If you have chosen a simplified taxation system with the “Income minus expenses” object, then you can reduce the tax amount at the expense of your expenses. To do this, you will have to carefully consider each payment that you want to take into account in the simplified tax system. Before recognizing an expense when calculating tax, check all prerequisites.

- The expense is economically justified and aimed at generating income.

- Corresponds to the list of expenses from Art. 346.16 Tax Code.

- You have paid the supplier in full.

- You have already received what you paid for: the goods have been shipped, the service has been provided, the work has been completed.

- You have documents that confirm the expense.

- To write off expenses for goods that you bought in order to resell later, the goods must be sold.

Take into account the expense in the simplified tax system according to the latest date:

- date of payment to the supplier,

- date of receipt of goods, works or services from the supplier,

- date of shipment of the goods to the final buyer.

List of expenses according to the simplified tax system for 2021 - 2021

Taking into account the requirements of the norms of Ch. 26.2 of the Tax Code of the Russian Federation, the object for calculating tax under the special regime in question must be determined in one of 2 ways:

- income;

- income minus expenses.

For the first method, the issue of expenses for tax purposes does not matter, but for the second it plays a very important role.

Read about how to change the object of taxation on a simplified basis in this article.

Clause 1 Art. 346.16 of the Tax Code of the Russian Federation identifies the following expenses under the simplified tax system - income minus expenses:

- costs for the purchase, production and installation of fixed assets;

Read about the procedure for writing off fixed assets for expenses under the simplified tax system here.

- costs of purchasing intangible assets;

- costs for the purchase of exclusive rights, know-how, intellectual property;

- costs incurred in obtaining patents;

- costs associated with R&D;

- costs of repairing and improving fixed assets - both own and leased;

- expenses incurred under lease agreements;

- material costs;

We also advise you to look at recommendations for accounting for expenses incurred due to the COVID-19 epidemic from ConsultantPlus experts. You can get trial access to the legal system for free.

- labor costs;

- costs for all types of compulsory insurance (pension, social, medical, life insurance);

- expenses related to payment for services provided by credit institutions;

What services provided by credit institutions can be taken into account in expenses under the simplified tax system, read the article “Accounting (nuances)”.

- costs in the form of input VAT amounts;

Read about the reflection of VAT under the simplified tax system here and in the material “How to take into account input VAT under the simplified tax system?”.

- costs aimed at paying customs duties;

- expenses associated with business trips (payment for travel to the place of performance of an official assignment and back, payment for accommodation, daily allowance);

- costs of accounting, auditing, legal and other similar services, including accounting services ;

Is it possible to take into account consulting costs under the simplified tax system, find out from the material “Consulting costs under the simplified tax system, income minus expenses”

- costs of training and retraining of personnel;

Can participation in a conference be considered expenses for training and retraining of personnel? Find out from the publication “Participation of employees in conferences - an expense under the simplified tax system?”

- stationery costs;

- costs for postal, telephone and other office services.

You can find out whether the amount of written off receivables is taken into account in the costs when applying the simplified tax system in the Ready-made solution from ConsultantPlus, having received free access to the system.

A detailed list of expenses under the simplified tax system is given in Art. 346.16 Tax Code of the Russian Federation. It is closed, that is, other expenses that are not indicated in this list cannot reduce the tax base under the simplified tax system.

Read about the requirements for expenses taken into account under the simplified tax system in this article..

What expenses cannot be recognized?

Despite the fact that the list of accepted costs, named in Art. 346.16, includes all the main costs that arise when conducting business; some payments cannot be taken into account:

- entertainment expenses that the taxpayer has the right to take into account on the OSN cannot be taken into account by the simplifier;

- the amount of advances transferred to suppliers for goods, works and services that will be received in the future. These payments can be taken into account only after the receipt of goods, works and services;

- VAT, which the simplified taxation system payer allocated in invoices issued to customers and paid to the budget;

- the simplified tax itself.

The Ministry of Finance in its clarifications emphasizes that the list of accepted costs under the simplified tax system is closed. It will not be possible to take into account other costs (Letter dated March 23, 2017 No. 03-11-11/16982).

Legal documents

- Chapter 26.3 of the Tax Code of the Russian Federation

- Art. 346.17 Tax Code of the Russian Federation

- Art. 346.16 Tax Code of the Russian Federation

- Art. 346.17 Tax Code of the Russian Federation.

- Art. 264 Tax Code of the Russian Federation

Rates according to the simplified tax system - 6 or 15%

According to Art. 345.20 of the Tax Code of the Russian Federation, when using the “income” object to calculate the single tax, a rate of 6% is provided, which from 2021 in the regions can be reduced to 1%. For the object “income minus expenses”, taking into account the type of activity of the taxpayer, the tax rate can vary from 5 to 15%.

Features of the recognition and assessment of expenses for a specific type of activity are given in the accounting policy.

Important! All expenses that reduce the tax base under the simplified tax system “income minus expenses” must be documented and economically justified (clause 2 of article 346.16, clause 1 of article 252 of the Tax Code of the Russian Federation).

Conditions of use

^To the top of the page

To apply the simplified tax system, certain conditions must be met:

| Employees (persons) | Income (million rubles) | Residual value (million rubles) |

| <� 130 | <� 200 | <� 150 |

The indicated income values are indexed by a deflator coefficient.

Separate conditions for organizations:

- The share of participation of other organizations in it cannot exceed 25%

- Prohibition of the use of the simplified tax system for organizations that have branches

- An organization has the right to switch to the simplified tax system if, based on the results of nine months of the year in which the organization submits a notice of transition, its income did not exceed 112.5 million rubles (Article 346.12 of the Tax Code of the Russian Federation)

Recognition of material expenses under the simplified tax system, as well as other types of expenses

Clause 2 Art. 346.17 of the Tax Code of the Russian Federation defines the following points for recognizing expenses by an organization or individual entrepreneur under the simplified tax system - income minus expenses:

1. Material expenses are accepted on the date of payment of the debt in one of the following ways:

- transfer of funds from the taxpayer’s current account;

- issuing funds from the cash register;

- any other way of repaying the debt.

Such expenses of the simplified tax system, the list of which is determined taking into account the requirements of Chapter. 25 of the Tax Code of the Russian Federation, include:

- purchase of raw materials, including those used for technological purposes;

- purchase of various types of equipment and other household supplies;

- purchase of components, semi-finished products;

- procurement of works and services involved in the production process;

- use of fixed assets and other property related to environmental activities.

2. Expenses incurred in connection with calculations for wages under the simplified tax system are recognized in the same manner as material expenses.

Regarding the list of simplified taxation system expenses related to payment for work activities, you should also be guided by the provisions of Chapter. 25 Tax Code of the Russian Federation. These costs include:

- payment of wages to employees;

- bonuses and other incentive payments;

- the cost of utilities, food and products provided to employees free of charge;

- expenses for the purchase and production of uniforms for employees, which are given to them free of charge or sold to them at a reduced price.

A complete list of labor costs is contained in Art. 255 Tax Code of the Russian Federation.

3. Expenses for payment of the cost of goods that were purchased for the purpose of further sale are accepted as they are sold.

Read more about accounting for the write-off of goods when applying the simplified tax system here.

4. Other features of recognizing expenses are as follows:

- tax expenses are written off based on the date of actual payment of taxes;

- expenses for fixed assets and intangible assets are recognized at the end of the tax period in the amount of amounts paid;

Read more here.

- when paying by bill of exchange, expenses are taken into account on the date of payment of the bill of exchange, however, if the bill of exchange is transferred in favor of third parties, then the date of recognition of the expense corresponds to the moment of its transfer.

Simplified people keep records of income and expenses in KUDIR. We described in this article how to fill out the book using the current form.

You can find a ready-made sample of filling out KUDIR for 2021 in ConsultantPlus. Get trial access for free and proceed to the material.

Replaces taxes

^To the top of the page

In connection with the application of the simplified tax system, taxpayers are exempt from taxes paid in connection with the application of the general taxation system: Organizations Individual entrepreneurs

- corporate income tax, with the exception of tax paid on income from dividends and certain types of debt obligations;

- property tax for organizations, however, from January 1, 2015, organizations using the simplified tax system are required to pay property tax in relation to real estate, the tax base for which is determined as their cadastral value (clause 2 of article 346.11 of the Tax Code of the Russian Federation, p. 1 Article 2, Part 4 Article 7 of the Federal Law of 04/02/2014 No. 52-FZ);

- value added tax.

- personal income tax in relation to income from business activities;

- property tax for individuals on property used in business activities. however, from January 1, 2015, for individual entrepreneurs using the simplified tax system, an obligation has been established to pay property tax in respect of real estate objects that are included in the list determined in accordance with paragraph 7 of Art. 378.2 of the Tax Code of the Russian Federation (clause 3 of article 346.11 of the Tax Code of the Russian Federation, clause 23 of article 2, part 1 of article 4 of the Federal Law of November 29, 2014 No. 382-FZ)";

- value added tax, with the exception of VAT paid when importing goods at customs, as well as when executing a simple partnership agreement or a property trust management agreement).

The use of the simplified tax system does not exempt you from performing the functions of calculating, withholding and transferring personal income tax from employee salaries.

Expenses that cannot be taken into account under the simplified tax system “income minus expenses”

A list of some types of expenses that, according to officials, do not reduce the tax base under the simplified tax system “income minus expenses” is presented in the table.

| Expenses that do not reduce the tax base under the simplified tax system “income minus expenses” | Rationale |

| Dividend payment expenses | Letter of the Ministry of Finance of Russia dated July 22, 2019 No. 03-11-11/54321 |

| Expenses of an individual entrepreneur for paying for travel and renting living quarters for himself as business travel expenses | Letters of the Ministry of Finance of Russia dated August 16, 2019 No. 03-11-11/62269, dated February 26, 2018 No. 03-11-11/11722 |

| Expenses for the acquisition of real estate under agreements for participation in shared construction before receiving ownership of completed construction objects | Letter of the Ministry of Finance of Russia dated August 26, 2019 No. 03-11-11/65390 |

| Commission to the bank for early repayment of the loan, paid in a fixed amount | Letter of the Ministry of Finance of Russia dated 08/06/2019 No. 03-11-11/59072 |

| Advance payments (prepayment) | Letters of the Ministry of Finance of Russia dated May 20, 2019 No. 03-11-11/36060, dated April 3, 2015 No. 03-11-11/18801 |

| Compensation to employees for expenses related to the performance of labor duties | Letter of the Ministry of Finance of Russia dated March 21, 2019 No. 03-11-06/2/18724 |

| Personal income tax on employee salaries* *The tax cannot be written off on a separate basis, but it is still taken into account in expenses - as part of the salary | Letter of the Ministry of Finance of Russia dated 06/01/2018 No. 03-11-06/2/37590 |

| Expenses in the form of theft of funds in the absence of perpetrators | Letter of the Ministry of Finance of Russia dated December 19, 2016 No. 03-11-06/2/76035 |

| Expenses associated with compensation of losses by a private security company to its clients from theft of property belonging to them | Letter of the Ministry of Finance of Russia dated August 17, 2007 No. 03-11-04/2/202 |

| Costs of postal services associated with unsold goods, including through computer networks | Letters of the Ministry of Finance of Russia dated 09/01/2016 No. 03-11-06/2/51055, dated 05/30/2016 No. 03-11-06/2/31125 |

| Costs of payment of the amount withheld by the transport agency or carrier when handing over the air ticket to business travelers due to the postponement of the departure date, and the cost of tickets for the postponed flight if it was not possible to hand over the tickets | Letter of the Ministry of Finance of Russia dated July 18, 2016 No. 03-11-06/2/41888 |

| Costs associated with writing off doubtful debts, including bad debts (debts that are unrealistic for collection) | Letters of the Ministry of Finance of Russia dated February 20, 2016 No. 03-11-06/2/9909, dated June 23, 2014 No. 03-03-06/1/29799 |

| Expenses for health resort treatment of employees | Letter of the Ministry of Finance of Russia dated April 30, 2015 No. 03-11-11/25285 |

| Expenses in the form of negative exchange rate differences arising when purchasing foreign currency at a rate higher than the rate of the Central Bank of the Russian Federation (selling foreign currency at a rate lower than the rate of the Central Bank of the Russian Federation) | Letters of the Ministry of Finance of Russia dated August 28, 2015 No. 03-11-09/49620, Federal Tax Service of Russia dated September 15, 2015 No. GD-4-3/ [email protected] |

| Expenses for remuneration of the founder of the organization, who is its sole founder and member | Letter of the Ministry of Finance of Russia dated February 19, 2015 No. 03-11-06/2/7790 |

| Expenses for services for the provision of personnel by third parties | Letters of the Ministry of Finance of Russia dated January 23, 2015 No. 03-07-08/1947, dated April 22, 2008 No. 03-11-04/2/75, Russia dated November 28, 2006 No. 03-11-04/3/511 |

| Expenses for personal needs of an individual entrepreneur | Letter of the Ministry of Finance of Russia dated January 16, 2015 No. 03-11-11/665 |

| Costs of paying for services for maintaining the register of shareholders of a special registrar organization that has the appropriate license | Letter of the Ministry of Finance of Russia dated November 17, 2014 No. 03-11-06/2/57962 |

| Expenses for ensuring normal working conditions | Letter of the Ministry of Finance of Russia dated October 24, 2014 No. 03-11-06/2/53908 |

| Costs of paying for the right to install and operate an advertising structure | Letters of the Ministry of Finance of Russia dated 01.09.2014 No. 03-11-06/2/43627, Federal Tax Service of Russia dated 06.08.2014 No. GD-4-3/ [email protected] |

| Expenses for an electronic digital signature, the purchase of services of a center certifying an electronic digital signature and the provision of an electronic digital signature key certificate, incurred for participation in electronic auctions | Letter of the Ministry of Finance of Russia dated 08.08.2014 No. 03-11-11/39673 |

| Expenses for a special assessment of working conditions | Letters of the Ministry of Finance of Russia dated June 30, 2014 No. 03-11-09/31528, dated June 16, 2014 No. 03-11-06/2/28551, Federal Tax Service of Russia dated July 30, 2014 No. GD-4-3/14877 |

| Expenses of the taxpayer-landlord for paying for the services of a third-party organization to find tenants | Letter of the Ministry of Finance of Russia dated 08/07/2014 No. 03-11-11/39112 |

| Cost of damaged goods | Letter of the Ministry of Finance of Russia dated May 12, 2014 No. 03-11-06/2/22114 |

| Expenses for information services | Letter of the Ministry of Finance of Russia dated April 16, 2014 No. 03-07-11/17285 |

| Expenses in the form of fees for the technological connection of reconstructed power receiving devices, electrical energy production facilities, as well as electrical grid facilities, the connected capacity of which is increasing, to existing electrical networks | Letter of the Ministry of Finance of Russia dated February 17, 2014 No. 03-11-06/2/6268 |

| Expenses for payment for services for managing the financial and economic activities of the organization | Letters of the Ministry of Finance of Russia dated 02/13/2013 No. 03-11-06/2/3694, dated 02/05/2009 No. 03-11-06/2/15 |

| Fee for issuing an extract from the Unified State Register of Legal Entities | Letter of the Ministry of Finance of Russia dated April 16, 2012 No. 03-11-06/2/57 |

| Costs for the production of an anti-terrorism passport for the shopping center, as well as for the production of signs indicating parking spaces for disabled people in the car park near the shopping center | Letter of the Ministry of Finance of Russia dated March 12, 2012 No. 03-11-06/2/41 |

| Reimbursement for employees of expenses associated with business trips, employees whose permanent work is carried out on the road or has a traveling nature, as well as employees working in the field or participating in expeditionary work | Letter of the Ministry of Finance of Russia dated December 16, 2011 No. 03-11-06/2/174 |

| Expenses for the acquisition of property rights, in particular the right to claim debt | Letters of the Ministry of Finance of Russia dated September 14, 2018 No. 03-11-12/65807, dated December 15, 2011 No. 03-11-06/2/172, dated June 2, 2011 No. 03-11-11/145, Determination of the Armed Forces of the Russian Federation dated April 9. 2018 No. 309-KG17-23668 |

| Expenses in the form of the cost of rights to music and video works acquired for resale on the basis of a license | Letter of the Ministry of Finance of Russia dated August 24, 2011 No. 03-11-11/218 |

| Costs of bringing goods to a state in which they are suitable for sale | Letter of the Ministry of Finance of Russia dated 06/08/2011 No. 03-11-06/2/91 |

| Expenses for the purchase of TIR Carnets, which give the right to travel vehicles through the territory of foreign states without customs inspection | Letter of the Ministry of Finance of Russia dated January 28, 2011 No. 03-11-06/2/09 |

| Costs of paying for the services of a third party for cleaning and removing snow from the adjacent territory, as well as costs associated with the work performed on territorial improvement | Letters of the Ministry of Finance of Russia dated 03/07/2019 No. 03-11-11/14858, dated 10/22/2010 No. 03-11-06/2/163 |

| Payment for housing for workers working on a rotational basis | Letter of the Federal Tax Service of Russia dated September 14, 2010 No. ШС-37-3/ [email protected] |

| Expenses for non-exclusive rights to computer programs and databases acquired for resale | Letters of the Ministry of Finance of Russia dated November 9, 2009 No. 03-11-06/2/238 and dated November 5, 2009 No. 03-11-06/2/236 |

| Expenses for paying money to the bank for acquiring the right to claim debt from the debtor organization under a loan agreement | Letter of the Ministry of Finance of Russia dated October 13, 2009 No. 03-11-06/2/207 |

| Expenses for subscription to printed publications, including expenses for subscription to accounting literature | Letters of the Ministry of Finance of Russia dated August 10, 2009 No. 03-11-06/2/151, dated January 17, 2007 No. 03-11-04/2/12 |

| Entry fees to non-profit organizations and contributions to funds of non-profit organizations | Letter of the Ministry of Finance of Russia dated July 14, 2009 No. 03-11-06/2/124 |

| Costs of paying commission to the bank for issuing bank cards | Letter of the Ministry of Finance of Russia dated July 14, 2009 No. 03-11-06/2/124 |

| Expenses for preparation of documentation and payment of fees associated with participation in competitive bidding | Letter of the Ministry of Finance of Russia dated May 13, 2009 No. 03-11-06/2/85 |

| Expenses in the form of the cost of purchased municipal land | Letter of the Ministry of Finance of Russia dated April 15, 2009 No. 03-11-06/2/65 |

| Costs for manufacturing and placing an illuminated sign on the facade of the building | Letter of the Ministry of Finance of Russia dated 09/08/2008 No. 03-11-04/2/135 |

| Expenses for the acquisition of property rights | Letter of the Ministry of Finance of Russia dated July 31, 2007 No. 03-11-04/2/191 |

| Expenses associated with the organization's participation in competitive bidding (tenders) for the right to conclude contracts and agreements | Letter of the Ministry of Finance of Russia dated July 2, 2007 No. 03-11-04/2/173 |

| Expenses for services provided by a third-party organization for maintaining personnel records (due to the lack of a personnel department) | Letter of the Ministry of Finance of Russia dated March 29, 2007 No. 03-11-04/2/72 |

| Costs for ensuring normal working conditions, namely costs associated with the purchase of drinking water and the purchase of heaters for the administrative building | Letter of the Ministry of Finance of Russia dated May 26, 2014 No. 03-11-06/2/24963, dated January 26, 2007 No. 03-11-04/2/19 |

| Costs for ensuring normal working conditions, namely costs associated with the purchase and installation of air conditioners in office premises | Letter of the Federal Tax Service of Russia for Moscow dated October 5, 2007 No. 18-11/3/095267 |

| Expenses for the purchase of printed publications on tax accounting, as well as industry directories | Letter from the Federal Tax Service of Russia for Moscow dated January 15, 2007 No. 18-11/3/ [email protected] |

| The amount of VAT charged to the buyer and paid to the budget | Letter of the Ministry of Finance of Russia dated November 9, 2016 No. 03-11-11/65552 |

| Fines, penalties, penalties under business contracts | Letter of the Ministry of Finance of the Russian Federation dated 04/07/2016 No. 03-11-06/2/19835 |

See also the article “Expenses that officials prohibit the “simplified” from taking into account.”

Rates and payment procedure

^To the top of the page

The tax is calculated using the following formula (Article 346.21 of the Tax Code of the Russian Federation):

Tax amount=Tax rate*Tax base

Tax rate Tax base

For a simplified taxation system, tax rates depend on the object of taxation chosen by the entrepreneur or organization.

For the object of taxation “income” the rate is 6%.

According to the laws of the constituent entities of the Russian Federation, the rate can be reduced to 1%. Tax is paid on the amount of income. When calculating the payment for the 1st quarter, income for the quarter is taken, for the half-year - income for the half-year, etc.

If the object of taxation is “income minus expenses”, the rate is 15%.

At the same time, regional laws may establish differentiated tax rates according to the simplified tax system in the range from 5 to 15 percent. The reduced rate may apply to all taxpayers or be established for certain categories. In this case, to calculate the tax, income is taken, reduced by the amount of expense.

For entrepreneurs who have chosen the “income minus expenses” object, the minimum tax rule applies: if at the end of the year the amount of calculated tax is less than 1% of the income received for the year, a minimum tax is paid in the amount of 1% of the income received.

When applying a simplified taxation system, the tax base depends on the selected object of taxation: income or income reduced by the amount of expenses:

- The tax base under the simplified tax system with the object “ income ” is the monetary value of all income of the entrepreneur.

- On the simplified tax system with the object “ income minus expenses ,” the base is the difference between income and expenses. The more expenses, the smaller the size of the base and, accordingly, the tax amount will be. However, reducing the tax base under the simplified tax system with the object “income minus expenses” is possible not for all expenses, but only for those listed in Art. 346.16 Tax Code of the Russian Federation.

Income and expenses are determined on an accrual basis from the beginning of the year. For taxpayers who have chosen the “income minus expenses” object, the minimum tax rule applies: if for the tax period the amount of tax calculated in the general procedure is less than the amount of the calculated minimum tax, then a minimum tax is paid in the amount of 1% of the actual income received.

An example of calculating the amount of an advance payment for an object “income minus expenses”

During the tax period, the entrepreneur received income in the amount of 25,000,000 rubles, and his expenses amounted to 24,000,000 rubles.

- We determine the tax base of

25,000,000 rubles. — 24,000,000 rub. = 1,000,000 rub. - We determine the amount of tax

1,000,000 rubles. * 15% = 150,000 rub. - We calculate the minimum tax of

25,000,000 rubles. * 1% = 250,000 rub.

You need to pay exactly this amount, and not the amount of tax calculated in the general manner.

The laws of the constituent entities of the Russian Federation may establish a tax rate of 0% for two years for individual entrepreneurs registered for the first time and carrying out activities in the production, social and (or) scientific spheres, as well as in the field of consumer services to the population. From September 29, 2021, services for providing places for temporary residence have been added to this list (clause 4 of Article 346.20 of the Tax Code of the Russian Federation).

The validity period of these tax holidays is until 2023.

From January 1, 2021, taxpayers whose income exceeded 150 million rubles, but did not exceed 200 million rubles, and (or) the number of employees exceeded 100 people, but did not exceed 130 employees, do not lose the right to use the simplified tax system, but pay tax according to increased rates:

- 8% for the object “income”;

- 20% for the object “income reduced by the amount of expenses”.

What to do if expenses exceed income under the simplified tax system?

When calculating and paying tax, you should pay attention to the fact that Art. 346.18 of the Tax Code of the Russian Federation provides for the payment of a minimum amount of tax, defined as the product of 1% and the amount of income received.

Payment of the minimum tax is carried out in the following cases:

- if a loss was incurred during the tax period;

- if the minimum tax amount exceeds the tax received at the end of the tax period.

Read about tax losses under the simplified tax system here.

A loss should be considered the amount of excess of expenses over the amount of income received for the tax period.

With regard to the loss, the following possibilities and conditions for its write-off must be taken into account for the purposes of Chapter. 26.2 of the Tax Code of the Russian Federation:

- the loss can be reflected in deferred expenses;

- it is possible to form a tax base taking into account its reduction by the amount of the loss within 10 years following the period of its receipt;

- in case of repeated receipt of losses, it is necessary to transfer them in the order of priority;

- it is necessary to ensure the safety of documents confirming the loss during the entire period of its transfer;

- there is no need to take the loss into account in the event of a change in the simplified taxation system.

About accounting for simplified taxation system losses in a situation of regime change, read the material “Is it possible to carry forward losses received during the period of application of the simplified taxation system to the future if you switched to the general taxation regime and then returned to the simplified taxation system again?” .

Advertising expenses under the simplified tax system

Advertising expenses under the simplified tax system are taken into account according to the rules established by clause 4 of Art. 264 of the Tax Code of the Russian Federation (clause 2 of Article 346.16 of the Tax Code of the Russian Federation). This means that some of them will have to be rationed.

Only the following are not standardized:

- expenses for advertising events carried out through the use of the media (ads in print, television and radio broadcasts) and information and telecommunication networks, as well as during film and video services;

- expenses for illuminated and other outdoor advertising, including the production of advertising stands and billboards;

- expenses for participation in exhibitions, fairs, expositions; design of shop windows, sales exhibitions, sample rooms and showrooms; discounting of goods that have completely or partially lost their original qualities during exhibition; production of advertising brochures and catalogs containing information about the organization itself, goods sold, work performed, services provided, trademarks and service marks.

All other advertising expenses are recognized in an amount not exceeding 1% of sales revenue, determined in accordance with Art. 249 of the Tax Code of the Russian Federation.

This standard is considered a cumulative total from the beginning of the year. Excessive expenses are not carried forward to the next year.

For more information about accounting for advertising costs, read the article How to account for advertising costs under the simplified tax system .

Since “simplified” income is taken into account by payment, the amount of prepayment received is also included in the calculation of the advertising standard. When an advance is returned, the standard is adjusted - and the income of the tax (reporting) period in which the return was made is reduced by the amount returned (letter of the Ministry of Finance of Russia dated 02/11/2015 No. 03-11-06/2/5832).

Example

The organization received an advance in 2021 and took it into account when calculating the standard advertising costs, but the advance was returned to the buyer in 2021. In this case, there is no need to recalculate the standard and adjust expenses for 2021; the return should be taken into account when calculating the standard in 2021.

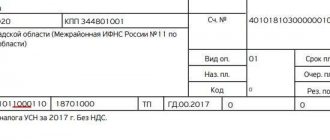

Filling out a declaration under the simplified tax system

In accordance with the Tax Code of the Russian Federation, the declaration is submitted once a year after its end no later than:

- March 31st organizations;

- April 30 IP.

The form and procedure for filling out a declaration under the simplified tax system for the report for 2020 are established by order of the Federal Tax Service of Russia dated February 26, 2016 No. ММВ-7-3/ [email protected]

When filling out a declaration form under the simplified tax system with the object of taxation “income minus expenses”, you need to pay attention to section 2.2, which contains information about the income received and the taxpayer’s expenses.

See and download the declaration form for the simplified tax system and examples of how to fill it out in this material.

Tax payment is made in advance payments based on the results of each reporting period (quarter) no later than the 25th day of the month following the end of the reporting quarter. In this case, the payment deadline for the 4th quarter corresponds to the reporting deadline for the specified period.

For more information about the deadlines for filing reports and paying taxes, read the article “What are the deadlines for submitting a declaration under the simplified tax system?” .

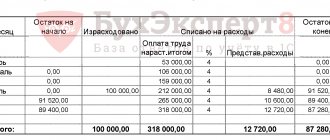

Write off expenses for fixed assets quarterly

Fixed assets are goods or property that are used in the operation of a business and not for resale. Their useful life is more than a year, their cost is more than 100,000 rubles.

The cost of purchasing fixed assets is the initial cost of the property. It is defined as the sum of all actual purchase costs. The main rule is to write off the cost of a fixed asset as expenses in equal shares within one calendar year. You can start writing off from the quarter in which the fixed asset was put into operation. Expenses are taken into account on the last day of the quarter: March 31, June 30, September 30, December 31. Thus, by the end of the year, the acquired property must be completely written off.

Read more about accounting for fixed assets in the article “Special accounting for fixed assets in the simplified tax system.”

Submit reports in three clicks

Elba will help you work without an accountant.

She will prepare reports, calculate taxes and will not require any special knowledge from you. Try 30 days free Gift for new entrepreneurs A year on “Premium” for individual entrepreneurs under 3 months

Results

Costs incurred under the simplified tax system must be determined for tax accounting purposes only if the tax object “income minus expenses” is used to calculate the tax. At the same time, Ch. 26.2 of the Tax Code of the Russian Federation provides for the concept of a minimum tax that should be paid when expenses exceed the taxpayer’s income and a loss is incurred.

Sources:

- Tax Code of the Russian Federation

- Order of the Federal Tax Service of Russia dated February 26, 2016 N ММВ-7-3/ [email protected]

You can find more complete information on the topic in ConsultantPlus. Free trial access to the system for 2 days.

Transition order

^To the top of the page

Voluntary transition procedure.

There are two options: 1 Transition to the simplified tax system simultaneously with the registration of individual entrepreneurs and organizations. The notification can be submitted along with a package of documents for registration.

If you have not done this, then you have another 30 days to think about it (clause 2 of Article 346.13 of the Tax Code of the Russian Federation) 2 Transition to the simplified tax system from other tax regimes The transition to the simplified tax system is possible only from the next calendar year. The notification must be submitted no later than December 31 (clause 1 of Article 346.13 of the Tax Code of the Russian Federation)

Organizations and individual entrepreneurs that have ceased to be UTII taxpayers due to the abolition of this special tax regime have the right to switch to the simplified tax system from 01/01/2021 by notifying the tax authority no later than 02/01/2021 (letter of the Federal Tax Service of Russia dated 01/14/2021 No. SD-4-3/ [email protected] ).

Form of notification of transition to a special tax regime (pdf 464 kb)

Download

The notification can be submitted in any form or in the form recommended by the Federal Tax Service of Russia.

Conditions for applying the simplified tax system in 2021 for LLCs and individual entrepreneurs

Not all organizations are allowed to use the “simplified” approach. The ban is established for those who have opened branches, for banks, insurers, budgetary institutions, pawnshops, investment and non-state pension funds, microfinance organizations and a number of other companies.

LLCs and individual entrepreneurs that produce excisable goods, extract and sell minerals, operate in the gambling business, or have switched to paying a unified agricultural tax cannot switch to the “simplified” tax system.

There are other restrictions:

- The company's income for 9 months of the previous year should not exceed 112.5 million rubles, multiplied by the deflator coefficient (for all except newly created ones). In 2021, the coefficient is 1.032. To switch to the simplified tax system from 2022, it is necessary that income for January-September 2021 does not exceed 116.1 million rubles (112.5 million rubles x 1.032):

- The income of LLCs and individual entrepreneurs for a quarter, half a year, 9 months or a year should not exceed 200 million rubles, multiplied by the deflator coefficient. In 2021, the coefficient is 1.032. So, in order to remain on the simplified tax system at 15% in 2021, it is necessary that income does not exceed 206.4 million rubles (200 million rubles x 1.032);

- The average number of employees of an organization or entrepreneur cannot exceed 130 people;

- The residual value of fixed assets of a company or individual entrepreneur cannot exceed 150 million rubles;

- The share of participation in the organization of other legal entities should not exceed 25%.

In 2021, the simplified tax system will be used by taxpayers who have submitted a corresponding notification to the inspectorate no later than December 31, 2020.

Legal entities and individual entrepreneurs registered in 2021 can become “simplified” if they submit a notification no later than 30 calendar days from the date of tax registration.

To apply the simplified tax system in 2022, a notification must be submitted no later than December 31, 2021.

Submit a free notification of the transition to the simplified tax system and submit a declaration under the simplified tax system via the Internet

What is the simplified tax system

A simplified taxation system is a type of single tax that replaces several others used in the general taxation system.

Thus, legal entities (LLC, JSC) and individual entrepreneurs (IP) who have switched to the “simplified system” are exempt from paying:

- income tax (for legal entities);

- Personal income tax (for individuals);

- property tax (with the exception of real estate objects subject to tax based on cadastral value);

- VAT (exception – VAT when importing goods from abroad).