Business trip expenses: what the employer pays for

When sending an employee to perform work functions in another locality in Russia, at the company’s expense it is necessary:

- purchase travel tickets, regardless of the type of transport. The only exception is a taxi - a trip in it, as a rule, is not compensated;

- pay for housing - this could be a hotel room or rental housing, provided that there are documents proving the corresponding expenses;

- issue daily allowances - they are calculated for each day of a business trip, including each day when the employee was on the way to another location and back. The exception is for one-day trips - if in the morning the employee went to another locality to fulfill the received official assignment, and returned in the evening (before 12 o'clock at night). No daily allowance is paid for them;

- other expenses, as agreed with management. For example, an organization’s internal documents may provide for compensation for entertainment expenses, costs for renting a car and/or a personal driver, for the services of VIP lounges at airports, communication services, and other issues.

As for trips abroad, the employer is also responsible for paying consular fees, issuing money for a visa, paying for insurance, and paying other mandatory payments when crossing the border.

In addition, the employer is obliged to maintain the posted employee’s salary, since in fact the person performs his work duties outside the organization. In this case, the salary is paid for each day of the business trip, including the days when the employee was on the road.

According to the general rules, if documents confirming expenses during a trip are presented, then they can be fully taken into account when calculating income tax or tax on the simplified tax system.

How much is the employee reimbursed?

It often happens that the purchase of tickets and booking a hotel room is handled directly by the company administration, which means that the employee does not receive money for this. And there are no questions with them. But if money for travel expenses is given to a person, then you need to understand what standards are used to reimburse them.

By law, travel expenses allow an employee to get to their destination, buy food, pay for accommodation, and afford other things previously agreed upon with the head of the company. And since the person went to perform an official assignment, he should be compensated for all expenses incurred and agreed upon with his superiors, and not consider the amount issued as income. That is, neither income tax nor insurance premiums are withheld from them. But this is provided that the company has approved a regulatory document (regulations on business trips), which provides for compensation standards, as well as the procedure for this procedure.

The only expense item that is standardized at the legislative level is the amount of daily allowance. In particular, the Tax Code of the Russian Federation states that daily allowances issued in the following amounts are not subject to personal income tax and insurance contributions:

- 700 rubles - per day of travel around the country;

- 2500 rubles - per day of a business trip abroad.

This does not mean that the employer cannot pay more. Maybe. But in this case, the company will have to withhold income tax and insurance premiums from the excess amount.

We also note that the subordinate is not required to report on what he spent the daily allowance on and whether he spent it at all. This is the item of travel expenses that is taken into account when taxing company profits without documents confirming that the money was spent.

Daily allowance abroad and in Russia: sizes

Since almost all travel expenses abroad and within the country can be taken into account when taxing company profits in full, we will dwell in more detail only on daily allowances, for which a personal income tax-free limit has been introduced.

About 5 years ago, the government required employers to provide employees with travel expenses that were no less than specified minimum amounts. But then they abandoned this, maintaining the standards only for state delegations. According to Government Decree No. 729 dated October 2, 2002, each federal civil servant is entitled to no more than 100 rubles per day if he goes on a business trip around the country. If you have to perform duties outside the Russian Federation, then the daily allowance is 50-70 dollars, depending on the specific country (Appendix No. 1 to Government Resolution No. 812 of December 26, 2005). Please note that these standards are not mandatory for employees of regional government agencies, local governments, and municipal institutions. For them, allowable travel expenses are determined locally.

As for private enterprises, the managers of such companies themselves decide what the daily allowance should be. But the majority tries to comply with the norms that are not subject to personal income tax and insurance contributions: no more than 700 rubles per day when traveling within Russia and up to 2,500 rubles outside its borders. Let us repeat: no one forbids giving more, it’s just that you will have to pay tax (Article 217 of the Tax Code of the Russian Federation) and insurance premiums (Article 422 of the Tax Code of the Russian Federation) on the excess amount. Please also note that for persons occupying different positions and specialties, different daily allowance rates may be established. But this must be stated in the organization’s regulatory document.

Please note that daily allowances are paid for each day of a business trip, for days en route and for periods of forced downtime. However, they do not replace wages; the employer is obliged to pay the average wage while the employee works in another locality.

Personnel support for business trips

A business trip is a trip by an employee by order of the employer for a certain period of time to carry out an official assignment outside the place of permanent work (Article 166 of the Labor Code of the Russian Federation). If an employee is on a business trip, his average earnings and his place of work are retained. Registration of business trips is stipulated in the Instruction of the Ministry of Finance of the USSR, the State Committee for Labor of the USSR and the All-Union Central Council of Trade Unions dated April 7, 1988 No. 62 “On official business trips within the USSR”.

| Accounting for individual entrepreneurs and LLCs Cost: 10,000 - 12,000 rubles. (all inclusive)

|

According to this instruction, when sending an employee on a business trip, the head of the department to which the employee belongs (his immediate supervisor) fills out for him a “Work assignment for sending on a business trip and a report on its implementation,” which indicates the purpose of the business trip, the tasks that need to be solved during of this trip, the name of the company to which the employee is being sent, the date of the trip. The “job assignment” in form No. T-10a must be approved by the head of the company. Then, based on this document, the personnel officer draws up a “Travel Certificate” in form No. T-10. Which indicates the name of the company, the city to which the employee is traveling, as well as the dates of the business trip. According to these dates, the employee makes a note in his company’s HR department that he is leaving on the day he is sent on a business trip, upon arrival at the place of business trip, the employee notes the date of arrival in the company’s HR department, then on the day of departure he makes a note that he is leaving the place of business trip and on The day of arrival at his workplace in his company makes the last mark for him - the day of arrival. All marks must be confirmed by the signatures and seals of officials. The validity of expenses incurred on a business trip and reimbursed by the company is confirmed by relevant documents, including a travel certificate.

After completing the official assignment and travel certificate, the employee goes to the accounting department, where he is given an advance for daily expenses, travel, accommodation, as well as expenses that the employer is willing to pay at the expense of the company. All these nuances can be approved in the internal local act of the company or in the regulations on remuneration. Daily allowances within the limits of the norms, the amount of which will not be subject to taxes such as personal income tax and insurance premiums are established in clause 3 of Art. 217 of the Tax Code of the Russian Federation in the amount of 700 rubles per day for the time spent on a business trip in the territory of the Russian Federation, 2,500 rubles per day for the time spent on a business trip abroad. Daily allowances are calculated for each day you are on a business trip, including holidays and weekends.

How are travel expenses compensated for a one-day business trip?

Sometimes subordinates are sent on short business trips lasting one day, or even several hours. In this case, the company compensates travel expenses for transport, as well as for other purposes, if agreed upon.

However, in this case, daily allowances are not paid if the employee travels to another locality in the Russian Federation. In return, he may be paid compensation, but its amount is specified in the company’s internal documents. And if the employer is a budgetary institution, then in the regulations of the government or other authorities.

As for foreign one-day business trips, both for private companies and for the public sector there is a daily allowance limit of half the prescribed norm. This was stated in paragraph 20 of the Decree of the Government of the Russian Federation of October 13, 2008 No. 749 and paragraph 30 of the Decree of the President of the Russian Federation of July 18, 2005 No. 813.

In addition, amounts spent on rental housing are not reimbursed, since there is no need to stop somewhere on one-day business trips. However, in exceptional cases, when objective reasons force the employee to spend some time in a hotel, the company will also have to pay for accommodation.

Let us note right away that during a one-day business trip, the employer is still obliged to pay the employee the average salary. But if a business trip falls on a weekend or holiday, then payment must be made in accordance with Art. 153 of the Labor Code of the Russian Federation, in double size. Or the employee can receive an additional day off (time off) and pay in a single amount.

Accounting for travel expenses

The procedure for registering a business trip is regulated by the Labor Code of the Russian Federation, the Tax Code of the Russian Federation, and other by-laws and documents are also in effect, in particular, the Regulations on the specifics of sending employees on business trips.

The employer reimburses the employee for the expenses incurred by him in the process of performing the task assigned to him, these expenses include the so-called daily allowance (a fixed amount of money per day, which is paid in connection with living outside the permanent place of residence and compensates for additional expenses associated with the business trip) , as well as all other expenses incurred by the employee and confirmed by relevant documents (accommodation, transportation costs and other expenses permitted by the employer). This is stated in Article 168 of the Labor Code of the Russian Federation.

The procedure and amount of reimbursement of travel expenses is regulated either by a collective agreement or other local regulations.

When sending an employee on a business trip, he is given a certain amount of money in advance; upon returning, the employee provides an advance report on the actual amounts spent with supporting documents, the balance of the advance is handed over to the cashier, but if the amount was spent in excess of the advance issued, then the employee is paid additional money spent in excess of the amount issued advance

Travel expenses can only be taken into account if supporting documents are available.

Daily allowance: a travel certificate serves as a supporting document. The actual amount of daily allowance that the organization will pay is determined by local acts of the organization or a collective agreement; their minimum and maximum amount is not limited and is established by the organization independently. Daily personal income tax is not subject to personal income tax within the permissible limits. Acceptable norms - 700 rubles. per day for business trips in Russia and 2500 rubles. per day for business trips abroad. If an organization, by its internal local act, establishes daily allowances in excess of the specified maximum values, then the value is above 700 and 2500 rubles. subject to personal income tax.

It is worth noting that clause 11 of the Regulations on the specifics of sending on a business trip stipulates that if for any reason an employee has the opportunity to return to his place of residence every day, then he is not paid per diem.

Travel expenses for transport: this includes payment for travel on public transport and a taxi to the place of embarkation for departure on a business trip, the travel itself to the appointed place and back, and the cost of public transport at the place of business trip. The Ministry of Finance also provides the opportunity to take into account as expenses for a business trip and rental of transport for moving to the place of business trip, to the place of business trip and back. Supporting documents here are tickets, travel documents, in the case of renting a vehicle - a rental agreement and documents confirming the fact of payment in cash or non-cash.

Travel expenses for accommodation: if payment for a hotel is made non-cash, then the supporting documents are an act, an invoice, a hotel check, if in cash, then a hotel check and a fiscal check. If the room is booked in advance and this service is paid, the cost of the reservation is also included in travel expenses. Additional hotel services related to room service, meals in a restaurant, health procedures used by the business traveler are not taken into account as business trip costs (sauna, gym, swimming pool, room service, porter services, etc.).

If a residential premises or apartment is rented for living, then the supporting document can be a drawn up lease agreement, which stipulates the cost of all accommodation services, as well as all documents confirming payment.

Transactions for accounting for travel expenses can be found in this article.

How to calculate travel and daily expenses

An invoice for travel tickets or the use of a hotel room, of course, can be sent to the organization. But most often, workers independently purchase the travel and accommodation services they need, and then provide documents confirming the costs.

However, even before sending an employee on a work assignment to another locality, the accountant needs to at least approximately calculate how much to pay in advance. To do this, the cost of round-trip tickets, the estimated cost of a hotel room, the amount of daily allowance for the number of days of a business trip, and other planned costs are taken into account.

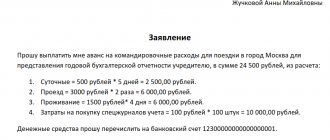

To calculate the daily allowance, it is necessary to determine how many days a person will be outside the “home” locality and add to them the days on the way. For example, engineer Ivanov A.S. goes to another city for commissioning work. It departs on 12/09/2018 (Sunday) at 5 a.m. and returns on 12/16/2018 (also on Sunday) at 9 a.m. The total number of days on a business trip will be 8 days. If the trip is domestic, then the daily allowance limit, not subject to personal income tax, will be 700 rubles. The amount of daily allowance that must be paid to engineer Ivanov will be:

700 × 8 = 5600 rubles.

If the trip is foreign, then travel expenses will increase as follows:

2500 × 8 = 20,000 rubles.

Please note that the day of departure is determined from 00 to 24 hours, the same as the day of arrival. It is important to take this into account when making final payments, for example using travel documents. If there are no tickets, for example, the employee used a personal or company car, then the duration of the business trip is calculated based on the dates specified in the memo at the end of the trip.

Since the employee still writes a statement for travel expenses (it is the basis for the cash order), you can ask him to independently estimate how much he will need, and then check his calculations. This option will be convenient, including if a person goes to a business trip in a personal car, so he will have expenses, for example, to buy gasoline. The template for filling out the application is at the end of the article.

After the estimate is approved by the chief accountant and manager, you can issue an advance for travel expenses in cash or to a bank card. The issuance of funds is carried out taking into account the standards established by the Central Bank of the Russian Federation. Read more about the requirements of the financial regulator in a separate material from PPT.ru.

As for payments in foreign currency, they are also not prohibited. To do this, travel expenses are calculated according to general rules, but then the amount received is exchanged for currency. Moreover, either the posted employee himself or someone else can exchange rubles for foreign currency. In both cases, you must attach a receipt from the bank confirming the money exchange transaction.

What documents will be needed to confirm travel expenses?

No later than three days after returning from a trip, the employee is required to report on the amounts spent. Please note that all expenses must be documented and be reasonable. Otherwise, the employer may refuse to compensate them.

Documents confirming travel expenses include:

- travel certificate with notes on departure and arrival, if it was issued at the beginning of the trip;

- travel tickets, including those issued via the Internet;

- any receipts and invoices for accommodation, rental vehicles, services received or goods purchased that were purchased to perform a work assignment;

- an advance report indicating the costs, as well as the amount paid to the employee. If more was spent on a business trip than the amount of the advance payment issued, an additional payment is made. If according to the documents there is still money left, it must be returned to the cashier. Or the employer will independently deduct the required amount from wages (Article 137 of the Labor Code of the Russian Federation).

Also an important document is a report (memo) on the completion of a work assignment during a trip. Otherwise, the feasibility of travel expenses will not be proven. Note that such a report can also become a source of information about the duration of a business trip if the employee traveled to the destination by personal or official transport.

Documentation of travel expenses

The advance report is prepared using the strict reporting form AO-1. The document indicates the amounts issued on account and received at the cash desk after the employee arrived at the enterprise.

The advance report and Form AO-1 also include supporting documents: waybills, checks, receipts, travel tickets. That is, all transactions made by an employee during a work trip, on which the issued funds were spent, must be documented. Do not forget that housing costs must also be documented, at least with an agreement or receipt for the rental of residential premises, with the amount of payment indicated in it. When checking, only funds actually issued and goods and services paid are taken into account.

Travel expenses, like any other, reduce the tax base. Since they are not so easy to identify for tax authorities, they monitor this expense item very closely. Therefore, the accountant needs to be especially scrupulous about the supporting documents provided by the employee and the preparation of the advance report.

How to reflect expenses in accounting and tax accounting

To begin with, let us remind you that for income tax expenses are taken into account on the day the advance report is approved. In this case, VAT on expenses is deductible provided that there is an invoice for them.

Expenses for the payment of average wages for the period of a business trip are included in labor costs. The remaining expenses during a business trip are required by the Tax Code of the Russian Federation to be considered as other expenses associated with production and sales.

How to reflect travel expenses in accounting? The correct order is:

- the operation when an advance is issued for a business trip is accompanied by posting Dt 71 Kt 50 (51);

- when the accountant wants to indicate that travel expenses (invoice) are taken into account, the posting should be: Dt 26 (08, 20, 23, 44) Kt 71.

Documentation of a business trip

Not everyone can be sent on a business trip.

In order to know how to properly arrange a business trip, you must first understand what it is.

A business trip is considered to be a dispatch of an employee, issued by order of the manager, outside the place of permanent work, to resolve issues that are directly related to the person’s official duties. The permanent place of work is reflected in the agreement concluded between the employee and the employer.

Please note that only a person with whom an employment contract has been concluded can be sent on a business trip. In the case of sending a person who performs his duties on the basis of a contract for the provision of services, this is not considered a business trip.

Labor legislation contains a list of persons whose assignment on a business trip is not permitted:

- Persons who work on the basis of an employment contract, but have not reached the age of majority;

- Pregnant employees.

There is a category of employees who can be sent on a trip for official matters only if several conditions are met: the written consent of these persons, as well as a medical certificate about the admissibility of such a referral.

By consent, the following are sent on business trips:

- female workers with children under three years of age;

- workers raising children under 5 years of age alone;

- persons working at the enterprise and having disabled children;

- persons working in the organization and caring for their sick relatives.

When the above conditions for sending employees on trips related to official matters are met, it is necessary to proceed with the correct registration of the business trip.

Please note that, as a rule, the procedure for sending on a trip, as well as issues related to the financial support of employees who are sent on a trip, are resolved by creating a local regulatory act.