In 6-NDFL, fixed advance payments are shown in the amount that the employer offset when determining the amount of personal income tax to be transferred to the budget. To make the adjustment, the employer must have a written application from the foreign employee and documentary evidence of the fact that he has paid advances for the patent. Additionally, the employer fills out an application (attaching documents confirming payment) to the Federal Tax Service to receive official notification from tax authorities about the possibility of taking into account patent payments for a specific person when calculating obligations to the budget.

Read also: Fixed advance payments in the 2-NDFL certificate

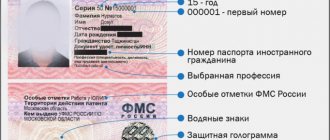

The company employs foreigners with a patent

The company employs Russian citizens and foreign patent employees. The company withholds personal income tax on all income at a rate of 13 percent.

The salaries of residents and foreigners on patent are subject to personal income tax at a rate of 13 percent. This rate is established by different standards. For residents' salaries - clause 1 of Article 224 of the Tax Code of the Russian Federation. And for foreigners - paragraph 3 of Article 224 of the Tax Code of the Russian Federation. Because of this, the tax authorities do not require you to fill out several blocks with a rate of 13 percent. The company has the right to show all income in one line 010–050.

For example

B - 7 resident employees and 5 foreigners with a patent. She did not reduce the calculated tax on advances for the patent. For the first half of the year, the company accrued income to foreigners - 630,000 rubles, calculated and withheld personal income tax - 81,900 rubles. (RUB 630,000 × 13%). She accrued income to residents - 940,000 rubles, calculated and withheld personal income tax - 122,200 rubles. (RUB 940,000 × 13%). The company recorded the income of foreigners and residents in one block of lines 010–050. In line 020 - 1,570,000 rubles. (630,000 + 940,000), in lines 040 and 070 - 204,100 rubles. (81,900 + 122,200). The company filled out Section 1 as in sample 94.

Sample 94. How to reflect the income of foreigners and residents in the calculation:

Top

Fines and penalties

The penalties for missing deadlines are strict. In this case, tax inspectors have the right to impose several types of penalties on an organization or entrepreneur:

- 1000 rubles for violating the deadline for filing 6-NDFL. This figure is multiplied by the number of months the form is overdue. For example, the agent reported on tax withholdings for the 1st quarter only in June. In this case, the fine will be 2,000 rubles.

- 500 rubles will be deducted for filing reports with errors or inaccurate data.

- 200 rubles for incorrectly submitting form 6-NDFL. This fine is relevant if an organization with more than 25 employees transferred tax data on paper.

Also, if there is a significant delay in filing reports, funds in the company’s bank accounts may be blocked.

The company reduces the calculated personal income tax on advances for a patent

The company employs a foreigner with a patent. Every month the company reduced the calculated personal income tax by the advances that the employee paid for the patent.

The employer has the right to reduce the personal income tax of foreigners for the advances they paid for the patent (clause 6 of article 227.1 of the Tax Code of the Russian Federation). To do this, you need to receive a notification from the inspectorate.

In line 020, write down the accrued income, and in line 040, the calculated personal income tax. The company reflects advances in line 050 of the calculation, and in line 070 the difference between the calculated personal income tax and advances. The difference cannot be negative. If a foreigner’s tax for the quarter is less than he paid for the patent, then the company reduces personal income tax only by part of the advances. Therefore, in line 050, write down only those advances for which personal income tax was actually reduced.

Even if the company did not withhold anything from the foreigner, reflect the salary in section 2. In line 130, show the accrued income, and in line 140 put zero.

For example

The company employs two foreigners with a patent. Every month they pay advances for the patent - 4,200 rubles. The salary of the first employee is 30,000 rubles. per month, personal income tax - 3900 rubles. (30,000 rubles × 13%), second - 32,000 rubles, personal income tax - 4160 rubles. (RUB 32,000 × 13%). Salary taxes are less than monthly advances, so the company does not withhold personal income tax.

Section 1.

During the six months, the company accrued income of 372,000 rubles. ((RUB 30,000 + RUB 32,000) × 6 months). Calculated personal income tax - 48,360 rubles. (RUB 372,000 × 13%). Advances for a patent for 6 months amounted to 50,400 rubles. (RUB 4,200 × 2 × 6 months). In line 050, the company recorded advances within the calculated tax - 48,360 rubles.

Section 2.

The company issued salaries for April on May 4 - 62,000 rubles. (30,000 + 32,000). Calculated personal income tax - 8060 rubles. (3900 + 4160). The company did not withhold tax. She filled out the calculation as in sample 95.

Sample 95. How to fill in the income of foreigners on a patent:

Top

Line 080

Let us recall the income that an individual received during the tax period in the form of a gift or other financial assistance. They are not subject to taxation when their amount is up to 4,000 rubles. When the value of gifts or material assistance is greater, the tax is taken from any income (not exceeding 50% of its amount).

All dates specified in Section 2 6-NDFL

must strictly comply with legal requirements and be checked by an accountant to avoid inconsistencies.

If you find an error, please select a piece of text and press Ctrl+Enter

.

It must be submitted to the regulatory authorities at the place of registration of the individual entrepreneur or organization.

This applies to both employers applying employment contracts and enterprises cooperating with individuals under any contracts (for example, of a civil nature or rental of premises), where the legal entity is obliged to withhold tax and pay it to the budget.

The peculiarity of this report is that it is formed on an accrual basis, and is also compiled for each separate division separately.

The foreigner became a resident in the second quarter

The company withheld personal income tax from the foreigner at a rate of 30 percent. He became a resident in the second quarter.

The income of non-residents is subject to personal income tax at a rate of 30 percent (clause 3 of article 224 of the Tax Code of the Russian Federation). But if an employee has spent 183 calendar days in Russia over the past 12 months, he will become a resident. Tax for the month in which the employee became a resident will need to be calculated at a rate of 13 percent. The company determines the employee’s status at the end of each month (letter of the Federal Tax Service of Russia dated October 22, 2014 No. OA-3-17/ [email protected] ).

Semi-annual calculation.

Do not recalculate the tax for previous months, because the employee can still become a non-resident. In section 1, show the employee’s income in two blocks of lines 010–050 - at a rate of 30 and 13 percent.

Calculation for nine months and for a year.

The company determines the final status of the employee based on the results of the year. At the same time, if during the year an employee stays in the Russian Federation for 183 calendar days, then his status will not change until the end of the year. This will happen in July. This means that this month you can recalculate personal income tax on all income from January to June (letter of the Ministry of Finance of Russia dated February 15, 2016 No. 03-04-06/7958).

Thus, all employee income will be taxed at a rate of 13 percent. When calculating for nine months and for a year, do not divide payments at different rates. In line 040, reflect the tax calculated at a rate of 13 percent. And in line 070 - personal income tax, which was actually withheld from the employee. The company does not have the right, after recalculation, to return money to the employee upon application. Show the overpayment in the 2-NDFL certificate as excessively withheld.

For example

The foreigner arrived in Russia on December 15. The following June he became a resident. The company calculated personal income tax on wages for this month at a rate of 13 percent. On income for January - May - at a rate of 30 percent. Salary for January - May - 450,000 rubles, calculated and withheld personal income tax - 135,000 rubles. (RUB 450,000 × 30%). Salary for June - 50,000 rubles, calculated and withheld personal income tax - 6,500 rubles. (RUB 50,000 × 13%). There are no other employees in the company. Total income - 500,000 rubles. (450,000 + 50,000). Personal income tax - 141,500 rubles. (135,000 + 6500). She filled out section 1 as in sample 96.

Sample 96. How to fill out the half-year calculation if the employee has become a resident:

Top

Features of vacation pay regarding personal income tax

Vacation pay, as well as sick leave, must be reflected in the 6-NDFL report along with the income of individuals subject to taxation. In accordance with Article 136 of the Labor Code of the Russian Federation, wages are paid in two stages (advance and main part), while vacation pay and sick leave are accrued as follows:

- vacation pay: when taking a vacation, no later than 3 calendar days before it begins (Article 136 of the Labor Code of the Russian Federation);

- Sick leave: within 10 calendar days after the employee provides a sick leave certificate or other relevant document. Sick leave is accrued in conjunction with the next salary, in accordance with paragraph 1 of Article 15 of the Law “On Compulsory Social Insurance in Case of Temporary Disability and in Connection with Maternity” dated December 29, 2006 No. 255-FZ.

Despite the differences in accrual periods, the rules for determining both vacation and sick leave are common:

- The date on which income is recognized as received for the purpose of calculating personal income tax must correspond to the date of payment of income (subparagraph 1, paragraph 1, Article 223 of the Tax Code of the Russian Federation).

- The deadline for payment of personal income tax should be the last date of the month in which payments were made (clause 6 of Article 226 of the Tax Code of the Russian Federation).

From the point of view of the deadline, vacation pay differs from other income of individuals, personal income tax on which must be paid no later than the day following the payment (clause 6 of Article 226 of the Tax Code of the Russian Federation). That is why vacation pay is reflected separately in the 6-NDFL reporting form.

The company provides deductions to the foreigner and reduces personal income tax on advances

The company employs a foreigner with a patent. He is a resident of the Russian Federation. The company provides him with a child deduction and reduces his calculated personal income tax by advances for the patent.

Foreigners with a patent have the right to receive a child deduction as soon as they become residents of Russia. To receive deductions, a foreigner must write an application and bring birth certificates of children. If the documents are in a foreign language, they must be translated and the translation certified by a notary.

The company has the right to provide a deduction to a foreigner and at the same time reduce the calculated personal income tax for advances for a patent. The Code does not prohibit this. First, reduce the foreigner’s income by deductions and calculate personal income tax. This amount can be reduced by advances.

In line 020, write down the accrued salary. Reflect the deductions that were provided to the employee in line 030 of section 1. And the advances for which the calculated personal income tax was reduced are reflected in line 050. In line 070 reflect the personal income tax that was withheld from the employee.

As for section 2, reflect the operation in it, even if the advances exceeded the calculated personal income tax. On line 130, record accrued income. And in line 140 - withheld personal income tax. If the company did not withhold anything, enter a zero on this line.

For example

The company employs a foreigner with a patent. Pays a monthly advance of 4,200 rubles. The employee's salary is 50,000 rubles. He has one child, so the company provides a deduction of 1,400 rubles. The company issued salaries for April on May 5. Calculated personal income tax - 6318 rubles. ((RUB 50,000 - RUB 1,400) × 13%). And I withheld tax minus the advance payment - 2118 rubles. (6318 - 4200). The company filled out Section 2 as in sample 97.

Sample 97. How to reflect salary if the company reduced income by deductions:

Top

Dates, deadlines and amounts

6-NDFL is a new reporting form for employers. It contains summarized information regarding:

- all people who received profit from the tax agent;

- all amounts of accruals and payments of income to them;

- deductions provided;

- income tax that has been calculated and withheld.

The bulk of the time is spent filling out Section 2 of form 6-NDFL

. It displays:

- the day the profit was actually received by the individual/persons;

- tax withholding time;

- the period within which the tax was transferred;

- the actual amount of profit received by a person;

- amount of tax withheld.

Information in Section 2 of form 6-NDFL

presented in a generalized form. In particular, this means that if the time of receipt of actual profit by different individuals coincides, the output data on the amounts of tax and income will ultimately be brought together.

Features of filling out the 6-NDFL declaration

A declaration, or report in form 6-NDFL, is a summary table that provides data on the income of the company’s employees, including vacation pay and sick leave payments, in a separate (for each employee separately) or general (total) form. Form 6-NDFL is unified, is not subject to change and currently, according to general practice, is filled out electronically.

Important: although at the legislative level there is no prohibition on drawing up a report by hand (the tax office must accept and process it), it is more advisable to enter the data into the form on a computer in order to include vacation pay or reflect sick leave in 6-NDFL. This will speed up processing and allow the accountant to correct incorrectly entered data on the fly, without reprinting the form each time

The declaration in Form 6-NDFL is sent to the Federal Tax Service four times a year on the last day of each quarter:

- first - March 31;

- second - June 30;

- third - September 30;

- fourth - December 31st.

Important: if the specified dates fall on weekends or holidays (and from December 31 this always happens), the deadline for filing the 6-NDFL report becomes the first working day after the end of the quarter. For example, if the date June 30 fell on a Saturday, the declaration should be sent to the Federal Tax Service no later than July 2, that is, the following Monday

For the fourth quarter, the deadline for filing 6-NDFL is the first day after the end of the New Year holidays.

Declaration 6-NDFL consists of two pages and three main sections:

- The first page contains the organization's data: full name, taxpayer identification number and checkpoint, OKTMO code, telephone number, information about the tax agent and his representative. On the same page, the tax inspector confirms that he has read the document and that it is correctly prepared.

- On the second page (in the first section), generalized indicators are indicated in numbered lines: the personal income tax rate, the total income of employees for the reporting quarter, accrued and withheld personal income tax and the number of employees for whom the report is being filled out. In the second section (in duplicate lines 100, 110, 120, 130 and 140), the accountant must reflect:

- in position number 100 - the calendar date (in the accepted format) the employee received income (vacation pay, sick leave payments, and so on);

- in position number 110 - the calendar date (in the accepted format) withholding personal income tax from each specific amount;

- in position number 120 - the calendar date (in the accepted format) of the transfer of the withheld tax to the Federal Tax Service;

- in position number 130 - the size of each income appearing in the second section;

- in position number 140 - the amount of tax withheld in relation to the income indicated above.

At the end of Form 6-NDFL, the signature of the originator with a transcript and the date of execution of the document are given. Since the declaration is filled out and sent to the tax office electronically, there is no need to affix the organization’s seal or stamp on it. A qualified digital signature is also not needed: in this case, the Federal Tax Service only needs the accountant’s signature and the company’s contact information.

Like the formula for calculating vacation pay, the procedure and timing for their reflection in the 6-NDFL declaration are clearly defined and cannot be changed at the request of the employer or accounting department specialists.

In accordance with paragraph 1 (subparagraph 1) of Article 223, paragraphs 4 and 6 of Article 226 of the Tax Code of the Russian Federation and the provisions of other documents, the following rules apply in relation to the deadlines for receiving vacation pay and withholding personal income tax:

- the date of receipt of income is the day the payment is transferred to the employee, regardless of the method used (on a plastic card, current account, at the cash desk);

- the date of personal income tax withholding coincides with the date the employee receives income (currently, tax is deducted from the amount automatically, without the participation of the employee);

- the date before which personal income tax must be transferred is the last day of the month of payment, although nothing prevents the employer from transferring money to the Federal Tax Service directly on the day of deduction.

Important: as in the previous example, if the last day of the calendar month in which the payment was made is a weekend or holiday, the due date is postponed to the next working day. For example, if an employee received vacation pay on April 15, April 30 is a Sunday, and May 1 and 2 are days off, a declaration in Form 6-NDFL should be submitted before May 3

In some cases, if the state is small, it makes sense to transfer funds to the tax office earlier, for example on the 16th or 17th.

Filling procedure and example

The personal income tax calculation form consists of 2 sections, which contain generalized data on accruals and deductions made, as well as specific data on tax transfers.

Example of filling out a declaration:

Important details:

- Section 1 contains cumulative data.

- Section 2 is completed based on data from the last three months of the reporting period.

- If there is a difference in tax withholding days, additional lines are filled in.

- A new report page is completed for each tax rate.

Corrections to the document are not allowed. In case of a calculation error or incorrect information about the company's details, corrected reporting is provided in the same way as other forms.

The correction number is indicated on the first page in the corresponding column. No resetting or cancellation reports required!