Accounting for cash transactions

Every organization that handles cash must have a cash register. The room for it must be made in such a way as to ensure complete safety of cash. The cashier is responsible for carrying out cash transactions. An agreement on financial liability must be concluded with him.

All companies are required to store their funds in credit institutions. Cash received at the cash desk can only be spent on the purposes for which it was received. A company can only keep money on hand within a certain limit set by the director of that company. As soon as the cash exceeds this limit, it must be handed over to a credit institution.

To record cash transactions, the “cash” account (50) is used. He is active. It means that:

- its balance indicates how much free cash is in the cash register at the beginning of the month:

- loan turnover shows the amounts that were disbursed from the cash desk;

- debit turnover - amounts that were deposited into the cash register.

In the last two cases, monetary documents, both accepted and issued, are also indicated.

The following subaccounts exist in the cash register account:

- organization's cash desk (50-1) - needed to take into account cash in the cash register when the company makes cash transactions using a non-national currency. In order to be able to separately account for each foreign currency, it is necessary to open the appropriate number of sub-accounts.

- operating cash desk (50-2) - used to take into account the availability and movement of money in the cash desks of ports, train stations, post offices, and so on.

- monetary papers (50-3) – necessary to take into account monetary documents stored in the cash register. Such documents are: tickets for various transport, vouchers, forms, stamps and others.

The following receipts can be recorded in the cash account:

- from an account with a credit institution;

- return of balances of amounts issued on account;

- founders' contributions;

- debt repayment by debtors;

- return of loans and credits;

- income from product sales;

- compensation for shortages and damage to property;

- surpluses identified during the inventory;

- funds from buyers for shipment of products;

- income from the sale of intangible and tangible assets.

The following expenses are also taken into account in this account:

- money given to accountable employees;

- payment to sellers;

- payment of duties and taxes;

- depositing money into an account with a credit institution;

- shortages identified during the inventory;

- issuance of various benefits and scholarships;

- issuing wages to employees;

- transferring cash to the bank through collection;

- issuance of deposited salaries.

Accounting info

Cash transactions are operations related to the receipt, storage and expenditure of various funds received by the organization's cash desk from the servicing bank. The receipt of funds to the cash desk from the current account in accounting is reflected by the following entry:Debit account 50 “Cash”, Credit account 51 “Current account”.

Primary documents:

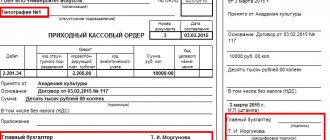

1) cash receipt order (to register the operation of cash receipts at the cash desk for any reason from one person);

2) expense cash order (to register the issuance of cash from the cash register to one person for any needs);

3) cash book;

4) payroll;

5) a journal for registering incoming and outgoing cash orders;

6) a book of accounting for money accepted and issued by the cashier for reporting to public distributors of wages and transactions to cashiers.

Changes to the accounting of cash transactions from June 1, 2014.

Incoming cash orders and receipts for them, as well as outgoing cash orders must be filled out without marks, clearly and clearly. The book of the cashier-operator must be numbered, laced and sealed with the signatures of the chief accountant and the head of the enterprise. The organization's seal must appear on each cash document.

The maximum amount that can be in the cash register is determined by the limit. The limit is set centrally.

All facts of receipt and issue of cash at the cash desk are recorded in the cash book (standard form). It must be numbered, laced, sealed with a wax seal and certified by the signatures of the director and chief accountant. Records in it are kept in 2 copies using carbon paper. The second copy (tear-off) is the cashier’s report; it is transferred to the accounting department with receipts and expenses documents every day at the end of the working day.

Accounting for current account transactions

The bank accepts, issues and non-cash transfers using documents of a specific form. Main documents:

1) for cash payments:

a) cash check;

b) an announcement for a cash contribution;

2) for non-cash payments:

a) acceptance form (consent to payment) of settlements (settlements with payment requests; valid to the bank for 10 days);

b) settlements by payment orders;

c) letter of credit form of payment (application for letter of credit), this is a transfer on behalf of the enterprise of an advance to the bank for payment upon presentation of shipping documents by the supplier to its bank;

d) statement of refusal of acceptance;

e) collection payment order - for direct debiting of funds from the company’s account in cases established by law;

f) memorial bank order - used to write off or credit non-cash funds to the company’s account by order of the servicing bank.

The main form of non-cash payments is acceptance (settlement by payment requests). The supplier, through the mediation of the bank, receives money from the payer on the basis of payment documents.

Collection is an order to the bank to collect an amount from the buyer.

Acceptance – there are different types of acceptance (preliminary, subsequent, etc.). If the payer does not refuse to accept within 3 days, the payment request is considered accepted, but the refusal must be documented.

Advice is an official bank notice about a settlement transaction performed (about the transfer of funds from the payer’s account to the supplier’s account).

Typical transactions for cash receipts and expenditures:

1) receiving cash from the bank:

Debit account 50 “Cash”, Credit account 51 “Current account”;

2) payment by the accountable person of the balance of unused funds:

Debit account 50 “Cash”,

Credit to account 71 “Settlements with accountable persons”;

3) repayment of the buyer’s debt for goods, works, services:

Debit account 50 “Cash”,

Credit to account 62 “Settlements with buyers and customers”;

4) repayment of debt for shortages and thefts:

Debit account 50 “Cash”,

Credit to account 73 “Settlements with personnel for other operations”;

5) capitalization of surpluses identified as a result of inventory (audit) of the cash register:

Debit account 50 “Cash”, Credit account 91 “Other income and expenses”;

6) receiving cash in foreign currency from the bank:

Debit account 50 “Cash”, Credit account 52 “Currency account”;

7) contribution by the accountable person of the balance of unused funds:

Debit account 50 “Cash”,

Credit to account 71 “Settlements with accountable persons”;

reflection of payments to employees from the cash register (salaries, social benefits, income from participation in the authorized capital, etc.):

reflection of payments to employees from the cash register (salaries, social benefits, income from participation in the authorized capital, etc.):

Debit account 70 “Settlements with personnel for wages”, Credit account 50 “Cash”.

Comments:

- In contact with

Download SocComments v1.3

| Next > |

The procedure for performing cash transactions

Each cash transaction must be carried out in compliance with the following order:

- Preparation of primary documentation (receipt or expense).

- Registration of cash documents in a special registration journal.

- Making entries in the cash book (made using carbon copies and in duplicate).

- Calculation of cash balance in the cash register at the end of each working day.

- Transferring the cashier's report (the second copy of the sheet from the cash book) to the accounting department along with documents on receipts and expenses. This is done against signature.

Read more about the procedure for conducting cash transactions in the article.

Documentation of cash transactions

When cash is received, cash orders are used, filled out according to f. 0310001; for expenses - expense orders according to f. 0310002. In this case, individual entrepreneurs may not draw up cash documents (orders) and registers (cash book), as mentioned in paragraphs. 4.1, 4.6 Instructions.

The preparation of cash documents is entrusted to the chief accountant, as well as to the accountant, cashier, or other person (official or individual entrusted with accounting), whose responsibilities include conducting cash transactions. The manager draws up cash documents if there is no chief accountant, cashier or other person authorized to conduct cash transactions on staff (at the workplace) (clause 4.2 of the Directive).

Cash register documents are signed by the chief accountant or an authorized accountant and cashier, and in their absence, by the head of the enterprise. The cashier must have his own seal with details confirming the conduct of cash transactions, and sample signatures of officials authorized to sign cash documents.

If there is a senior cashier on staff, then the fact of his transfer/acceptance of money to/from the cashier is reflected in the cash book according to f. 0310005. Each entry on the movement of funds between the senior cashier and cashiers is confirmed by their signatures.

A special place (room) is allocated for the cash register, in which the safety of both cash and cash documents can be ensured.

The responsibilities of the cashier include not only counting the cash received at the cash desk, but also checking the cash document for compliance with the sample, the presence of reliable signatures and the accuracy of the indicated amount. In addition, the availability of supporting documentation listed in the order is checked. Cash is accepted by counting, and the person depositing funds into the cash register must observe the counting process.

Accounting for cash received at the cash desk is kept in the cash book, prepared according to f. 0310004. In this case, each entry in this register is made by the cashier on the basis of each cash order (f. 0310001 and 0310002). The cashier must withdraw the balance in the cash register at the end of each working day - the final entry is made in f. 0310004 and certified by his signature. If there were no cash transactions during the day, then no entries are made in the book.

At the end of his working day, the cashier must verify all entries made in f. 0310004, with the available cash documents, withdraw the balance and put your signature. Also, the reconciliation must be carried out and signed in the book by the chief accountant or responsible accountant.

Cash documents and registers can be issued in paper or electronic form. In this case, paper documents can be drawn up using typewriting or filled out by hand. Signatures on paper documents must be affixed by hand.

Corrections cannot be made to cash documents. Corrections in registers are acceptable, but it is necessary that the date of the correction be indicated, as well as the initials and signature of the employee making the corrections.

To prepare cash documents and registers in electronic format, special technical means are used to ensure the protection of records from unauthorized corrections and distortions of information, as well as to identify the responsible person. Once such documents have been digitally signed, they cannot be corrected.

Necessary for accounting. accounting documents

For accounting of cash transactions, the following primary documentation is used:

- arrival orders;

- expenditure orders;

- a journal in which all orders for receipts and expenses are recorded;

- cash book;

- a book in which a record of all money issued and accepted by the cashier is kept.

The cashier's reporting is the basis for entries in the "cash" account.

To record cash transactions, statement No. 1 is used, as well as order journal No. 1. They are filled out in accordance with the information from the cashier's reports. One line is allocated for each report in the registers. Moreover, the period for which the report was compiled does not matter. The number of reports submitted and the number of lines written in the journal must match exactly. If a small number of documents are received at the cash desk every day, entries in the register can be made not every day, but every three to five days, according to several cashier reports at once. With this filling method, the start and end dates for which entries are made are written in the “date” field.

The results for one working day (or several days at once) are calculated by calculating the amounts of identical transactions specified in the reporting or other papers attached to it.

The balance of cash in the cash register is recorded in the statement at the end and beginning of the month. To control cash during the month, information about cash balances indicated in the cashier’s report is used.

What is a cash limit

Correct cash reporting consists of several concepts. One of them is the cash limit. This concept refers to the amount of cash that is allowed to be kept inside the cash register at the end of the operating period. Any amount exceeding this limit must be deposited with an approved bank with which the company cooperates.

The value of the presented amount is approved by the company, based on the type of business and accounting for incoming and outgoing flows of funds, as well as taxation: individual entrepreneur on the simplified tax system or LLC on UTII, etc. Representatives of individual entrepreneurship and small businesses have the right to refuse to apply the cash limit rule.

Exceeding the limit is allowed only for the period of payment of salaries to employees of the institution or other payments of financial resources to contractors, banks, clients and similar counterparties. This rule also applies to receiving financial support from banks and other financial institutions. This is only relevant if the organization conducts cash transactions on such days. At this time, the institution and its responsible officials will not be assessed fines if the established cash limit is exceeded.

Expert opinion

Tatyana Nikolaevna

Chief Accountant

Ask a Question

The concept of a limit on cash payments between institutions and individual entrepreneurs has been introduced. The official limit is set by the state at 100 thousand rubles. This is clearly seen from the following example: an institution purchases some goods from another company with a total cost of 150 thousand rubles. The rules for the balance of 100 thousand rubles are observed. The amount exceeding this value is transferred to the seller to a non-cash account. This allows you to work within the framework of the law and conduct business transparently for government inspection services.

Basic entries in accounting

It is worth considering the main standard entries for accounting for cash transactions used in accounting:

- D50 – K51 – cash was received at the cash desk from the company’s account with a credit institution.

- D50 – K91 – the company’s partner paid the rent.

- D50 - K62 - the cash register received cash from customers for the goods they purchased.

- D50 - K71 - the reporting employee returned the unused cash.

- D50 - K73-2 - a company employee deposited money into the cash register as repayment of a debt on a loan received or as repayment of damage caused.

- D50 – K75-1 – the founder contributed cash to the cash desk as a contribution to the organization’s management company.

- D50 – K91-1 – the person paid for the temporary use of the company’s property.

- D50 - K91-1 - during the inventory of the cash register, excess cash was discovered.

- D50 - K66 - the company received a short-term loan.

- D51 - K50 - the organization deposited cash to a credit institution, to its own account.

- D60 - K50 - the company has repaid its debt to the supplier; The organization made an advance payment to its supplier for the future supply of any products.

- D69 - K50 - the company paid its employees any benefits from the Insurance Fund.

- D70 - K50 - the organization paid wages or advance payments for the first half of the month.

- D 71 - K50 - the organization issued cash to the reporting employee for any purpose.

- D75-2 - K50 - the company paid its founders the dividends due to them.

- D76 - K50 - the organization paid deposited salaries and other deposited amounts.

Documentation of cash at the cash register

All main types of cash flows and documents equivalent to them can be presented as follows:

| Receipt at the cash desk (receipt) | Issue from the cash register (expense) |

| From a bank account to salaries, household, operating and travel expenses | Amounts of wages due to employees |

| Revenue from the sale of works, services or goods | Amounts to report to employees for travel, business and operating expenses |

| Return of unused imprest amounts | Payment of compensation, benefits or loans to employees |

| For other reasons | Transfer for collection |

Documentation of cash transactions of the organization is carried out using the established forms:

- Receipt order

- Withdrawal slip

- Journal of registration of cash documents

- Cash book (book for registering cash transactions)

- Book of accounting of received and issued funds and documents

In addition, organizations are required to use documents in the forms established by the Central Bank of the Russian Federation to ensure the reliability and control of cash flows or compliance with cash discipline.

Transactions with foreign currency

Organizations can carry out cash transactions both in national currency and in foreign currency. Basically, accounting for transactions with foreign money is associated with payment for business trips abroad.

To receive currency for this purpose, you must have the following documents:

- Order for the purchase of currency;

- An order that sets out the rate of expenses per day;

- An order stating that the employee was sent on a business trip;

- Application for receiving currency.

The credit institution issues currency along with a certificate confirming the purchase, drawn up in a special form. It must be issued in the name of the employee sent on a business trip.

If an organization carries out cash transactions in foreign currency, the accountant must take into account these transactions in rubles in the amounts received when converting the currency at the official exchange rate of the Bank of Russia. Recalculation must be carried out on the day of the transaction.

Cash book

All movements at the cash register are reflected in the cash book (form according to OKUD 0310004).

Entries in the book are made by the cashier or other authorized person for each PKO or RKO.

At the end of the working day, the cashier checks the data contained in the cash book with the data of cash documents, displays the amount of the cash balance and affixes a signature. Then the entries in the cash book are verified with the data in cash documents by the chief accountant, accountant or manager and signed.

See also “Procedure for making corrections to the cash book (nuances)”.

If no cash transactions were carried out during the working day, no entries are made in the cash book. Separate divisions provide the legal entity with a copy of the cash book sheet in the manner established by it. From November 30, 2020, departments that do not store money, but hand it over to the cash register of a legal entity, are allowed not to maintain a cash book.

The chief accountant controls the maintenance of the cash book; in his absence, the manager.

Postings for foreign currency transactions

Accounting for cash transactions with currency involves the following typical entries:

- D50-1 - K52-22 - the organization received foreign currency cash from the bank for the expenses of employees on a business trip. The primary document will be the receipt order.

- D71 - K50-1 - the company issued foreign currency cash to the reporting employee for his expenses on a business trip. The operation is accompanied by the execution of an expense order.

- D50-1 - K71 - the reporting employee returned money in foreign currency that was not used on a business trip to the cash desk. The primary documentation will be advance reporting, as well as a receipt order.

- D91-2 – K50-1 – a negative exchange rate difference was received. Documentation – certificate from an accountant.

- D50-1 – K91-1 – a positive difference in rates was obtained. The documentation is the same as in the previous case.

- D52-22 - K50-1 - the company deposited foreign currency cash into its account with a credit institution. For this operation, an order for the expense and a statement for the foreign currency account must be issued.

Preparation of cash documents

There are two options for maintaining cash documents - basic and simplified (for individual entrepreneurs and small organizations, we will consider it below). In the basic version, individual entrepreneurs and LLCs must formalize all cash transactions using the following documents:

- cash receipt order - is formed when cash arrives at the cash desk;

- expense cash order - generated when cash is issued from the cash register;

- cash book (according to form KO-4) - it keeps records of all cash receipts and expenditures based on all receipts and expenditure orders;

- settlement and payment form (according to form No. T-49) and payroll (according to form No. T-53) - documents for the calculation and payment of wages and other payments to personnel;

- An advance report is a document that is drawn up by an employee or director of an organization (but not an individual entrepreneur) to account for cash expenses previously given to him in advance or spent from personal funds.

Cash discipline does not include KUDiR, the BSO accounting book, a certificate report (on the KM-6 form) and the cashier-operator’s journal (on the KM-4 form).

Simply put, cash discipline means maintaining a cash book and reflecting cash transactions, drawing up cash documents (receipt orders, expense orders, advance payments). Also, compliance with the cash payment limit when making payments to counterparties (not individuals or employees): the limit should not exceed 100,000 rubles for a one-time payment in cash. It is also important to keep money in the cash register within the limit established by the organization, and deposit funds exceeding it to the bank.

Cash documents can be maintained electronically and on paper. Paper documents are filled out by hand or on a computer, then printed and signed. In electronic form, documents are prepared in a special program or accounting service and signed with electronic signatures.

Accounting for monetary securities

Companies can store not only cash, but also banknotes in their cash registers. Such papers will be various stamps, transport tickets, vouchers, coupons and others. They must be accounted for at their actual price. The organization must store such documents in a fireproof cash safe.

The employee who is responsible for the safety of these documents is the cashier.

Read more about accounting for cash documents in the article.

Typical transactions for monetary securities

The main entries made when accounting for monetary documents are:

- D50-3 - K71 - monetary documents purchased for cash are credited to the company's cash desk. To carry out the operation, advance reporting and an invoice are prepared.

- D50-3 – K60 (76) – monetary securities purchased by bank transfer were entered into the cash register. The primary documentation is the invoice.

- D73-1 – K50-3 – a company employee received a tourist voucher in part of the money he contributed. In this case, documents such as an order from the manager of the company, a statement on the issuance of vouchers, and a certificate from an accountant must be drawn up.

- D91-2 - K50-3 - the employee received a voucher, which was fully paid for by his employer. The primary documentation is the same as in the previous case.

- D71 - K50-3 - an employee going on a business trip received travel tickets. This operation is recorded in the cash register.

- D71 – K50-3 – the employee received various stamps from the company’s cash register for their intended use. The operation is recorded in a special journal.

- D94 - K50-3 - an inventory was carried out, during which a shortage was discovered. An accountant's certificate and an inventory list must be prepared.

- D99 - K50-3 - during emergency incidents, some of the monetary documents were lost. The same documents are drawn up as in the previous case.

Postings according to reporting forms

- D006 - K - the organization received reporting forms from the printing house. An invoice from the printing house and a receipt order must be issued.

- D – K006 – forms used to sell tickets were written off. An accountant's statement and a cashier's report on tickets sold are prepared.

Similar articles

- Accounting of cash transactions

- Cash discipline in 2016-2017

- The procedure for conducting cash transactions in 2016-2017

- Cash transactions in 2021

- Maintaining and recording cash transactions in foreign currency