Registration of purchase of components for a new fixed asset (OS)

First of all, in 1C 8.3 all OS components must be capitalized as equipment. A receipt document with the Equipment type is suitable for this. Let’s find the document by going to: Purchases – Receipts (acts, invoices):

Follow the link, click on Receipt and select Equipment from the list that opens:

Next, fill out the document according to the rules and put all the necessary information in the header:

- Organization – select the one you need from the list (if there are several);

- Warehouse – where the components will be located;

- Counterparty – indicate the supplier;

- Agreement – indicate the agreement with the supplier:

Then, on the Equipment tab, add the components that arrive using Add:

We will sequentially select the item, indicate the quantity and price. The 1C 8.3 program will calculate the remaining details automatically.

It is important to note here that the accounting account should be 07, since components are purchased for further assembly. VAT account 19.01 VAT on the acquisition of fixed assets.

Let’s post the document by clicking Post and using the Dt/Kt button we’ll see what kind of postings we got. From the figure below we see that the 1C 8.3 program made all the necessary postings:

- Dt 07 Kt 60.01 – equipment was received from the supplier to the account Equipment for installation;

- Dt 19.01 Kt 60.01 – for the amount of VAT:

If you need to enter more components into the 1C 8.3 database, but on a different day or from a different supplier, etc., then this is done in a similar way, each time creating a new receipt document.

Fixed Asset Accounting

Purpose of the lecture

: get acquainted with the features of organizing the accounting of fixed assets in 1C: Accounting.

9.1. Basic provisions

Fixed assets accounting in 1C:Accounting is based on PBU 6/01 “Accounting for fixed assets” and related regulatory documents.

The life cycle of a fixed asset item in an organization is as follows:

- Accounting for the acquisition or creation of a fixed asset. At this stage, it is important to take into account investments in fixed assets and calculate their initial cost.

- Acceptance of an asset for accounting. When the initial cost of an asset is formed, it is prepared for operation, and is taken into account for subsequent use.

- Accounting for depreciation of fixed assets. Depreciation is charged on fixed assets, distributing their initial cost over useful periods in accordance with the chosen depreciation method.

- Accounting for the movement of OS objects. OS objects can be moved from one division of the organization to another - these movements should be correctly reflected in accounting.

- Accounting for the modernization of OS objects. When upgrading, the properties of the OS improve, they acquire new capabilities.

- Revaluation of OS objects. OS objects are objects that are typically used for several years. During the operation of an object, it may turn out that its value changes - during major repairs, completion or additional equipment, during revaluation in order to bring information about the cost of fixed assets to the current state. During revaluations, the value of objects changes; this also needs to be reflected in accounting.

- Inventory of OS objects. Inventory is a reconciliation of the actual presence and condition of fixed assets with accounting data. OS objects, like other valuables, periodically require inventory.

- Disposal of fixed assets. The life cycle of fixed assets in an organization ends with their disposal. Disposal of fixed assets occurs for various reasons. This may be moral and physical obsolescence, sale of fixed assets to another organization, transfer as a contribution to the authorized capital. The disposal of fixed assets also requires recording.

As you can see, fixed asset accounting is very multifaceted. Let's begin its description by revealing the features of accounting for investments in fixed assets and the formation of their initial cost.

9.2. Accounting for the acquisition or creation of OS

To account for investments in non-current assets, that is, to account for the costs that form the initial cost of fixed assets, account 08 “Investments in non-current assets” is used, Fig. 9.1.

Rice.

9.1. Account 08 “Investments in non-current assets”

Analytical accounting for account 08 and its subaccounts is organized in the context of individual construction projects (Subconto 1) and cost items (Subconto 2). For some subaccounts, subaccounts have been created Nomenclature

(Sub-account 1),

Batches

(Sub-conto 2 - if the organization uses batch accounting) and

Warehouses

(Sub-conto 3).

To account for equipment that requires installation, account 07 “Equipment for installation” is used. On this account, accounting is maintained in the context of item items (Sub-Conto 1), batches (Sub-Conto 2) and warehouses (Sub-Conto 3). Let's consider the schemes of accounting records for fixed assets, depending on the methods of entry into the organization and on the characteristics of the operating system.

General schemes of accounting entries for accounting for the acquisition or creation of fixed assets

If an organization acquires a fixed asset that does not require installation, this is reflected as follows:

| D08 K60 - For the cost of the fixed asset without VAT |

| D19 K60 – VAT |

| D01 K08 - Accepted for accounting of fixed assets at historical cost |

If an organization purchases an OS that requires installation, this is reflected as follows:

| D07 K60 - For the cost of the fixed asset without VAT |

| D19 K60 – VAT |

| D08 K07 - Transfer of OS object for installation |

| D08 K60 - Installation work carried out by a third party has been accepted for accounting |

| D19 K60 - VAT on installation work |

| D08 K10 - Materials required for installation have been written off |

| D08 K70 - Wages accrued to employees of the organization involved in installation |

| D08 K69 - Contributions for social needs |

| D01 K08 - Accepted for accounting of fixed assets at historical cost |

When constructing an OS facility using the services of third-party organizations, the following record scheme can be used:

| D08 K60 - Accepted for accounting of work on the construction of the OS |

| D19 K60 – VAT |

| D01 K08 - Accepted for accounting asset asset |

When constructing fixed assets that require installation using the services of a third party, their acceptance for accounting will look like this:

| D07 K60 - Work on the construction of the OS, which requires subsequent installation, has been taken into account |

| D19 K60 – VAT |

| D08 K07 - OS completed for installation |

| D08 K60, 10, 70, etc. — Installation costs are reflected, incl. payment for third-party services, materials consumed, wages, etc. |

| D19 K60 - VAT when using third-party services in installation |

| D01 K08 - Accepted for accounting asset asset |

When constructing an OS object using your own resources, account 08 collects the costs of creating an OS object, which ultimately give its initial cost, at which it is accepted for accounting.

Let's consider the procedure for working in 1C: Accounting when accepting a new OS object for accounting.

Purchasing an OS

As you can see below, there are many specialized documents for working with the OS. However, such an important transaction as the acquisition of an asset is formalized using a regular document used to record the receipt of goods and services. We will look at details about purchasing goods and services in one of the following lectures, but now we will look at purchasing issues in the part that is important for working with the OS.

Consider the following example:

On January 16, 2009, the organization received from Technodrive LLC (Invoice No. 23 dated January 16, 2009) an Epson color laser printer worth 47,200 rubles, incl. VAT 7200 rubles. The supplier issued invoice No. 21 dated January 16, 2009. The printer was registered at the Main warehouse according to receipt order No. 17 dated 01/16/09

.

Let's create a new document Receipt of goods and services

(

Purchase > Receipt of goods and services

).

When creating a new document, select the document type Equipment

. This is what the document form looks like (Fig. 9.2).

Rice.

9.2. Document form Receipt of goods and services

We fill out the document as follows:

In the Account

We enter information about the counterparty (in our case, Technodrive LLC) in the

Contract

- the contract corresponding to this delivery.

Information about the agreement in such an operation can be entered by clicking the button with three dots after filling out the Contractor

(Fig. 9.3).

Rice.

9.3. Entering information about the contract with the supplier

Now you need to fill out the Equipment

.

Let's create a new row in the Equipment

and enter information about the incoming printer.

It should be noted that in the reference book Nomenclature

a special nomenclature group is provided for storing information about fixed assets objects.

In order for the correct settings to be applied to a fixed asset received at the warehouse, relating, in particular, to accounting accounts, it must be placed in the Equipment group (fixed asset objects)

, Fig. 9.4.

Rice.

9.4. Entering information about the purchased printer in the Nomenclature directory, in the Equipment group

When a product item that has just been created and placed in the desired group is selected in the corresponding position in the table row, some data - in particular, accounting accounts - will be filled in automatically. Other data must be filled in in accordance with the contract received by the organization. This is what our document looks like at this stage of filling out (Fig. 9.5).

Rice.

9.5. Entering printer information in a document

Please note that when filling out a document, you need to set up information about the prices and currencies used in the document. We did this by selecting the price type when filling out the parameters of the contract with the supplier. You can also do this by clicking the Prices and currency

, which is located in the document toolbar and setting the necessary parameters in the window that appears (Fig. 9.6).

In our case, everything is already installed as needed. And here we are, in particular, interested in the type of price ( Negotiated (with VAT)

) and the method of calculating VAT. The calculation method chosen is one that separates VAT from the total cost of the document.

Rice.

9.6. Currency and price settings window

Now let's go to the Advanced

and enter information about the receipt order with which the printer was posted to the warehouse and about the person responsible for the operation (Fig. 9.7).

Rice.

9.7. Entering data about a receipt order in the Additional tab

On the Accounts

Accounts 60.01 and 60.02 must be indicated.

Now let's resolve the issue with the invoice. Since we have received an invoice, let's go to the Invoice

(Fig. 9.8).

Rice.

9.8. Filling out the invoice tab

Here we have checked the Invoice presented checkbox

and filled in the fields

Incoming invoice number

and

Incoming invoice date

.

This tab is filled in if an invoice is received along with the product. If, for example, the invoice arrived later or there are several invoices, you need to use the Enter invoice

.

Installation (assembly) of received equipment

Now that all the necessary components are in stock, you can begin assembling (installing) the equipment. You can easily do this in 1C 8.3 using the document Transfer of equipment for installation: OS and intangible assets – Transfer of equipment for installation:

Let's create a new document and move on to filling out the header:

- Construction object - we will indicate the OS that will be obtained during the assembly process;

- Cost account – account for accounting of the construction project;

- Cost item – indicate the item for accounting for construction costs;

- Organization – indicate the one you need (if there are several);

- Warehouse – specify a warehouse, equipment will be written off from it.

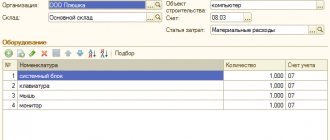

Next, in the document table, we will add all the components that arrived at account 07. We will indicate the quantity, and the invoice will be entered automatically:

Click Post and close. Let's see what postings the document made: the 1C 8.3 Accounting 3.0 program generated the correct postings - Dt 08.03 Kt 07 transfer of equipment for installation:

If installation (assembly) of the OS from components occurs on the side

There are cases when the installation (assembly) of the OS from components occurs externally. Then these expenses are documented in 1C 8.3 with the document Receipt: Purchases - Receipt (acts, invoices). The document is created in the same way as at the stage of purchasing components, and we select the type of operation Equipment:

We are interested in the Services tab. Here we will add a new line where we indicate the name of the service. Be sure to indicate the cost account 03/08 and indicate the construction project in the first subconto:

After completing the document, we will evaluate what movements were generated by the 1C 8.3 program. We see that assembly services are included in the initial cost of the OS:

Acceptance of the collected OS for accounting

After all costs have been collected on account 08.3, it is necessary to accept the collected OS for accounting in the 1C 8.3 database. Let's move on: fixed assets and intangible assets - Acceptance for accounting of fixed assets:

By clicking on the link, we will go to the Acceptance for accounting of fixed assets journal, where we will add a new document. Let's fill it out. In the header:

- Organization – select the one you need from the directory (if there are several of them);

- Event – indicate the OS event. For example, Acceptance for accounting with commissioning;

- MOL – we will indicate the financially responsible person;

- OS location – indicate the storage location from the reference. Divisions:

Next, on the Non-current asset tab:

- Type of operation – indicate the type of operation. In the example under consideration – Construction site;

- Method of receipt – method of receipt of the OS;

- Construction object – indicate our construction object;

- Warehouse – where equipment is stored;

- The account is the one where the equipment is accounted for.

If everything is filled out correctly, then after clicking Calculate amounts, the 1C 8.3 program will automatically generate the initial cost of the operating system according to accounting and accounting records. This amount will be debited from the account on 03/08:

Let's go to the Fixed Assets tab. The document table here is not filled in yet. To fill it out, you need to create an OS:

Let's go to the Fixed Assets directory by clicking on the Fixed Assets field in the tabular section. There we will add a new element by clicking Create:

Most of the details will be filled in after the OS is accepted for accounting, so for now we will only fill in the name and accounting group:

Click Record and Close. Let's select a new OS in the document of acceptance for accounting:

Let's move on to the Accounting tab. Let's fill in:

- Accounting account;

- Accounting procedure;

- Depreciation account;

- Method of reflecting depreciation expenses;

- Useful life:

Also, by analogy, fill in the required fields on the Tax Accounting tab:

Let's post the document by clicking Post. Let's see what postings were generated by the 1C 8.3 program. We see that the OS from the components in 1C 8.3 has been successfully accepted for accounting.

From the document of acceptance for accounting in 1C 8.3, you can also print the Certificate of Acceptance and Transfer of OS:

An example of filling out the Certificate of Acceptance and Transfer of OS (OS-1):

We can also create a “turnover” to make sure that all actions are correct: Reports – Balance sheet:

We see that on 07 and 08.03 the accounts were closed, and in 1C 8.3 on 01.01 a new OS, assembled from components, appeared in debit:

Thus, we learned how to assemble the main tool from components in 1C 8.3. On the PROFBUKH8 website you can read other free articles and video tutorials on the 1C Accounting 8.3 (8.2) configuration. A full list of our offers can be found in the catalog.

How in 1C 8.2 (8.3) to make changes to the information on the fixed assets, in the case when the fixed assets are first used in one division and depreciation is calculated according to one account, then the fixed assets are transferred to another division, the MOL changes, the account for accounting for depreciation costs changes - see our video lesson:

Give your rating to this article: (

1 ratings, average: 5.00 out of 5)

Registered users have access to more than 300 video lessons on working in 1C: Accounting 8, 1C: ZUP

Registered users have access to more than 300 video lessons on working in 1C: Accounting 8, 1C: ZUP

I am already registered

After registering, you will receive a link to the specified address to watch more than 300 video lessons on working in 1C: Accounting 8, 1C: ZUP 8 (free)

By submitting this form, you agree to the Privacy Policy and consent to the processing of personal data

Login to your account

Forgot your password?

Creating a fixed asset using an economic method in 1C 8.3 ACCOUNTING

Content:

1. Posting of parts in 1C

2. Transfer of materials into non-current assets

3. Calculate salary in 1C

4. We will put the server into operation using the document Acceptance for accounting in 1C

In practice, a situation often arises when it is necessary to assemble a fixed asset from materials in the warehouse. Let's understand this process using an example in 1C 8.3 Enterprise Accounting 3.0:

15.01. 2021, Vesna LLC purchased parts for the server in the amount of 124,200.00 rubles, including VAT 20,700.00 rubles. A system administrator was hired to assemble and connect the server.

It is necessary to put the fixed asset – “Server” – on the balance sheet.

Posting of parts in 1C

Let’s create a document “Receipt of goods” and select the value of the accounting account for spare parts – 10.05 – “Spare parts”.

Next, we look at the movements of the document and see: spare parts were credited to 1C in the amount of 103,500.00 rubles excluding VAT.

Transfer of materials into non-current assets

We formalize the transfer of materials into non-current assets using the “Demand-invoice” from the “Production” section.

On the “Cost Account” tab, select account 08.03 “Construction of fixed assets”, fill in the sub-account as in the picture. We carry out the document.

Let's look at the movement along the wires.

Thus, we wrote off the spare parts to VNA.

Let's calculate salary in 1C

System administrator Viktor Petrovich Ivanov assembled and tested the server from 01/27/2020-01/31/2020. The employee's salary is 80,000.00 rubles. Let's calculate the salary in 1C for assembling a server: 80,000/17*5 = 23,530.00 rubles.

To accumulate wage costs on account 08.03, we will make the following settings:

In the “Salary Settings” reference book, we will create a new type of accrual: “Server assembly”.

In the same section in the directory “Salary Cost Items” we will create two new types of Social Insurance Fund: “Server Assembly” and “Insurance Contributions (Server Assembly)”.

This will allow us to see all the expenses when calculating salaries separately for the server assembly in 1C 8.3 Enterprise Accounting 3.0.

Let’s create the “Payroll” document in the Salaries and Personnel section dated January 31, 2020, fill it out and click the “Accrue” button to select the previously created “Server Assembly” view.

Let's calculate our costs:

· cost of materials – 103,500.00 rubles;

· salary of an assembly worker – 23,500;

· employee contributions for assembly – 23500*30.2%=7106.06 rubles.

Total: 134,136.06 rubles.

We will also check our calculations in the SALT report for account 08.03 for January.

We will put the server into operation using the document “Acceptance for accounting” in 1C

Upon completion of all assembly work, we will put the server into operation using the “Acceptance for OS accounting” document. Fill in the lines and click on the “Calculate” button. The program will automatically calculate the initial cost of the OS.

Having filled out all the bookmarks, we post the document. The process of creating and accepting fixed assets for accounting is completed.

With us, the incomprehensible becomes simple, and the complex becomes automated!

Specialist

Serebryakova Galina Stanislavovna