New definition of current income tax

Current income tax is the amount that is actually payable to the budget.

It is determined based on the income tax base. The income tax base is determined as the difference between income and expenses. Until 2021, the current income tax was calculated from profit according to accounting data, adjusted by the amount of PNA (PNA) and the amount of change in IT (ONA). In 2021, the current income tax is the amount of tax calculated in accordance with the Tax Code.

Now only the norms of the Tax Code of the Russian Federation are taken as a basis. To calculate income tax, the tax base is multiplied by the tax rate.

The basic tax rate is 20%: 3% to the federal budget, 17% to the regional budget.

The main thing is to correctly determine the tax base.

Let us remind you that income tax income is determined on the basis of Articles 249, 250, 251 of the Tax Code of the Russian Federation, expenses - 253, 265, 270 of the Tax Code of the Russian Federation.

They contain lists of income and expenses from sales, non-operating income and expenses that are included in the tax base. It also lists costs and revenues that are not taken into account when calculating the tax base.

Read in the berator “Practical Encyclopedia of an Accountant”

Income not subject to income tax

What expenses are not taken into account?

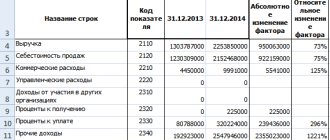

Income statement

From which reserve funds are created and funds for circulating production are increased.

Net profit is calculated as follows:

Income Tax Expense – Income Tax Recovered + Extraordinary Expenses – Extraordinary Revenues + Interest Paid – Interest Received. The result is an amount equal to EBIT, which stands for “earnings before interest and taxes.”

If you add depreciation deductions to the resulting amount and subtract the revaluation of assets, you get the EBITDA value. This indicator is used to level out the impact of income tax payments, borrowed funds and non-current assets.

Two options for determining the current income tax

PBU 18/02 provides two options by which you can determine the amount of the current tax:

- method of deferment - according to accounting data;

- balance sheet method - according to the data reflected in the tax return.

In any case, the amount of current income tax reflected in accounting must be equal to the amount entered in the tax return on line 180.

The rules by which tax is calculated are contained in PBU 18/02. Changes to this document were made by the Ministry of Finance by order No. 236n dated November 20, 2018. Income tax is reflected in the financial statements, in the income statement. Its form was also changed by order of the Ministry of Finance dated April 19, 2021 No. 61n.

in the Statement of Financial Results

According to the line “Gross profit (loss)” (line 2100)

information about the gross profit of the organization is reflected, i.e. on profit from ordinary activities, calculated without taking into account commercial and administrative expenses (if, in accordance with the accounting policy of the organization, administrative expenses are recognized as semi-fixed and are shown in the line “Administrative expenses”).

The value of the line “Gross profit (loss)” is determined as the difference between the indicators of the lines “Revenue” and “Cost of sales”. If, as a result of subtracting these indicators, the organization receives a negative value (loss), then it is shown in the Statement of Financial Results in parentheses.

The indicator in line 2100 “Gross profit (loss)” (for the same reporting period of the previous year) is transferred from the Statement of Financial Results for this reporting period of the previous year.

According to the line “Profit (loss) from sales” (line 2200)

information about the organization’s profit (loss) from ordinary activities is reflected.

The value of this line is determined by subtracting from the line indicator “Gross profit (loss)” the indicators of the lines “Commercial expenses” and “Administrative expenses”. If, as a result of subtracting these indicators, the organization receives a negative value (loss), then it is shown in the Statement of Financial Results in parentheses.

The indicator in line 2200 “Profit (loss) from sales” (for the same reporting period of the previous year) is generally transferred from the Statement of Financial Results for this reporting period of the previous year.

On the line “Profit (loss) before tax” (line 2300)

information about profit (loss) before tax (accounting profit (loss) of the organization) is reflected.

The value of this line is determined by adding the indicators of the lines “Profit (loss) from sales”, “Income from participation in other organizations”, “Interest receivable” and “Other income” and subtracting from the resulting amount the indicators of the lines “Interest payable” and “ Other expenses".

Current income tax by deferment method

The current income tax, determined by the deferral method (that is, in the old way), is formed on a separate sub-account to account 68. Its amount will consist of a conditional expense or income, a permanent tax expense or income (PNR and PND), as well as a deferred tax asset and deferred tax liability (ONA and ONO). In this case, we reflect all the indicators in the same way as we did before. Deferred taxes and liabilities should be reflected in account 09 or 77 in correspondence with account 68. Conditional expenses, PNR and PND - in accounts 68 and 99.

We will not give a cumbersome formula. Everything is clear from the contents of the accounting entries:

- Debit 99 Credit 68

- a contingent income tax expense is reflected;

- fixed tax expense is reflected;

- constant tax income is reflected;

- a deferred tax asset is reflected;

- deferred tax liability is reflected.

How to fill out individual lines on an income statement

In line 2110 “Revenue”, indicate the amount calculated using the formula:

In line 2120 “Cost of sales”, indicate in parentheses the debit turnover for the subaccount “Cost of sales” to account 90 “Sales”.

In line 2100 “Gross profit (loss)” indicate the amount calculated using the formula:

If you get a negative result (loss), then indicate it in parentheses.

In line 2210 “Business expenses” in parentheses, indicate the debit turnover for the subaccount “Sales expenses” or another similar subaccount to account 90 “Sales”.

In line 2220 “Administrative expenses” in parentheses, indicate the debit turnover for the subaccount “Administrative expenses” to account 90 “Sales”.

Fill in line 2200 “Profit (loss) from sales” as follows.

1. If line 2100 reflects profit (indicator without brackets), indicate in line 2200 the value calculated using the formula:

If you receive a negative result (loss), indicate it in parentheses.

2. If line 2100 reflects a loss (indicator in parentheses), indicate in line 2200 in parentheses the amount calculated using the formula:

You can check whether the line indicator 2200 is calculated correctly using the formula:

In line 2310 “Income from participation in other organizations”, indicate the credit turnover under the “Dividends” sub-account or another similar sub-account to the “Other income” sub-account of account 91, which you use to account for dividends received.

In line 2320 “Interest receivable”, indicate the credit turnover under the “Interest receivable” subaccount or another similar subaccount to the “Other income” subaccount of account 91, which you use to account for interest on loans issued.

In line 2330 “Interest payable”, indicate in brackets the debit turnover for the “Interest payable” sub-account or another similar sub-account to the “Other expenses” sub-account of account 91, which you use to account for interest on loans received.

In line 2340 “Other income”, indicate the amount calculated using the formula:

This value includes all income recorded on account 91, with the exception of interest and dividends received, in particular positive exchange rate differences.

In line 2350 “Other expenses” in parentheses, indicate the amount calculated using the formula:

This amount includes all expenses recorded on account 91, with the exception of interest payable, in particular:

— negative exchange rate differences;

— contributions to valuation reserves, incl. to the reserve for doubtful debts.

Fill out line 2300 “Profit (loss) before tax” as follows.

Current income tax using the balance sheet method

When using the balance sheet method, transfer the current income tax from the income tax return and reflect it by posting debit 99 and credit 68.

Do not reflect conditional expenses or income, PNR, PND on the accounting accounts.

But deferred taxes need to be reflected in a collapsed form in account 09 or 77 in correspondence with account 99.

The accounting entries will be as follows:

- Debit 99 Credit 68

- current income tax is reflected;

- a deferred tax asset is reflected;

- deferred tax liability is reflected.

Income Statement Line

Return to Financial result

Line 2110 “Revenue” reflects: credit turnover on account 90 “Sales” minus debit turnover on subaccount 90 “Value Added Tax” minus debit turnover on subaccount 90 “Excise Taxes”. An organization's income is recognized as an increase in economic benefits as a result of the receipt of assets (cash, other property) and (or) repayment of liabilities, leading to an increase in the capital of this organization, with the exception of contributions from participants (owners of property).

Line 2120 “Cost of sales” reflects: debit turnover in subaccount 90 “Cost of sales” minus turnover in the debit of subaccount 90 “Cost of sales” from the credit of account 26 “General expenses” minus turnover in the debit of subaccount 90 “Cost of sales” from the credit of account 44 "Sale expenses." An organization's expenses are recognized as a decrease in economic benefits as a result of the disposal of assets (cash, other property) and (or) the occurrence of liabilities, leading to a decrease in the capital of this organization, with the exception of a decrease in contributions by decision of participants (owners of property).

Line 2100 “Gross profit (loss)” reflects: line 2110 “Revenue” minus line 2120 “Cost of sales”.

Line 2210 “Business expenses” reflects: turnover in the debit of subaccount 90 “Cost of sales” from the credit of account 44 “Sales expenses”.

Line 2220 “Administrative expenses” reflects: turnover in the debit of subaccount 90 “Cost of sales” from the credit of account 26 “General expenses”.

Line 2200 “Profit (loss) from sales” reflects: line 2100 “Gross profit (loss)” minus line 2210 “Commercial expenses” minus line 2220 “Administrative expenses”. This amount should be identical to the result generated in subaccount 90 “Profit (loss) from sales.”

Line 2320 “Interest receivable” reflects: turnover on credit of subaccount 91.1 “Other income” from the debit of interest receivable accounts.

Line 2330 “Interest payable” reflects: turnover to the debit of subaccount 91.2 “Other expenses” from the credit of the interest payable accounts.

Line 2340 “Other income” reflects: credit turnover in subaccount 91.1 “Other income” (except for income included in lines 2310 “Income from participation in other organizations” and 2320 “Interest receivable”) minus turnover in the debit of subaccount 91.2 “ Other expenses" from the credit of account 68 "Calculations for taxes and fees" (in terms of value added tax, excise taxes, export duties accrued upon sale).

Line 2350 “Other expenses” reflects (if not reflected in other lines): turnover in the debit of subaccount 91.2 “Other expenses” from the credit of various accounts (except for interest payable, as well as VAT, excise taxes and other similar mandatory payments).

Line 2300 “Profit (loss) before tax” reflects: line 2200 “Profit (loss) from sales” plus line 2310 “Income from participation in other organizations” plus line 2320 “Interest receivable” minus line 2330 “Interest payable” plus line 2340 “Other income” minus line 2350 “Other expenses”.