The need for Russian companies to employ workers is quite effectively solved by the possibility of inviting citizens of nearby states to work. Particularly favorable conditions are not provided here, but difficult obstacles are not created. It is for this reason that in companies and enterprises you can increasingly see workers with a foreign passport. Finding and accepting this category of employees is easy. But it doesn't end there. The employer must pay certain taxes for such employees . This is exactly what this article will discuss.

Legal provisions

The labor activity of citizens of other countries is not considered arbitrary. It has completely legitimate justifications. 114-FZ dated August 15, 1996 spells out the rules for travel across Russian borders. It states here that after arriving without official permission, invitation or visa, a person must write down the purpose of employment on the migration card. If a foreigner enters on one of the visas, he will need to receive an invitation or the visa itself must be a special one - a work visa.

Another important law is No. 115-FZ of July 25, 2002. This provision provides information about foreigners and their status. At the same time, here you can study the peculiarities of employment in the Russian economy.

Rights of foreign citizens

In accordance with paragraph 1 of Article 5 of the Federal Law of July 24, 1998 No. 125-FZ “On compulsory social insurance against accidents at work and occupational diseases” (hereinafter referred to as Federal Law No. 125-FZ), compulsory social insurance against accidents at work and occupational diseases are subject to:

- individuals performing work on the basis of an employment contract concluded with the insured;

- individuals performing work on the basis of a civil contract, the subject of which is the performance of work and (or) provision of services, an author's order contract, if in accordance with these contracts the customer is obliged to pay insurance premiums to the insurer.

- individuals sentenced to imprisonment and recruited to work by the insurer.

This law applies to both citizens of the Russian Federation and foreign citizens and stateless persons, unless otherwise provided by federal laws or international treaties of the Russian Federation.

When an insured event occurs, insurance coverage is provided:

1) in the form of a temporary disability benefit assigned in connection with an insured event and paid from funds for compulsory social insurance against industrial accidents and occupational diseases;

2) in the form of insurance payments:

a one-time insurance payment to the insured or to persons entitled to receive such payment in the event of his death;

monthly insurance payments to the insured or persons entitled to receive such payments in the event of his death;

3) in the form of payment of additional expenses associated with the medical, social and professional rehabilitation of the insured in the presence of direct consequences of the insured event

An insured event is a fact of damage to the health or death of the insured as a result of an industrial accident or occupational disease, confirmed in the prescribed manner, which entails the insurer’s obligation to provide insurance coverage (Article 3 of Federal Law No. 125-FZ)

The procedure for providing compulsory social insurance against industrial accidents and occupational diseases for persons entitled to receive it and who have left for permanent residence outside the Russian Federation is determined by Decree of the Government of the Russian Federation dated July 17, 2000 No. 529.

In accordance with Part 1 of Article 2 of Law No. 255-FZ, foreign citizens and stateless persons permanently or temporarily residing on the territory of the Russian Federation, as well as foreign citizens, are subject to compulsory social insurance in case of temporary disability and in connection with maternity and stateless persons temporarily staying in the Russian Federation and working under employment contracts.

It should be noted that the right to receive all types of benefits for compulsory social insurance in case of temporary disability and in connection with maternity (temporary disability benefits, maternity benefits, one-time benefits for women registered with medical organizations in the early stages of pregnancy, lump sum allowance for the birth of a child, monthly child care allowance, social funeral allowance) are available only to foreign citizens permanently or temporarily residing in the territory of the Russian Federation, as well as citizens of the countries of the Eurasian Economic Union (hereinafter referred to as the EAEU) temporarily staying in the Russian Federation, without any restrictions.

At the same time, Part 4.1 of Article 2 of Law No. 255-FZ establishes that foreign citizens temporarily staying (with the exception of citizens of EAEU countries) on the territory of the Russian Federation have the right to receive only temporary disability benefits and subject to the payment of insurance contributions for them by their employers. Social Insurance Fund of the Russian Federation for a period of at least six months preceding the month of the onset of temporary disability.

FAQ:

Question: Can I count on temporary disability benefits if I work under a patent, but an employment contract has not been concluded with me?

Answer:

The provisions of Article 2 of Law No. 255-FZ establish that persons working under employment contracts are subject to compulsory social insurance in case of temporary disability and in connection with maternity. The right to provide temporary disability benefits will arise only if an employment contract is concluded and the employer pays insurance contributions to the Social Insurance Fund of the Russian Federation;

Question: I am a citizen of Ukraine, I worked under a patent (I am temporarily staying in the territory of the Russian Federation), I am currently on maternity leave, and in a month I will have a temporary residence permit ready. Please tell me - can I apply for maternity benefits in this situation from the moment I receive temporary resident status?

Answer:

You will acquire the right to receive compulsory social insurance benefits in case of temporary disability and in connection with maternity in accordance with Law No. 255-FZ for insured events that occur after the date of your receipt of a temporary residence permit in the territory of the Russian Federation. Since in this situation pregnancy and childbirth occurred before you received a temporary residence permit, you do not have the right to this benefit.

Question: I am a citizen of Uzbekistan, have received a temporary residence permit on the territory of the Russian Federation, will I be entitled to a lump sum benefit upon the birth of a child?

Answer

: If you work under an employment contract and you have a temporary residence permit on the territory of the Russian Federation, then you have the right to receive a lump sum benefit upon the birth of a child (Article 2 of Law No. 255-FZ).

Question: I am a citizen of Ukraine who has received temporary asylum on the territory of the Russian Federation, and I am currently applying for a temporary residence permit. Officially employed in the Russian Federation. I am currently 5 months pregnant. Tell me, what benefits will I be entitled to if I receive a temporary residence permit?

Answer:

If you work under an employment contract and receive a temporary residence permit in the Russian Federation before receiving a certificate of incapacity for pregnancy and childbirth, then you will be entitled to maternity benefits and a one-time benefit for women registered with medical organizations in the early stages of pregnancy . Regardless of whether you have a sick leave certificate, you also have the right to a lump sum benefit for the birth of a child and a monthly child care benefit.

Question: Are foreign citizens subject to registration as insurers with the Social Insurance Fund of the Russian Federation?

Answer: In accordance with Article 13 of Federal Law No. 115-FZ of July 25, 2002 “On the Legal Status of Foreign Citizens in the Russian Federation,” a foreign citizen registered in the Russian Federation as an individual entrepreneur can act as an employer.

Based on Article 6 of Law No. 125-FZ of the Federal Law of July 24, 1998 No. 125-FZ “On compulsory social insurance against accidents at work and occupational diseases” (hereinafter referred to as Law No. 125-FZ), individuals are subject to registration as insurers who have entered into an employment contract with an employee, or a civil contract, the terms of which provide for the obligation of the policyholder to pay insurance premiums for compulsory social insurance against industrial accidents and occupational diseases (hereinafter referred to as the civil contract).

Simultaneously with registration as insurers for compulsory social insurance against accidents at work and occupational diseases in accordance with Law No. 125-FZ, individuals who have entered into an employment contract with an employee are registered for compulsory social insurance in case of temporary disability and in connection with maternity ( Article 2.3 of the Federal Law of December 29, 2006 No. 255-FZ “On compulsory social insurance in case of temporary disability and in connection with maternity”).

Thus, if an individual, including a foreign citizen registered in the Russian Federation as an individual entrepreneur, uses hired labor, then such a person is obliged to register as an insurer, as well as calculate and timely pay insurance contributions to the Social Insurance Fund of the Russian Federation. Federation.

Question: What documents must be submitted to a foreign citizen using hired labor to register as an insurer with the Social Insurance Fund of the Russian Federation?

Answer: In accordance with Article 13 of Federal Law No. 115-FZ of July 25, 2002 “On the Legal Status of Foreign Citizens in the Russian Federation,” a foreign citizen registered in the Russian Federation as an individual entrepreneur can act as an employer.

In accordance with Article 6 of the Federal Law of July 24, 1998 No. 125-FZ “On compulsory social insurance against accidents at work and occupational diseases” (hereinafter referred to as Law No. 125-FZ) to individuals, including foreign citizens registered in the Russian Federation Federation as individual entrepreneurs, you must register as an insurer with the territorial body of the Fund at your place of residence no later than 30 calendar days from the date of concluding an employment (civil law) contract with the first of the hired employees.

Article 26.28 of Law No. 125-FZ establishes measures of liability for the policyholder for failure to fulfill or improper performance of the duties assigned to him for timely registration as a policyholder with the Fund.

Registration as an insurer - an individual, including a foreign citizen registered in the Russian Federation as an individual entrepreneur who has entered into an employment (civil) contract with an employee, is carried out on the basis of an application for registration, the form of which is provided for accordingly by the Administrative Regulations of the Social Insurance Fund of the Russian Federation for the provision of public services for registration and deregistration of policyholders - individuals who have entered into an employment contract with an employee, approved by Order of the Fund dated April 22, 2019 No. 215 (hereinafter referred to as Regulation No. 215), and the Administrative Regulations of the Social Insurance Fund of the Russian Federation for provision of public services for registration and deregistration of policyholders - individuals obligated to pay insurance premiums in connection with the conclusion of a civil contract, approved by Order of the Fund dated April 22, 2019 No. 214 (hereinafter referred to as Regulation No. 214).

Simultaneously with the application for registration, the individual entrepreneur-employer submits copies of the following documents:

— work books of accepted employees or employment contracts concluded with employees (subparagraph “a” of paragraph 15 of Regulation No. 215);

— civil contracts with individuals, if they contain conditions that the policyholder is obliged to pay insurance premiums for compulsory social insurance against industrial accidents and occupational diseases for these individuals (subparagraph “a” of paragraph 15 of Regulation No. 214).

Based on the application for registration and copies of documents, the territorial body of the Fund, within a period not exceeding three working days from the date of receipt of the last document necessary for registration of the policyholder, registers him as a policyholder.

Question: Can foreign citizens voluntarily enter into legal relations under compulsory social insurance in case of temporary disability and in connection with maternity?

Answer: In accordance with Part 3 of Article 2 of the Federal Law of December 29, 2006 No. 255-FZ “On compulsory social insurance in case of temporary disability and in connection with maternity” (hereinafter referred to as Law No. 255-FZ), individuals, including foreign citizens registered in the Russian Federation as individual entrepreneurs are subject to compulsory social insurance in case of temporary disability and in connection with maternity if they voluntarily entered into a relationship under compulsory social insurance in case of temporary disability and in connection with maternity (hereinafter referred to as legal relations for compulsory social insurance) and pay insurance premiums for themselves in accordance with Article 4.5 of the Law

No. 255-FZ.

The application form for entering into legal relations under compulsory social insurance is provided for by the Administrative Regulations of the Social Insurance Fund of the Russian Federation for the provision of state services for registration and deregistration of persons who voluntarily entered into legal relations under compulsory social insurance in case of temporary disability and in connection with maternity, approved by order of the Foundation dated April 22, 2019 No. 216.

Taking into account the provisions of Article 4.5 of Law No. 255-FZ, persons who voluntarily entered into legal relations under compulsory social insurance acquire the right to receive insurance coverage in the next calendar year, subject to their payment of insurance premiums no later than December 31 of the current year, starting from the year of filing the application for voluntary entering into these legal relations.

Question: At what rate are insurance premiums calculated for the two types of compulsory social insurance for payments to foreign citizens working in Russia?

Answer: 1. The procedure for calculating insurance premiums for industrial accidents and occupational diseases is regulated by Federal Law No. 125-FZ of July 24, 1998 “On compulsory social insurance against industrial accidents and occupational diseases” (hereinafter referred to as Law No. 125-FZ) .

Paragraph 2 of Article 5 of Law No. 125-FZ establishes that the effect of this Federal Law extends, in particular, to foreign citizens and stateless persons, unless otherwise provided by federal laws or international treaties of the Russian Federation. Consequently, foreign citizens, regardless of their migration status, are also subject to compulsory social insurance against industrial accidents and occupational diseases.

In accordance with Article 20.1 of Law No. 125-FZ, the object of taxation with insurance premiums is payments and other remuneration accrued by policyholders in favor of the insured within the framework of labor relations and civil contracts, the subject of which is the performance of work and (or) provision of services, author's order agreements , if, in accordance with these contracts, the customer is obliged to pay insurance premiums to the insurer.

Thus, a foreign citizen is an insured person from the moment of concluding the relevant agreement with the employer.

Insurance premiums are charged at the rate established by the policyholder - the employer for the current year, depending on the main type of activity carried out by the employer.

2. In accordance with Article 420 of the Tax Code of the Russian Federation (hereinafter referred to as the Tax Code of the Russian Federation), payments and other remuneration in favor of individuals, including foreign citizens, subject to compulsory social insurance in accordance with federal laws on specific types compulsory social insurance.

Article 425 of the Tax Code of the Russian Federation establishes the tariffs of insurance contributions for compulsory social insurance in case of temporary disability and in connection with maternity (hereinafter referred to as VNIM).

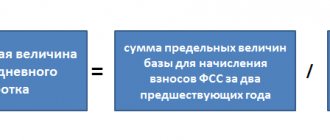

Insurance contributions for compulsory social insurance in case of VNIM are charged within the established maximum base value:

- at a tariff of 1.8% in relation to payments and other remuneration in favor of foreign citizens and stateless persons temporarily staying in the Russian Federation (with the exception of highly qualified specialists in accordance with Federal Law of July 25, 2002 No. 115-FZ “On the Legal Status foreign citizens in the Russian Federation");

— at a tariff of 2.9% in relation to payments and other remuneration in favor of foreign citizens of all categories (including highly qualified specialists) who are citizens of the EAEU member states (Belarus, Kazakhstan, Armenia, Kyrgyzstan).

Employment algorithm

The general procedure for applying for a job varies significantly depending on the situation. Circumstances such as:

- Received official status;

- Arrival time.

The best option would be to hire citizens who have a temporary residence permit, residence permit, or those who have received refugee status. Another suitable candidate could be a person from the EAEU countries. It is quite simple to sign an agreement with this category of citizens. Within three working days, information about such employees is transmitted to special authorities that monitor employment.

In order to hire individuals who are nationals of “visa” countries, you need to obtain special permission to attract such specialists. The received invitation is sent to the applicant, after which he will need assistance in the visa application process.

Employment of citizens living in visa-free countries is accompanied by less hassle. They themselves receive the necessary documents, among which the patent deserves special attention.

Personal income tax rates for foreigners

The tax rate on income received in favor of a foreign citizen from Russian sources is 30%.

In practice the following rates are used:

| Category | Bet size |

| Tax residents | 13% from all income |

| Foreign citizens with refugee status, with a temporary residence permit, from the EAEU countries | 13% from wages, 15% from dividends |

| Dividends of a legal entity of the Russian Federation, the founder of which is a citizen of another state permanently residing in his homeland | will be reduced by 15%, and all other income by 30% |

If the status of a foreign worker changes during a calendar year from non-resident to resident, then the previously withheld personal income tax will be recalculated at a preferential rate of 13%.

Registration of an employment agreement

Established legislative standards do not exempt from the need to comply with the requirements of the modern Labor Code of the Russian Federation. Invited employees are also not deprived of social protection.

Agreements concluded with foreigners must be drawn up with the understanding that the established provisions should not worsen the general working conditions of the employee.

Important! Regardless of citizenship, the requirements of the Labor Code of the Russian Federation must be complied with without fail.

This directly concerns the legal conditions in the process of signing fixed-term employment contracts. As judicial practice has shown, it is better for an employer to enter into contracts that do not have a time limit.

Deductions for foreigners

Every head of an organization and large enterprise understands perfectly well that after hiring a foreigner, he is required to pay certain taxes.

Citizenship in such a situation does not matter. It is important what deductions he needs to pay, when to transfer the necessary amounts and what rates to use .

The issue directly related to the deduction of the necessary amounts is considered very important. The reason is that the taxation of a Russian employee and a foreigner is different. Equal rates apply to the salary of a Russian citizen in any place of residence. As for foreigners, deductions depend on the status and time of stay in the country.

The main tax rates are presented in this table:

| Type of deduction | Employee status | Resident/with residence permit | Non-resident/temporarily staying in the Russian Federation |

| Personal income tax | Invitees from visa countries | 13% with recalculation of previously paid 30% | 30% |

| Highly qualified specialists (HQS) | 13% | 13% | |

| Visitors from visa-free countries | 13% with deduction for patent payment | 13% | |

| Citizens of EAEU countries | 13% | 13% | |

| PFU | All foreign employees (except HQS) | 22% | 22% |

| VKS | 22% | 0% | |

| Compulsory medical insurance | All foreign employees (except HQS) | 5.1% with VHI policy | 0% (with VHI policy) |

| FSS | All foreign employees (except HQS) | 2,9% | 1,8% |

| VKS | 2,9% | 0% |

Each head of an enterprise in the process of accepting foreigners must understand that from the date of registration he bears legal responsibility for everyone. At the same time, he becomes their official tax agent.

The costs associated with remuneration do not consist only of the part that is transferred to the employee. There are other statutory deductions.

Standard procedure for paying taxes and insurance premiums

Not every foreigner is destined to get a job in Russia. Moreover, your very stay in the country may be a big question. The fact is that migration legislation clearly classifies foreigners and dictates the procedure for their stay in the Russian Federation.

- The first category is foreign guests temporarily staying in Russia. There are no special requirements for them regarding the preparation of permits: representatives of the law will be satisfied with the presence of a migration card. Under these conditions, migrants can stay in the Russian Federation for no more than 90 days in each half-year, and if their stay is more than 7 days, they are required to register with the migration authorities. If a foreign citizen expects to live in Russia for more than 90 days, he will smoothly move to the next category, the representatives of which are subject to more stringent requirements.

- The second category is foreigners temporarily residing in Russia. They differ from the former not only in the period of stay, but also in the obligation to obtain a temporary residence permit (hereinafter referred to as TRP). This document will get rid of the title of illegal immigrant and claims from migration authorities.

- The third category is foreigners who permanently live in Russia. A person falls into this group when he has in his hands a document so desired by many - a residence permit (hereinafter - residence permit). It is believed that holders of residence permits are citizens of the Russian Federation. However, this is often what happens: obtaining a residence permit is followed by an application for Russian citizenship.

There is an opinion that having a residence permit greatly simplifies the job search process. There is some truth in this: it just so happens that there is much more trust in those foreigners who permanently reside in the Russian Federation. But this does not eliminate fierce competition and, alas, does not scare off other applicants.

The legislation does not prohibit concluding an employment contract with a migrant who does not have a residence permit, but has a temporary residence permit. By and large, the employer does not care which of the above categories the potential employee belongs to. At least from the point of view of calculations with the budget, nothing will change: insurance premiums for temporarily residing foreigners in 2021 are made in the same manner as before, the calculation and payment of income tax is still mandatory.

True, with personal income tax everything is a little more complicated. The rate of this tax is not always equal to the usual 13%; in some cases its size is adjusted. For example, the rate may vary depending on whether the foreigner is a tax resident of the Russian Federation, whether he belongs to special categories of citizens, and so on. It is highly desirable for the employer to know about all these nuances in order to correctly calculate, withhold and pay taxes on the salaries of foreigners to the budget.

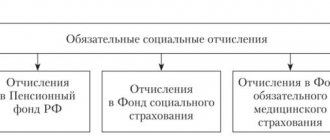

Contributions to the Social Insurance Fund

Special insurance funds are regulated. It is stated here that every visitor to the territory of the Russian Federation is insured from the first day of his stay. Applicants can provide such insurance with a VHI policy in their possession. It also covers possible accidents.

As soon as the employer enters into an employment agreement, the process of assessing insurance contributions for foreign citizens is carried out according to a scheme that coincides with that for Russian employees.

Personal income tax on the income of a foreigner from the EAEU

If you involve foreigners from EAEU member countries (Belarusians, Kazakhs, Kyrgyz, Armenians) in your work, then consider the following rules:

- From the first day of their work on the territory of the Russian Federation, the income of such citizens is taxed at a personal income tax rate of 13% (Article 73 of the Treaty on the Eurasian Economic Union of May 29, 2014, clause 1 of Article 224 of the Tax Code of the Russian Federation).

- At the end of the year, the final tax status of an individual is determined depending on the time of his stay in the Russian Federation (Resolution of the Constitutional Court of the Russian Federation dated June 25, 2015 No. 16-P).

As for the standard deductions used when calculating personal income tax, foreign employees from the EAEU have the right to use them only after acquiring the status of a tax resident of the Russian Federation (Letter of the Ministry of Finance dated June 15, 2018 No. 03-04-05/40970).

The Ministry of Finance believes that if at the end of the year a foreigner from the EAEU has not acquired the status of a tax resident of the Russian Federation, then the personal income tax on his income from employment for the entire period from the beginning of the year should be recalculated at a rate of 30% (Letter of the Ministry of Finance dated February 18, 2020 No. 03-04 -07/11392). Tax officials do not agree with this ─ The Federal Tax Service sees no reason to recalculate the tax at the end of the year if the status of a citizen from the EAEU has changed (Letter of the Federal Tax Service dated November 28, 2016 No. BS-4-11 / [email protected] ).

The Ministry of Finance in Letter No. 03-04-06/74275 dated August 25, 2020 also clarified that after the dismissal of a foreign employee from the EAEU, there is no need to recalculate personal income tax withheld at a rate of 13% if no payments are made to him after the date of dismissal.

Foreigners who are citizens of the EAEU may not receive confirmation of their tax status from tax authorities. The employer himself will determine it on the basis of a copy of the pages of the passport with marks from the border control authorities about crossing the border (Letter of the Federal Tax Service dated June 10, 2015 No. OA-3-17 / [email protected] ).

Health insurance

After arriving in populated areas of Russia, every guest of the country must take out a VHI policy . Thanks to this, two main issues can be solved simultaneously:

- The foreigner receives emergency medical care if necessary.

- The state will easily reimburse the funds spent on the treatment of a guest of the country.

Important! It is prohibited to conclude an employment contract without presenting a VHI policy.

Despite the presence of such a policy in the hands of a foreigner, each employer must exercise additional control over employees. Provide them with the assistance they need.

Contributions to the Pension Fund

Necessary pension insurance is mandatory for all Russians and for foreigners who come to work . The only exceptions are those citizens who belong to the VSK category. For such categories that have the status of residence permit and temporary residence permit, payment of contributions to the Pension Fund is considered mandatory.

The employer must also contribute the required amounts for those migrants who arrived from visa-free countries. For a labor patent, 22% is deducted. This is the size of the insurance portion. Another 10% additional charges are added to it.

Transfers to the Social Insurance Fund

We are talking about accruals that insure against accidents. All employees who come from other countries that have signed the required employment agreement must be insured against various possible accidents and unpleasant situations.

Based on this rule, it becomes clear that employees’ salaries are required to contribute special amounts to the Social Insurance Fund. Their size depends on the risk. If a citizen plans to work under a civil contract, he must insure himself. The amounts of deductions are specified in the executed GPA.

A foreigner temporarily staying on the territory of the Russian Federation

Foreign citizens temporarily staying on the territory of the Russian Federation are divided into two subcategories:

- temporarily staying in the Russian Federation on the basis of a visa;

- temporarily staying in the Russian Federation in a manner that does not require a visa.

Foreigners temporarily staying in the Russian Federation on the basis of a visa

If a foreign citizen comes to Russia to work, he is issued an ordinary work visa. As a general rule, such a visa is issued for the duration of an employment contract or a civil contract for the performance of work (provision of services), but not more than for one year.

Employers and customers of work (services) who employ such foreigners are required to notify the territorial body of the Ministry of Internal Affairs about the conclusion and termination (termination) of employment contracts or civil contracts with them for the performance of work (rendering services). The notification period is no later than three working days from the date of conclusion or termination (termination) of the relevant agreement (paragraph 1, clause 8, article 13 of Law No. 115-FZ).

Payroll tax

According to the legislation of the Russian Federation, transfers required for compulsory social insurance for employees are paid by the employer. Only personal income tax is deducted from the salary received. This rule applies to all categories of employees - Russians and foreigners.

Expert opinion

Accordingly, each hired foreigner must remit special income tax from the salary received. Such transfers are paid both by the mercenary and the founder of the economic community. In all situations, regardless of activity, the transfer amount must be equal to 30%.

Employee of the Federal Tax Service, Yekaterinburg, Semenov Ivan Stepanovich.

Table of tariffs for insurance premiums on the income of foreign workers

Insurance premium rates in 2021 for foreign employees are presented in the table:

| Foreign employee status | Contributions to compulsory pension insurance, % | Contributions to compulsory social insurance in case of VNIM, % | Contributions for compulsory health insurance, % | ||

| With income within 1,292,000 rubles. | From incomes over 1,292,000 rubles. | With income within 912,000 rubles. | With income over 912,000 rubles. | ||

| Citizens from the EAEU | 22 | 10 | 2,9 | — | 5,1 |

| Permanently and temporarily residing citizens | 22 | 10 | 2,9 | — | 5,1 |

| Temporarily staying citizens | 22 | 10 | 1,8 | — | — |

| Highly qualified specialists permanently or temporarily residing | 22 | 10 | 2,9 | — | — |

| Highly qualified specialists temporarily staying | — | — | — | — | — |

Thus, contributions for payments to foreigners (not HQS), permanently or temporarily residing in the Russian Federation, are calculated in the same way as for Russians (Letter of the Ministry of Finance dated January 28, 2020 No. 03-15-06/4835).

For foreigners-HQS, permanently or temporarily residing in the Russian Federation, contributions to compulsory medical insurance and VNiM are paid according to the same rules as for Russians, with the exception of contributions to compulsory medical insurance - they do not need to be paid (Letter of the Ministry of Finance dated 02/04/2020 No. 03-15-05 /6890).

Transfer calculation scheme

Situations related to hiring foreigners are quite diverse. They cannot be brought under a general scheme. The size of the required insurance contributions differs especially greatly. The amount of transfers directly depends on the general status of citizens. They are divided into categories:

- Labor migrants who came from visa-free countries, from the CIS and EAEU countries. This does not include VSK and those who have documented the right of residence.

- Qualified employees temporarily living in the Russian Federation.

- Professionals who have the right to live in Russia.

- Employees who came from a visa country.

Tariffs for contributions for citizens of the first group are completely the same as those for Russians. In this category, hired foreigners who have received a residence permit are equal. Those who did not take care of having a temporary residence permit or residence permit pay smaller amounts under the Social Insurance Fund.

Fine for non-payment

The modern Tax Code of the Russian Federation establishes objects of taxation and payers, that is, residents and, accordingly, non-residents. This suggests that the level of responsibility for violating the rules applies to everyone who profits from the property.

Important! Violation of such rules is expressed in failure to comply with established deadlines and refusal to transfer taxes.

Due to the fact that the head of the enterprise who hired the foreigner acts as his tax agent, he must perform the required functions. Taxes are transferred on income received. Fines imposed for violations in this area are paid accordingly.

If a citizen who is considered a non-resident has not registered his income and transferred it to the treasury, he will be subject to financial and administrative responsibility. In particularly serious cases, criminal liability will be imposed. Trying to avoid punishment by leaving Russia will not bring the desired result.

Tax debts are strictly verified and regulated by law. Russia has concluded many official agreements with other states. They are aimed at assisting in international fiscal as well as standard administrative proceedings. Such treaties and agreements regulate issues directly related to double tax deductions.

Personal income tax on the income of foreigners working under a patent

The employer is obliged to calculate personal income tax in relation to all income of a foreigner, the source of which he is (clause 2 of article 226 of the Tax Code of the Russian Federation).

The personal income tax rate and the procedure for calculating tax on the income of foreigners working in the Russian Federation under a patent are determined according to the norms of clause 2 of Art. 210, paragraph 1 and paragraph 3 of Art. 224 of the Tax Code of the Russian Federation, taking into account clarifications from the Letter of the Ministry of Finance dated June 13, 2017 No. 03-04-05/36673.

Thus, a single personal income tax rate of 13% applies to residents and non-residents, but the procedure for calculating the tax differs. At the same time, foreign employees, whose income is subject to a personal income tax rate of 13% from the first day of work in the Russian Federation, are not entitled to any deductions for this tax. They can be provided only after a foreign employee acquires the status of a tax resident of the Russian Federation.

Let us recall that foreigners with a patent independently pay fixed advance payments and have the right to apply to the employer to reduce the amount of personal income tax by their amount (clause 6 of Article 227.1 of the Tax Code of the Russian Federation).

Popular questions

Modern business managers who need to employ citizens of other countries ask many different questions online. The most common ones include the following.

Question 1. Under what conditions can citizens of Kazakhstan be employed in a company?

These countries have established a loyal visa-free regime. Residents of these states can work under a patent. Recently, a special EAEU was organized. Kazakhstan is included in a similar composition. Therefore, its residents are hired on fairly favorable terms.

Question 2. What are the features of employment and payment of taxes for Belarusians and citizens of Kyrgyzstan?

Russia has concluded a special agreement with these republics regarding the creation of an official Union State Community. To hire these people, it is enough to follow the standard scheme. Employees can fully enjoy the rights inherent in the EAEU. You can work without an official patent. And the salary received will be reduced only by 13% - personal income tax.

Employer mistakes

Employment-related tax transactions are considered quite complex. For this reason, managers have many questions and make various mistakes. Here are the most important of them.

Mistake 1. When arranging a job for a refugee, special conditions are not provided.

It is worth remembering that this category of citizens does not just come to the country for the purpose of employment. Citizens are forced to leave their homes for certain reasons; they seek protection in the cities of the Russian Federation. This category of workers is entitled to all necessary social security. Also, the taxation of their salary should be the same as that of citizens of the Russian Federation.

Error 2. Organizational managers do not take out insurance for employees immediately after they are hired.

Previously, there was no mandatory full social insurance for foreign employees. But this situation has changed since 2017. Today, all foreign employees without exception are subject to insurance. The duration of the employment agreement is not important here. Insurance is issued from the date of employment.