Income tax expenses: general rules

The general requirements for income tax expenses are known to everyone. According to paragraph 1 of Art. 252 of the Tax Code of the Russian Federation is:

- justification of expenses;

- their documentary evidence;

- as well as the connection with the activity from which income is expected to be generated.

At first glance, everything is simple and extremely clear, and most importantly, logical. These restrictions are designed to cut off all opportunities for abuse and attempts by management or owners to obtain any personal benefit at the expense of the company and, ultimately, the budget (in the form of tax savings).

At the same time, compliance with these requirements does not seem difficult at first. However, in practice, the issue of recognizing expenses for income tax is one of the key issues in the taxation of organizations. It gives rise to no less controversy than the procedure for VAT deductions. And controllers who guard the interests of the budget carefully examine every expense of the organization and, at the slightest suspicion, try to remove expenses from the base, which leads to additional tax assessment.

Therefore, you need to not only know these requirements, but also be able to apply them in accounting work.

article will help you learn everything about the conditions for recognizing expenses for “profitable” purposes .

Read about some of the nuances of documenting expenses in the following articles:

- “When is a qualified electronic signature required?”;

- “Printing is not a mandatory attribute of the primary document”;

- “To confirm the costs of road transportation of goods, a bill of lading is required”;

- “It is impossible to confirm expenses with a facsimile document”;

- “Monthly act - how to confirm rental expenses?”

What do you need to know about expense accounting?

Income tax is the “main” tax for those who work under the general taxation system (GTS). Its rate is not the same for different categories of taxpayers, but for online stores, as a rule, it is never less than 13.5%. A complete list of rates for this tax can be found in Article 284 of the Tax Code of the Russian Federation.

The tax base for it is determined by subtracting all documented and justified expenses from the amount of income. Do not forget about the limitation: the tax amount can be reduced by no more than 50% at a time.

All expenses that reduce the income tax base are divided into expenses associated with production and sales

, and

non-operating

(clause 2 of Article 252 of the Tax Code).

In accordance with Article 252 of the Tax Code of the Russian Federation, expenses are recognized as documented

and

economically justified costs

. The list of such expenses specified in the Tax Code remains open. The famous Resolution of the Supreme Arbitration Court No. 53 on unjustified tax benefits marked the beginning of the arbitration practice of “offsetting” various types of expenses. The resolution states that a tax benefit cannot be justified if it is not related to actual business activity. This thesis results in thorough checks of your expenses, for which you need to prepare in advance.

For online stores, it is very important to correctly take into account and justify the costs of creating and promoting a website.

For example, you used a programmer, and the site cost you a pretty penny. The tax office will check to see if you could have gotten by with a simpler website. Have you ordered promotion from a renowned SEO company? The inspector will check to see if you are deliberately inflating expenses. Be prepared to answer these questions and justify your decisions.

Practicing accountants advise collecting in advance as many unified documents signed by you and your counterparties as possible, and attaching internal economic calculations to them. This way, you may avoid claims from tax inspectors already at the reporting stage.

Remember: you must justify the connection of your expenses with activities aimed at generating income. For example, the cost of postal delivery of goods to customers is directly related to revenue generation. But the rent for an apartment for business travelers is only for the periods when your employees lived there.

However, the connection between many costs and income generation is possible and even easy to prove. You sent an employee on a business trip, submitted an application to a recruitment agency, rented an apartment for the employee, having written down the provision for official housing in the employment contract - write off such expenses.

Expenses in foreign currency should be recalculated into Russian rubles at the rate of the National Bank of Russia on the date of recognition of the expense. In this case, a so-called exchange rate difference may arise when the exchange rate on the date of the expense itself and on the date of its recognition is not the same. If the exchange rate difference is positive, it will have to be included in non-operating income. The negative difference can be included in non-operating expenses.

Classification of expenses for tax purposes

The list of income tax expenses and their classification are also defined in the Tax Code of the Russian Federation. First of all, they are divided:

- for production and sales costs;

- non-operating expenses;

- expenses that are not taken into account for income tax purposes.

They can be divided differently:

- into direct and indirect;

- taken into account and not taken into account when calculating income tax.

The correct attribution of expenses within a particular classification directly affects the amount of tax payable. Without exception, all materials in this section are designed to help you correctly determine the nature of expenses and the procedure for their accounting in the tax base. Let's look at some in a little more detail.

Standardized expenses. Entertainment expenses

Entertainment expenses include (clause 2 of Article 264 of the Tax Code of the Russian Federation):

- Expenses for an official reception (breakfast, lunch or other similar event). The location of the reception does not matter;

- Service costs (transportation, catering during negotiations, payment for translators) for representatives of other organizations participating in negotiations in order to establish and maintain cooperation, participants who arrived at meetings of the board of directors and other management. The Ministry of Finance allowed to accept individuals (Letter of the Ministry of Finance of the Russian Federation dated 06/03/2013 N 03−03−06/2/20149).

Expenses for organizing entertainment, recreation, prevention or treatment of diseases are not included in entertainment expenses.

Costs for the buffet, the ship and the artists are not taken into account in entertainment expenses (Letter of the Ministry of Finance of the Russian Federation dated December 1, 2011 N 03-03-06/1/796).

How much are hospitality expenses taken into account for NU?

Representation expenses for NU purposes are taken into account in an amount not exceeding 4% of labor costs for the reporting period. To recognize entertainment expenses in NU, they must be:

- economically justified (signing contracts, attracting new customers, increasing sales volume (Resolution of the Federal Antimonopoly Service of the Ural District dated January 19, 2012 N F09-9140/11);

- documented;

- were taken into account in expenses according to the standard (4%).

Previously, the Federal Tax Service required the following documents to be completed to confirm entertainment expenses (Letter of the Ministry of Finance of the Russian Federation dated March 22, 2010 N 03-03-06/4/26):

- Order on organizing the event;

- Estimate for the event;

- Report on the event;

- Primary documents confirming expenses.

Chapter 25 of the Tax Code of the Russian Federation does not establish a specific list of documents confirming entertainment expenses.

Now the list of documents for confirming entertainment expenses has been reduced (Letter of the Ministry of Finance of the Russian Federation dated 04/10/2014 N 03−03−РЗ/16288, Letter of the Federal Tax Service of the Russian Federation dated 05/08/2014 N ГД-4-3/8852.) A supporting document can be a report on entertainment expenses , approved by the head of the organization. Moreover, all expenses listed in the report must be confirmed by relevant primary documents. It is safer in the report information about the event, date, place, its purpose, representatives of the parties, results achieved as a result of the reception, etc.

An example of calculating the amount of standardized entertainment expenses included in expenses for NU:

Production costs

So, classification group I of costs is expenses for core activities. These include the following:

- Material costs. These are expenses for the purchase of all types of raw materials, materials, components, equipment, works and services of a production nature, etc.

The features and nuances of accounting for these expenses are described in detail in this article .

- Labor costs. And this is not only salary, but a much wider range of accruals in favor of employees: bonuses, various additional payments and compensations, payment based on average earnings for legally unworked periods, dismissal, etc.

article is devoted to general issues of “salary” expenses .

Our other materials will help you correctly account for your expenses:

- bonuses;

For accounting nuances, see here and here ;

- vacation pay;

We wrote about them here .

- salary supplements;

this publication about them .

- and other expenses.

- Amounts of accrued depreciation. Our articles will help you decide on its method and correctly calculate the amounts:

- “What method to choose for calculating depreciation in tax accounting?”;

- “Linear method of calculating depreciation of fixed assets (example, formula)”;

- “A practical example of using the non-linear depreciation method”;

- “The essence and features of the application of the accelerated depreciation method.”

- Other expenses. These are all other expenses in addition to those listed above. For example, for rent, business trips, etc.

Find the main issues of their accounting in this article .

Income and expenses of the organization from core activities

Income of the organization in accordance with the Accounting Regulations “Income of the Organization” PBU 9/99, approved by Order of the Ministry of Finance of Russia dated 05/06/1999 No. 32n (as amended on 04/06/2015; hereinafter referred to as PBU 9/99) is recognized as an increase in economic benefits as a result receipt of assets (cash, other property) and (or) repayment of liabilities, leading to an increase in the capital of this organization, with the exception of contributions from participants (owners of property).

The following types of income do not count as income:

- commissions received under contracts, subject to transfer to the principal;

- advances received for upcoming deliveries of products, goods, performance of work, provision of services;

- amounts of deposits and pledges received;

- amounts received to repay a credit (loan) previously provided to the borrower.

The expenses of an organization in accordance with PBU 10/99 are a decrease in economic benefits as a result of the disposal of assets (cash, other property) and (or) the occurrence of liabilities, leading to a decrease in the capital of this organization, with the exception of a decrease in contributions by decision of participants (owners of property ).

The following are not recognized as expenses:

- contributions to the authorized (share) capitals of other organizations, acquisition of shares and other securities not for the purpose of resale;

- transfers under commission agreements, agency and other similar agreements in favor of the principal, principal, etc.;

- advance payments to suppliers and contractors for inventories, fixed assets, intangible assets, works, services;

- transfers against deposits and guarantees under supply contracts;

- repayment of loans and borrowings received by the organization.

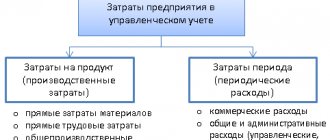

Expenses for ordinary activities for the analysis of financial results can be grouped into variable and fixed.

Variables include material costs, labor costs for production workers, social contributions, depreciation of production assets, and other costs directly related to production. Variable costs are directly proportional to the volume of output.

Fixed expenses are divided into administrative and commercial. Administrative expenses are indirectly related to the production process and include the cost of maintaining the administrative staff of a production enterprise, travel and entertainment expenses, communication costs, Internet, office rental, etc.

Commercial expenses are associated with pre-sale preparation, advertising, and product promotion.

Fixed costs do not depend on production volume.

Variable costs form an incomplete cost of production. Revenue minus variable expenses forms gross (marginal) profit.

The gross profit indicator does not depend on changes in the volume of output (in other words, the share of gross profit per unit and for the entire volume of product sold will be the same).

Variable and fixed costs form the total cost of production. goods, works, services.

Revenue less total cost is operating profit.

The relationship between income, expenses and profit is shown in Fig. 1.

Non-operating expenses

This group of expenses includes expenses that are not related to production and sales, as well as some losses.

Read more here .

One of the types of non-operating expenses that are quite often encountered in practice is interest on debt obligations, for example, on loans and borrowings. For them Art. 269 of the Tax Code of the Russian Federation provides for a special accounting procedure.

Read more about this procedure here and here.

The current economic situation is not entirely favorable. In times of crisis, the risk of non-payments always increases. This means that the question of accounting for doubtful and bad debts arises much more often. Of course, we couldn't ignore it.

“Procedure for forming reserves for doubtful debts” will help you to correctly form a “ .

And about what’s new in the formation of the reserve since 2017, read the article “The procedure for calculating the reserve for doubtful debts has changed .

We devoted a separate article to the procedure for writing off overdue receivables.

All the details are here .

The meaning of the concept of profit and its types

The concept of profit is that it represents all the money that a company received from its activities after subtracting from it the costs incurred in producing and selling products.

The profit formula looks like:

The relationship between the concepts of costs (expenses) and profit is obvious from the formula.

Logos LLC received revenue in the amount of 50,000 rubles, while 25,000 rubles were spent on production. This means that the profit will be equal to: 50,000 – 25,000 = 25,000 rubles. From this amount the company will pay taxes and other obligatory payments, only after this will it result in net profit, which Logos LLC can dispose of at its own discretion.

The concept of enterprise profit characterizes only the positive value (difference) between costs and income. If its size is less than the sum of all costs incurred (cost), and the difference turns out to be negative, this is called a loss . Many enterprises, if they do not try to change the situation, go bankrupt.

Let's take a closer look at what the definition of profit . Economists call this the difference between all production costs and revenue, which reflects how successfully the company is managed and the need for its products in the market. In addition, you need to remember that it is the basis for the development of an enterprise, the growth of its competitiveness, from which firms form various types of cash reserves that will be used in the event of a decrease in income or unforeseen situations.

Let's consider the types of profit of an enterprise:

Depending on the type of profit, its structure contains:

- Amounts from sales, produced, sold products, services;

- Sale or rental of various property (premises, vehicles);

- Receiving dividends (if the company has shares of other organizations);

- Sale of various securities.

Organizations constantly monitor the income received; for this purpose, an analysis is carried out and within its framework it is determined what types of profits and in what amount were generated as a result of the activities of the enterprise.

The considered economic concepts have different meanings, which is why it is so important to give the concept of revenue, profit and income and distinguish between them.

Direct and indirect income tax expenses: list

Costs are divided into direct and indirect based on their connection with production. The general procedure for such division is enshrined in Art. 318 Tax Code of the Russian Federation.

Thus, direct costs include material costs, wages of production personnel and depreciation of production assets. All other costs are indirect.

The company determines the specific list of direct expenses independently.

Read about how to do this here .

Proper allocation of expenses is extremely important because the period for recognizing direct expenses is completely different than indirect expenses. This means that an error in qualification can lead to incorrect allocation of expenses between periods, underestimation of the tax base in one of them and overpayment of tax in another. That is why we did not limit ourselves to just one material on this topic.

Another article on our site is devoted to the division of costs into direct and indirect.

Looking ahead a little, we note that you should divide expenses into direct and indirect, taking into account the specifics of your activity and economic justification. Otherwise, tax authorities will recalculate the tax as they see fit, and, most likely, they will prove their case in court.

See, for example, “Rent of industrial premises may not be recognized as an indirect expense .

Standardized income tax expenses in 2017–2018

Some expenses do not reduce income tax completely, but within certain limits - according to the standards established by the Tax Code of the Russian Federation. For example:

- representative;

Their accounting is described in detail in this article .

- advertising;

Read about them here .

- to create some reserves, etc.

Expenses in excess of the norm are taken into account against profit after tax.

You need to know the types of standardized costs, the size of standards and the procedure for calculating them so as not to inflate costs and not underestimate taxes.

We have compiled the standards for you into a single table “Standards provided for by the Tax Code of the Russian Federation” .

Methods for recognizing expenses in NU

It is important not only to correctly classify expenses, but also to determine the correct date for their inclusion in the tax base. And this date depends on which method of accounting for income and expenses you have chosen. There are 2 such methods:

- accrual method, when expenses are recognized in the period in which they are incurred, regardless of the payment period;

- cash method - based on payment.

Each of them has its own characteristics, advantages and disadvantages. In addition, there is a very clear limitation on the use of the cash method of recognizing income and expenses.

The following articles in this section will help you choose the optimal method:

- “Accrual method and cash method: main differences”;

- “What is the procedure (conditions) for recognizing income and expenses using the cash method?”.

These articles are just a small part of what is presented in this subsection of our website. It is constantly updated with new relevant and useful materials. Visit it often and you will know everything about expense accounting.