Which regulatory act approved the financial statements of KND 0710099

The list of reports included in the accounting records is determined by Order of the Ministry of Finance of Russia dated July 2, 2010 No. 66n. This document divides the sets of prepared reporting forms into 2 types:

- Full;

- Simplified.

The simplified version is available to persons who are permitted by law to conduct accounting using the simplified version (small enterprises, non-profit organizations, participants in the Skolkovo project). At the same time, they must fully meet the conditions provided for in paragraph 5 of Art. 6 of Law No. 402-FZ of December 6, 2011 “On Accounting”.

Both sets include:

- Balance.

- Income statement.

- Report on the intended use of funds.

- Explanations for accounting.

The first three documents for full and simplified reporting are different, since simplification entails combining report indicators, and therefore changing the number of lines in it. The last two documents are drawn up only if necessary.

The full set of reporting forms additionally includes reports:

- about changes in capital;

- about cash flow.

Each of the above forms has its own code according to OKUD (All-Russian Classifier of Management Documentation), indicated in its upper right corner. The codes are assigned numbers 0710001-0710004, 0710006, of which 0710001 and 0710002 correspond to the balance sheet and income statement. Moreover, for the simplified and full forms they do not differ. Numbers 0710003, 0710004 and 071006 are assigned respectively to statements of changes in capital, cash flows and intended use of funds.

As you can see, accounting (financial) statements 0710099 are not among them. However, accounting statements 0710099 have every right to exist. The fact is that this code is assigned by another classifier (departmental, used by the Federal Tax Service).

The departmental tax classifier not only takes into account the codes entered by OKUD, but also supplements them with its own. It is in the KND (classifier of tax documentation) that the accounting reporting form 0710099 is present. At the same time, it is more correct to call it with reference to the classifier - accounting (financial) reporting form according to KND 0710099.

General points

First of all, you should familiarize yourself with what reporting on this form is and what the main features of this paper are.

What it is

KND 0710099 is a code corresponding to the tax documentation classifier. Today, any reporting form that has been approved by the Federal Tax Service for reporting is distinguished by its unique code, and in this case we are talking about the recommended form that should be used when filing reports in paper form.

This format for submitting financial statements is supported by the inspection’s standard software, and therefore employees of this body have the opportunity to accept the statements in writing and process them.

The abbreviation KND itself stands for “classifier of tax documentation”, and it was adopted in 1999 by order of the Ministry of Taxes of Russia No. AP-3-14/319.

Order On Forms of Accounting Reports

Adj. No. 1 Balance Sheet and Income Statement

Adj. No. 2 Cash flow statement

Adj. No. 2 Report on the intended use of funds

Adj. No. 2 Statement of changes in capital

Adj. No. 3 Explanations

Adj. No. 4 Line codes

Adj. No. 5 Simplified forms

Paper Features

In accordance with this form, financial statements are submitted in electronic form. Machine-readable forms include the same set of indicators as in the elements of financial statements, which were established in accordance with Order of the Ministry of Finance No. 66n, issued on July 2, 2010.

In this regard, the total number of indicators and, accordingly, the number of sheets can be reduced only after appropriate changes are made to the accounting documents.

Proposals related to reducing the volume of financial statements can be addressed directly to the Ministry of Finance.

In addition, the department also says that annual reporting includes:

- report on the financial results of the company;

- balance sheet;

- appendices to these documents.

Small businesses have the right to use simplified financial statements, which include much fewer indicators.

What is accounting reporting form according to KND 0710099

Code 0710099 is assigned in the KND to a form containing all the reports included in the full version of the accounting report. But this form is standardized to accept a report in machine-readable form and forms the basis for electronically submitted reporting. Its latest formats are reflected by the order of the Federal Tax Service of Russia dated March 20, 2017 No. ММВ-7-6/ And using the barcode available in the upper left corner of each page of the form, such a report can be easily submitted on paper.

The accounting (financial) reporting form KND 0710099 is not the only one that combines several forms with the code OKUD. A similar form with code KND 0710096 was created for a simplified version of accounting. Its electronic version is also presented in the order of the Federal Tax Service of Russia No. ММВ-7-6/

Cash flow statement

The report is intended to provide information in two areas:

- firstly, using the tabular part of the report, you can trace the movement of funds during the period, how their amount changed: how much money was at the disposal of the organization at the beginning of the period, what amount of funds was received and how much was spent, what amount is in the balance at the reporting date;

- secondly, from the reports one can draw a conclusion about the company’s activity in investment and financial activities.

The report provides for the reflection of information in the context of current activities - the main aspect, as well as activity in the field of investment and finance - additional aspects. This allows reporting users to draw additional conclusions about the organization's performance and interests.

Receipts and expenditures of funds are detailed in the report for the corresponding items of income/expense.

The report form was also put into use by Order of the Ministry of Finance No. 66n dated July 2, 2010, and was assigned OKUD code 0710004. Like the main forms, it is used by all legal entities with the exception of banks, insurance companies and budgetary institutions.

Where is the accounting reporting form KND 0710099?

All versions of this form, starting from 2011, are available on the sites:

- JSC "GNIVC" in templates for accounting forms (https://www.gnivc.ru/inf_provision/form_templates/forms_buch/);

- Federal Tax Service of Russia in templates for accounting (financial) reporting forms (https://www.nalog.ru/rn78/taxation/submission_statements/).

Here you can find accounting statements KND 0710099, as well as a simplified accounting form with code KND 0710096.

Why do you need a summary report form? Then, you first need to create a report by entering all the necessary data into it. And only after verification can you generate a report that will be sent to the tax office electronically.

Well, to prepare a paper version of accounting reporting 0710099 you will have to do even more so. You can download it here:

Read also

11.12.2017

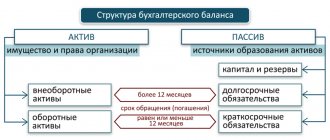

Balance sheet

The basis of the financial statements of any company is the balance sheet , which reflects the state of affairs in the organization from the financial side. The information contained in this form characterizes the financial condition of the business entity as of the reporting date - at the end of the quarter for interim reporting, as of December 31 for annual reporting.

Information in the balance sheet is distributed into two parts of indicators - assets and liabilities, and into five sections - this distribution depends on the maturity period (for the active part) or maturity (for the passive part).

The first part of the balance sheet is Assets , which are distributed into two sections: non-current and current. The first section, which characterizes non-current assets, reflects information on fixed assets, intangible assets and long-term investments. The second section, which characterizes current assets, shows data on inventories, accounts receivable (buyers, suppliers for advances, other debtors), financial investments for up to a year and the availability of cash in hand and a bank account.

The second part of the balance is Liabilities , which are distributed into three sections. The first section of this part discloses information about capital and reserves (the amount of authorized capital, as well as additional and reserve capital, plus retained earnings (loss)). The second section provides data on the amount of long-term liabilities to banks (loans) and other creditors (loans, etc.). The last section contains information on short-term liabilities to banks (loans with a repayment period of up to a year), accounts payable to suppliers and customers for advances received, and other debt.

The balance sheet is drawn up in the form approved by Order of the Ministry of Finance of the Russian Federation No. 66n dated July 2, 2010, OKUD code 0710001. The form is used by all organizations, with the exception of credit, insurance and budget institutions.

New forms of accounting: how to apply

The Federal Tax Service has sent recommended machine-readable forms of financial statements - general and simplified - for use in work. Also in the letter from the Federal Tax Service, updated control ratios of accounting indicators were published. The letter was a logical continuation of the adoption of Federal Law No. 444-FZ dated November 28, 2018, the publication of Order No. 61n of the Ministry of Finance of the Russian Federation dated April 19, 201, and the approval of the new edition of PBU 18/02 “Accounting for corporate income tax calculations.”

Accounting information resource

Federal Law No. 444-FZ dated November 28, 2018 “On Amendments to the Federal Law “On Accounting” provides that from 2020, instead of submitting to statistics, the obligation to submit reports to the tax authority for inclusion in the accounting reporting information resource is introduced. It will be conducted by the Federal Tax Service. All functions related to the submission of reports - the development of forms and formats, the procedure for submission - were transferred to the tax authorities.

And all those reporting will submit financial statements electronically, and this will already affect the report for 2021.

The exception is representatives of small businesses. They are allowed to submit financial statements to the tax office on paper or according to the TKS.

All document flow will be electronic, including the presentation of the audit report in cases of mandatory audit. Reporting and conclusions will be transmitted via TCS through EDI operators.

The following are exempt from submitting a mandatory copy of reporting to government resources:

- public sector organizations;

- Central Bank (it will submit reports to the Federal Tax Service in a special manner);

- religious organizations;

- organizations submitting accounting (financial) statements to the Central Bank;

- organizations whose reports contain information classified as state secrets;

- organizations in cases established by the government.

The last two categories will continue to report to statistics.

Interested users (with the exception of government agencies, local governments and the Bank of Russia) will be able to obtain information from the accounting reporting information resource for a fee.

Accounting reporting forms have been changed

Order of the Ministry of Finance of Russia dated April 19, 2019 No. 61n introduced changes to the financial reporting forms approved by Order of the Ministry of Finance of Russia dated July 2, 2010 No. 66n.

The amendments affected all forms of reporting: balance sheet, statement of financial results, statement of changes in capital, report on the intended use of funds, as well as simplified reporting for small businesses.

The type of economic activity in all forms must now be indicated in accordance with OKVED-2. In addition, all forms must be filled out in thousands of rubles only. Unit of measurement "millions" rub." excluded from all forms.

A new line “Accounting statements are subject to mandatory audit” is included in the balance sheet form. If applicable, enter “1”. If not – “0”. If there is such an obligation, the auditor’s data is provided in the balance sheet: name of the audit organization (full name of the individual auditor), INN, OGRN (OGRNIP).

The most significant changes were made to the “Statement of Financial Results” form.

The composition and name of the indicators disclosing the amount of income tax have been clarified (see Information message dated May 28, 2019 No. IS-accounting-18). In this regard, the report contains the following articles:

- income tax - expense (income) for income tax (previously absent);

- current income tax (formerly current income tax, including permanent tax liabilities (assets));

- deferred income tax (previously – change in deferred tax liabilities, change in deferred tax assets);

- tax on profit from operations, the result of which is not included in the net profit (loss) of the period (participates in the formation of the total financial result of the period) (previously it was absent).

The names and codes of report lines have been changed accordingly.

The name of line 2410 has been changed. It is now called “Income Tax”. In addition, lines 2421, 2430 and 2450 were excluded from the form. They indicated the amounts of permanent tax liabilities (assets) and changes in deferred tax liabilities (assets). New lines have been introduced instead of these lines:

- 2411 “Current income tax”;

- 2412 “Deferred income tax”;

- 2530 “Tax on profits from transactions, the results of which are not included in the net profit (loss) of the period.”

In the simplified form of the income statement, the line names have not changed. However, in the line “Income tax (income)”, instead of current income tax and changes in deferred tax liabilities (assets), current and deferred income taxes should now be reflected.

Thus, the reporting forms of the financial statements reflect changes in PBU 18/02 “Accounting for calculations of corporate income tax”, which were approved by Order of the Ministry of Finance dated December 1, 2018 No. 236n. They must be applied without fail, starting with reporting for 2021. In this case, early application is possible.

Therefore, organizations are required to apply amendments made to the financial results statement (including in a simplified form) from the financial statements for 2021. However, they can apply these amendments earlier than the specified period if they make such a decision. The remaining amendments, mainly technical, are effective from June 1, 2021.

The reporting deadlines remain the same.

New machine-readable forms and control ratios

In the letter commented on, the Federal Tax Service published recommended machine-readable reporting forms that must be submitted to the tax authorities for the reporting year 2021.

Two packages of documents were presented:

- "Financial statements". Includes a balance sheet, income statement, statement of intended use of funds, statement of changes in capital, statement of cash flows;

- "Simplified accounting reporting." Includes the same reports, only in a simplified version - for small businesses.

Also given are the control ratios necessary to verify the financial statements provided.

The main changes in reporting are related to the “Statement of Financial Results” form. The name, line numbers and composition of the “Income Tax” indicator have changed. The control ratios of the “Net profit” line change accordingly.

Thus, “Net profit or loss” of the report on line 2400, column 4, 5 is equal to the sum of the lines (column 4, 5, respectively):

- 2300 “Profit (loss) before tax”;

- 2410 “Income tax”;

- 2460 "Other".

If a line indicator is in parentheses, a minus sign is placed in front of it.

The indicator “Cumulative financial result of the period” for line 2500, column 4, 5 is equal to the sum of lines (column 4, 5, respectively):

- 2400 “Net profit (loss)”;

- 2510 “Result from the revaluation of non-current assets, not included in the net profit (loss) of the period”;

- 2520 “Result from other operations not included in the net profit (loss) of the period”;

- 2530 “Tax on profits from transactions, the results of which are not included in the net profit (loss) of the period.”

The rule for reflecting the indicator in brackets also applies here, as in the previous case.

The letter also discloses other control ratios based on the interrelation of indicators of other reporting forms.

But what should those who decided not to apply the changes provided for by Order No. 61n and the new edition of PBU 18/02 in their reporting for 2021 do?

They will all find the answer in the commented letter.

So, as part of the “Statement of financial results” form there is a sheet “Additional lines of the statement of financial results”. This is what you need to fill out in this case. It repeats the line composition of the old report, which is now excluded from the new form. And the indicator in the line “Current income tax” of this sheet must be indicated on line 2411 of the Statement of Financial Results.

Tasks

The reference book itself focuses on the relationship between budget classification codes and tax return codes. This is necessary, from the point of view of tax regulation, in order to automatically open obligations to the Federal Tax Service of the Russian Federation.

The LPCs themselves are also intended for:

- simplified reception and prompt processing of reports from individuals and legal entities, organizations and individual entrepreneurs (according to the indicator under discussion, specialists from the Federal Tax Service of the Russian Federation can quickly check the correctness of the BCC indication, which significantly reduces the time spent on processing);

- correct and prompt conduct of on-site inspections by the Federal Tax Service of the Russian Federation (based on the indicator under discussion, specialists quickly establish a list of BCCs; it is also used when checking zero reporting forms).

Zero declaration

1 There is no activity, do you need to report?

It often happens that at the beginning of activity, after registering an LLC or individual entrepreneur, it is not possible to start your own business for several reporting periods. As a result, there are expenses, but no income.

Or there are no business transactions. And here the question arises:

“In the absence of activity, do I need to report to the tax authorities or the Pension Fund?”

The answer is clear - they are required to report within the appropriate deadlines, submitting zero declarations or calculations, so as not to receive a fine.

This applies to all taxpayers, organizations, and individual entrepreneurs, no matter what tax system they are on.

The mere fact of lack of activity is not a violation. But for failure to submit (late submission) of zero declarations, fines in the amount of 1000 rubles are provided. 2 Who submits a zero declaration under the simplified tax system A zero declaration under the simplified tax system must be submitted by LLCs and individual entrepreneurs in the form KND-1152021.

Accounting (financial) reporting form according to KND 0710099

Copyright: Lori's photo bank At the end of each year, accounting (financial) statements - KND form 0710099 - are submitted by business entities to the tax office.

A distinctive feature of these reporting forms is the presence of a special barcode and the possibility of transmission in electronic form.

Let's consider the composition and features of these reporting forms. regulated by Art. 14 of the Law of December 6, 2011

No. 402-FZ. Templates for reporting forms, including simplified ones, were approved by the Ministry of Finance in Order No. 66n dated July 2, 2010. Each form has its own OKUD code. If reporting is generated for internal users, you can use the forms from Order No. 66n without line codes, the same forms can be used for submission to , (with completed line codes).

Simplified reporting

If a company has the right to conduct simplified accounting, then the use of standard accounting forms is inappropriate. For subjects of this category, legislators have developed special forms: simplified accounting.

Previously, lightweight accounting included KND form 0710098, but the updated Order of the Ministry of Finance No. 66n, which came into force in 2015, adjusted the current list of reporting formats. Now all accounting reports are divided into two large groups:

- Standard - mandatory for most taxpayers who are required to keep records in generally accepted ways.

- Simplified - they are filled out by organizations and small businesses that maintain simplified accounting.

Now let’s determine who has the right to keep records in a simplified way.