Account 91 in accounting

A complete list of other income and expenses can be studied in the order of the Ministry of Finance of the Russian Federation dated October 31, 2000 No. 94n.

The “Other income and expenses” account is active-passive. The credit of the account reflects the receipt, and the debit records the expense:

The main subaccounts for 91 accounts are presented in the figure:

The purpose of analytical accounting for 91 accounts is to provide the ability to determine the financial result based on each type of income and expense. Consequently, when classifying income and expenses, it is necessary to take into account the homogeneous type of costs to ensure the possibility of determining the financial result for each operation of the same type.

For example, amounts under the article “Fines and penalties for contractual obligations” can be attributed to both expenses and income, therefore, the financial result under this article can be analyzed. Or, by analyzing the expense item for paying for the services of credit institutions, the enterprise will be able to see the effectiveness of working with the bank, whether the bank’s “products” are beneficial to the enterprise.

Subaccounts 91 accounts:

- 91.1 “Other income” - 91 1 accounting account is intended to reflect various income transactions for non-core activities of the company. An exception is extraordinary income of the organization.

- 91.2 “Other expenses” - account 91 2 in accounting is used to reflect transactions on expenses not related to the main activities of the business.

- 91.9 “Balance of other income/expenses - the account is intended for monthly calculation of the balance of 91 accounts. in order to close it. At the same time, the balance of the remaining sub-accounts continues to “hang”, which allows you to obtain information about the accumulated balances at any time. Closing with final transactions is written off to the debit or credit of the savings account. 99.

The financial characteristics of account 91 “Other income and expenses” make it possible to obtain generalized information on those operations of the company that are not directly related to the main types of OKVED. As a rule, such operations do not greatly affect the financial results of a business, but are nevertheless important for calculating reliable data on income, costs, and profits. Information can be presented in a generalized form or with analytics by types of income and expenses.

Closing 91 accounts

All subaccounts under the “Other income and expenses” account at the end of the year: balance for December, internal records - must be closed by posting to subaccount 91.09.

The financial result is credited to the debit (loss) or credit (profit) of account 99 “Profits and losses”.

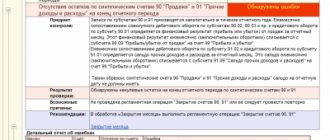

Here is a schematic example of closing 91 accounts:

Account details 91

For additional detailing of analytical accounting for business operations from other types of activities, the opening of special sub-accounts is provided:

- 91-1 “Other income” (PD);

- 91-2 “Other expenses” (PR);

- 91-3 “VAT”;

- 91-9 “Balance of other income and expenses.”

Please note that, taking into account the specifics of the company’s activities, additional sub-accounts may be opened. So, for example, you can further detail account 91-2 by type of other expenses. However, such a decision must be fixed in the accounting policies of the organization.

Postings to 91 accounts “Other income and expenses”

Correspondence and main transactions for 91 accounts are shown in the table:

| Dt | CT | Wiring Description | A document base |

| 91 | 01 | Write-off of retired fixed assets at residual/initial value. | OS-1, SP-51 |

| 91 | 02 | Calculation of depreciation on fixed assets that are leased (not an object of activity). | Accounting statement, Depreciation sheet |

| 91 | 03/04 | Write-off of retired income-generating investments in tangible assets (hereinafter referred to as MT)/intangible assets. | Accounting certificate, Acceptance certificate |

| 91 | 07 | Write-off of equipment for installation (sold/transferred free of charge) at cost. | Acceptance certificate, Invoice |

| 91 | 08 | Write-off of the cost of investments in VNA. | Certificate of acceptance and transfer, Certificate of gratuitous transfer of valuables |

| 91 | 10 | Write-off of materials sold/transferred free of charge (upon disposal of fixed assets) at actual cost. | Acceptance certificate, Invoice |

| 91 | 11 | Write-off of the cost of sold animals (not an activity item). | TTN (SP-32) |

| 91 | 14/59/63 | Creation of a reserve to reduce the value of the investment capital/ensure investments in securities/for doubtful debts. Write-off of amounts to reserves – by reverse posting. | Accounting certificate, accounting calculation for creating a reserve |

| 91 | 15 | Reflection of write-off of materials (actual cost). | Acceptance certificate, Invoice |

| 91 | 16 | Write-off of the share of deviations from the accounting cost of materials sold (if a negative value - a red reversal). | Accounting certificate, accounting calculation for writing off deviations |

| 91 | 19 | Write-off of VAT on materials sold (non-refundable). | Accounting information |

| 91 | 20/21/23 /29 | Write-off of expenses for maintaining production facilities/facilities for conservation. | Accounting certificate, accounting calculations |

| 91 | 23 | Write-off of the cost of services of auxiliary production (upon disposal of fixed assets). | |

| 91 | 28 | Write-off of the cost of irreparable defects (work of an operational nature). | |

| 91 | 43 | Write-off of commercial expenses (for the sale of operating systems, materials). | |

| 91/ 19 | 60 | Reflection of amounts accrued by the contractor for work/services performed upon liquidation/sale of fixed assets, other assets/VAT amount. | Invoice |

| 91 | 60/62/76 | The amount of receivables/debt is written off after the expiration of the statute of limitations/ cannot be recovered in any way. | INV-17, Accounting certificate, Minutes/order of the manager |

| 91 | 66/67 | Reflection of the percentage amount payable for using credits/loans. | Accounting certificate, Bank account statement |

| 91 | 68 | VAT accrual (income from the sale of operating systems/materials). | Accounting certificate, VAT accounting calculation |

| 91 | 70/69/10 | Reflection of expenses for liquidation of OS-v. | Work order for piece work, Certificate of write-off of valuables |

| 91 | 75 | Reflection of expenses (simple partnership agreement). | Accounting certificate-calculation |

| 91 | 51/76 | Reflection of violations of the terms of business contracts (paid/recognized for payment). | Bank account statement, Invoice, Accounting certificate |

| 91.02 91.01 | 52/60/62 /58/… + 55/67 | Reflection of exchange rate differences (negative). Positive - reverse wiring. | Act on revaluation of values, Accounting certificate |

| 91 | 73 | Write-off of the cost of material damage (it is unrealistic to recover, for example, a court refusal). | INV-17, Leader's order Accounting information |

| 91 | 76 | Payment for services of credit institutions/costs of consideration of cases in courts. Profit receivable under a simple partnership agreement / interest on loans, income on shares, shares and securities / fines, penalties and interest for violation of the terms of agreements - reverse posting. | Accounting certificate, Notice/Bank statement, Invoice, KO-1 |

| 91 | 79 | Reflection of expenses on transactions with structural divisions (on a separate balance sheet). Reflection of income - reverse posting. | Invoice, Advice |

| 91 | 81 | The difference between actual costs (repurchase of shares/shares) and par value (participant's own shares/shares). When repurchasing, the difference is reflected by reverse posting. | Accounting statement, calculation of the difference between the actual costs of repurchasing shares and their nominal value |

| 91 | 94 | Write-off of the cost of shortage of valuables in excess of the norm / from damage (in the absence of specific culprits). | INV-3, Manager's order, Accounting certificate |

| 91 | 98 | Write-off of other income amounts (future periods). Enrollment – reverse posting. | Accounting information |

| 99.02/ 99.03 | 91 | Write-off of the balance of income/expenses at the end of the month. | Calculation of the balance of other income and expenses, Accounting certificate |

| 96 | 91 | Crediting to income the amount of unused reserve for upcoming expenses/payments. | Accounting information |

| 60/76 | 91 | Crediting of accounts payable/receivable (unclaimed after the expiration of the limitation period). | INV-17 |

| 10/62 | 91 | The amounts of transactions with containers are reflected. | Waybill, Invoice |

| 07/10/11 /41/43/45 08 /20/21/29 /23 | 91 | The surplus/unaccounted amounts of inventory items identified during the inventory are reflected. | INV-3, INV-19, INV-24 |

D) writing off the amount of accrued depreciation on retired fixed assets?

122. Which accounting entries reflect the accrual of depreciation on fixed assets for general economic purposes:

A) Dt 20 “Main production” Kt 02 “Depreciation of fixed assets”;

B) Dt 25 “General production expenses” Kt 02 “Depreciation of fixed assets”;

C) Dt 26 “General business expenses” Kt 02 “Depreciation of fixed assets”;

D) Dt 29 “Service production and facilities” Kt 02 “Depreciation of fixed assets”?

????123.What do the accounting entries mean in the accounting accounts Dt 91 “Other income and expenses”, subaccount 91-2 “Other expenses” Kt 70 “Settlements with personnel for wages”:

A) Wages are accrued to workers for production maintenance work;

B) wages are accrued to workers for work on manufacturing products;

C) wages were accrued to workers for major repairs of machines;

D) have workers been paid wages for dismantling the liquidated facility?

124. What accounting entries in the accounting accounts reflect the receipt of fixed assets to the enterprise under the terms of the current lease agreement:

A) Dt 001 “Leased fixed assets”;

B) Dt 01 “Fixed assets” Kt 08 “Investments in non-current assets”;

C) Dt 03 “Income-generating investments in tangible assets” Kt 08 “Investments in non-current assets”;

D) Dt 08 “Investments in non-current assets” Kt 83 “Additional capital”?

Examples of transactions and postings for 91 accounts

Example 1. Accounting for other rental income on account 91.01

Let's say Leto LLC, with its main activity in the production of confectionery products, receives income from renting out premises in one of the industrial buildings. The tenant of “Vasilek” pays 50,000 rubles monthly, according to the concluded agreement. Payment for rent was credited to the account in the amount of 50,000 rubles.

The amount of monthly expenses incurred by Leto LLC for maintaining the premises consists of:

- depreciation charges - 2,000 rubles;

- wages for service personnel - 8,000 rubles;

- wage taxes - 1,500 rubles;

- utilities and other services - 3,000 rubles.

Based on the results of November 2021, the following entries were made in the accounting department of Leto LLC:

| Dt | CT | Wiring Description | Amount, rub. | A document base |

| 76 | 91.01 | The amount of rent for November 2021 has been accrued | 50 000 | Certificate of completion |

| 91.02 | 02/70/69/23 | The costs of maintaining the rented premises were written off (2,000 + 8,000 + 1,500 + 3,000) | 14 500 | Receipts, invoices, acts, etc. |

| 51 | 76 | Payment for rental services has been credited to the personal account received from the tenant “Vasilek” | 50 000 | Bank statement |

Example 2. Accounting for other income from the sale of materials on account 91.01

Let’s assume that Leto LLC sold other materials not used in the production of confectionery products. Wherein:

- sales cost - 40,000 rubles;

- cost of materials - 15,000 rubles;

- salary and taxes on wages of production workers - 4,000 rubles.

Accounting for other income from materials sold was reflected in the accounting of Leto LLC with the following entries to account 91:

| Dt | CT | Wiring Description | Amount, rub. | A document base |

| 76 | 91.01 | Accrued income from the sale of materials | 40 000 | Sales Invoice |

| 91.02 | 10 | The cost of materials has been written off | 15 000 | Costing |

| 91.02 | 23 | Costs associated with sales (salaries and taxes) are written off | 4 000 | Payroll |

| 51 | 76 | Funds received for materials sold | 40 000 | Bank statement |

Example 3. Accounting for banking services on account 91.02

Let’s say Leto LLC has entered into an agreement with a bank for the provision of services. At the end of the month (reporting period), the bank provided the following services:

- for installing the Bank-Client system for a period of 3 years (one-time service) - 7,000 rubles;

- for “Bank-Client” service (monthly service) - 400 rubles;

- for settlement and cash services (RKO) - 2,000 rubles;

- for cash collection - 6,000 rubles.

In the accounting of Leto LLC, entries were made to reflect banking services:

| Dt | CT | Wiring Description | Amount, rub. | A document base |

| 91.02 | 60 | RKO services are reflected | 2 000 | Agreement for servicing a bank account, bank statements |

| 91.02 | 60 | Cash collection expenses | 6 000 | Certificate of services rendered |

| 91.02 | 60 | Costs for installing “Bank-Client” | 7 000 | Certificate of services rendered |

| 91.02 | 60 | Expenses for servicing “Bank-Client” per month | 400 | Certificate of services rendered |

Typical transactions for account 91:

- D account 91 02 K 66, 67 – the accrual of credit percentage is reflected.

- D 91.02 K 10 – reflects the write-off of inventory items upon disposal.

- D 91.09 K 99 – the closing of the account balance is reflected.

- D 91.02 K 70 – reflects the accrual of semi-annual bonuses to staff.

- D 10 (41, 01) K 91.01 - surplus inventory, goods, fixed assets were identified.

- D 76 K 91.01 – reflects the accrual of interest on bonds.

- D 91.02 K 76 – reflects the accrual of the commission for the bank’s cash settlement services.

- D 51 K 91.01 – reflects the receipt of penalties for non-compliance with contractual terms.