Introductory information about the simplified tax system

Under the simplified tax system, the taxpayer has the right to choose for himself the object of taxation from two options (clauses 1, 2, article 346.14 of the Tax Code of the Russian Federation):

- income;

- income reduced by expenses.

Each of these taxation objects has both advantages and disadvantages, which it is advisable for organizations and entrepreneurs to take into account when planning work on the simplified tax system. The table below shows a comparative analysis for each object of taxation under the simplified tax system

| How is the simplified tax system different? | |

| "income" | "income minus expenses" |

| Tax rate | |

| The general rate is 6% (clause 1 of Article 346.20 of the Tax Code of the Russian Federation) | The general rate is 15% (clause 2 of article 346.20 of the Tax Code of the Russian Federation) |

| The tax base | |

| Amount of income | The amount of income reduced by the amount of expenses |

Next, we’ll tell you how, with a simplified tax system of 6%, you can reduce the “simplified” tax on expenses incurred.

Material costs.

This category of expenses is “simplified” by virtue of clause 1 of Art. 254 and paragraphs. 5 p. 1 art. 346.17 of the Tax Code of the Russian Federation can include costs:

- for the purchase of raw materials and (or) materials used in the production of goods (performance of work, provision of services) (clause 1);

- for the purchase of materials used for packaging or other production and economic needs (clause 2);

- for the purchase of tools, fixtures, inventory, instruments, laboratory equipment, workwear (including PPE) and other property that is not depreciable property (clause 3);

- for the purchase of components and semi-finished products (clause 4);

- for the purchase of fuel, water, energy of all types, spent on technological purposes, production of all types of energy, heating of buildings, as well as costs for the production and (or) acquisition of power, transformation and transmission of energy (clause 5);

- for the acquisition of works and services of a production nature, performed by third parties, as well as for the performance of these works (provision of services) by structural divisions of the taxpayer (clause 6);

- related to the maintenance and operation of fixed assets and other property for environmental purposes (clause 7).

Expenses in the tax base, named in paragraphs, obviously need additional explanation. 6 clause 1 art. 254 of the Tax Code of the Russian Federation, – work and services of a production nature performed by third parties. But so that the category of costs associated with such works and services is not interpreted broadly, the legislator in this norm specifies the criterion that the mentioned works and services must meet. In particular, works (services) of a production nature include the performance of individual operations for the production (manufacturing) of products, performance of work, provision of services, processing of raw materials (materials), monitoring compliance with established technological processes, maintenance of fixed assets and other similar work.

Guided by tax regulations (clause 6, clause 1, article 254 and clause 5, clause 1, article 346.17 of the Tax Code of the Russian Federation) in conjunction with this criterion, officials of the Ministry of Finance allow the “simplified” to classify, for example, the following types of expenses as material expenses.

| Type of consumption | Details of letters from the Ministry of Finance |

| Payment for work performed by a third-party individual entrepreneur to monitor compliance with established technological processes | From 04.10.2017 No. 03‑11‑11/64613 |

| Payment for work performed by a third party to calculate fees for negative environmental impact, keep records of waste movement, fill out waste forms and compile and submit a report on the generation, use, neutralization and disposal of waste, which is necessary for paying pollution fees | From 04/21/2017 No. 03‑11‑06/2/23989 |

| Payment for the services of a transport organization for the delivery and forwarding of finished printed products to customers, as well as the costs of purchasing and refilling cartridges for office equipment | From 12/25/2015 No. 03‑11‑06/2/76408 |

| Payment for work performed by contractors and subcontractors | From 04/26/2016 No. 03‑11‑06/2/24019 |

| Payment for services for medical examinations of employees | From 05/05/2016 No. 03‑11‑06/2/25906 |

| Payment of utilities (for example, fees for electricity, hot and cold water, garbage collection) | From 07/11/2016 No. 03‑11‑06/2/40349 |

| Posting vacancies in newspapers, magazines and on Internet sites, if these expenses are directly related to the entrepreneurial activity of the “simplified worker” | From 08/16/2012 No. 03‑11‑06/2/111 |

| Maintenance of leased objects, if under the lease agreement these costs are assigned to the lessor | From 10.06.2015 No. 03‑11‑09/33555 |

Analysis of the above explanations showed that the qualification of certain works or services as works (services) of a production nature in order to take into account the costs of their payment in the tax base as part of material expenses also depends on the type of activity of the “simplified worker”. For example, the Letter of the Ministry of Finance of Russia dated March 17, 2014 No. 03-11-06/2/11342 literally says the following: an organization that uses the simplified tax system and conducts business activities in the field of outdoor advertising distribution has the right to take into account installation and operation costs as part of material expenses advertising structures carried out in accordance with agreements for the placement of such structures concluded with the owners of land plots, buildings or other real estate, including the owners of premises in an apartment building.

When deciding on the possibility of taking into account in material expenses the cost of certain works (services) of third parties, the “simplified” person needs to take into account not only the connection between these costs and the business activity he carries out, but also the general requirements for the recognition of expenses - the criteria named in paragraph. 1 tbsp. 252 of the Tax Code of the Russian Federation. This is stated in paragraph 2 of Art. 346.16 Tax Code of the Russian Federation. That is, the costs of paying for work or services of a production nature, like all other expenses, must be confirmed by primary accounting documents.

No cost control

Under the simplified tax system with the object of taxation “income,” the “simplified” tax should be calculated and paid on the entire amount of income received (clause 1 of article 346.18 of the Tax Code of the Russian Federation). In this case, the expenses incurred are not taken into account when calculating the tax base, and you are not required to document them. Therefore, the tax office does not check expenses under the simplified tax system with the object “income” at a rate of 6% (Letters of the Ministry of Finance of Russia dated June 16, 2010 No. 03-11-11/169, dated October 20, 2009 No. 03-11-09/353). This approach applies to both organizations and individual entrepreneurs. They are required to pay expenses. Neither your own expenses nor the expenses of suppliers are taken into account when calculating the simplified tax system at a rate of 6 percent. This, in essence, is the difference with the simplified tax system “income minus expenses”, when incurred expenses reduce the amount of tax.

What is the difference between different objects of simplified taxation?

In accordance with Art.

346.14 of the Tax Code of the Russian Federation, when switching to a simplified tax system or before the end of the next tax period, the taxpayer has the opportunity to choose one of two objects of taxation: “income” and “income minus expenses.” Here are their main differences:

| Object of taxation | simplified tax system "income" | Simplified tax system “income minus expenses” |

| Tax rate (in general) | 6% | 15% |

| Calculation basis | The amount of income determined in accordance with Art. 346.15 Tax Code of the Russian Federation | Expenses calculated in accordance with Art. 346.16 Tax Code of the Russian Federation |

EXPLANATIONS from ConsultantPlus experts: The simplified tax system with the object “income” is more profitable to use if you have small expenses. Then you will pay less tax and it will be easier to keep records than with the “income minus expenses” object. Income must be determined according to income tax rules. In general, they are taxed at a rate of 6%, but in regions there may be lower rates. Starting from January 1, 2021, a rate of 8% is provided for a number of cases... How to apply the simplified tax system with the object “income” was explained in detail by ConsultantPlus experts. To do everything correctly, get trial access to the system and go to the Ready solution.

Read about the procedure for switching from simplified tax system 6% to simplified tax system 15% in this material.

When reflecting the costs of any simplified object, it is necessary to remember that the income and expenses of simplifiers are recorded in tax accounting using the cash method (clause 1 of Article 346.17 of the Tax Code of the Russian Federation). In addition, it is necessary to comply with the general rules for recognizing expenses (Article 252 of the Tax Code of the Russian Federation): they must be economically feasible and confirmed by primary sources.

The complexity of accounting under the simplified tax system of 15% lies in the fact that the possibility of including expenses in the tax base is limited to the so-called hard list. From this point of view, accounting for the “Income” object is technically much simpler. Some types of expenses under the simplified tax system of 6% are also subject to tax accounting, reducing not the base, but the already calculated tax.

What expenses reduce tax?

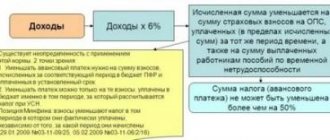

According to the rules of the Tax Code of the Russian Federation, an organization or individual entrepreneur using the simplified tax system can still reduce the simplified tax for some expenses. In the formula for calculating tax on income simplification, expenses that reduce the amount of the simplified tax system of 6% are distributed according to the following formula:

Tax = Income x 6% – Expenses

Organizations and individual entrepreneurs can reduce the “simplified” tax at a rate of 6% for the following expenses (clause 3.1 of Article 346.21 of the Tax Code of the Russian Federation):

- insurance premiums and “injury” contributions paid from employee benefits;

- temporary disability benefits paid at the expense of the employer (except for industrial accidents and occupational diseases);

- contributions for voluntary insurance of employees in case of their temporary disability (under certain conditions).

However, keep in mind that expenses will not be able to reduce the simplified tax by more than 50%.

The expenses of an individual entrepreneur under the simplified tax system of 6%, if he has no employees, can include the insurance contributions he paid in a fixed amount for compulsory pension and medical insurance “for himself.”

Compensation for the traveling nature of work.

In accordance with Art. 168.1 of the Labor Code of the Russian Federation, an employee who is constantly or regularly on the road is entitled to compensation for the traveling nature of the work. This means that the employer must reimburse such an employee for travel expenses, rental accommodation, as well as additional costs in the form of daily allowance and field allowance.

It would seem that “simplifiers” have the right to take such payments into account for taxation by virtue of Art. 255 and paragraphs. 6 clause 1 art. 346.16 of the Tax Code of the Russian Federation as compensation charges related to work hours and working conditions. After all, their payment is subject to the requirements of labor legislation.

Meanwhile, the Ministry of Finance in Letter dated December 16, 2011 No. 03‑11‑06/2/174 indicated that compensation payments are of two types:

- compensation payments related to special working conditions. These are additional payments for work with harmful and (or) dangerous working conditions, work in areas with special climatic conditions (Articles 146 - 148 of the Labor Code of the Russian Federation), overtime work, work at night, weekends and holidays, for combining positions (Article 149 – 154 Labor Code of the Russian Federation). Such payments are an integral part of wages (Article 129 of the Labor Code of the Russian Federation);

- cash payments that are aimed at reimbursing expenses incurred by an employee in the performance of work duties. The payment of such compensation is stipulated by Art. 164, 165 Labor Code of the Russian Federation. Examples include payments for the traveling nature of work when moving to work in another area (Article 168.1). As a rule, such payments compensate for the material costs of workers and are not included in the remuneration system.

Accordingly, the compensation that the employer pays to employees on the basis of Art. 168.1 of the Labor Code of the Russian Federation, due to the traveling nature of the work, should be classified in the second category of payments. As a general rule, they are of a social nature, despite the existence of labor relations, and are not included in the remuneration system: the amount and procedure for paying such compensation (as well as the list of jobs, professions, positions of employees to whom they are paid) are established by the employer’s local documents. Since compensation for traveling is not an element of remuneration, the costs of their payment are not included in the tax base when calculating the single tax (see also Letter of the Federal Tax Service of the Russian Federation dated April 4, 2011 No. KE-4-3/5226).

An alternative position on this issue is reflected in the Resolution of the Federal Antimonopoly Service of the North-West District dated November 14, 2013 in case No. A66-420/2013. In it, the arbitrators came to the conclusion that any compensation, including for the traveling nature of the work, can be attributed to labor costs.

Don't forget about the expense book

All “simplified” people are required to keep a book of income and expenses (Article 346.24 of the Tax Code of the Russian Federation). It is also called KUDiR. The booklet was approved by Order of the Ministry of Finance of the Russian Federation dated October 22, 2012 No. 135n. In this case, for example, at the simplified tax system of 6 percent, accounting for suppliers’ expenses in the Book may not be carried out, since they do not reduce the tax base.

With the simplified tax system at a rate of 6%, “income” expenses can be recorded in KUDiR - at the request of an LLC or individual entrepreneur. They, anyway, do not affect the calculation of tax.

Read also

17.04.2017