Let's understand the basics

Legislators have determined a unified way of systematizing and grouping information about the economic activities of Russian enterprises and institutions.

Order of the Ministry of Finance No. 94n establishes a Unified Chart of Accounts for commercial and non-profit organizations, and Order No. 157n - for public sector institutions. Accounting accounts are special digital and alphabetic codes that are used to reflect business transactions in accounting, or more precisely, when drawing up accounting entries.

Each account has its own classification characteristic, which is determined by the “balance sheet” method. This means that, like a balance sheet, all accounts are divided into assets and liabilities. And some accounts can be reflected in both assets and liabilities. Consequently, all accounts are divided into active, passive and active-passive accounts; the table for budgetary organizations contains about 1000 such codes.

Standard Accounting Plan 2021 - table with explanation

The standard account plan contains 99 accounting accounts, but only 62 numbers are occupied, the remaining numbers are free and can be used by the organization to create new accounts necessary to reflect the characteristics of the activities of a particular company.

According to the type of objects and operations taken into account, all accounts of the standard Plan are divided into active, passive and active-passive.

Active ones reflect accounting of assets, passive ones - accounting of liabilities, active-passive ones - take into account both.

Each account has a name and number. On-balance sheet numbers are two-digit, off-balance sheet numbers are three-digit.

All accounts in the standard accounting plan are called synthetic of the first order; for more detailed accounting, you can open second-order subaccounts for them. The plan contains recommendations for their reopening.

If you need even more accurate accounting, analytical accounts are opened for subaccounts.

Small enterprises usually need synthetic first-order accounting; large enterprises need more detailed accounting, so they also use second-order subaccounts and analytical accounting.

In general, the standard Plan allows you to speed up the work of an accountant. Since accounts have a number, in the process of accounting and making transactions you can not use names, but indicate only numbers that are understandable to everyone.

Example:

Business transaction - Receipt of cash payment from the buyer.

This operation is accounted for in accounting using the following posting: Debit of account 50 “Cash” - Credit of account 62 “Settlements with buyers and customers”. You can indicate it briefly without names: Debit 50 - Credit 62, such an entry will also be clear to everyone.

Below is a table that contains all the accounts of the standard Plan, indicating the number, name, division into active, passive and active-passive, and also indicates sub-accounts that can be opened in accordance with the recommendations of the standard Plan.

Download in word

Download a standard Chart of Accounts (table with subaccounts) - word.

Download instructions for the Chart of Accounts - word.

How to remember and learn quickly?

One of the possible, but not the best, ways to memorize accounting accounts is to memorize the number and name, without understanding the purpose and features of application.

You can memorize accounting accounts more conveniently and quickly by applying them in practice in various tasks, understanding the order of their application.

To account for transactions, it is necessary to draw up transactions; for this, you will have to constantly determine the corresponding accounts, selecting them from the Plan. By turning to the Plan again and again, gradual memorization occurs.

There is no need to specifically memorize numbers and names; the best way is to solve accounting problems for drawing up transactions.

You also need to understand that the accountant may not need all the accounts. In practice, a Work Plan is formed from those numbers that are needed for accounting. Manufacturing enterprises use one set of accounts, trade enterprises use another. Large enterprises keep more detailed records, while small companies can simplify accounting by summarizing data.

Active accounting accounts

To reflect property, material and monetary values in the chart of accounts, special active accounting accounts are provided. In simple words, active accounts are accounts for accounting:

- company property, both tangible and intangible (fixed assets, inventories, intangible assets);

- amounts of funds, both in cash and in current bank deposits and accounts (in rubles, foreign currencies, precious metals);

- production costs, work in progress and semi-finished products;

- financial investments of various types, both short-term and long-term.

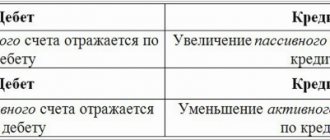

Since active accounts are intended to account for the property and finances of the company, the balances on such accounts can only be in debit, that is, have a positive value.

For example, active accounts include:

- account 01 “Fixed Assets”, for which there cannot be a negative balance, because the initial cost of an asset cannot have a negative value;

- or active account 10 “Inventories”. Transactions involving the receipt of property and monetary assets are reflected in accounting as a debit turnover, and disposals as a credit turnover;

- active account 50 “Cashier”, which cannot reflect a negative cash balance in the cash register.

The final debit balance on active accounts should be reflected in the asset balance sheet, in the corresponding lines of the reporting form.

Chart of Accounts.

This section provides a complete and comprehensive list of accounting accounts. To finally understand why a chart of accounts is needed, the council should read the lesson from the series “7 lessons about accounting in understandable Russian language.”The link on the account opens an information card for each accounting account. In the information card on the accounting account:

— a description is given of what is accounted for in this accounting account . — a list of accounting accounts with which this accounting account ( account posting plan ). — the moment when a posting is created for the accounting account and its corresponding account is given.

Attention!

The material is in partial development, so not all cards are ready. The accounts for which the account card has been published are marked in red. I apologize, I want to prepare high-quality material. CHART OF ACCOUNTS / PLAN OF ACCOUNT ENTRY / CORRESPONDING ACCOUNTS

| CODE | ACCOUNT NAME | ACCOUNT TYPE |

| 01 | Account 01 “Fixed assets” | ACTIVE |

| 02 | Account 02 “Depreciation of fixed assets” | PASSIVE |

| 03 | Account 03 “Profitable investments in material assets” | ACTIVE |

| 04 | Account 04 “Intangible assets” | ACTIVE |

| 05 | Account 05 “Amortization of intangible assets” | PASSIVE |

| 08 | Account 08 “Investments in non-current assets” | ACTIVE |

| 10 | Account 10 “Materials” | ACTIVE |

| 19 | Account 19 “VAT on purchased assets” | ACTIVE |

| 20 | Account 20 “Main production” | ACTIVE |

| 25 | Account 25 “General production expenses” | ACTIVE |

| 26 | Account 26 “General business expenses” | ACTIVE |

| 40 | Account 40 “Production of products (works, goods” | ACTIVE |

| 42 | Account 42 “Trade margin” | PASSIVE |

| 43 | Account 43 “Finished products” | ACTIVE |

| 44 | Account 44 “Sales expenses” | ACTIVE |

| 45 | Account 45 “Goods shipped” | ACTIVE |

| 50 | Account 50 "Cashier" | ACTIVE |

| 51 | Account 51 “Current accounts” | ACTIVE |

| 52 | Account 52 “Currency accounts” | ACTIVE |

| 58 | Account 58 “Financial investments” | ACTIVE |

| 60 | Account 60 “Settlements with suppliers and contractors” | ACTIVE-PASSIVE |

| 62 | Account 62 “Settlements with buyers and customers” | ACTIVE-PASSIVE |

| 66 | Account 66 “Settlements for short-term loans and borrowings” | PASSIVE |

| 67 | Account 67 “Settlements for long-term loans and borrowings” | PASSIVE |

| 68 | Account 68.02 “VAT” | ACTIVE-PASSIVE |

| 69 | Account 69 “Calculations for social insurance and security” | ACTIVE-PASSIVE |

| 70 | Account 70 “Settlements with personnel for wages” | PASSIVE |

| 71 | Account 71 “Settlements with accountable persons” | ACTIVE-PASSIVE |

| 73 | Account 73 “Settlements with personnel for other operations” | ACTIVE-PASSIVE |

| 75 | Account 75 “Settlements with founders” | ACTIVE-PASSIVE |

| 76 | Account 76 “Settlements with various debtors and creditors” | ACTIVE-PASSIVE |

| 80 | Account 80 “Authorized capital” | PASSIVE |

| 84 | Account 84 “Retained earnings (uncovered loss)” | ACTIVE-PASSIVE |

| 90 | Account 90 “Sales” | ACTIVE-PASSIVE |

| 91 | Account 91 “Other income and expenses” | ACTIVE-PASSIVE |

| 97 | Account 97 “Deferred expenses” | ACTIVE |

| 98 | Account 98 “Deferred income” | PASSIVE |

| 99 | Account 99 “Profits and losses” | ACTIVE-PASSIVE |

Passive accounts

The sources of formation of the enterprise's assets constitute the passive side of the balance sheet. Passive accounts reflect:

- capital of an economic entity (statutory, reserve, additional);

- obligations accepted by the company for execution;

- loan, credit and loans received;

- some types of expenses, such as depreciation;

- reserve funds for doubtful debts.

Passive accounts can only have a credit balance at the end of the reporting period; a debit balance on passive accounts indicates the presence of errors in accounting. An increase in indicators on passive accounts is formalized by a credit turnover, and a decrease in liabilities, capital or write-off of expenses is formalized by an operation on the debit of a passive account.

In the balance sheet, passive accounts represent the corresponding section - liabilities. The generated balances at the end of the reporting year are distributed along the corresponding lines of the liability side of the balance sheet, in accordance with the current rules for preparing financial statements.

Which accounts are passive and which are active?

When working with active accounts, transactions to increase the asset are recorded in the debit part. In the same part, the final balance of the selected account at the end of the reporting period is recorded, if there is such a balance. If the transaction caused a decrease in the asset, it is recorded in the credit column. In general, active accounts are used to record the organization’s property, which includes goods, materials, equipment and cash.

Passive accounts display the change, movement and status of the company’s sources of funds, i.e. accounting of all events occurring on them.

Example of passive accounts in an NPO

Passive account 02 “Accrued depreciation” has a credit balance on the account. Turnover in the debit of the account reflects the write-off of accrued depreciation upon disposal of fixed assets.

The following example: passive account 70 “Settlements with personnel for wages”. The credit of the passive account reflects the accrual of earnings. Debit account turnover - withholding income tax or making payments. A negative account balance is a declaration of an erroneous account.

Instructions for use

The chart of accounts contains all the necessary information for accounting. A working chart of accounts should always include the following sections in a certain sequence:

Accounting

- Capital.

- Credits and loans.

- Cash, cash equivalents and other settlements.

- Capital investments and long-term assets.

- Procurement process and production costs.

- Production and social sphere.

- Finished products and goods.

- Sales process and financial results.

- Off-balance sheet accounting accounts.

Accountant

Chart of Accounts is a diagram that contains 99 accounting accounts grouped according to different characteristics. It is needed for convenience and unification. Each organization can approve on its basis a work plan that will contain the most used accounts. It can be printed and used as a visual aid for daily operations.

Mixed accounts

Some ledger accounts may have both credit and debit balances. Such mixed accounts are called active-passive accounting accounts. For example, accounting accounts reflecting information on settlements with customers or suppliers. Consequently, when goods are shipped to a buyer, an account receivable is formed in the accounting system, and when an advance payment is received from the same buyer against future deliveries, an account payable is formed. It cannot be hidden. Settlements with suppliers are carried out similarly to account 60.

Account 84 “Retained earnings, loss” is also considered both an active and passive account, since it can have both a credit and a debit balance at the end of the reporting period.

Active and passive accounts

In general, active-passive accounts reflect accounting transactions not only with individuals, but also with organizations for which accounts payable and receivable are kept.

An enterprise that uses borrowed or borrowed funds in its activities forms its accounts payable to individuals and organizations at their expense. In this situation, the mentioned counterparties act as creditors.

When individuals or organizations owe a certain amount back to a company after a predetermined period, it is called a receivable.