The responsibility of companies, as tax agents, is to submit information on the payment of income to staff and other individuals in 2-NDFL certificates. They must be submitted for the past tax period before April 1 of the next year at the place of registration with the Federal Tax Service (Clause 2 of Article 230 of the Tax Code of the Russian Federation).

In situations where a company ceases to exist or is reorganized before the end of the year, forms 2-NDFL should be submitted for the calculated tax period, i.e. for the time while the enterprise was operating - from the beginning of the year to the date of the termination of the company’s previous operation registered in the state register status (clause 3.5 of Article 55 of the Tax Code of the Russian Federation). The nuances of filling out 2-NDFL certificates in situations related to the termination of activities or reorganization of an enterprise will be discussed in the article.

2-NDFL when changing the status of the company

As a rule, a company ceases to exist after submitting all reports in full, including 2-NDFL certificates for employees. After all, after the termination of activity, it does not have successors who could report on the data on tax accruals and withholding. Closing companies, submitting 2-personal income tax until the moment of liquidation, fill out certificates according to the usual algorithm - the name of the company is indicated in the line “tax agent”, and its details - in the appropriate fields provided.

When reorganizing (“reshaping” a company according to a selected criterion and registering it in a new capacity), the range of actions is wider. If, due to any circumstances, the company did not submit 2-NDFL before changes in status, the legal successor is obliged to report for it. This requirement has been in effect since the beginning of 2021 (clause 5 of Article 230 of the Tax Code). Therefore, the successor company in this case will submit information on the income of individuals twice:

- as a successor to the tax agent - for the period from the beginning of the year to the date of recorded reorganization;

- as a tax agent - for the time from the beginning of operation of the changed company until the end of the year.

Termination of activities of one of the companies

Depending on the situation, the outcome may vary. So, if one of the companies is subject to liquidation, this indicates that a new entity is being formed. Therefore, there are more nuances in the reporting documentation provided. If there is no liquidation and all firms are operational, then it is assumed that the company continues to operate. Therefore, you need to bring proof of income in accordance with the generally established procedure.

| Type of changes | Deadline for submitting income information |

| Merger Aims to create a new company consisting of two or more former legal entities. As a result, they cease their activities | 2-NDFL is submitted by the reorganized company before the day when state registration of the new legal entity occurs. The latter must send certificates of income for the year according to the general rules |

| Affiliation is a form of introducing change in which there is a transfer of authority from one company to another. In this situation, the affiliated organization ceases to exist | The merged company submits certificates before the date on which the record of its liquidation is made in the Unified State Register of Legal Entities. As for the company it joined, it submits reports based on the results of the year according to generally established rules |

| Division involves the transfer of powers to companies that are created again. And the original company ceases its activities and is liquidated | The organization that has undergone changes submits 2-NDFL until the state registration of new legal entities occurs. Newly formed companies must submit documents according to generally established rules |

Thus, the tax authorities must receive at least two certificates from companies. This is due to the fact that information on income received by individuals is submitted by the existing company - before the procedures are carried out, and then by another company formed after the changes (the tax period lasts from the beginning of its activities until the end of the year). If more than two companies took part in the process of all perturbations, then the number of sets of certificates will be correspondingly large.

Changes to form 2-NDFL in 2021

To ensure the correct preparation of forms based on the right of succession and their subsequent submission to the Federal Tax Service, the legislator updated the 2-NDFL certificate. Since 2021, changes have been made to it, however, these do not affect the procedure for reflecting income, deductions and taxes.

Read also: Certificate 2-NDFL: new form 2019

Two new lines have been added to section 1 “Data about the tax agent”:

- “Reorganization/liquidation form”, where a code corresponding to the type of changes being made is entered:

– 0 – liquidation;

– 1 – transformation;

– 2 – merger;

– 3 – separation;

– 5 – connection;

– 6 – separation with simultaneous joining;

- “TIN/KPP of the reorganized company”

In the 5th section, in the field certifying the signature of the decryption of the signatory, an entry has been entered about the possibility of certifying the certificate by the legal successor. In the “tax agent” field of this section, the successor enters code “1”, and his representative - “2”.

Thus, new form fields are filled out exclusively by assignees. 2-NDFL certificates for the transformed company are submitted by them to the Federal Tax Service at the place of their territorial registration. At the same time, they indicate:

- OKTMO code of the reformed company;

- in the line “tax agent” - its name;

- in the field “TIN/KPP of the reorganized organization” - exactly the TIN/KPP of the reorganized company.

Let's look at filling out the 2-NDFL certificate using examples.

Where can I get a personal income tax certificate 2 for an employee if the organization is liquidated?

What to do if the organization no longer exists or a reorganization has occurred. In this case, contact the tax service. The fact is that personal income tax certificate 2 is issued to employees and relates to reporting.

Each organization is required to submit such a report to employees by April 1 of the year following the reporting period. When liquidating a company 2, personal income tax is also submitted to the supervisory authorities.

To obtain a certificate, a citizen applies to the inspectorate at the place of registration of the enterprise. This information is posted on the Federal Tax Service website according to the company’s TIN and is located on the organization’s seal.

A certificate is also issued within 3 days based on the application. The application is drawn up in free form and in two copies. The second copy with the registration mark remains with the citizen.

If a person does not need the certificate itself, but only information on income and taxes, he will find out about this in the following ways:

- From the legal successor, if reorganization has taken place;

- through your personal account on the Federal Tax Service website;

- through a new employer, who will make a corresponding request to the Federal Tax Service and extra-budgetary funds.

1-2.jpg

Example 2. Filling out 2-NDFL by the legal successor during reorganization

The company MIR LLC, located in Chelyabinsk (OKTMO 75712000, INN 7404215894, KPP 740445028) is being transformed by merging with Topol LLC from Yekaterinburg (OKTMO 65701000, INN 6612456456, KPP 661200012) from December 1 2021 This date is recorded in the state register termination of the activities of MIR LLC and the transfer of its assets by right of succession.

2-NDFL information for MIR LLC was not submitted to the Federal Tax Service. Topol LLC will report:

- as the legal successor of the transformed company, filling out 2-NDFL for the period from January 1 to November 30, 2021:

What happens during reorganization by merger

Upon merger, a legal entity merging with another legal entity ceases to exist. The reorganization process is regarded as completed at the moment when a record that the legal entity has completed its activities appears in the Unified State Register of Legal Entities (clause 4 of Article 57 of the Civil Code of the Russian Federation). All rights and obligations of the organization that has completed its activities are transferred to the legal entity to which the merger took place (Clause 2 of Article 58 of the Civil Code of the Russian Federation), which must be duly notified to the registering authority and creditors (Article 60 of the Civil Code of the Russian Federation).

Early (before the end of the tax period, the duration of which is 1 year) termination of activities by a legal entity entails the obligation to early submit reports on those taxes that are considered a cumulative total for the year (clause 3 of Article 55 of the Tax Code of the Russian Federation). In particular, this applies to 2-NDFL certificates (clause 5 of Article 230 of the Tax Code of the Russian Federation, Law “On Amendments to the Tax Code” dated November 27, 2017 No. 335-FZ). In this case, the form of reorganization is unimportant.

See here for details.

That is, the merging legal entity must, for the period from the beginning of the year until the date of registration of the completion of its activities, submit to the Federal Tax Service certificates in form 2-NDFL for its employees. Certificates are issued in the usual manner for them on behalf of the organization being merged (i.e. with its name, TIN, KPP, OKTMO and signature of the responsible person). If the acquired legal entity has separate divisions, certificates are also generated for them, indicating information on the tax agent with data related to the division (KPP, OKTMO, signature of the responsible person).

If the reorganized company does not fulfill its obligations and does not submit a certificate to the tax authorities before closing, then the successor will have to do this (clause 5 of Article 230 of the Tax Code of the Russian Federation).

The legal successor of the acquired legal entity will also have to pay tax if at the time the legal entity completes its activities this obligation remains unfulfilled by it (Clause 5 of Article 50 of the Tax Code of the Russian Federation).

Consequences of legal entity transformation

The procedure for transforming a legal entity involves changing its organizational and legal form and does not lead to a change in either the rights or obligations it has to persons other than the founders (Clause 5 of Article 58 of the Civil Code of the Russian Federation). Accordingly, Art. 60 of the Civil Code of the Russian Federation, guaranteeing the implementation of the rights of creditors.

The absence of changes in terms of rights and obligations during transformation leads to the fact that nothing changes in terms of tax reporting and payment of taxes for a legal entity that has changed its form. That is, in the usual manner (but on behalf of an already changed organization), reports will be submitted within the same deadlines and taxes will be paid in the same way (clause 9 of Article 50 of the Tax Code of the Russian Federation). And if, before its transformation, the legal entity did not submit any reports or pay any taxes, this must be done by the organization existing in the new form (letter of the Ministry of Finance of Russia dated September 25, 2012 No. 03-02-07/1-229).

Accordingly, in this case there will be no special features in the procedure for filing reports in Form 2-NDFL. These certificates in their usual form will be created by a legal entity of a new organizational and legal form on its own behalf and in accordance with the established clause 2 of Art. 230 of the Tax Code of the Russian Federation (until April 1 of the year following the reporting year) to submit them to the Federal Tax Service.

For information on how to prepare 2-NDFL reports for 2017 for submission, read the article “Nuances of filling out form 2-NDFL in 2021” .

Where to get a certificate

The income document is requested by the interested person at the place of his study or work. According to the provisions of legal acts, an individual must submit a written request for the issuance of a certificate, after which the tax agent is obliged to issue it within three days.

The request is written in any form addressed to management in the form of a request. It must reflect specific information about who needs the certificate, for what purposes and for what period. The date the letter was issued and the applicant’s signature are required elements.

In practice, issues regarding the issuance of a certificate are resolved through oral and not recorded negotiations.

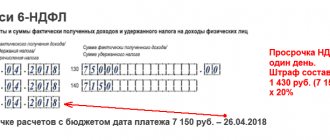

Penalties

For late filing of 2-NDFL, the following penalties apply:

- fine for an organization under paragraph 1 of Article 126 of the Tax Code - 200 rubles for each certificate not submitted on time ;

- fine for an official under Part 1 of Article 15.6 of the Code of Administrative Offenses of the Russian Federation - 300-500 rubles .

For false information contained in 2-NDFL, for example, for indicating the TIN of another person, a fine of 500 rubles is imposed for each erroneous certificate .

You can avoid sanctions for false information in the standard way: if the error is identified independently, then before the Federal Tax Service Inspectorate discovers it, you need to submit an updated Form 2-NDFL.

Is it worth submitting the certificate in advance to allow time for correction? From the letter of the Ministry of Finance dated June 30, 2016 No. 03-04-06/38424 it follows that this does not make sense.

Explanation . The organization filed 2-NDFL ahead of schedule, for example, in early February. The tax authority found errors when checking the form. The accountant corrected everything and submitted an updated certificate before the end of the period, but the organization was still fined because the errors were discovered by the tax authority .

Review of 2-NDFL during liquidation and reorganization

Income tax levied on the income of individuals is calculated and paid by tax agents, which include enterprises and individual entrepreneurs - in some cases, and by citizens themselves - in others. Based on the results of the reporting tax period, which is a calendar year, agents are required to submit a report to the territorial branch of the Tax Service at the place of registration. 2-NDFL.

The certificate must contain information about all remunerations that the tax agent paid during the reporting period to employees and other individuals. persons, the amount of income withheld from them. According to the general rules, the HD entity is required to submit a certificate before April 1 of the year following the reporting year.

But such a restriction applies only to tax agents; if the taxpayer himself needs, for example, to receive a property deduction, then he has the right to submit a report throughout the year at any time. In other cases, employees require a certificate from employers to submit to various authorities and institutions.

The tax agent is required to submit certificates separately for all employees, as well as a register of these certificates in 2 copies. If the organization did not accrue or pay wages during the reporting period, then the certificate is not submitted.

There is also no requirement to submit a report in cases where the enterprise acquired property or property rights from a citizen or paid remuneration to the individual entrepreneur. The situation changes in relation to entities that have undergone changes in their activities during the calendar year, for example, the enterprise has been reorganized or it has been liquidated.

If reorganization should be understood as some changes in the structure of the enterprise, then liquidation means the complete cessation of activity. In this case, the deadlines for filing 2-NDFL during liquidation and reorganization change.

Main provisions

If an enterprise is liquidated or undergoes reorganization, this means that its latest tax period, for which various reports are required, is changing. This is indicated in the Tax Code, in Art. 55, in paragraph 3. Moreover, this period will depend on the operating time of the enterprise during the year.

Article 55. Representative offices and branches of a legal entity

Legal deadlines

On the issue of providing information on the income of employees, the Federal Tax Service states that the information must be submitted by the storage system itself, which is being liquidated or reorganizing the structure. Tax authorities make their conclusions based on the provisions of the Tax Code, Art. 50, which deals with the succession of newly created legal entities. persons to fulfill the obligation to pay taxes.

In this article and others, the legislator does not impose responsibility for providing information according to f. 2-NDFL for legal successors. According to Art. 216 reporting is submitted for the past period in which the tax agent paid remuneration.

The deadlines for submitting reports can be considered using the example of some situations:

| What is happening to the enterprise | Which period should be considered the last tax period? |

| By the end of the year, reorganization took place or the enterprise ceased operations. | The tax period for filing reports should be considered the period from the beginning of the calendar year until the moment when the reorganization was completed or the enterprise (separate division) ceased its activities. |

| An enterprise was created and liquidated or underwent reorganization during the same calendar year. | The tax period should be considered the period from the moment of establishment of the enterprise until the moment of changes, which is less than 12 months. Situations are possible when small businesses open for 2–3 months in order to carry out a certain type of work or order. |

| The company was registered in December, but the changes occurred in the middle or towards the end of the next calendar year. | The period for the report will be considered the period of operation of the enterprise from the moment of opening until liquidation or reorganization, which should not be more than 13 months. Having opened in December, the enterprise could not calculate and pay wages to employees in the same month, i.e. all payments would fall on the next calendar year. |

The reorganized enterprise still remains an active legal entity, but the liquidated organization ceases to exist as a legal entity. face.

General nuances

In NK, in Art. 226, paragraph 1 states that the tax agent who calculated and withheld personal income tax from the taxpayer is obliged to transfer it to the local budget at the place of registration of the enterprise. But when a Russian organization has separate divisions that are on a separate balance sheet, it is also obliged to pay income taxes to the budget at their location (Article 226, paragraph 7).

The amount of tax that is withheld is calculated based on the income subject to taxation paid to employees or other individuals. persons who have an employment relationship with a separate unit.

Article 226. Peculiarities of tax calculation by tax agents

Thus, at the location of the separate unit, i.e., a certificate according to f. is also submitted to the territorial branch of the National Assembly. 2-NDFL. The main enterprise submits it at the place of its registration.

Form 2-NDFL

Large tax agents report to the tax office according to f. 2-NDFL and 6-NDFL, which are filled out separately for all separate divisions. Until the process of changes at the enterprise is completed, a f. must be submitted in relation to a separate division. 2-NDFL during liquidation and reorganization.

Comparison of shapes

To present information from an enterprise that is undergoing a reorganization process, the change procedure plays an important role. If f. “2-NDFL – liquidation” is submitted according to the general rules, then in case of reorganization of the f. “2-NDFL – reorganization”, taking into account the type of changes and the further procedure of the enterprise.

The general rules for submitting a certificate cannot be applied during reorganization, when there is a division or transformation of an enterprise, as a result of which:

- one or more enterprises are allocated;

- joins one or more enterprises;

- the company ceases to exist after the changes are made.

| Reorganization procedure | Submission deadline f. 2-NDFL |

| Merger. Two or more companies merge to form one large enterprise. As a result, small firms individually go out of business. | Enterprises that are going through the merger process submit a certificate until they become part of a large enterprise and it undergoes state registration. After the merger, the new legal entity submits a report within the established time frame, i.e., based on the results of the year. |

| Joining. One or more enterprises join a larger one, as a result of which they transfer their rights and obligations to it. The joining enterprises cease their HD. | The merging enterprises submit a report until information about the termination of activities is entered in the Unified State Register of Legal Entities for each. The organization to which small firms have joined submits annual reports. |

| Separation. A large enterprise is undergoing a process of division into several small ones. As a result, a large enterprise ceases to exist. | A large dividing enterprise is required to report to the tax authorities before the new organizations register the status of legal entities. In turn, new enterprises will submit certificates according to generally accepted rules. |

But there are also forms of reorganization when, as a result of the changes made, it is not necessary to liquidate the enterprise(s):

- From a large enterprise, one or several small ones are separated, in this case the main organization transfers some of the powers to the newly opened ones. The activities of the main company remain unchanged. Information on f. 2-NDFL, according to the general rules, represents the main enterprise and the spun-off one separately, i.e., based on the results of the reporting year until April 1.

- As a result of the transformation of the company, it can change the form of ownership, for example, an LLC is transformed into a joint-stock company, a cooperative or a partnership. A joint stock company can become an LLC or a cooperative. Due to the fact that the enterprise did not stop its work, the reorganization carried out is not reflected in the reporting deadlines. F. 2-NDFL is submitted according to the general rules.

How 2-NDFL certificates are presented during liquidation and reorganization

Due to the fact that the liquidated enterprise is completing its activities, no one except it can submit a report to the tax office. Therefore, the form is filled out based on information related to the closing enterprise. This must be done before the business closes completely.

In practice, what usually happens is that first the company’s activities are suspended, then for some time the results are summed up, all reports are submitted, and taxes are paid. The final moment during liquidation can be considered the date when the enterprise is deleted from the register of legal entities. This is done by the Tax Service at the request of the enterprise.

When carrying out reorganization, several certificates are submitted to the tax office according to f. 2-NDFL. First, personal income tax is calculated, withheld, transferred and displayed in a certificate for a certain period by the existing company(s), and then by the one(s) that was formed after the changes.

In fact, enterprises submit reports only for the period when they operated and paid income to individuals. Reporting can be submitted in several ways; it depends on the number of employees, the deductions from whose income are indicated in the certificate.

Enterprises can submit f. 2-NDFL:

- on paper in person through your representative (responsible employee);

- by sending by registered mail with an inventory of the papers being sent enclosed in the envelope;

- in electronic form on a disk or flash drive;

- via a communication channel, also in electronic form.

If the number of employees does not exceed 25 people, then it is allowed to submit a report on paper, in other cases only in electronic form. The submitted certificates are accompanied by a register where information about all income indicated in the compiled forms is entered.

If one of the certificates does not pass the inspection by the tax inspector, he will delete it from the register and record the results of the inspection in the protocol. The inspector will give one copy of the protocol and register to the enterprise.

When a report is submitted on removable media, a paper register must be attached to it. Moreover, a separate register is created for each completed file. Based on the results of the inspection, the inspector can accept all files. If errors are detected in one of the files, it will not be accepted.

In the same way, a protocol is drawn up and sent to the enterprise along with the register. Moreover, they can be given to a company representative personally or sent to a postal address. Through a telecommunications channel, send f. 2-NDFL is possible if the enterprise has an electronic signature. After verification, the protocol and register will be sent to the enterprise in the same way.

Other points

If, for example, during the liquidation procedure of an enterprise all employees quit, then a report can be sent to the liquidation commission before submitting the liquidation balance sheet. In exceptional cases, tax agents must report in a different form. 2-NDFL, but submit another reporting form.

This applies to cases, as indicated by the legislator in Art. 226.1, when the enterprise:

- carried out transactions with securities and futures transactions;

- made payments on securities issued by Russian companies.

Such enterprises submit the necessary information to the tax office about the recipients of income, amounts paid, accrued, withheld and transferred personal income tax in the income tax return. Such information is submitted not once a year, but according to the results of each reporting period, which is a quarter, until the 28th of the next month.

Accordingly, if during the calendar year the enterprise carried out such operations, and then at some point was liquidated (reorganized), then the declaration will have to be submitted not at the end of the quarter in which the changes took place, but upon completion of the changes, as the legislator indicates in Art. 230 (clauses 2, 4) and 289.

An example would be a situation where an enterprise is liquidated (makes changes in structure) in April, i.e. in the 2nd quarter, but you do not need to wait until the end of the reporting period to submit a declaration in order to submit it before July 28. This can be done as soon as the process is completed.

Source: https://buhuchetpro.ru/2-ndfl-pri-likvidacii-i-reorganizacii/

Where to submit information?

The question of which inspectorate should submit information on form 2-NDFL is perhaps the most common among all questions related to this form.

Let's start with it. If you look at the Tax Code, the answer to this question seems obvious. According to paragraph 2 of Article 230 of the Tax Code of the Russian Federation, information on the income of individuals is submitted to the tax office at the place of registration of the tax agent. However, Russian organizations quite often have several places of accounting - they are registered at the location of real estate, separate divisions, activities subject to UTII, etc. Unfortunately, the Tax Code does not explain what to do in this case. To what place of registration should 2-NDFL be sent? This problem is especially relevant for organizations that have branches in other cities or even constituent entities of the Russian Federation.

The Russian Ministry of Finance offers the following way out of this situation. If a separate division independently pays income to employees, and its head is authorized to represent the organization in the tax authorities, then information in Form 2-NDFL must be submitted to the inspectorate at the place of registration of this division (letter dated October 12, 2010 No. 03-04-06/3-251 and dated 03/29/10 No. 03-04-06/55). If at least one of the above conditions is not met, then the information is submitted to the inspectorate at the place of the company’s “main” registration.

In our opinion, this approach should be considered only a recommendation from the financial department, because the Tax Code does not oblige tax agents to act in this way. Formally, an organization can submit information to any of the inspectorates with which it is registered. However, it is safest to submit 2-NDFL to the inspectorate where the organization was originally registered as a taxpayer. Such an approach in the event of a dispute with controllers will definitely not cause misunderstanding among judges. And, in our opinion, it is still more consistent with the meaning of paragraph 2 of Article 230 of the Tax Code of the Russian Federation, which talks about the place of “one’s” accounting, which is linguistically closer to the term “place of accounting of the organization.”