An employee who has the right to a property deduction has the right to use any convenient method for receiving it: draw up a declaration at the end of the year and return the money from the Federal Tax Service or receive it from the employer on the basis of a special notice, approved. By Order of the Federal Tax Service dated January 14, 2015 No. ММВ-7-11/ [email protected] All income tax accruals and deductions for companies and entrepreneurial employers are reflected quarterly in Calculation 6-NDFL. We’ll tell you how to reflect property deductions in 6-NDFL and give examples.

imushchestvennyy_vychet_v_6-ndfl.jpg

An employee who has the right to a property deduction has the right to use any convenient method for receiving it: draw up a declaration at the end of the year and return the money from the Federal Tax Service or receive it from the employer on the basis of a special notice, approved. By Order of the Federal Tax Service dated January 14, 2015 No. ММВ-7-11/ [email protected] All income tax accruals and deductions for companies and entrepreneurial employers are reflected quarterly in Calculation 6-NDFL. We’ll tell you how to reflect property deductions in 6-NDFL and give examples.

How are property deductions and 6-NDFL reports related?

Property deductions, which are described in Art.

220 of the Tax Code of the Russian Federation is a legal opportunity for individuals (who have purchased or built housing) to return part of previously paid income tax (through the tax office) or reduce current tax liabilities for personal income tax (if the deduction is provided by the employer). As a result of the provision of a property deduction by the employer, the amount of personal income tax included in the budget is reduced. This change in tax obligations is reflected in personal income tax reporting. First of all, this information falls into 6-NDFL, since this calculation is intended to fix the calculated and withheld personal income tax (order of the Federal Tax Service of Russia dated October 14, 2015 No. ММВ-7-11 / [email protected] ).

Thus, the provision of a property deduction and the data of the 6-NDFL report are closely interrelated.

Who is entitled to deduction

You can receive a deduction from your employer before the end of the tax period (clause 8 of Article 220 of the Tax Code):

for construction, purchase of housing (or a share in it) and land for individual housing construction;

on interest paid on loans, loans for the purchase of new housing or land.

Tax agents-employers do not provide property deductions for other types.

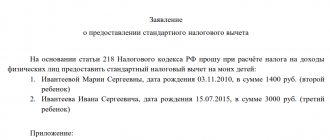

To receive a property deduction, an employee must:

obtain from the Federal Tax Service a notice confirming the right to a deduction, which indicates its amount;

write an application to the employer, attaching to it the document received from the tax office.

Beginning in the month of application, the employer will provide a deduction on accrued income until the end of the year, or until the deduction is fully spent. If the employee who submitted the application has the right to standard deductions (for children, for example), then first you need to take into account the standard deductions, and only then the property deductions.

Controversial points in section 2 of form 6-NDFL

Let us note right away: filling out section 1 is not difficult, and the data in it is indicated on an accrual basis. Problems appear only when filling out lines 070, 080, 090, since the data overlaps with section 2.

About the cumulative total

From the procedure for filling out the report, approved by Order of the Federal Tax Service of the Russian Federation dated October 14, 2015 No. ММВ-7-11/ [email protected] , it follows that the report is filled out on an accrual basis from the beginning of the year, including section 2. But the explanatory letters from the Federal Tax Service inform that in section 2 you need to indicate data only for the last 3 months of the reporting period. When submitting a half-year report, this becomes important: section 1 will contain cumulative data from the beginning of the year, and section 2 will need to display data only for 3 months: April, May, June.

About what is not necessary to fill out

When filling out the report for the 1st quarter of 2021, it was not clear how to fill out section 2 if there were no payments during the last 3 months of the reporting period. The presence of this section was mandatory in the electronic report format, so it was necessary to fill out lines with zero income and tax values and fictitious dates. The format has now been changed and Section 2 is not required to be completed. If there have been no payments for three months, section 2 should be empty.

About payment dates

There is no clear understanding of how and when (by what date) payments should fall into section 2.

In Kontur.Accounting, when the calculation is automatically filled out, the second section includes all payments accrued for 3 months, that is, those for which the date in line 100 falls in the last three months of the reporting period. The Federal Tax Service allows not to include in section 2 payments for which the date in line 110 is not included in these 3 months. For example, a salary for June paid in July.

We believe that this type of filling, in which section 2 includes all payments accrued for 3 months, is simpler and more transparent. In this case, the data in section 2 coincides with the data in section 1 and 2-NDFL, and users do not have additional questions about filling out lines 070, 080, 090 in section 1. And since the filling procedure and format of the electronic report do not provide for any restrictions, such filling is also considered correct.

Therefore, for transparency and ease of filling out 6-NDFL, we recommend that you first pay wages for the last month of the reporting period, withhold and transfer personal income tax, and then submit the report. In Kontur.Accounting, all data in the report will be filled in automatically.

About repeated payments

The filling order does not record the fact that if lines 100-140 for a specific payment fall into the second section of the report for one reporting period, they no longer need to be included again in the report for the next reporting period. For example, if the salary for March, paid in April, has already been reflected in the second section of the report for the 1st quarter, then the same data does not need to be included in the report for the half-year. We asked the Federal Tax Service employees about this and received confirmation. There is no official clarification on this issue yet, but we hope to receive it before the start of the reporting period.

About filling out a report when returning personal income tax

Difficulties arise with how to show the tax refund to the payer in the 6-NDFL report. What exactly is considered a return is also not clear. For example, is a negative tax amount resulting from a tax recalculation considered a refund? This situation may occur when providing deductions.

Example:

We have a conditional employee, his part-time salary is 5,000 rubles. He has a deduction for a child of 3,000 rubles, but in January the deduction was not issued. It was provided in February immediately for 2 months, and the excess tax withheld was returned to the employee.

January: salary 5000 rubles, personal income tax = 650 rubles (no deduction provided) February: salary 5000 rubles, personal income tax = (10000 - 6000) * 13% - 650 = -130 rubles (2 deductions provided) March: salary 5000 rubles, personal income tax = (15000 - 9000) * 13% - 520 = 260 rubles

It is not clear whether to fill out a refund in the amount of 130 rubles in line 090 of section 1 in this case? Or in line 070 indicate 780 rubles (650 - 130 + 260) already taking into account the refund? How to fill out section 2 in this case?

At the moment, in the described case, in Kontur.Accounting, line 090 is not filled in; the recalculation is taken into account in line 070.

About the calculation of personal income tax from intersettlement payments

When calculating tax on payments during the inter-calculation period (for example, from vacation pay), it is not clear how to take these deductions into account. They are provided for the month as a whole, and when calculating only vacation pay at the beginning of the month, it is not yet clear whether they can be provided. This can lead in some cases to problems in filling out 6-NDFL.

Example:

On January 10, the employee was paid vacation pay in the amount of 10,000 rubles, a deduction for a child of 3,000 rubles was not provided, and personal income tax was withheld in the amount of 1,300 rubles (that is, 10,000 * 13%). At the end of the month, the salary was calculated in the amount of 1000 rubles, the tax was calculated as an accrual total, taking into account the deduction for the month as a whole

Personal income tax on all income = (11000 - 3000) * 13% = 1040 rubles.

In general, the tax for the month turned out to be less than what was already paid on vacation pay. We reflect this in the reporting:

In section 1, the value in line 040 is equal to the value in line 070 = 1040 rubles.

In section 2:

Lines for vacation pay: line 130 - write 10000 line 140 - write 1300

Salary lines: line 130 - write 1000 line 140 - write -260

However, in the form of negative values and conversions are not provided. This situation was not visible in 2-NDFL, since there is no monthly tax calculation, especially for individual payments. In 6-NDFL, this situation arose, but it is not clear how to properly handle the “minuses”. There have been no explanations regarding this situation from the Federal Tax Service yet.

Therefore, when filling out a report in our service, we recommend changing the amount of vacation pay tax in Section 2 so that the salary tax is not negative. In our case, we need to change 1300 to 1040.

How to reflect a property deduction in 6-NDFL

in the amount of income received, if the deduction is greater than the income itself. If the employee’s notice, for example, indicated the amount of 1,500,000 rubles, and the accrued wages since the beginning of the year are 250,000 rubles, then line 030 includes the provided deduction equal to income -250,000 rubles.

in the amount of the accrued deduction if the amount according to the notification is less than the income for the period. For example: if the balance of the property deduction according to the notification is 20,000 rubles, and the accrued salary is 30,000 rubles, in line 030 you need to put 20,000 rubles.

Manager Krasnov brought a notice in January 2021 to provide a property deduction in the amount of 800,000 rubles, and wrote a statement. Krasnov’s salary is 50,000 rubles monthly. How to show the property deduction provided to him in 6-NDFL for the 1st quarter of 2021:

Salaries accrued for the 1st quarter: 50,000 x 3 months = 150,000 rubles.

The actual deduction provided will also be 150,000 rubles.

In the 6-NDFL report for the employee:

Reflection in reporting

How to reflect a property deduction in 6NDFL? In the 1st section of the report on form 6NDFL there is line 330. It is here that you need to indicate the amount of tax relief provided to the employee for the reporting period. It needs to be reflected on an accrual basis.

Correct filling of line 090 in report 6 personal income tax

To correctly fill out this line, you need to consider the following nuances:

- First you need to calculate the amount of tax deductions received by these employees for the reporting period. This includes not only property, but also the standard deduction for individuals, and others;

- summarize all information for all employees who wrote an application for such a benefit and confirmed their right with a package of documents.

- must be indicated on a cumulative basis from the beginning of the year to the end; if the amount of the deduction provided exceeds the tax accrued for payment, this leads to the fact that the personal income tax for this employee is equal to 0.

On a note! You can apply for a refund of property deduction at any time, starting from the moment of registration of legal rights to real estate. However, the general civil statute of limitations applies to returns. Therefore, you can only return for the last 3 years.

Recalculation since the beginning of the year

It often happens that employees submit a deduction application to the employer not in the first month of the year, but later. Then you have to recalculate the tax from the beginning of the year and return the overpaid amount to the employee. The tax liabilities of an individual are recalculated in the current period. Excessively withheld tax is returned, previous accruals are not corrected, all changes are reflected in the month in which they occurred (letter of the Federal Tax Service dated April 12, 2017 No. BS-4-11/6925).

In this case, the property deduction in 6-NDFL must be shown as follows:

The director of the company brought to the accounting department a notice and application for a property deduction in April 2021 in the amount of 1,600,000 rubles. For all months since the beginning of the year, wages were accrued in the amount of salary - 100,000 rubles. The accountant recalculated the tax in April and returned the excess withheld amount to the director’s salary card.

salary accrued for January - March: 100,000 x 3 months = 300,000 rubles;

withheld income tax for January - March: 300,000 x 13% = 39,000 rubles.

salary accrued 100,000 x 6 months = 600,000 rubles;

income tax for the 1st quarter was recalculated and returned in the amount of 39,000 rubles.

In fact, the property deduction was provided in the second quarter; the data must be indicated in the reporting for the half-year:

Financial assistance in 6-NDFL: what is not reflected

In the calculation part of 6-NDFL, some types of payments are not shown. These include cash payments issued for the following reasons:

- providing assistance to family members of a retired or deceased employee;

- loss of a loved one or relative by an employee;

- natural disaster or force majeure, including the presence of seriously injured persons;

- terrorist events resulting in injury to an employee or members of his family.

Also see “Personal income tax on financial assistance”.