Categories

- VAT 2021. VAT deduction

- Insurance premiums 2020

- VAT return 2020

- USN income 2021. All about the simplified taxation system 2020. Simplified

- Cost accounting. Accounting for expenses and income

- Accounting. Accounting

- FSS. 4 Form FSS 2020

- Trade fee 2020

- UTII in 2021. Single tax on imputed income

- Trademark

- Maternity

- Children's benefits 2020

- Sick leave 2020

- Travel expenses 2020

- Vacation pay 2021. Calculation of vacation pay

- Personal income tax 2020

- Individual entrepreneur taxes 2021. Individual entrepreneur - all about taxes

- Transport tax 2020

- Salary, labor relations

- Pension Fund. News. Articles

- Income tax 2020

- Maternity capital 2020

- Source documents

- Property tax 2020

- We correct accounting errors. Fines, penalties.

- Cash register, cash register, cash and non-cash payments

- Tax (on-site, office) and other audits

- New in legislation

- Fixed assets, intangible assets, accounting of materials, goods, warehouse, loss

- Reporting: tax, accounting.

Property tax

Property tax is collected from organizations on the OSN, simplified tax system and UTII. Moreover, companies are subject to tax on special tax purposes not only on real estate, but also on movable types of property. It is the taxation of movable property that has its own characteristics regarding reorganized companies.

According to clause 25 of Article 381 of the Tax Code of the Russian Federation, economic entities are provided with a benefit according to which they are not required to pay tax on movable property recorded as fixed assets from 01/01/2019. However, this benefit does not apply to companies that received their property during the reorganization process. This property is taxed in accordance with the general procedure, starting from the date of entering information about the reorganization into the Unified State Register of Legal Entities. It does not matter when the registration of ownership rights to the transferred objects is carried out.

Taxation occurs at the cadastral value if the property is included in the cadastral list. In other cases, at the average annual cost. This method of calculating property tax for reorganized companies was approved by letter of the Federal Tax Service No. BS411/ dated June 27, 2016.

Useful information about property tax during reorganization is contained in this video:

Asking is faster than reading! Ask a question using the form (below), and within an hour a specialized specialist will call you back to provide a free consultation.

Other forms

The table shows the main time guidelines for when it is necessary to submit 2-NDFL certificates for other types of reorganization.

| Type of changes | Deadlines to meet when submitting certificates |

| Spin-off involves the creation of new organizations - one or several. In this case, there is a transfer of part of the powers of the reorganized company. At the same time, its activities remain unshakable | Since the activity does not stop, the main organization brings certificates according to the general rules at the end of the reporting year, on the same basis as a legal entity separated into a separate business |

| Transformation Represents a reorganization and transformation from one person to another with a change of form. Thus, an LLC can take a different form and re-qualify as a joint-stock company, a commercial cooperative, or a partnership. For JSC - to LLC, cooperative | An organization that has been reorganized must submit certificates in accordance with the generally established procedure and deadlines |

Regardless of the form in which the reorganization takes place, the successor is not assigned the duties of a tax agent from the original organization in accordance with Article 50 of the Tax Code. Therefore, the successor should not represent 2-NDFL for her.

Let's summarize. Depending on the procedure, the procedure for submitting documentation on the income of individuals to the relevant tax authorities is individual. Certificate 2-NDFL within the framework of liquidation is in any case submitted under general conditions. When reorganizing a business, it is necessary to proceed from a specific situation, all possible options of which are described above.

Termination of activities of one of the companies

Depending on the situation, the outcome may vary. So, if one of the companies is subject to liquidation, this indicates that a new entity is being formed. Therefore, there are more nuances in the reporting documentation provided. If there is no liquidation and all firms are operational, then it is assumed that the company continues to operate. Therefore, you need to bring proof of income in accordance with the generally established procedure.

| Type of changes | Deadline for submitting income information |

| Merger Aims to create a new company consisting of two or more former legal entities. As a result, they cease their activities | 2-NDFL is submitted by the reorganized company before the day when state registration of the new legal entity occurs. The latter must send certificates of income for the year according to the general rules |

| Affiliation is a form of introducing change in which there is a transfer of authority from one company to another. In this situation, the affiliated organization ceases to exist | The merged company submits certificates before the date on which the record of its liquidation is made in the Unified State Register of Legal Entities. As for the company it joined, it submits reports based on the results of the year according to generally established rules |

| Division involves the transfer of powers to companies that are created again. And the original company ceases its activities and is liquidated | The organization that has undergone changes submits 2-NDFL until the state registration of new legal entities occurs. Newly formed companies must submit documents according to generally established rules |

Thus, the tax authorities must receive at least two certificates from companies. This is due to the fact that information on income received by individuals is submitted by the existing company - before the procedures are carried out, and then by another company formed after the changes (the tax period lasts from the beginning of its activities until the end of the year). If more than two companies took part in the process of all perturbations, then the number of sets of certificates will be correspondingly large.

How to fill out 2-NDFL reporting during reorganization

Question

: How to fill out and submit reports on Form 2-NDFL during reorganization?

Answer

: Before completion of the reorganization, the organization fills out and submits to the tax authority at the place of its registration forms 2-NDFL for the period of time from the beginning of the calendar year until the day its reorganization is completed. If this obligation is not fulfilled, these forms are submitted by the legal successor to the tax authority at the place of its registration, in which the OKTMO code of the reorganized organization must be indicated in the “OKTMO Code” field. The assignee also submits Form 2-NDFL for the period from the moment of its creation as a result of the reorganization until the end of the year.

Rationale

: Reorganization of a legal entity can be in the form of merger, accession, division, separation, transformation. A legal entity is considered reorganized, with the exception of cases of reorganization in the form of merger, from the moment of state registration of legal entities created as a result of the reorganization. When another legal entity is merged with a legal entity, the first of them is considered reorganized from the moment an entry is made in the Unified State Register of Legal Entities about the termination of the activities of the merged legal entity (clauses 1, 4 of Article 57 of the Civil Code of the Russian Federation).

Reporting during reorganization: what mistakes should a successor be wary of?

- News

- Registration and registration

Reporting during reorganization: what mistakes should a successor be wary of?

April 5, 2021 Elena Mavritskaya Leading expert, chief accountant with 10 years of experience

In most cases, the final tax returns of a reorganized company are submitted by its legal successor.

He needs to take into account a number of nuances: combine the bases in the VAT declaration, separate the bases in the profit declarations, indicate the correct INN and KPP, etc.

Our article will help you fill out basic reports for the Federal Tax Service: income tax, VAT, property tax returns, as well as forms 2-NDFL and 6-NDFL.

Since January 2021, a rule has appeared in the Tax Code regulating the procedure for submitting final personal income tax reports for a reorganized company. So, if before the moment of reorganization the company did not have time to submit forms 2-NDFL and 6-NDFL, then its legal successor must do this (clause 5 of Article 230 of the Tax Code of the Russian Federation).

Such reporting must be submitted to the Federal Tax Service at the place of registration of the legal successor. An important detail: an organization that reports both as a tax agent and as a legal successor must submit separate forms 2-NDFL and 6-NDFL.

In other words, you should report twice: the first time for your predecessor, and the second time for yourself.

Let us remind you that starting with reporting for 2021, you need to use form 6-NDFL with the amendments made by order of the Federal Tax Service of Russia dated January 17, 2018 No. ММВ-7-11 / [email protected] (see “New form 6-NDFL will be used for reporting for 2021").

Also, for reporting for 2021, you need to use form 2-NDFL with the changes made by order of the Federal Tax Service of Russia dated January 17, 2018 No. ММВ-7-11/ [email protected] However, you can report for 2021 using the previous form 2-NDFL (see.

“2-NDFL for 2021: tax authorities allowed to report using the old form”).

Please note: when submitting 6-NDFL and 2-NDFL, those tax agents who use web services to prepare and check reports (for example, the Kontur.Extern system for sending reports) will feel most comfortable.

There, all necessary updates and current test programs are installed automatically, without user intervention.

If the tax agent has chosen a form that does not correspond to the reporting period, or has filled out the form incorrectly, the system will certainly warn him about this and tell him how to correct the errors.

Fill out, check and submit 6-NDFL and 2-NDFL through “Kontur.Extern”

Table 1

How to fill out 2-NDFL and 6-NDFL for a reorganized company

Field name

Form 2-NDFL

Form 6-NDFL

| Reorganization (liquidation) form code | 1 - transformation 2 - merge 3 - separation 5 - connection 6 - separation with simultaneous joining | |

| By location (registration) (code) | 215 (for the largest taxpayers - 216) | |

| Tax agent | name of the reorganized organization or its separate division | |

| TIN/KPP of the reorganized organization | TIN and KPP of the reorganized company or its division | TIN and KPP of the reorganized company or its division. In this case, the TIN and KPP of the legal successor are indicated at the top of the title page |

| OKTMO code | OKTMO of the reorganized company or its division | OKTMO at the location of the workplace of the employee of the reorganized company |

| Sign | 4 - if the legal successor submits a certificate to the Federal Tax Service; 3- if the legal successor issues a certificate to an individual at his request |

VAT and income tax returns

If the company did not have time to submit its final income tax return before the reorganization, its legal successor must do so.

The Russian Ministry of Finance announced that reporting should be submitted to the inspectorate at the place of registration of the legal successor (letter dated 02/09/18 No. 03-03-06/1/7849; see “The latest income tax return for a transformed organization can be submitted by its legal successor”).

This letter is about transformation, but it can also be used as a guide for other forms of reorganization.

Please note: the successor cannot combine its data and the data of the reorganized company in reporting. This means that he needs to submit two declarations: one for himself and the other for his legal successor.

In particular, in the case of transformation, the first declaration will reflect the period from the beginning of the year until the moment of transformation (the data of the predecessor is indicated), and the second - the period from the moment of transformation to the end of the current year (the data of the successor is indicated).

As for value added tax, the situation here is somewhat different. The legal successor must also report for the reorganized company, which did not have time to submit the final declaration. But, unlike profit reporting, he needs to combine both his and his predecessor’s operations in one VAT return.

This is stated in the letter of the Federal Tax Service of Russia dated 05.13.15 No. 24-15 / [email protected] , dedicated to the transformation (see “Tax officials explained the features of submitting a VAT return when transforming an organization”) and in the letter of the Federal Tax Service of Russia dated 03.09.11 No. KE -4-3/ [email protected] , dedicated to joining.

This approach, in our opinion, should be applied to other forms of reorganization.

Let us add that the Tax Code does not establish special deadlines for submitting reports during reorganization.

For this reason, the successor must submit the profit declaration for the last tax period within the same time frame as the “regular” declaration, that is, no later than March 28 of the next year.

The VAT return, which includes the data of the reorganized company, is submitted by the successor no later than the 25th day of the month following the quarter in which the reorganization took place.

Submit VAT and income tax reports online for free

Personal income tax upon reorganization of a legal entity

In accordance with Art. 226 of the Tax Code of the Russian Federation, Russian organizations from which or as a result of relations with which the taxpayer received income are obliged to withhold from him and pay to the budget the amount of tax calculated in accordance with Art. 224 Tax Code of the Russian Federation. Clause 3 of Art. 210 of the Tax Code of the Russian Federation for income in respect of which the tax rate established by clause 1 of Art. 224 of the Tax Code of the Russian Federation, the tax base for personal income tax is defined as the monetary expression of such income subject to taxation, reduced by the amount of tax deductions enshrined in Art. 218 – 221 Tax Code of the Russian Federation. By virtue of clause 3 of Art. 218 of the Tax Code of the Russian Federation, standard tax deductions are provided to the taxpayer by one of the tax agents who are the source of payment of income, at the taxpayer’s choice based on his written application and documents confirming the right to such deductions.

Application of standard deductions. According to paragraph 1 of Art. 218 of the Tax Code of the Russian Federation when determining the size of the tax base in accordance with paragraph 3 of Art. 210 of the Tax Code of the Russian Federation, the taxpayer has the right to receive standard tax deductions. In paragraph 3 of Art. 218 of the Tax Code of the Russian Federation it is noted that if the taxpayer does not start working from the first month of the tax period, tax deductions provided for in paragraphs. 4 clause 1 of this article (standard tax deduction for children) are provided at this place of work, taking into account the income received from the beginning of the tax period at another place of work in which the taxpayer was provided with tax deductions. The amount of income received is confirmed by a certificate of income received by the taxpayer, issued by a tax agent in accordance with clause 3 of Art. 230 Tax Code of the Russian Federation.

Thus, the successor organization is obliged to provide employees with standard tax deductions from the moment they work in this organization, but taking into account income received from the beginning of the calendar year in which the reorganization was carried out.

Application of property and social deductions. According to the rules of paragraph 8 of Art. 220 and paragraph 2 of Art. 219 of the Tax Code of the Russian Federation, property and social tax deductions can be provided to the taxpayer before the end of the tax period when he submits a written application to the employer, subject to confirmation of the taxpayer’s right to these tax deductions by the tax authority in the form approved by the federal executive body authorized for control and supervision in areas of taxes and fees. The taxpayer has the right to receive these deductions from one withholding agent of his choice.

Thus, the tax agent is obliged to provide property and social tax deductions upon receipt from the taxpayer of confirmation of the right to these deductions issued by the tax authority.

Please note that tax legislation does not provide for the succession of persons in terms of providing deductions for personal income tax. A new organization formed as a result of reorganization cannot provide tax deductions on the basis of notifications issued by tax authorities in relation to a pre-existing employer - tax agent. Such clarifications are given in the Letter of the Federal Tax Service of the Russian Federation dated September 18, 2014 No. BS-4-11/

So, if the taxpayer at the end of the tax period was unable to take advantage of the property or social tax deduction in full, he has the right to apply to the tax authority with an application to submit a new (repeated) notification confirming the right to the tax deduction. At the same time, he submits to the tax authority two certificates in form 2‑NDFL: a certificate issued by the previous tax agent before the reorganization of the legal entity on the taxpayer’s income from the beginning of the tax period until the date of termination of the activity of this legal entity, and a certificate issued by the new tax agent on the taxpayer’s income from the date of state registration of the newly emerged legal entity until the end of the tax period.

These clarifications are presented in letters of the Ministry of Finance of the Russian Federation dated August 25, 2011 No. 03-04-05/7-599, dated December 22, 2011 No. 03-04-05/7-1089.

Insurance premiums, personal income tax and benefits during company reorganization

01.09.2019

Vitaly Semenikhin,

Head of the Semenikhin Expert Bureau

By virtue of universal legal succession, when a legal entity is reorganized, its rights and obligations are transferred to the legal successor.

Any legal entity participating in the reorganization has its own staff, which means it is a payer of insurance premiums and a tax agent for personal income tax.

Reorganization is not a basis for terminating employment relationships with staff - for the most part they continue automatically, but in such conditions the reorganized company has many questions about insurance premiums, personal income tax and the payment of benefits.

Legal basis for the reorganization of legal entities

First, we note that the general legal basis for the reorganization of legal entities is established by Chapter 4 “Legal Entities” of the Civil Code of the Russian Federation. In accordance with Art. 57 of the Civil Code of the Russian Federation distinguishes five main forms of reorganization: merger, accession, division, separation and transformation.

In addition, mixed reorganization of a legal entity is also allowed, that is, a simultaneous combination of the forms listed above, for example, reorganization in the form of transformation with simultaneous merger with another organization.

At the same time, reorganization with the participation of two or more legal entities, including those created in different organizational and legal forms, is not prohibited, if the possibility of such a transformation is provided for by the Civil Code of the Russian Federation itself or another law.

The decision to reorganize is usually voluntary, made by the founders (participants) of the company or a body of a legal entity authorized to take such actions by the constituent document.

At the same time, in the event of a business fragmentation, under certain circumstances, reorganization can also be carried out forcibly - by decision of authorized state bodies or a court.

Reorganization of a legal entity is always accompanied by the appearance of a successor (one or more), to whom the rights and obligations of the reorganized company are transferred in the order of universal legal succession.

In accordance with Art. 58 Civil Code of the Russian Federation:

- when

legal entities merge, the rights and obligations of each of them are transferred to the newly emerged legal entity; - when

a legal entity merges with another legal entity, the rights and obligations of the merged legal entity are transferred to the latter; - when

a legal entity is divided, its rights and obligations are transferred to the newly emerged legal entities in accordance with the transfer deed; - when

one or more legal entities are separated from a legal entity, the rights and obligations of the reorganized legal entity are transferred to each of them in accordance with the transfer act; - when

a legal entity of one organizational and legal form is transformed into a legal entity of another organizational and legal form, the rights and obligations of the reorganized legal entity in relation to other persons do not change, with the exception of the rights and obligations in relation to the founders (participants), the change of which is caused by the reorganization.

As a general rule, an organization is considered reorganized from the moment of state registration of the successor company created as a result of the reorganization.

The only exception is reorganization in the form of merger, during which the merging company is considered reorganized from the moment an entry is made in the unified state register of legal entities that the activities of the merging organization have been terminated.

Labor relations with employees during the reorganization of organizations

So, for the most part, the result of the reorganization of a legal entity, as a rule, is the cessation of the activities of some and the creation of new organizations.

At the same time, as already noted, reorganization is not a basis for terminating employment relations with the company’s employees, as is directly indicated by Art. 75 Labor Code of the Russian Federation. Consequently, labor relations with employees of reorganized companies who agree to work in new business conditions are preserved even after this procedure is completed.

During reorganization, the employer company has the right to terminate an employment contract with an employee in the only case - if the employee does not want to continue working under the conditions of the new employer. Moreover, this applies to all companies participating in the reorganization, both those that will cease to exist as it is completed, and those that will continue to operate.

If the employee refuses to continue working after the reorganization, the employment contract with him is terminated at the request of the employee, but on a special basis provided for in paragraph 6 of Part 1 of Art. 77 Labor Code of the Russian Federation.

Thus, basically, during reorganization (in any form), labor relations with the company’s personnel continue automatically, which means that the new employer, like his legal predecessor, calculates and pays wages to employees, and also makes other payments within the framework of labor relations.

Insurance premiums during reorganization

Source: https://www.tls-cons.ru/services/pravovoy-konsalting/stati-nashikh-yuristov/strakhovye-vznosy-ndfl-i-posobiya-pri-reorganizatsii-kompanii/

Other rules

According to the general rules of law applicable to companies, tax agents must submit data on personal income tax - 2-NDFL at the place of their registration before April 1 of the following year. This is provided for by the second paragraph of Article 230 of the Tax Code of the Russian Federation.

If there is a cessation of activity - liquidation, or changes in the structure of the enterprise, then to determine its last tax period, other rules are applied - in accordance with the third paragraph of Article 55 of the Tax Code of the Russian Federation.

Submit “2-NDFL – reorganization” if changes occur in the company. They may be associated with changes in structure, management, or the merger of companies into one. If we are talking about the complete closure of the company and the termination of its activities, confirmed by law, then there is a certificate “2-NDFL - liquidation”.

Nuances when providing 2-NDFL

The employer is required to provide 2-NDFL certificates to the Federal Tax Service at the end of the year for each employee. In general, they are submitted before April 1 of the year following the reporting year. But for reorganized companies, separate deadlines are established, depending on the form of reorganization:

- When merging, 2-NDFL must be submitted before the day of registration of the new legal entity.

- When joining, certificates are submitted before the day of making an entry in the Unified State Register of Legal Entities about the termination of the activities of the reorganized company.

- In case of division, it is necessary to report before the day of registration of new organizations.

- When separating and transforming, reporting is submitted within generally established deadlines, since there is no liquidation of the reorganized companies.

More details about the various methods of reorganization can be found in Article 51 of Law No. 14FZ of 02/08/1998. and Article 15 of Law No. 208FZ of December 26, 1995.

Newly created companies report only for themselves within the time limits established by law, since the responsibilities of a tax agent of reorganized organizations do not pass to them (Article 50 of the Tax Code of the Russian Federation).

Asking is faster than reading! Ask a question using the form (below), and within an hour a specialized specialist will call you back to provide a free consultation.

How to issue certificates 2-NDFL and 182N in case of reorganization of an organization in the form of affiliation

Questions and answers on the topic

The organization ceased operations due to reorganization in the form of merger and reported to the Federal Tax Service itself on the date of reorganization (03/15/2019). Question: An employee quits in the same year (05/25/2019), already from a new organization, how to issue certificates 2-NDFL, 182N in this case? For example: one certificate, combining data for the old and new organizations (how it is filled out) or two separate ones for each organization, but in this case it is not possible to certify the certificate from the old organization with signatures and a seal. If the certificates of the reorganized organization are certified by the successor organization, then what document should be provided to the employee for confirmation?

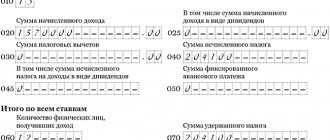

Certificate 2-NDFL is issued by the successor organization. In the certificate, indicate the name of the reorganized organization and its OKTMO code. An example of how to fill out a certificate of income for a successor in Form 2-NDFL for a reorganized company is presented below.

Certificate 182n is also issued by the successor organization. Include the work hours and earnings of the predecessor organization in the certificate.

An example of how to fill out an income certificate for a successor in Form 2-NDFL for a reorganized company

The Trading organization ceased operations on January 1, 2021 by joining the Alpha organization.

Hermes details: TIN 7708123443, KPP 770801001, OKTMO 453410000, Federal Tax Service Inspectorate 7708.

Alpha details: INN 7709123450, KPP 770901001, OKTMO 453420000, Federal Tax Service 7709.

In the 2-NDFL certificate for 2021, the legal successor of Alpha indicated:*

in the “Characteristic” field – “3”;

in the field “in the Federal Tax Service” – 7709;

in the “OKTMO code” field: OKTMO of the reorganized company – 453410000;

in the upper part: TIN and KPP of the legal successor – “Alpha”;

in the “Tax Agent” field: name of the reorganized company;

in the “Form of reorganization (liquidation)” field: code 5 – merger;

TIN and checkpoint reorganized.

I.I. Ivanov worked as an economist at Hermes. His details: Ivan Ivanovich Ivanov, citizen of the Russian Federation, date of birth - April 15, 1978, passport series 46 00 No. 462135 issued by the Voikovsky Department of Internal Affairs of Moscow on November 23, 2000, TIN 703254479214.

In 2021, Ivanov’s monthly salary was 19,200 rubles. In July 2021, Ivanov took annual paid leave and was paid vacation pay in the amount of RUB 17,300. and the salary for the time actually worked in July is 1800 rubles.

In December, Ivanov was paid a production bonus for November - 3,000 rubles. and financial assistance - 5000 rubles.

Ivanov is married and has a five-year-old son. In this regard, throughout 2021 he was provided with a standard tax deduction of 1,400 rubles. per month (subparagraph 4, paragraph 1, paragraph 2, article 218 of the Tax Code). Ivanov has no rights to other standard deductions.

The amount of standard deductions for the year amounted to 16,800 rubles.

Thus, Ivanov’s total tax base for 2021 amounted to 217,500 rubles. (19,200 rubles × 11 months + 1800 rubles + 17,300 rubles + 3000 rubles + 5000 rubles – 4000 rubles – 1400 rubles × 12 months). The amount of tax withheld was RUB 28,275.

On March 27, 2021, the successor of Alpha submitted to the inspectorate a certificate of Ivanov’s income for 2021 for the reorganized organization Hermes.*

Question

The organization ceased operations due to reorganization in the form of merger and reported to the Federal Tax Service itself on the date of reorganization (03/15/2019). Question: An employee quits in the same year (05/25/2019), already from a new organization, how to issue certificates 2-NDFL, 182N in this case? For example: one certificate, combining data for the old and new organizations (how it is filled out) or two separate ones for each organization, but in this case it is not possible to certify the certificate from the old organization with signatures and a seal. If the certificates of the reorganized organization are certified by the successor organization, then what document should be provided to the employee for confirmation?

Tags: accountant, job description of the general director, capital, tax, personal income tax, expense, Form