Procedure for submitting a VAT return

You need to submit your VAT return to the Federal Tax Service at the location of the tax agent.

Important! The declaration is submitted electronically through specialized operators. Moreover, all tax agents submit returns electronically, regardless of the number of employees.

An exception to this requirement are tax agents who are not VAT payers, including those who do not conduct intermediary activities in issuing invoices on their own behalf.

The Federal Tax Service has expanded the list of tax agents

From January 1, 2021, three categories of new tax agents appeared. Let's figure out who this concerns, how to pay tax and what to indicate in the declaration.

| Tax agent from 01/01/2020 | How to pay tax | What to include in the declaration |

| Owners of watercraft and civil aircraft who have not registered their transport in state registers within 90 days (clause 6 of Article 161 of the Tax Code of the Russian Federation) | The owner must pay 20% VAT on the cost of the vessel | For each vessel separately, you need to fill out section 2 of the VAT declaration. In line 070, select transaction code 1011718 or 1011709 - depending on the type of vessel |

| Tenants and lessees of civil aircraft who have not registered their transport in state registers within 90 days (clause 6.1 of Article 161 of the Tax Code of the Russian Federation) | The tax agent pays VAT on the cost of services under a rental (leasing) agreement | For each vessel, you must fill out a separate section 2 of the VAT declaration and select transaction code 1011716 in line 070 |

| Owners of vessels excluded from the State Register of Civil Aircraft of the Russian Federation (Clause 6.2 of Article 161 of the Tax Code of the Russian Federation) | VAT is paid on the cost of the vessel | For each vessel separately, you need to fill out section 2 of the VAT declaration and select transaction code 1011717 in line 070 |

To enter data in section 2, go to the line with the transaction code. Immediately enter the code or click on the three dots to open a directory with codes:

You can find the required code in the directory by number or keyword from the code description:

How to fill out a VAT return for a tax agent

In the case when the organization was only a tax agent during the tax period, then in addition to the title page, only the second section of the declaration needs to be filled out. And in the first one, dashes are simply added.

When a tax agent also carries out transactions subject to VAT, the second section must be included. If, in addition to all of the above, the organization carries out transactions exempt from VAT, then the seventh section is also included in the declaration.

Important! It should be borne in mind that the first section is filled in as the last section in the declaration, after all other data (except for the second section) has been filled out.

The VAT calculated as for the taxpayer cannot be summed up with the VAT of the tax agent. They are reflected on different lines - 040 and 050 of the first section (

Payment of VAT by a tax agent

The list of duties of a tax agent for VAT is established by the Tax Code of the Russian Federation (clause 3 of Article 24 of the Tax Code of the Russian Federation).

The main responsibility of agents is to calculate, withhold and transfer tax to the budget (subclause 1, clause 3, article 24 of the Tax Code of the Russian Federation). To implement its main function, the VAT tax agent must withhold tax from the taxpayer’s funds at his disposal.

IMPORTANT! There is no need to pay tax for persons who are not recognized as VAT payers. Thus, tax is not paid when purchasing goods (work, services) from a foreign person who is not an entrepreneur (letter of the Ministry of Finance of Russia dated March 5, 2010 No. 03-07-08/62), as well as when selling seized property of an individual (letter of the Ministry of Finance of Russia dated November 18, 2010 No. 03-07-14/81).

If no payments were made to the taxpayer in a given tax period, tax withholding is impossible. In such a situation, instead of withholding VAT, the tax agent is obliged to provide information about the impossibility of withholding tax amounts on payments of the taxpayer, indicating the amount of debt for unfulfilled obligations to the budget (subclause 2, clause 3, article 24 of the Tax Code of the Russian Federation, clause 1 of the resolution of the Plenum of the Supreme Arbitration Court of the Russian Federation dated 30.07 .2013 No. 57). This information is provided within a month from the date of discovery of the impossibility of withholding VAT.

Filling out the Declaration Cover Page

The TIN and KPP of the organization are filled out on the title page. The data can be found in the registration certificate received upon registration. You need to fill out the TIN from the first cell, if the organization's TIN has only 10 digits, the last two cells do not need to be filled in, dashes are placed in them.

The “adjustment number” depends on what kind of declaration the organization submits: primary or updated. When submitting an initial declaration, you need to enter “0–”, and when submitting an updated declaration, indicate the adjustment number, that is, “1–” for the first clarification and “2–” for the second.

The “tax period” is set depending on the quarter for which the declaration is submitted, that is, 21 – the first quarter, 22 – the second quarter, 23 – the third quarter, 24 – the fourth quarter.

“Reporting year” – enter the year of the quarter for which the declaration is submitted. For the 3rd quarter of 2021 – “Reporting year” should be entered as 2021.

“Submitted to the tax authority” - enter the code of the Federal Tax Service that registered the tax agent. This code can be found in the same certificate as the TIN, or at the address of the Federal Tax Service on the official website.

“At the location (registration)” it is indicated that the declaration is submitted at the place of registration of the organization. For this, the code “214” is indicated.

“Taxpayer” – indicate the full name of the organization, or the full last name, first name and patronymic of the entrepreneur. It should be indicated in the same way as written in the registration certificate.

“Code of the type of economic activity according to the OKVED classifier” - it should be borne in mind that from 2021 the code is indicated in accordance with the OKVED2 classifier.

“Contact telephone number” – indicate a landline or cell phone number, including the area code.

Filling out the second section of the declaration

If the organization performed transactions with several counterparties, then section 2 should be filled out for each of them; to do this, you need to add additional pages of the second section.

For one counterparty, one page of the second section is filled out, regardless of how many contracts of the same type are concluded with him. If the type of agreement for each transaction with a counterparty is different, then you will still have to add additional pages. Moreover, each page must contain information on contracts of the same type.

In line 020, the counterparty is indicated if it relates to:

- To the government agency leasing the property;

- To the seller selling treasury property;

- To a foreign organization that is not registered with the tax authority of the Russian Federation;

- To a bankrupt debtor, and the tax agent acquires property from him.

In line 020, dashes are added if the organization purchased a vessel that is not registered in the Russian Register of Ships within 45 days from the date of purchase, or when the organization sells:

- Property in accordance with a court decision or confiscated;

- Confiscated property;

- Ownerless or purchased assets;

- Treasures;

- Values that were transferred to the state by right of inheritance.

Line 040 “Budget classification code” – is entered by KBK VAT 182 1 0300 110.

Line 050 – indicated by OKTMO according to the registration of the organization. You can find out OKTMO on the official website of the Federal Tax Service.

Line 070 – indicates the transaction code where the organization was a tax agent. You can find the required code in Appendix No. 1 to the Procedure, approved by Order of the Federal Tax Service No. ММВ-7-3 / [email protected] dated 10.29.2014.

Line 060 - before filling it out, the need to fill in lines 080, 090, and 100 is checked. They are filled in in cases where dashes are placed in line 020, or if the organization acted as an intermediary in the sale of goods by foreign companies. In all other cases, dashes are placed in these lines.

Line 080 – VAT on shipment is indicated.

Line 090 – VAT on prepayment of the reporting period is indicated.

Line 100 – VAT is indicated on prepayments of the current and previous quarters, against which the shipment was made in the reporting period.

Line 060 – indicates the amount of VAT payable. When 080-100 lines are filled in, the amounts are calculated using the formula:

Line 060 = line 080 + line 090 – line 100.

If lines 080-100 contain dashes, then VAT is calculated on transactions in line 070.

VAT return form

In 2021, VAT reporting must be submitted in the form approved by Order of the Federal Tax Service dated October 29, 2014 N ММВ-7-3/ [email protected] (as amended on December 20, 2016).

tax return for value added tax (VAT).

Please note the last 4 digits of the barcode located in the upper left corner of the Cover Page. They should be 0017:

Example

Continent LLC is an intermediary in the sale of goods by a foreign company that is not registered for tax purposes in the Russian Federation. Continent LLC enters into an agreement for the amount of 1,250 thousand rubles for the supply of goods with Federation LLC.

On March 20, 2021, Federation LLC made an advance payment to Continent LLC of 850 thousand rubles, including VAT.

On May 20, Continent LLC shipped goods to Federation LLC for 625 thousand rubles.

On July 20, Continent LLC made a second shipment to Federation LLC for 625 thousand rubles.

On July 25, Federation LLC paid the remaining amount of the contract - 400 thousand rubles.

Filling out a VAT return.

First quarter:

Line 090 – RUB 129,661, based on 18% VAT on the prepayment amount.

Line 080 is not filled in.

Line 060 – 129,661 rub.

Second quarter:

Line 080 – RUB 112,500, based on 18% VAT on shipment.

Line 100 – 112,500 rubles, since VAT on prepayment is higher than VAT on shipment;

Line 060 – 0 rub.

Third quarter:

Line 080 – 112,500, based on 18% VAT on shipment.

Line 090 – put a dash.

Line 100 – 17,161 rubles, based on the calculation of 129,661 – 112,500.

Line 060 – 95,339 rubles, based on 112,500 – 17,161.

Who can submit a VAT return on paper

Only individual entrepreneurs and organizations exempt from paying this tax and tax agents who are not VAT payers can submit value added tax reports in paper form.

Please note that submitting a VAT return on paper while being required to submit it electronically will be equated by the tax authority to failure to submit reports at all, which will entail tax liability and the imposition of penalties.

A single simplified declaration (SUD) is also submitted on paper.

Filling out sections 8 and 9 of the declaration

Section 8 should contain information from the purchase book. Only transactions for which the right to deduction arose during the reporting period are reflected. The section is completed by all tax agents, with the exception of organizations selling seized property by court decision, or goods of foreign companies.

Section 9 should contain information from the sales book. The section is filled in by all tax agents for transactions that resulted in an obligation to pay VAT to the budget (

Who files a VAT return?

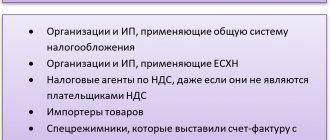

Value added tax reporting is required to be submitted by:

- Individual entrepreneurs and organizations on the general taxation system.

An exception is provided for taxpayers exempt from paying VAT in accordance with Art. 145 Tax Code of the Russian Federation.

- Importers of goods to the territory of the Russian Federation.

When importing goods into Russia, all individual entrepreneurs and organizations are required to pay VAT and submit appropriate reports, regardless of the taxation system applied.

- Tax agents.

Tax agents for VAT are individual entrepreneurs and organizations purchasing goods from foreign persons who are not registered for tax purposes in the Russian Federation for further sale of this product on the territory of the Russian Federation, as well as tenants of federal and municipal property and property of constituent entities of the Russian Federation. Also, a tax agent is a person who acquires state property and property of persons declared bankrupt (with the exception of individuals who are not individual entrepreneurs).

- Intermediaries issuing invoices with an allocated VAT amount on their own behalf.

Individual entrepreneurs and organizations that are intermediaries (acting on the basis of an agency agreement, commission agreement or mandate) pay VAT based on the remuneration they receive under the specified agreement.

- Individual entrepreneurs and organizations that are not VAT payers, but have issued an invoice with the allocated VAT amount during the tax period.

Individual entrepreneurs and organizations that are not OSNO payers and operate within the framework of special tax regimes (USN, UTII, Unified Agricultural Tax or PSN), but have issued an invoice to their counterparties with the allocated amount of VAT, are required to pay the VAT received from the counterparty to the budget and submit a tax return.