Re-exposed how to write correctly

Has entered! (“The Golden Calf”, I. According to the existing rules, the letter e is written in the personal endings of verbs of the first conjugation of the indicative mood in the second and third person singular, as well as the first and second person of the plural of the present and future tense; in the corresponding forms of verbs of the second conjugation - And.

Let's compare the endings of the verbs of the future tense I and II conjugations: Future tense I conjugation II conjugation Singular Plural Singular Plural I will write We will write I will study We will study You will write You will write You will study You will study He, she, it will write They will write He, she, it will study They will study Write - a verb form that corresponds to the imperative mood of the verb write. Info Thus, “Russian Grammar” (M., 1980) considers the forms miss you and miss you as variable. In the reference book by D. E. Rosenthal “Management in the Russian Language” it is indicated that with nouns and 3rd person pronouns it is correct: to miss someone or something, for example: to miss your son, to miss him.

But with personal pronouns of the 1st and 2nd person plural.

numbers are correct: miss someone, for example: missed us, miss you. But the option of missing someone, which is also asked quite often, is not normative and goes beyond the scope of the Russian literary language. 9. What do the words glamorous, creative, brutal mean?

Glamor - from English. glamor – 'charm, charm'; 'romantic halo'; 'enchantment, magic', (colloquial) 'luxury, chic'. At the end of it, the letter i is written under the accent.

Re-invoice as spelled

But even if there is no such condition, it is more advisable to first write a letter of claim and try to resolve everything peacefully, rather than spending huge resources on legal proceedings.

If the intermediary makes a transaction on terms more favorable than those specified by the customer, an additional benefit is generated; it can be divided equally between the counterparties, unless otherwise provided by the contract (Article 992 of the Civil Code of the Russian Federation). The Tax Code does not regulate the procedure for re-billing expenses and the procedure for deducting VAT in such cases.

Therefore, companies have a question: can “input” VAT on these transactions be deducted?

As it turns out, this largely depends on the documentation of the rebilling transactions. To reissue adjustment documents to the principal, a Sales Adjustment document is created with the operation type Adjustment as agreed by the parties, and the invoice issued to the principal on behalf of the supplier is indicated as the basis document.

The commission agent's report, from an accounting point of view, is the primary document for both parties to the contract. The form of the report can be arbitrary or established in the contract.

Moreover, it must contain the mandatory details listed in Part 2 of Article 9 of the Law of December 6, 2011 No. 402-FZ.

If you do not want to deal with the sale of goods, you can entrust this to an intermediary (commission agent) by concluding a commission agreement with him. Commissioner

How to re-invoice the services of another organization

Consequently, not 1.53 million rubles are paid to the budget, but 460 thousand rubles.

This can be a simplification, imputation or unified agricultural tax. Typically, the choice in favor of one of the preferential regimes without VAT is due to the desire to reduce the tax burden and time costs for maintaining accounting records.

Thus, the income tax rate is 20%, while the single tax under the simplified tax system is calculated at a rate of 6 or 15%, and in some regions there is a reduced rate.

Working without VAT is especially justified for small organizations, the main circle of clients of which are individuals.

These are, for example, representatives of the retail trade sector or organizations providing personal services to the population (for example, hairdressers or apartment renovations).

What are the disadvantages for the counterparty?

On the one hand, when purchasing goods from a company under a special regime, an organization using OSNO can take into account the entire amount of costs when calculating income tax.

VAT when re-invoicing expenses (Misnikovich L.)

Rebilling of utility costs by the landlord According to Art. 606 of the Civil Code, under a lease agreement, the lessor undertakes to provide the tenant with property for a fee for temporary possession and use or for temporary use.

The tenant is obliged to maintain the property in good condition, carry out routine repairs at his own expense and bear the costs of maintaining the property, unless otherwise provided by law or the lease agreement (Clause 2 of Article 616 of the Civil Code of the Russian Federation). The costs of maintaining the rented premises include, in particular, electricity costs. Based on paragraph.

1 tbsp.

539 of the Civil Code, under an energy supply agreement, the energy supplying organization undertakes to supply energy to the subscriber (consumer) through the connected network, and the subscriber undertakes to pay for the received energy, as well as to comply with the regime of its consumption stipulated in the agreement, to ensure the safe operation of the energy networks under its control and the serviceability of the devices it uses and equipment related to energy consumption.

Rebilling expenses from another organization

I receive posting 62.01/7609.

SF is included in the accounting journal. There are no sales in the book. ?6.09 closes A should B at 60. C should A at 62. In principle, there is no need to even redo anything.

Maybe you see some pitfalls in this scheme - if you have a similar principle implemented? The only caveat is that in the Federation Council from A to B they want to see the participation of organization B in some form.

Otherwise, there is no sign that this is a re-invoicing of someone else’s services, and not the provision of one’s own. Your company gives out some kind of extra.

Re-invoicing of reimbursable costs: how not to lose VAT deductions from end customers

At the same time, the parent company does not reflect these invoices in the books of purchases and sales and does not accept VAT for deduction and does not charge VAT to the budget, while subsidiaries reflect such invoices in the purchase book and accept VAT for deduction.

Starting from the 1st quarter of 2015, tax authorities conduct global electronic reconciliation of all invoices and all counterparties. If discrepancies are detected, the parties will be sent a request for clarification, and buyers may lose their VAT deduction.

The rules for filling out an invoice used in VAT calculations (hereinafter referred to as the Rules for filling out an invoice), approved (hereinafter referred to as Resolution No. 1137), provide for the procedure for issuing invoices within the framework of intermediary agreements (commission, agency).

According to this procedure, in the case of purchasing goods (work, services) on his own behalf, the commission agent (agent), when issuing invoices to the principal (principal), reflects in them the indicators of the invoices that were issued to him by the sellers of these goods (works, services) (subclause

Registration and taxation of overbilled expenses

Please also note that in this situation, your organization may have problems with deducting VAT on overbilled expenses. In accordance with paragraph 1 of Art. 171 of the Tax Code of the Russian Federation has the right to reduce the total amount of tax by established tax deductions. The procedure for applying tax deductions is established in Art.

172 of the Tax Code of the Russian Federation. Tax amounts are subject to deductions if three conditions are met: - goods (work, services) must be accepted for accounting (clause 1 of Article 172 of the Tax Code of the Russian Federation), which must be confirmed by relevant documents; - goods (work, services) must be used in activities subject to VAT or are intended for resale (clause

2 tbsp. 171 Tax Code of the Russian Federation); — the taxpayer must receive an invoice from the supplier (clause 2 of article 169, clause 1 of article 172 of the Tax Code of the Russian Federation). Thus, the organization has the right to claim VAT for deduction in the period in which all the conditions provided for in Art.

171, art. 172 of the Tax Code of the Russian Federation.

We record the invoices received from the carrier organization in the journal of received and issued invoices (clause

1, sub. "a" clause 11 section. II adj.

Source: https://gmvp.ru/kak-perevystavit-uslugi-drugoj-organizatsii/

How can I correctly re-invoice?

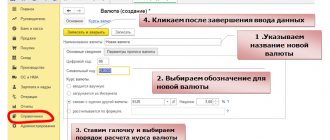

One copy is given to the buyer, the second remains with him. The intermediary indicates his copy in the accounting journal, but does not register it in the sales book. He must also make a copy of it and send it to the customer. The customer receives a copy of the document and issues an invoice to the intermediary, who in his the queue is recorded in the accounting journal, but not recorded in the purchase book. At the conclusion of the transaction, the intermediary gives the customer an invoice for the amount of remuneration for the transaction. After this, the customer already records it in the purchase book. About how to generate a consolidated invoice for the intermediary in the 1C program , see the following video: Accounting entries in this case are indicated on account 76: first, the intermediary puts funds from the buyer as receipts, then he puts the same funds as expenses, transferring them to the customer. The main thing in re-issuing an invoice is to indicate in the contract that the expenses or the proceeds from the transaction are transferred to another company. Re-invoicing is a very common practice in legal relations between individuals and legal entities.

For this you will have to pay him a reward.

This article discusses this issue in detail. Often in commercial activities, situations arise when a third party pays for goods or services provided by one enterprise, and the transaction is concluded thanks to the active participation of intermediaries. It is in such situations that the procedure for re-invoicing is initiated. The legislation does not establish a procedure re-listing

How to correctly recharge utilities to tenants

It draws these conclusions:

- The lessor takes into account the costs reimbursed by the tenant in the structure of income.

- The lessor takes into account the amounts sent to housing and communal services organizations in the income structure.

The Ministry of Finance of the entire country shares a similar position. That is, these norms apply to each region. Paragraph 1 of Article 146 of the Tax Code of the Russian Federation states that transactions for the sale of goods and services are considered the object of taxation.

When selling services, the seller issues invoices. This must be done no later than 5 days. The basis is paragraph 3 of Article 168 of the Tax Code of the Russian Federation.

Official structures believe that the landlord does not issue invoices to the tenant. This is due to the fact that re-listing does not imply the sale of services. That is, when receiving funds as reimbursement of the lessor's expenses, VAT is not subject to VAT. The basis is numerous letters from the Ministry of Finance. For example, letter of the Ministry of Finance No. 03-03-06/2/51 dated May 14, 2008.

How to reflect this in the organization's accounting? What documents must the supplier provide to the organization?

How is the re-billing of the services in question to the end buyer processed?

— video, comments

By virtue of paragraph 1 of Art. 509 of the Civil Code of the Russian Federation, the supply of goods is carried out by the supplier by shipping (transferring) the goods to the buyer, who is a party to the supply agreement or to the person specified in the agreement as the recipient.

In this case, the delivery of goods is carried out by the supplier using the transport provided for in the supply agreement and on the terms specified in the agreement; if the contract does not specify what type of transport or under what conditions delivery is carried out, the right to choose the type of transport or determine the conditions for delivery of goods belongs to the supplier, unless otherwise follows from the law, other legal acts, the essence of the obligation or business customs (clause 1 Article 510 of the Civil Code of the Russian Federation). At the same time, the parties to a civil law contract are free to conclude an agreement and determine its terms, except in cases where the content of the relevant condition is prescribed by law or other legal acts (clauses 1, 4 of Article 421 of the Civil Code of the Russian Federation).

Reissue an invoice - what needs to be done for this?

When considering such an example, we can make the assumption that such a transport company, on its own behalf, but at the expense of the customer, is capable of providing cargo transportation services for a certain fee.

In such a situation, agents have an obligation to provide reports to the principals under the conditions provided for in a specific agreement. If the agreement is missing certain conditions, the agent will have to draw up a report on the progress of fulfilling the conditions specified in the drawn up agreement.

In accordance with generally accepted rules, certain evidence of expenses incurred by the agent at the expense of the customer must be attached to the agent's reporting.

This rule is discussed in paragraphs.

,2 tbsp. 1008 of the Civil Code of the Russian Federation. All possible situations that arise in the process of issuing and recording invoices by the parties involved in drawing up an intermediary agreement are indicated in the Rules for maintaining lists of provided invoices, databases with purchases and sales in the process of VAT calculations, described in the current resolution of 02.12. 2000 No. 914. When purchasing services for the principal, the agent provides an invoice, which must provide the details of the invoice issued by the seller of the services provided to this intermediary.

Civil Code of the Russian Federation The basic principle of selling goods through an intermediary: If the sale of products is carried out with the participation of an intermediary, it must be indicated in the invoice for payment.

Registration and taxation of overbilled expenses

Please also note that in this situation, your organization may have problems with deducting VAT on overbilled expenses. In accordance with paragraph 1 of Art. 171 of the Tax Code of the Russian Federation has the right to reduce the total amount of tax by established tax deductions. The procedure for applying tax deductions is established in Art.

172 of the Tax Code of the Russian Federation. Tax amounts are subject to deductions if three conditions are met: - goods (work, services) must be accepted for accounting (clause 1 of Article 172 of the Tax Code of the Russian Federation), which must be confirmed by relevant documents; - goods (work, services) must be used in activities subject to VAT or are intended for resale (clause

2 tbsp. 171 Tax Code of the Russian Federation); — the taxpayer must receive an invoice from the supplier (clause 2 of article 169, clause 1 of article 172 of the Tax Code of the Russian Federation). Thus, the organization has the right to claim VAT for deduction in the period in which all the conditions provided for in Art.

171, art. 172 of the Tax Code of the Russian Federation.

- Invoice

We record the invoices received from the carrier organization in the journal of received and issued invoices (clause

1, sub. "a" clause 11 section. II adj.

3 to the Decree of the Government of the Russian Federation “On filling out documents for VAT calculations” dated December 26, 2011 No. 1137).

For the buyer:

- we issue an invoice for transport services on our behalf and attach to it a copy of the invoice of the carrier organization (clause 1, subparagraph “a”, clause 7, section II, appendix 3 of the Decree of the Government of the Russian Federation “On filling out documents when making payments for VAT" dated December 26, 2011 No. 1137), registered in the invoice journal;

- We register the invoice for the brokerage fee in the sales book.

NOTE! When re-issuing an invoice for transport services, in lines 1 (date), 2, 2b, enter the information of the carrier organization, and not your own (sub.

“a”, “c” clause 1 section. II adj. 1 to the resolution of December 26, 2011 No. 1137)

Attention

In this case, in order to accept VAT for deduction, the taxpayer must register the work (services) (Resolution of the Federal Antimonopoly Service of the Moscow District dated June 24, 2014 N F05-5989/2014 in case N A40-137020/13). The courts recognize the lawfulness of the use of deductions on invoices , issued to the buyer by suppliers of goods for transport services, which were actually provided by carriers, since Ch.

Comments and opinions Sasha_1CK 07.16.14 — 11:20 Organization A brought goods in a container for itself and for organization B.

For which I paid the transport company B. Let the goods be divided equally, and the transport company issued an invoice for 118 rubles (including 18 rubles VAT per hour). All participants in the process are VAT payers. Now organization A must pay B 118 rubles and re-bille 59 rubles to organization B. We are talking about re-billing expenses.

Info

Reissue an invoice for payment

In addition, the date of preparation and the name of the document must be indicated. The invoice may be reissued in the case when the document is issued to one person, and another person will pay for it. This is permissible in the following cases:

- Within the scope of the rental agreement.

- When the legal entity purchasing the product or service is a representative of another company. In this case, the invoice comes to the name of the trustee, who in turn must reissue it to the principal.

- As part of the commission agreement. In this case, the paper is first submitted for payment to the commission agent, and after payment he forwards it to the committent.

We recommend reading:

In these cases, the invoice must be reissued to another person (individual or legal). Read about how to write a letter of guarantee for payment here. In order to redirect a document, it is necessary that the contract contains a column indicating that another company can make payment for the company. Without this column, this action is impossible. The whole point is that if this is not stated in the agreement, there is simply no one to redirect the invoice to. The principle of the sale of goods through an intermediary:

- He must also make a copy of it and send it to the customer.

- If the sale of products occurs through an intermediary, he indicates himself in the invoice for payment and draws up two copies of the document. One copy is given to the buyer, the second remains with him.

- Customer

- The intermediary indicates his copy in the accounting journal, but does not register it in the sales book.

Method 2. Changing the cost of the product

This type of re-invoicing of transport costs is not common in practice, but it is simpler in terms of documentation compared to the first.

- Agreement

Clause 3 Art. 485 of the Civil Code of the Russian Federation provides that in the sales contract it is possible to include a clause on changing the value of the goods upon the occurrence of certain circumstances. Alternatively, you can add a condition: if the delivery of the goods to the buyer is organized by the supplier, then the cost of the goods increases by the cost of transporting the goods to the buyer.

- Source documents

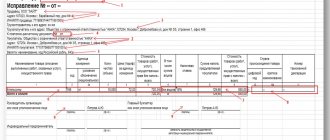

At the time of transfer of the goods to the carrier organization, you will already have an agreement on the provision of transport services and an invoice for payment for these services. Using these documents, we determine the amount of transportation costs (including VAT) and add it to the cost of the goods shipped to the buyer. We indicate the amount received in the delivery note. If several types of goods are shipped, then we distribute transportation costs between them in equal shares.

You can familiarize yourself with the form of the consignment note in the article “Unified form TORG-12 - form and sample.”

IMPORTANT! Do not include the cost of transport services as a separate line in the invoice. You do not provide services for the transportation of goods, therefore such a service should not be included in the invoices you issue.

If the cost of transport services changes after the buyer receives the invoice, adjustments are made to it in one of two ways:

- registration of a new adjusted invoice;

- making corrections to already completed 2 copies of the invoice: yours and the buyer’s.

For information on making changes to primary documents, read the material “Correcting errors in primary documents: The Federal Tax Service introduces new rules.”

The invoice received from the carrier organization will be considered the basis for reflecting expenses associated with the sale of goods (subclause 1, clause 1, article 253 of the Tax Code of the Russian Federation).

- Invoice

We issue an invoice for the amount indicated in the delivery note: the cost of the goods, increased by the cost of transport services. We record it in the sales book. If the cost of transport services included in the price of the goods changes, we generate an adjustment invoice for the amount of the increase (decrease) in transport costs (paragraph 3, clause 1, article 169 of the Tax Code of the Russian Federation). There is no need to correct the old invoice.

For an example of filling out adjustment invoices, see the article “Sample of filling out an adjustment invoice (2017-2018)”.

We register the invoice received from the carrier organization in the purchase book.

How to reissue an invoice for payment: why is it necessary and how to do it correctly

In addition, a word may use more letters than sounds.

For example, “children’s” - the letters “T” and “S” merge into one phoneme [ts]. And vice versa, the number of sounds in the word “blacken” is greater, since the letter “Yu” in this case is pronounced as [yu].

It is possible to make a correct sound analysis and accurately determine the characteristics of a vowel only after placing stress in the word. Do not forget also about the existence of homonymy in our language: za'mok - zamo'k and about the change in phonetic qualities depending on the context (case, number):

- New houses [no'vye dama'].

- I'm home [ya do'ma].

In an unstressed position, the vowel is modified, that is, it is pronounced differently than written:

- witness = [sv'id'e't'il'n'itsa].

- mountains - mountain = [go'ry] - [gara'];

- he - online = [o'n] - [anla'yn]

Such changes in vowels in unstressed syllables are called reduction. Quantitative, when the duration of the sound changes.

The same unstressed vowel letter can change its phonetic characteristics depending on its position:

- at the absolute beginning or end of a word;

- in open syllables (consisting of only one vowel);

- primarily relative to the stressed syllable;

- on the influence of neighboring signs (ь, ъ) and consonant.

Thus, the 1st degree of reduction is distinguished.

And high-quality reduction, when the characteristics of the original sound change.

It is subject to:

- vowels in the first pre-stressed syllable;

- naked syllable at the very beginning;

Re-invoice as spelled

- initial form – milk;

- direct object in the sentence.

- variable morphological features: accusative case, singular;

- constant morphological characteristics of the word: neuter, inanimate, real, common noun, II declension;

Here is another example of how to make a morphological analysis of a noun, based on a literary source: “Two ladies ran up to Luzhin and helped him get up.

(example from: “Luzhin’s Defense”, Vladimir Nabokov).” Ladies (who?) is a noun;

- initial form - queen;

- syntactic role: part of the subject.

- constant morphological features: common noun, animate, concrete, feminine, first declension;

- inconsistent morphological characteristics of the noun: singular, genitive case;

Luzhin (to whom?) - noun;

- initial form - Luzhin;

- inconsistent morphological features of the noun: singular, dative case;

- correct morphological characteristics of the word: proper name, animate, concrete, masculine, mixed declension;

- syntactic role: addition.

Palm (with what?) - noun;

- constant morphological features: feminine, inanimate, common noun, concrete, I declension;

- inconsistent morpho.

He began to knock the dust off his coat with his palm.signs:

- initial shape - palm;

How to re-issue an invoice for payment?

The law does not provide a list of required fields, but organizations usually include the following sections in the invoice:

- serial number and date of issue - this will make it easier to understand why exactly the money was received on the account (usually the buyer writes in the purpose section of the payment order something like the following phrase “Payment of invoice No.... dated ... 2016 for construction materials”); bank details of the supplier: name of the bank and its BIC, bank address, correspondent account and current account;

- name of the seller (contractor);

- supplier contact details: phone, fact and email;

- the name of the services provided or goods shipped, their quantity, unit price and total cost.

- its details: INN and KPP (for companies only), legal and actual address;

Instead of indicating the name of the product, you can refer to the Agreement (for example, “Advance payment under contract No. 245 dated September 28, 2016”) or simply indicate the basis for its issuance (“For, etc.). To create an invoice for payment as an offer, it must contain indications of important terms of the transaction. For example, the goods will be shipped within 3 business days after payment or receipt of money to the seller’s account.

In this case, specifying the due date for payment of the invoice allows you to fix the terms of the agreement for a certain period.

Thus, complying with the rules for preparing invoices for payment becomes a very important element of the enterprise’s work, since it bears a certain legal responsibility. According

Re-spelt it correctly

It’s easy to remember how to correctly spell perevystavit or perevystavit, you just have to learn and remember a simple rule, let’s figure it out together. Which rule is spelled correctly? A verb form formed using the prefix “pere” and the ending “te.” Examples of sentences:

- “Re-rate me, please, I corrected it,” Marianna was indignant.

- It’s easy to say “re-list”, but how can you do this if the electronic magazine has been closed for a long time?

Incorrect spelling: Re-expose, peri-expose, re-expose. Why?

Spelling, rule. How to correctly spell the word: “reset” or “reset”? How to correctly write the word: “reset” or “reset”? What part of speech is the word reset? An example sentence with the word reset? Read also: How to make tea with fresh mint How to parse the word by its composition to re-expose? Morphemic analysis of the word re-expose? There is such a verb in the Russian language. According to the buyer’s remark, the manager had to (WHAT TO DO?) re-invoice for the services provided and “put” is.

They represent a word-formation chain of words with the same root. The morphemic composition of the given verb pere/vy/stav/i/t is already visible: it has two prefixes pere- and vy-, the root stav-, the verbal suffix -i- and the formative suffix -t (in school the program is interpreted as the end).

The base of the word is re-exposed (neither the formative suffix nor the ending is included in the base of the word). So. The part of speech has been determined, the morphemic composition too, all that remains is to answer the question about the spelling of the given word. Firstly, you need to understand once and for all that prepositions and verbs are not friends.

How can I correctly re-invoice?

An invoice for payment is a document that the seller of goods or services gives to the buyer so that, using his details, the client can pay for the goods or services received or make an advance payment. This paper indicates the exact details of both companies (seller and buyer), their name and address.

In addition, the date of preparation and the title of the document must be indicated. The invoice may be reissued in the case when the document is issued to one person, and another person will pay for it. This is permissible in the following cases:

- When the legal entity purchasing the product or service is a representative of another company. In this case, the invoice comes to the name of the trustee, who in turn must reissue it to the principal.

- As part of the commission agreement. In this case, the paper is first submitted for payment to the commission agent, and after payment he forwards it to the committent.

- Within the scope of the rental agreement.

In these cases, the invoice must be reissued to another person (individual or legal).

If you are interested, read this material. Read about how to write a letter of guarantee for payment.

In order to redirect a document, it is necessary that the contract contains a column indicating that another company can make payment for the company.

Without this column, this action is impossible. The thing is that if this is not stated in the agreement, there is simply no one to redirect the account to.

The operating principle of selling goods through an intermediary:

- If the sale of products occurs through an intermediary, he indicates himself in the invoice for payment and draws up two copies of the document. One copy is given to the buyer, the second remains with him.

- The intermediary indicates its copy in the accounting journal, but does not register it in .

- He must also make a copy of it and send it to the customer.

- The customer receives a copy of the document and issues an invoice to the intermediary, which in turn is recorded in the accounting journal, but not recorded in.

- At the conclusion of the transaction, the intermediary gives the customer an invoice for the amount of remuneration for the transaction.

- After this, the customer records it in the purchase book.

To learn how to generate a consolidated invoice for an intermediary in the 1C program, see the following video: Accounting entries in this case are indicated on account 76: first, the intermediary puts funds from the buyer as receipts, then he puts the same funds as expenses, transferring them to the customer . The main thing in re-invoicing is to indicate in the contract that the costs or income from the transaction are transferred to another company.

How to pay an invoice

There are several ways to pay invoices issued by a company or individual entrepreneur for goods purchased or services used.

For example, a novice entrepreneur, purchasing the initially necessary equipment, receives an invoice that is based on the generated estimate for the product of interest.

When a businessman places an order, he is given an invoice that must be paid. To do this, the entrepreneur should familiarize himself with payment methods.

Payment by cash

Cash payment today is considered the simplest and most straightforward. The buyer must come to the main office or store and pay the invoice provided to him in cash.

However, using this method in some situations is difficult or even impossible. For example, when the seller is located a thousand kilometers from the buyer.

Flying to the city where the seller is located in order to pay the bill is hardly advisable. Here the entrepreneur just needs to use another method - cashless payment.

Statistics show that today in small businesses no more than five percent of payments made are in cash.

Payment by bank transfer

With the development of technology and the transition of the whole world to the card system for receiving wages, the topic of paying invoices through non-cash payments has become especially relevant.

There are two types of non-cash payment:

— payment of a bill at a banking organization. Any modern invoice can be paid at the cash desk of a banking organization. However, this method has its significant disadvantage. For paying the bill, each bank sets its own commission, which the buyer must additionally pay.

The amount of such tax ranges from two to seven percent, that is, the higher the payment amount, the greater the amount of commission you will have to pay in favor of the banking institution.

For example, for paying a bill in the amount of two hundred thousand rubles, the commission will be equal to four to fourteen thousand rubles.

Such costs, of course, are undesirable, so the buyer can use the following calculation method;

— payment to the bank account. Each organization has its own current account, where funds are credited after a purchase/sale transaction is completed. An entrepreneur who opens an individual entrepreneur or is engaged in private entrepreneurship will also have to open a personal bank account where buyers will deposit payments.

The downside is the monthly payment for using the service. Typically, the amount of such payment ranges from 500 to 2000 rubles, depending on the range of opportunities provided. However, there are also undeniable advantages.

A fixed rate is charged for performing a specific operation, which on average equals 25 rubles. That is, for payment of one million rubles a commission of 25 rubles will be taken. Another advantage is the fact that information about all transfers is stored in the banking organization.

The entrepreneur does not have to worry that all the data may be lost, damaged, and so on.

Payment order

Transfer of funds from a personal account is carried out by settlement according to the presented payment order. This order can be either electronic or printed on paper. The payment order is typed using the bank’s specific accounting programs and printed out on paper. The most commonly used program is called 1C Enterprise.

I use it to earn money:

Workzilla - remote work for everyone High-quality business plans with a guarantee

For a new entrepreneur, installing this program on your computer is a very profitable operation. A 1C Enterprise license costs about three thousand rubles. The program is quite simple, easy to use, and has many useful options that will be useful and understandable to a novice businessman.

The payment order can be made independently or with the help of a bank employee who maintains the current account of a particular entrepreneur.

The average price for this service is one hundred rubles, which completely eliminates the need to understand an unfamiliar program. A businessman can also install a special program for working with payment orders and paying them via the Internet.

In this case, you won’t even have to leave the walls of your own home or office to make calculations.

How to re-issue an invoice for payment?

- /

- /

December 31, 2021 0 Rating Share Re-invoicing is sometimes required in the course of commercial activities of organizations and individual entrepreneurs.

In our article we will tell you what this means and when it is allowed. In commercial practice, there are cases when another person must pay for services (goods) provided (supplied) to one person.

According to the law, this requires, as accountants say, to reissue the invoice. In what cases is such an action allowed?

Don't know your rights? Subscribe to the People's Adviser newsletter.

Free, minute to read, once a week. Subscribe

There may be several options here:

- As part of the order. Under this agreement, one party acts on behalf and at the expense of the other (principal). Accordingly, she will forward all invoices sent to her to the principal.

- Within the framework of the commission. Here the commission agent will already act on his own behalf. Therefore, if the contract provides for the obligation of the principal to reimburse expenses, then first the commission agent will pay the invoice himself, and then send his invoice to the principal.

- As part of the lease and sublease agreement.

To re-invoice, only one thing is necessary - that the contracts clearly indicate the obligation of one party to pay for the other.

Otherwise, there will simply be no one to re-invoice. Rating Share Legal advice Still have questions after reading?

Call the number and our lawyers will advise you! The call is free. We recommend reading October 3, 2021 0 October 3, 2021 0 October 2, 2021 0 Section news April 26, 2021 0 April 10, 2021 0 February 26, 2021 0

Subscribe to newsletter Subscribe

Re-invoicing

The problem of over-invoicing in various situations has been around for a long time. More and more often, counterparties refuse to issue invoices to organizations indicating the amount of expenses actually incurred by these organizations. As a result, these organizations are deprived of the opportunity to deduct VAT on certain expenses. This acute problem will be discussed in this article.

Let us immediately note that we will not find such a concept as “re-issuance of invoices” either in the Tax Code of the Russian Federation or in Decree of the Government of the Russian Federation of December 2, 2000 N 914. In this regard, it turns out that organizations cannot re-issue invoices .

The Ministry of Finance of Russia and the Federal Tax Service of Russia also explain in their letters that an organization does not have the right to deduct VAT on the basis of re-issued invoices (Letters of the Ministry of Finance of Russia dated 03.03.2006 N 03-04-15/52, Federal Tax Service of Russia dated 29.12.2005 N 03 -4-03/2299/ [email protected] ). These Letters refer to invoices for the cost of utilities issued by the landlord. Later, Letter of the Ministry of Finance of Russia dated March 24, 2007 N 03-07-15/39 provides clarifications regarding VAT not only on utility services, but also on communication services, cleaning and security services, the cost of which is reimbursed by the tenant to the landlord in excess of the rent. The officials' explanations are based on the fact that for the services listed above, within the framework of concluded contracts, landlords do not have the right to issue invoices to tenants, since these services are not sold by the landlord.

However, sometimes (though not in all cases) regulatory authorities allow re-invoicing. An example of this is the Letter of the Ministry of Finance of Russia dated May 24, 2006 N 03-04-10/07, which talks about re-issuing invoices for the cost of work (services) that are not implemented by the organization: The Ministry of Finance allows the customer-developer to issue consolidated invoices to the investor for the cost of contract work performed by third party contractors based on invoices received from those contractors.

Re-invoice as spelled

At the end of it, the letter i is written under the accent. You can determine which mood a verb belongs to by the meaning of the sentence:

- Write to me more about your trip.

- When you write about all this, it will turn out to be a good story.

In the first sentence, the verb write is used in the indicative mood.

It simply indicates the action to be performed. In the second, write the imperative verb induces to perform this action.

- The verb write indicates an action; the verb write encourages its implementation.

- Write the verb form of the imperative mood. Write - the personal form of the verb I conjugation in the indicative mood.

In the verb write, the stress falls on the vowel -i- at the ending -ite; in the verb write, the stress is not on the ending, but on the root vowel. To understand the scheme, let’s conduct a written analysis of the morphology of the verb using the example sentence: God somehow sent a piece of cheese to the crow... (fable, I.