Maintaining accounting records in the public sector

A budgetary institution is a separate non-profit organization formed in the Russian Federation at any level for the purpose of providing state and municipal services and implementing specific government programs (7-FZ of January 12, 1996).

Currently, there are 3 types of such institutions:

- budget;

- autonomous;

- official

Accounting at an enterprise of this type is regulated by the current budget legislation, as well as 402-FZ “On Accounting” dated December 6, 2011.

Let's consider three types of state budgetary institutions in a comparative table:

| Name of comparative parameter | Budget | Autonomous | State-owned |

| NPA | 7-FZ “On Non-Profit Associations and Companies” | 174-FZ “On Autonomous Organizations” | BC RF |

| Main activity | Providing services to the population in the field of science, education, healthcare, social protection | Provision of public services and performance of certain functions | |

| Possibility of using funds from income-generating activities | Possible at the discretion of the organization (clauses 2, 3 of Article 298 of the Civil Code of the Russian Federation) | Transfer of such income to the regional and federal budgets | |

| Main source of funding | Subsidization | Budget resources | |

| Document on the basis of which funds are spent | Financial and economic activity plan | Budget estimate | |

| Checking account | In the Federal Treasury | In FCs and commercial banks | In FC |

| Ownership of property | Right of operational management | ||

| Disposal of property objects | Upon receipt of the consent of the owner of the property | ||

| Responsibility for basic obligations | Liability with one’s own assets, except for cases when such obligations are formed due to harm to citizens, in the absence of assets that can be disposed of (liability remains with the founder) | Responsibility is exercised through monetary means. If there are any shortages, the founder becomes liable. | |

Planning income and expenses

When a budgetary institution in its charter has prescribed the right to conduct income-generating activities, it is necessary to include indicators of planned revenues in the FCD plan.

The requirements for the FCD plan are determined by order of the Ministry of Finance of the Russian Federation dated July 28, 2010 No. 81n (hereinafter referred to as Requirements No. 81n). A financial management plan is drawn up using the cash method and includes indicators for receipts and payments. The indicators of the approved FCD plan for the next year and planning period can be clarified if necessary (clauses 9, 17 of Requirements No. 81n).

The budgetary institution reflects information on planned receipts (income) and payments (expenses), as well as the amounts of changes made to the indicators of assignments, in the corresponding analytical accounts of account 504.00 “Estimated (planned) assignments.” The balance of account 504.00.100 “Estimated (planned) income assignments,” as well as its credit turnover, show the amounts that the institution plans to receive in accordance with the FCD plan. The balance of account 504.00.200 “Estimated (planned) assignments for expenses,” as well as its debit turnover, show the amount of expenses that the institution plans to make in accordance with the FCD plan.

The amounts of receipts (income) of the institution approved by the FCD plan are reflected in the debit of the analytical accounts of account 507.00.000 “Approved volume of financial support.” The debit balance of the specified account shows the amount of funds that are provided within the planned assignments for income (receipts) by the FCD plan, but have not yet been credited to the institution’s personal account.

The amounts of receipts and income received from financial security, as well as the return of previously received income and receipts are recorded in account 508.00.000.

The analytical accounting accounts of account 506.00.000 “Right to assume obligations” reflect information on the implementation of planned assignments for the institution’s expenses. Credit turnover on the specified institution account shows the volume of rights to assume obligations, and the credit balance shows the free balance for accepting obligations.

Income-generating activity is, in particular, the profit-generating production of goods, works and services that meet the goals of creating a non-profit organization, as well as the acquisition and sale of securities, property and non-property rights, participation in business companies and participation in limited partnerships as an investor .

Budgetary institutions are vested with the right to carry out income-generating activities, provided that this activity serves to achieve the goals for which the institution was created and corresponds to the goals specified in the constituent documents of the institution (clause 3 of article 298 of the Civil Code of the Russian Federation and clause 2 of article 24 Federal Law of January 12, 1996 No. 7-FZ “On Non-Profit Organizations”).

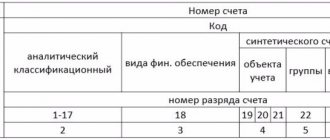

Sections 24-26 of the account number for analytical accounting of accounts 504.00.000, 506.00.000, 507.00.000, 508.00.000 reflect the corresponding KOSGU codes. Please note that in accordance with the order of the Ministry of Finance of the Russian Federation dated December 27, 2017 No. 255n, the procedure for applying KOSGU has changed in 2021.