprises).

The procedure for writing off fixed assets

The procedure can only be performed in certain situations.

Regardless of the reason, the procedure for writing off fixed assets must be followed.

It should be noted that the movement of any type of property between different structures of one organization does not constitute a disposal.

See this article about the procedure for calculating and calculating depreciation of fixed assets.

In addition, upon completion of the operation of the property due to reconstruction or installation of additional equipment, the fact that the item has been removed from the account does not occur.

If the value of the object is lost or the property cannot guarantee income for the enterprise, evidence of changes in a certain part of the accounting must occur.

The event that occurs must be reflected in the income and expenses of the enterprise.

Focusing on the debit of account 91, it is necessary to reflect that the residual value of the equipment has been disposed of, as well as all subsequent expenses due to the procedure.

In this case, the loan must take into account the amount of depreciation, possible income from the sale of property or renting it out.

In order for the necessary procedure to be carried out legally, you should open not only account 01, but also a sub-account that will perform a certain task immediately.

Account 99 “Profits and losses” should be a direct reflection of all expenses of the enterprise.

In this case, income, as well as expenses after the event regarding the written-off property has been completed, should be reflected in the reporting documentation.