Agency agreement - legal basis, structure

The rules for concluding an agency agreement and the procedure for its application in practice are regulated by the provisions of Chapter 52 of the Civil Code of the Russian Federation.

According to the provisions of Art. 1005 of the Civil Code, an agency agreement is an agreement in which one party (the agent), on behalf of the second party (the principal), undertakes to perform certain actions in its interests. In this case, actions can be performed on behalf of both the agent and the principal, but in any case the second finances them. Thus, within the meaning of Art. 1005 of the Civil Code of the Russian Federation in an agency agreement, the principal is a party, in order to satisfy whose interests the other party undertakes to perform the actions specified in the agreement. An agency agreement may have the following structure:

- Introductory part, which includes:

- name of the document and date of its preparation;

- Full name or official name of the persons entering into the agreement.

- The main part, which indicates:

- subject of the contract;

- rights and obligations of the parties to the contract;

- deadlines for fulfilling the terms of the agreement;

- deadlines for submitting reports on the results of work performed;

- the procedure for making payments between the parties (this is a paid agreement, you can read about the procedure for paying remuneration here);

- settlement of disputes;

- confidentiality terms;

- other conditions that may be important when concluding a contract of a certain type.

- The final part, which contains:

- an indication of the possibility of applying legal norms when resolving issues not regulated by the agreement;

- the number of drawn up copies of the contract that have legal force;

- details and signatures of the parties entering into the agreement.

Why should an agency agreement contain a remuneration clause?

Under the agency agreement, the principal is obliged to pay the agent remuneration (paragraph 1 of article 1006 of the Civil Code of the Russian Federation). In other words, the agency agreement is for a fee. This is an imperative rule: the parties cannot formulate a condition on the gratuitous nature of the contract. Thus, in one of its rulings, the Supreme Arbitration Court of the Russian Federation indicated that Article 1006 of the Civil Code of the Russian Federation does not provide for cases when agency fees are not paid (determination of the Supreme Arbitration Court of the Russian Federation dated October 13, 2008 No. 13250/08).

The lawyer of the organization acting as an agent must ensure that the agreement contains a condition on the amount of remuneration and a condition on the procedure for paying the remuneration. Only in this case will the agent’s interests be best protected.

If the contract does not contain such conditions, then this may lead to one of the following negative consequences.

1. The agency agreement will be considered concluded, but it will be difficult for the agent to receive remuneration.

Firstly, the agent will be able to claim it only after he submits to the principal a report on the actions performed (paragraph 3 of Article 1006 of the Civil Code of the Russian Federation). The principal is obliged to pay the award within a week from the receipt of such a report.

Secondly, the amount of remuneration will be calculated according to the rules of paragraph 3 of Article 424 of the Civil Code of the Russian Federation (paragraph 2 of Article 1006 of the Civil Code of the Russian Federation). This means that the agent will be able to receive the amount that, under comparable circumstances, would normally be charged for similar services. In the event of a dispute, the obligation to prove the amount of remuneration will lie with the mediator as an interested party (clause 54 of the resolution of July 1, 1996 of the Plenum of the Supreme Court of the Russian Federation No. 6, Plenum of the Supreme Arbitration Court of the Russian Federation No. 8 “On some issues related to the application of part one of the Civil Code of the Russian Federation"). As a result, the amount of the award may be significantly less than what the agent expected when concluding the contract. Thus, if the agency agreement does not include a remuneration clause, then the procedure for calculating and collecting funds will be difficult for the intermediary.

2. The agency agreement will be considered not concluded. This negative consequence will occur only if the condition of remuneration is an essential condition of the contract (clause 1 of Article 432 of the Civil Code of the Russian Federation, clause 1 of the information letter of the Presidium of the Supreme Arbitration Court of the Russian Federation dated February 25, 2014 No. 165 “Review of judicial practice on disputes related to the recognition of contracts as not concluded”; hereinafter referred to as information letter No. 165).

An essential condition regarding the award is, for example, when a lawyer acts as an agent. According to the law, the condition of remuneration is an essential condition of the agreement on the provision of legal assistance (subparagraph 3, paragraph 4, article 25 of the Federal Law of May 31, 2002 No. 63-FZ “On advocacy and advocacy in the Russian Federation”). An agreement with a lawyer can be concluded in the form of an agency agreement using the model of a mandate agreement. Consequently, in such a situation, the court may consider the remuneration clause an essential condition of the agency agreement.

In addition, the remuneration condition is significant if, during negotiations, one of the parties to the contract proposed the wording of this condition or stated the need to agree on a reward. In such a situation, the contract will not be considered concluded until the parties agree on the remuneration condition or the party that proposed this condition or announced the agreement of the reward refuses its proposal (clause 11 of information letter No. 165).

Parties to the agency agreement

Based on the above definition of an agency agreement, we can conclude that its parties are:

- An agent is a executor of the terms of the transaction, acting in the interests of the customer.

- The principal is the orderer of certain actions that the performing agent must perform.

Responsibility for the results obtained as a result of the agent’s execution of the principal’s instructions rests with the latter, since it is he who will have the status of their owner. If it turns out that the agent did not have sufficient experience or knowledge to solve the task assigned to him or deliberately abused the powers granted to him, the principal may file a claim in court to recover material damages or other types of compensation.

Who can be a party to an agency agreement?

The legislator does not establish certain requirements for the status of persons who are parties to agency agreements, and does not limit the rights of individual entrepreneurs and individuals (how to conclude an agency agreement with an individual, you can read here) who are not registered as the owner of their own business, to conclude agency agreements. That is why an agent can be either an organization or an individual who does not have the status of an entrepreneur and is not an employee of the principal.

According to the provisions of paragraph 1 of Art. 226 of the Tax Code of the Russian Federation, in the latter case, the principal who has entered into an agency agreement with such a person is recognized as his tax agent. On this basis, he acquires the obligation to withhold personal income tax from the funds earned (clauses 4 and 6 of Article 226 of the Tax Code of the Russian Federation).

You can find more complete information on the topic in ConsultantPlus. Free trial access to the system for 2 days.

The principal in an agency agreement can also be a legal entity or an individual. Legal practice that has developed in the field of contractual relations shows that in both cases it is possible to interact with both companies and citizens registered as individual entrepreneurs.

Let's look at how settlements with an agent are made.

At this step, the agent’s services are posted and payment is made.

The agency agreement belongs to the category of paid contracts. Therefore, for actions performed under an agency agreement, the agent must receive remuneration from the principal, the amount and procedure for payment of which must also be stipulated by the agreement between them.

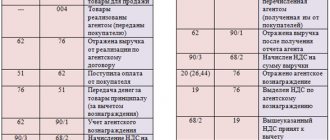

The agent issues an invoice to the principal for the amount of his remuneration, files such a document in the journal of issued invoices and registers it in the sales book. The agent must give the second copy of the invoice to the principal.

Posting agent services:

•Let's go to the journal of the movement of values and. Let's select one or more invoices with the operation type “Principal. Report from the agent (on behalf of the agent)”, for which it is necessary to capitalize the agent’s service.

•Select the context menu item “Generate reward”.

•In the request window that appears, enter the remuneration expense account. Click <OK>.

•In the header of the invoice that appears we will indicate the number and date of the invoice. The agent's account and VAT accounting type will be entered automatically. In the invoice details, the agent service will be automatically added with the calculated quantity, price including VAT, amount including VAT and VAT amount. Click <OK>. In the journal “Movement of Values and Services” the operation “Capitalization” will be added.

•A capitalization transaction will appear in the journal of accounting transactions, with the following entries: 44/USL/01588 – 76/PROCH/Agent = Amount of agency fee excluding VAT 19/USL – 76/PROCH/Agent = Amount of VAT of agency fee 68/VAT – 19/USL = VAT amount of agent remuneration

•An invoice from the agent will be automatically added to the journal of posted invoices.

| Attention! From January 1, 2015, the obligation to keep accounting logs remained only for agents (commission agents) who issue or receive invoices when carrying out activities in the interests of another person on their own behalf. Therefore, in this case, invoices made after 01/01/2015 do not appear in the journal of recorded invoices. |

Payment from the agent.

Advance from agent

A situation is possible when the agent first receives an advance payment from the buyer, and then uses this advance to ship the goods.

Based on the invoice issued by the agent to the buyer upon receipt of an advance from him, the principal “re-issues” an invoice with similar indicators to the agent in the name of the buyer. The principal registers the “overissued” invoice in the sales book without recording the issued invoices in the journal.

To register an invoice for an advance payment from a buyer (received from an agent), do the following:

•Let's go to the journal of payment documents in the main menu “Operations | Payment documents" (or "Operations | Incoming bank"). Let’s add a payment document with the transaction type “Receipt from commission agent, agent”, indicate the payer’s account (this is the buyer’s account), the agent’s account, indicate the amount that the agent returns, as well as the number of the invoice for the advance and the date of the invoice for the advance. The remaining parameters will be entered automatically. Click <OK>;

•A payment document for the advance received from the agent will appear in the payment document journal.

•In the journal of accounting transactions, the operation of receiving an advance payment to the account from an agent will appear, with transactions: 51/0784 – 62/AB/Agent = Advance amount 76/VAT/Agent – 68/VAT = Advance VAT amount

•In the form of the sales book, a record will appear about the advance received with the note “Advance received” indicating information about the intermediary (commission agent, agent) (with transaction type code 05). This invoice is not recorded in the journal of issued invoices;

•Let’s go to the journal of the movement of values and services in the main menu “Operations | Movement of values and services." Let's open the operation “Principal. Report from the agent (on behalf of the agent).” On the “Payments” tab, add this payment document for the advance as payment; the “This is an advance” checkbox should be selected automatically. Click <OK>.

•In the journal of the accounting transactions of the transaction, an entry will be added to offset the amount of the advance from the buyer, listed by the agent: 62/AB/Agent – 62/REAL/Agent = Amount of the specified advance (not a payment document, namely indicated on the advance tab) 68/VAT – 76 /VAT/AGENT = VAT amount of the specified advance

•In the form of the purchase book, a record will appear about the reversal of a previously received advance from the buyer, listed by the agent with the note “Advance credited” (with transaction type code 22). Please note that there will be no “advance invoice” in the “Capitalized invoices” journal; an entry in the sales book appears automatically on the “advance invoice” and “sales invoice”. This invoice is not recorded in the journal of posted invoices;

This action is performed both for the case when the agent acts on his own behalf, and for the case when the agent acts on behalf of the principal.

| Comment! In the case of a partial advance, it is necessary to post the payment document, indicating it on the “Payments” tab in the previously entered transaction “Principal. Report from the agent (on behalf of the agent).” In this case, you need to uncheck the “This is an advance payment” checkbox (the program turns it on automatically). |

Agent fee payment:

| Comment! When an agent takes his remuneration from the amount of goods sold, then the action “Payment of remuneration to the agent” is not performed, and payment from the agent is formalized by the operation “Receipt from commission agent, agent” (if there is no such operation, enable it in the menu “Service | Operation settings | Types payment documents"), where the amount of goods sold is indicated as the amount, and the amount of the commission is indicated in the “Remuneration” column. |

•Let's go to the journal of the movement of values and. Let's select the invoice with the type of transaction "Capitalization" that needs to be paid.

•Select the “Pay” context menu item.

•The payment document that appears will automatically indicate the recipient's (commission agent's) account, the recipient's current account, the amount, the VAT rate, and the VAT amount. Click <OK>.

•A payment transaction will appear in the journal of accounting transactions, with the following entries: 60/POST/Agent – 51/Current account = Amount of agency fee including VAT

If in an agency agreement the principal is an individual

An example of an agency agreement in which an individual acts as a principal is:

- an agreement concluded between a tourist and a travel agency - a company that sells the product offered by tour operators (principal - an individual, agent - a legal entity);

- an agreement concluded between the buyer of an apartment and a realtor who provides services for selecting housing according to specified criteria and performs subsequent support of the purchase and sale transaction (principal - an individual, agent - an individual with the status of an individual entrepreneur).

The advantages of concluding this type of agreement for an individual as a principal is the opportunity to save effort and time on solving any problem. After all, agents have the necessary knowledge and skills that allow them to use resources as efficiently as possible to fulfill the terms of the contract.

The disadvantages of involving an intermediary in solving a certain type of problem are:

- The risk of obtaining a result that does not meet the stated requirements.

- The need to monitor the agent’s progress in fulfilling his duties.

Taxation of income received by the principal - an individual

In some cases, the principal, who has the status of an individual, may receive a certain amount of funds based on the results of the agent’s fulfillment of his obligations. An example of such a situation would be the conclusion of an agreement between a real estate agency and the owner of an apartment to rent it out. The income received by the owner of the property from the rental of such housing is subject to income tax, the amount of which is 13% of the amount of money paid by the tenant. In this case, the question arises: should the agent withhold this tax from the principal?

The person from whom the landlord receives funds is the tenant of the residential premises. Based on the provisions of sub. 1 clause 1 art. 228 of the Tax Code of the Russian Federation, the obligation to calculate and pay tax on income received from an organization or individual who is not a tax agent is assigned to the person who received such income.

A real estate agency, acting as an intermediary between the landlord and the tenant, is not a source of income, does not have the status of a tax agent and, as a result, does not assume obligations for the calculation and payment of tax. The remuneration received by the agent from the principal for the performance of the duties assigned to him is taxed in accordance with the tax system chosen by him.

Subscribe to our newsletter

Yandex.Zen VKontakte Telegram

Rights of the principal under an agency agreement

Civil legislation establishes a list of rights and obligations of the principal, the scope of which depends on the type of agreement being concluded and the conditions it contains.

Based on current legislative norms, when executing an agency agreement, the principal has the right to:

- Instruct the agent to perform legal and other actions (actual) to the extent established by the provisions of the agreement (Article 1005 of the Civil Code of the Russian Federation).

- Require the agent to submit a report on the work he has performed (clause 1 of Article 1008 of the Civil Code of the Russian Federation).

- Require the agent to provide documentary evidence of the fact of spending the funds withheld by him from the principal, unless otherwise established by the provisions of the concluded agreement (Clause 2 of Article 1008 of the Civil Code of the Russian Federation).

- Submit to the agent objections to the report drawn up by him within 30 days from the date of receipt of such a report, unless the provisions of the concluded agreement provide for other deadlines for the submission of objections (failure to submit such objections entails the recognition of the report as accepted, in accordance with clause 3 of Article 1008 of the Civil Code of the Russian Federation).

- Refuse to execute the contract, provided that its provisions do not establish the exact period of its validity (Article 1010 of the Civil Code of the Russian Federation).

In addition, Art. 1007 of the Civil Code of the Russian Federation indicates that the concluded agreement may limit the rights and obligations of its parties. In particular, the principal has the right to prohibit the agent from interacting with other principals in the agency agreement - this follows from the provisions of paragraph 2 of this article.

Agency contract. Advance payment from the Agent to the Principal.

AGENCY AGREEMENT No.

LLC, represented by the General Director acting on the basis of the Charter, hereinafter referred to as the “Principal”, on the one hand, and LLC, represented by the director acting on the basis of the Charter, hereinafter referred to as the “Agent”, on the other hand, have entered into this Agreement on the following :

1. THE SUBJECT OF THE AGREEMENT

1.1. The Agent undertakes, for a fee, to carry out, on behalf of the Principal, legal and other actions on behalf of the Principal and at his own expense in the territory of the region.

1.2. Under a transaction made by the Agent with a third party on behalf of the Principal, the rights and obligations arise with the Principal.

2. OBLIGATIONS OF THE PARTIES

In order to fulfill this agreement, the Agent has the right to enter into subagency agreements with third parties.

2.1. The Agent undertakes:

2.1.1. Conclude, on behalf of the Principal, contracts with subscribers (users) for the provision of communication services by the Principal;

2.1.2. Register all subscribers when providing access to the Principal’s network and issue them subscriber numbers (network details) to access services on behalf of the Principal;

2.1.3. During the Billing Period, issue (generate and provide) invoices on behalf of the Principal for the Communication Services provided to subscribers (users). Invoices for rendered Communication Services must be issued to subscribers (users) before the 10th day of the Billing Period, indicating the total amount of payment, as well as indicating the date of provision of each type of Communication Services, its volume and the cost of each type of service, as well as indicating that that the subscriber (user) is obliged to pay for communication services within 20 days from the date of invoice. The basis for issuing invoices to subscribers (users) is the readings of the Principal’s communication equipment. Invoices for communication services provided to subscribers (users) must be issued at the Tariffs established by the Principal.

2.1.4. Generate and carry out actions for the delivery of invoices and certificates of completed work to subscribers (users).

2.1.5. Receive funds from subscribers (users) into your current account, sent to pay for the Services provided by the Principal.

2.1.6. To collect debts from subscribers (users) arising in connection with non-payment for services provided.

2.1.7. Provide information and reference services to subscribers (users).

2.1.8. Generate and provide the Principal with documents for the purposes of accounting, tax and statistical accounting provided for in this Agreement.

2.1.9. Ensure the storage of primary documents, namely invoices, cash receipts and receipts, in accordance with current legislation.

2.1.10.Officially communicate information on Services and Tariffs to subscribers (users) in accordance with current legislation.

2.1.11. Provide the Principal with a report every month no later than the 5th day of the month following the settlement month, as well as at any time upon the Principal’s request. The agent's report must be accompanied by the necessary evidence of expenses incurred by the Agent at the expense of the Principal.

2.1.12. Carry out installation and installation of the necessary equipment for individuals and legal entities to provide the Principal’s services, including from their own funds;

2.1.13. Provide technical support to subscribers, carry out troubleshooting work in the Principal’s network, perform warranty and maintenance maintenance of network and switching equipment, including from own funds;

2.1.14. Conduct organizational and propaganda work to attract new subscribers and users of the Principal’s services;

2.1.15. Follow the Principal’s instructions regarding transactions and other actions performed by the Agent, if these instructions do not contradict the requirements of the legislation of the Russian Federation.

2.2. The principal undertakes:

2.2.1. Pay the Agent a fee. Payment is made by the Agent deducting the amount of agency fees due from the collected funds. The amount of remuneration is confirmed by a report for the corresponding period or a report on the fulfillment of obligations for individual transactions completed by the Agent;

2.2.2. If necessary, provide the Agent with advertising materials and technologies for their effective distribution;

2.2.4. If necessary, provide the Agent with the necessary equipment and materials to perform its troubleshooting duties.

2.2.5. Provide assistance to the Agent in carrying out the instructions of the Principal.

3. SIZE OF REMUNERATION AND PROCEDURE FOR ITS PAYMENT

3.1. The amount of remuneration is determined in an amount equal to at least 90% of the amounts received by the Agent for payment for the Principal’s services.

3.2. The Agent monthly transfers to the Principal the amount of income received from subscribers for the reporting month, minus the agreed remuneration.

4. RESPONSIBILITY OF THE PARTIES

4.1. For failure to fulfill or improper fulfillment of obligations under this Agreement, the parties are liable in accordance with current legislation.

4.2. Neither party to this Agreement is liable to the other party for failure to fulfill obligations caused by circumstances arising as a result of force majeure.

4.3. A party that fails to fulfill its obligation due to force majeure must immediately notify the other party of the obstacle and its impact on the fulfillment of obligations under the Agreement.

5. DISPUTE RESOLUTION PROCEDURE

5.1. All disputes and disagreements between the parties arising during the period of validity of this Agreement are resolved by the parties through negotiations.

5.2. If disputes and disagreements are not resolved through negotiations, the dispute shall be resolved in accordance with the legislation of the Russian Federation.

5.3. Provisions not regulated by this Agreement are governed by the provisions of the current legislation of the Russian Federation.

6. TERM OF THE AGREEMENT

6.1. This Agreement comes into force on May 1, 2009 and is valid until December 31, 2009.

6.2. The term of the Agreement is automatically extended for another year if neither party notifies the other party in writing one month before the expiration of the Agreement of its intention to terminate the Agreement.

6.3. The Principal and Agent have the right to terminate the Agreement early with written notice to the other party no less than 10 days before the date of termination of the Agreement.

7. ADDRESSES AND DETAILS OF THE PARTIES

8. SIGNATURES OF THE PARTIES.

Obligations of the principal (general provisions)

In addition to the rights listed above, the principal is assigned certain responsibilities that he bears in the course of fulfilling the terms of the current agreement.

To them, in accordance with the provisions of Art. 1006 of the Civil Code of the Russian Federation, include:

- payment to the agent of remuneration in the amount fixed by the provisions of the document (if the amount of payment is not established by the agreement, it is determined based on the average market value);

- compliance with the deadlines for payment of remuneration, if established by the provisions of the contract. Otherwise, you will have to pay the agent no later than a week after he submits a report on the results of activities for the past working period.

In addition, the principal, in accordance with the provisions of Art. 1007 of the Civil Code of the Russian Federation, may acquire additional obligations, if any are provided for by the concluded agreement. Thus, the provisions of the document may oblige him:

- do not enter into similar agreements with other agents in the territory specified by the agreement;

- refrain from independently performing actions constituting the subject of the contract in this territory.

Reporting under an agency agreement

The principal has the right to control the activities of the agent based on the reports he provides. All reports must be provided within the deadlines specified in the contract. If the parties have not included such clauses in the contract specifying the procedure and form of reporting, reports are provided as the contract is fulfilled or upon its completion. (Article 1008 of the Civil Code of the Russian Federation).

The report provided must contain a list of actions performed by the agent in pursuance of the contract, as well as a list of expenses incurred.

Since, according to paragraph 1 of Art. 1005, all actions must be performed by the agent at the expense of the principal, the latter is obliged to pay all expenses incurred by the agent in executing the contract. To avoid legal disputes, lawyers recommend that the parties provide in the contract a special procedure for reimbursement of expenses incurred. If such a procedure was not provided for by the contract, the general rule established by the legislator comes into force: the agent undertakes to provide documents confirming the fact and amount of expenses (checks, invoices, receipts, etc.) incurred during the execution of the contract.

To accept the agent’s report, the principal is given a certain period of time, during which he has the opportunity to study the report provided by the agent and, if he disagrees with his actions, raise any objections that arise. The deadline for acceptance of the report is established by agreement of the parties. In the event that the parties have not agreed on this condition in the contract, the thirty-day period established by law applies. After the expiration of the allotted period, the report is considered accepted, and the agent has the right to count on remuneration and reimbursement of expenses incurred by him (clause 3 of Article 1008 of the Civil Code of the Russian Federation).

Obligations of the principal as a party to the agency agreement

In the event that the actions performed by the agent entail the emergence of rights and obligations not for him, but for the principal, their relationship is regulated by the provisions of Chapter. 49 of the Civil Code of the Russian Federation, which defines the rules for applying the agency agreement (Article 1011 of the Civil Code of the Russian Federation).

According to the provisions of Art. 975 of the Civil Code of the Russian Federation, the principal (aka the principal) is obliged (unless otherwise established by the provisions of the concluded agreement):

- Reimburse the costs incurred by the contractor in the course of performing the task assigned to him.

- Provide the contractor with the means necessary to complete the task.

- Accept the result of the work performed by the performer.