The emergence of the need for accounting

The need to keep records of work records does not arise if the employee brings the form for storage at the personnel authority. After employment, a corresponding entry is made in the document with subsequent registration in the accounting journal. In this case, actions are limited to personnel records.

The need for accounting arises when an employee is employed without experience or there is no space in the book to enter text about hiring or dismissal. When maintaining records, a record of transactions accompanying the actions is made:

- Purchase of work books by the enterprise.

- Registration of documents.

- Issuance of the document to the employee.

- Acceptance of a fee equal to the cost of the enterprise's purchase.

A new document is issued after the employee applies to the manager with an application. According to Art. 65 of the Labor Code of the Russian Federation, an organization or individual entrepreneur is required to provide a new form or insert if it is missing or lost by the employee.

You must receive compensation for the provision of your work book. The refusal of the recipient of the document to pay the expenses of the organization or individual entrepreneur for the purchase of the form is not grounds for refusal to issue it. All actions related to the purchase, accounting, and write-off of documents are accompanied by accounting records.

Options for recording work records

According to clause 42 of the Rules for maintaining and storing work books, producing work book forms and providing employers with them, the work book forms and inserts in it are stored in the organization as strict reporting documents, as a result of which the work book form and the insert in it are accepted for accounting as a form strict reporting.

After the work book is issued to the employee, the employee’s debt to the employer, equal to the cost of the work book form, is taken into account.

The letter of the Ministry of Finance of the Russian Federation dated May 19, 2017 No. 03-03-06/1/30818 contains information provided by the Department of Tax and Customs Policy, which states that:

- operations involving the issuance by an employer of work books or inserts in them to employees, including the cost of their acquisition, are operations for the sale of goods and, accordingly, are subject to taxation with value added tax;

- the fee charged to the employee for the provision of work books or inserts in them is subject to corporate income tax in the generally established manner.

Basic norms in document flow

At enterprises, work books are recorded as strict reporting forms (SSR). Despite the prevalence of the document in retail, the only legal way to purchase is to purchase BSO forms from legal representatives of Goznak. The enterprise was organized on the basis of a federal institution and has been a joint-stock company since 2014. The company produces products marked with state marks, including work books.

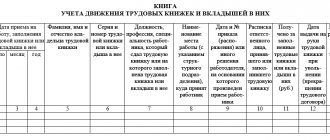

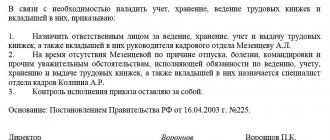

In the document flow, responsible persons are guided by the Rules approved by GD dated March 16, 2003 No. 225 (hereinafter referred to as the Rules). To make entries, a journal is used - a receipt and expenditure book for recording forms and inserts.

Sample accounting book 2021

Registration of pension

To apply for a pension, the employee will need the original work book. It is the work book that is the main document confirming the period of work under an employment contract (clause 11 of the Rules, approved by Decree of the Government of the Russian Federation of October 2, 2014 No. 1015).

The employer is obliged to issue the original work book no later than three working days from the day the employee submits the relevant application. In this case, a maximum of three working days after receiving the work book at the Pension Fund branch, the person will have to return the document to the organization. This is stated in Article 62 of the Labor Code of the Russian Federation.

Procedure for maintaining the accounting book

Enterprise managers appoint persons responsible for maintaining the journal. The movement of documents is carried out in the company's accounting department.

When maintaining records, the procedure established by the Rules is applied: (click to expand)

- The magazine sheets are numbered and stitched with thread. The tabular part of the document after stapling must be accessible for writing and reading or photocopying.

- A seal is installed on the firmware indicating standard text about the number of sheets, the name of the enterprise and information about the certifying person. The entry must be certified by the signature of the director or a substitute person in accordance with the order.

- Records of the movement of forms or inserts are made in the book. Documents are issued to the personnel officer responsible for maintaining work records.

- Records are kept for each document indicating the series and number.

At the end of each monthly period, the responsible person must provide a report on the movement of books, the quantity at the beginning and end of the period, and whether they are registered. Additionally, indicate the amount of funds received to compensate for the costs of the enterprise.

Commercial companies and budgetary organizations are required to have a sufficient number of forms registered to meet the needs of employed persons (

Responsibility

For the absence of labor records or their incorrect registration, the labor inspectorate may fine the organization (entrepreneur) and its officials.

In this case, the amount of the fine will be:

- for officials (for example, a manager) – from 1000 to 5000 rubles;

- for an entrepreneur – from 1000 to 5000 rubles;

- for an organization – from 30,000 to 50,000 rubles.

And for repeated violation you face the following:

- for a manager (official) – a fine in the amount of 10,000 to 20,000 rubles. or disqualification for a period of one to three years;

- for an entrepreneur – a fine in the amount of 10,000 to 20,000 rubles;

- for an organization – a fine in the amount of 50,000 to 70,000 rubles.

Such measures of liability are provided for in parts 1 and 4 of Article 5.27 of the Code of the Russian Federation on Administrative Offenses.

Accounting entries when purchasing forms

Accounting for transactions for the purchase of work books is carried out using account 76 when purchasing by bank transfer. When registering, you must have an invoice issued by the seller. Work books purchased by an enterprise cannot be classified as goods. The reason is that the document is not intended for further resale.

Accounting for the movement of forms is mainly carried out by entries on account 10. A number of enterprises use account 41, which does not correspond to the position that there are no signs of the goods. When registering, an entry is simultaneously made to account 006, intended for accounting for BSO. Off-balance sheet accounting allows you to have information about the presence of the required number of documents on record.

| Purpose of the operation | Account debit | Account credit |

| Payment for forms has been made | 60 (76) | 51 |

| Posting of forms is reflected | 10 | 60 (76) |

| VAT from the supplier is included | 19 | 60 (76) |

| Forms accepted for off-balance sheet accounting | 006 |

In the future, when accounting for the movement of the form and funds to pay the cost, account 73 is used, to which subaccount 3 “Payments for work books” is opened.

Issuing a form to an employee without experience or an insert for it

In connection with the transfer of ownership from the employer to the employee, a VAT tax base arises. The tax billed by the supplier is deductible. The obligation to pay tax does not arise if the enterprise is not a VAT payer. The moment the VAT base arises is the day the work book is opened.

Example of issuing a form ⇓

The company Novost LLC hired employee V. without work experience. The acquisition cost after VAT was 100 rubles. The following entries were made in the accounting of Novost LLC:

- The cost of the completed form is included in the expenses: Dt 91/2 Kt 10 in the amount of 100 rubles;

- The accrual of VAT is reflected: Dt 91/2 Kt 68/1 in the amount of 18 rubles;

- The form was written off based on the certificate: Kt 006 in the amount of 100 rubles;

- The cost of the form is reflected in income: Dt 73/3 Kt 91/1 in the amount of 118 rubles;

- The amount of debt is withheld when calculating wages at the request of the person: Dt 70 Kt 73/3 in the amount of 118 rubles.

The moment of accounting for enterprise expenses is determined when costs arise - the purchase of forms. The amount of payment for the forms received is taken into account as part of income when a debt arises to the enterprise.

Accounting for cash receipts

Enterprises must receive compensation for the cost of the document - the amount spent on its acquisition. The amount of the fee should not exceed the purchase price (excluding VAT). The possibility of receiving payment is provided for in clause 47 of the Rules. Despite the fact that the presentation of the work book is the responsibility of the company, the amount deposited by the employee into the cash register of the enterprise can be considered as revenue, the receipt of which requires the use of cash register equipment.

To avoid controversial issues with the tax office, the best option is to withhold the amount when calculating the employee’s wages. Withholding is carried out at the request of a person sent to the manager or chief accountant.

No deduction is made without the employee's consent: (click to expand)

| Purpose of the operation | Account debit | Account credit |

| Receipt of payment for the provided form at the cash desk is reflected | 50 | 73/3 |

| Deduction of the cost of the form from the payslip is reflected | 70 | 73/3 |

| Income from the fee received is reflected | 73/3 | 91/1 |

If an employee refuses to pay the amount spent by the employer on the purchase of a work book, the cost is written off from the company’s funds. The amount is reflected in other expenses of the enterprise.

Accounting for books provided free of charge

Free issuance of forms to employees occurs in the event of mass loss of books during storage at the enterprise or damage to the document due to the fault of the person in charge. In these cases, the company is obliged to provide forms to employed employees with no experience or in the absence of unfilled sheets free of charge. Legislative norms do not establish restrictions on the free issuance of work books and their inserts. When completing the procedure, the following features arise:

- To justify actions to issue forms free of charge, an order is issued.

- The procedure must be included in a local act, for example, a collective agreement.

- In calculating the base when calculating profits and the single tax, the costs of purchasing forms issued free of charge are not included. The cost of the issued book is subject to VAT; the seller's tax is not deductible.

Forms issued free of charge must be subject to personal income tax to the employee as income received. You can exclude taxation if you register 4,000 rubles as a non-taxable amount. If the form is issued in the form of a gift, the obligation to tax the amount does not arise (

Accounting and taxes

Situation: how can an organization take into account the acquisition and issuance of a new work book to an employee under the general regime?

The procedure for accounting and taxation of transactions related to the provision of work books to employees is not regulated by law.

The right of an organization to charge an employee a fee for issuing a work book is provided for in paragraph 47 of the Rules, approved by Decree of the Government of the Russian Federation of April 16, 2003 No. 225.

In accounting, the cost of purchased work books can be taken into account as part of:

- materials on account 10 of the same name (as assets used for management needs (clause 2 of PBU 5/01)) with subsequent write-off to other expenses;

- goods on account 41 “Goods”.

A more correct way of reflection is to take books into account as materials. The fact is that the sale of work books for ordinary organizations is not the main activity. Organizations provide themselves with such forms on a contractual basis for a fee (clause 46 of the Rules, approved by Decree of the Government of the Russian Federation of April 16, 2003 No. 225). In this case, work record forms can be purchased directly from the Goznak association, as well as from distributors that meet the requirements of this association (clauses 2 and 3 of the Procedure approved by Order of the Ministry of Finance of Russia dated December 22, 2003 No. 117n).

Therefore, account 41, which summarizes information on the availability and movement of inventory items purchased as goods for sale, and account 90 “Sales,” which summarizes information on income and expenses associated with ordinary activities, are more convenient to use for distributors of labor books.

Other organizations that purchase forms of work books and inserts for them for their own needs (for subsequent issuance to employees) can account for these forms in account 10.

Simultaneously with the posting of work record forms, reflect on account 006 “Strict reporting forms” in conditional valuation (clause 42 of the Rules approved by Decree of the Government of the Russian Federation of April 16, 2003 No. 225).

When you receive the forms, please make the following notes:

Debit 10 Credit 60 – work books have been capitalized;

Debit 19 Credit 60 – reflects the amount of VAT presented by the supplier;

Debit 68 subaccount “Calculations for VAT” Credit 19 – the amount of VAT presented by the supplier is accepted for deduction;

Debit 006 – work record book forms are accepted for accounting.

If an organization charges a fee for issuing work books, the transaction is reflected in account 73 “Settlements with personnel for other transactions.” If an organization deducts payment for a work book form from an employee’s salary, use account 70 “Settlements with personnel for wages”.

The issuance of work books and their inserts to employees of the organization is recognized as the sale of goods. Therefore, VAT must be paid on such a transaction. This conclusion follows from the provisions of subparagraph 1 of paragraph 1 of Article 146 of the Tax Code of the Russian Federation and is confirmed in letters of the Ministry of Finance of Russia dated September 30, 2015 No. 03-07-11/55714, Federal Tax Service of Russia dated June 23, 2015 No. GD-4-3/ [email protected] In this case, the employee pays the organization the cost of the work book including VAT (letters of the Ministry of Finance of Russia dated September 26, 2007 No. 07-05-06/242 and dated June 13, 2007 No. 03-07-11/159).

In accounting, operations for issuing work books and their inserts to employees and receiving payment for the forms are reflected in the following entries:

Debit 50 (51, 70) Credit 73 – the cost of the issued work book was reimbursed (including VAT);

Debit 73 Credit 91-1 – income is recognized in the amount of payment received for the work book form (including VAT);

Debit 91-2 Credit 68 subaccount “Calculations for VAT” - VAT is charged on the reimbursement of the cost (sale) of a work book by an employee (if the organization is a tax payer);

Debit 91-2 Credit 10 – the cost of work books transferred to an employee of the organization is written off.

When transferring work books and their inserts to employees free of charge, make the following entries in accounting:

Debit 91-2 Credit 10 – the cost of work books transferred free of charge is written off;

Debit 91-2 Credit 68 subaccount “Calculations for VAT” - VAT is charged on the free transfer of work books to employees (if the organization is a tax payer).

You can write off the work book form (the insert for it) on the day it is issued to the employee. In this case, the date of issue should be considered not the day of dismissal of the employee, but the day when the work book is opened on the basis of Part 4 of Article 65 of the Labor Code of the Russian Federation.

Credit 006 – forms of work books (inserts for them) have been written off.

Advice: there are arguments that allow an organization not to pay VAT on the issuance of a work book (its insert) to an employee. They are as follows.

Firstly, the work book (the insert for it) does not have the characteristics of the goods defined in paragraph 2 of PBU 5/01 and article 38 of the Tax Code of the Russian Federation.

Secondly, providing work books to employees who do not have work experience is the responsibility of the organization established by labor legislation (Part 4 of Article 65 of the Labor Code of the Russian Federation).

Thirdly, the amount of payment for the form charged to an employee should not exceed the amount of costs for its acquisition (clause 47 of the Rules, approved by Decree of the Government of the Russian Federation of April 16, 2003 No. 225).

Since, by issuing work books to employees, the organization does not pursue the goal of making a profit, such operations cannot be considered as entrepreneurial activity (sale of goods, work, services) (Article 2 of the Civil Code of the Russian Federation). A similar point of view is reflected in the decisions of the Federal Antimonopoly Service of the North-Western District dated October 1, 2003 No. A26-5317/02-28 and dated March 2, 2007 No. A56-44214/2006. Consequently, the issuance of work books (free of charge or for a fee) is not a sale. This means that such an operation is not subject to VAT (subclause 1, clause 1, article 146 of the Tax Code of the Russian Federation).

If, when filling out, you spoiled the work book form (the insert for it), make the following entries in accounting:

Debit 91-2 Credit 10 – the cost of damaged work books has been written off;

Debit 19 Credit 68 subaccount “Calculations for VAT” – VAT previously accepted for deduction has been restored;

Debit 91-2 Credit 19 – the restored amount of VAT is written off;

Credit 006 – forms of damaged work books (inserts for them) have been written off.

When calculating income tax, the costs of purchasing forms of work books (inserts for them) can be taken into account. Such costs are economically justified and are associated with activities aimed at generating income (clause 1 of Article 252 of the Tax Code of the Russian Federation, letters of the Ministry of Finance of Russia dated September 26, 2007 No. 07-05-06/242, Federal Tax Service of Russia dated June 23, 2015 No. GD-4-3/ [email protected] ). These expenses reduce the tax base for income tax at the time of issuing a work book (insert to it) to an employee of the organization (clause 2 of Article 318 of the Tax Code of the Russian Federation).

Include the amount of reimbursement by the employee for the issuance of a work book as part of income subject to taxation.

If the amount of compensation is equal to the cost of the organization to purchase the form, the profit is zero. Consequently, the organization does not pay income tax (Article 247 of the Tax Code of the Russian Federation).

If an organization does not charge an employee for a work book form (for example, in the case of mass loss of books, damage or incorrect initial filling), it will not be able to take into account when calculating income tax either the costs of its acquisition or the VAT accrued on the gratuitous transfer ( Clause 16, Article 270 of the Tax Code of the Russian Federation). As a result, due to differences between accounting and tax accounting, a constant difference is formed, with which the permanent tax liability must be calculated (clauses 4 and 7 of PBU 18/02):

Debit 99 Credit 68 subaccount “Calculations for income tax” - reflects the permanent tax liability.

In addition, when transferring a form free of charge, personal income tax must be withheld from an employee (Article 1, 226 of the Tax Code of the Russian Federation). Its market value is recognized as the employee’s income (clause 1 of Article 210, subclause 1 of clause 2 of Article 211 of the Tax Code of the Russian Federation). This is confirmed by the Russian Ministry of Finance in a letter dated November 27, 2008 No. 03-07-11/367.