How to maintain tax registers for calculating personal income tax: general requirements for development

When developing a personal income tax register, it is necessary to take into account some requirements:

- Tax registers for personal income tax in 2021 must necessarily contain the following information:

- information to enable identification of an individual;

- sign of tax residence;

- types of income and deductions indicating the corresponding code;

- amounts and dates of payment of income;

- dates of tax withholding, its transfer to the budget and details of payment orders.

- The register is maintained throughout the year for each employee.

- The form and sample of the tax accounting register for personal income tax must be determined by the accounting policy.

- If, during a tax audit, tax accounting registers for personal income tax are not provided, the organization may be fined 10,000 rubles. in case the register was not maintained during the calendar year, and for 30,000 rubles if the register was not formalized for several years (Article 120 of the Tax Code of the Russian Federation).

If you have access to ConsultantPlus, check whether you have developed the personal income tax register correctly. If you do not have access to the legal system, get a trial demo access for free.

Register form

There is no standard sample tax register for calculating personal income tax. Therefore, the tax agent must develop this form independently.

Include the following information in the register:

- tax agent data: name, tax identification number, checkpoint;

- personal data of the citizen to whom you are paying income (including his TIN - if available);

- types of income paid to a citizen - for each code (in accordance with the order of the Federal Tax Service of Russia dated September 10, 2015 No. ММВ-7-11/387);

- types of deductions provided - for each code (in accordance with the order of the Federal Tax Service of Russia dated September 10, 2015 No. ММВ-7-11/387);

- amounts of income;

- tax status of a citizen;

- the dates of actual receipt of income, payment of income, tax withholding, as well as the date when the tax withheld from this type of income should be transferred to the budget;

- date and number of the payment order for the transfer of personal income tax to the budget.

This follows from the provisions of paragraph 2 of paragraph 1 of Article 230 of the Tax Code of the Russian Federation.

Please note that the main purpose of the register is to generate indicators for compiling 2-NDFL certificates and 6-NDFL calculations. Therefore, when developing the register, adhere to the structure of these forms, as well as the reference books given in the appendices to the orders of the Federal Tax Service of Russia, which approved these forms.

An example of how to fill out a tax register to calculate personal income tax

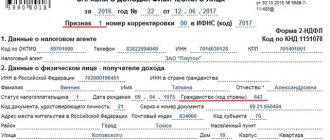

A.S. Kondratyev has been working for the Alpha organization since August 1, 2011. His details: Alexander Sergeevich Kondratiev, citizen of the Russian Federation, date of birth - June 15, 1978, passport series 46 00 No. 462135 issued by the Voikovsky police station in Moscow on November 23, 2000, registered at the address: 125127, Moscow, st. 2-ya Radiatorskaya, 5, building 1, apt. 40, TIN 703254479214.

Alpha details: OKTMO code – 45338000; TIN 7708123456, checkpoint 770801001.

Director – Alexander Vladimirovich Lvov, tel..

Kondratiev has one child, nine years old. An employee receives a standard tax deduction for a child of 1,400 rubles.

During the year, Alpha pays Kondratiev a monthly salary of 15,000 rubles. It is paid twice a month: no later than the 20th day - advance payment (3000 rubles) and no later than the 5th day of the next month - final payment.

On May 16, the organization paid the employee temporary disability benefits on sick leave in the amount of 4,932 rubles. Salary for May – 10,000 rubles.

On June 27, Kondratyev was paid financial assistance in the amount of 6,000 rubles.

From August 15, Kondratiev was given another paid leave for 14 days. On August 10, the accountant calculated and paid vacation pay - 7,200 rubles.

The income accrued to Kondratiev in 2021, deductions, as well as personal income tax amounts are reflected in the tax register.

If a tax agent does not maintain a tax register, he may be punished for gross violation of the rules for accounting for income, expenses and taxable items. Tax and administrative liability is provided for this.

The tax inspectorate will fine the organization 10,000 rubles. If the register has not been maintained for several years, the fine is 30,000 rubles. At the same time, if the tax base has been underestimated, the fine is more serious: 20 percent of the amount of unpaid tax, but not less than 40,000 rubles.

Such liability measures are contained in Article 120 of the Tax Code of the Russian Federation.

If you do not provide the registers at the request of the tax inspectorate, you will be prosecuted under Article 126 of the Tax Code of the Russian Federation. Fine amount:

- 200 rub. for each document that was not submitted on time;

- 10,000 rub. for refusal to hand over documents and information.

In addition, at the request of the tax inspectorate, the court may fine officials of the organization (for example, the manager) in the amount of 300 to 500 rubles. (Part 1 of Article 15.6 of the Code of Administrative Offenses of the Russian Federation).

Mandatory details of the tax accounting register for personal income tax

An enterprise accountant must clearly understand how to maintain tax registers for calculating personal income tax. The main purpose of this list is to formulate the indicators necessary for promptly and accurately filling out a certificate of income for an individual, and therefore the following details and information should be reflected in the personal income tax register form:

- Basic information about the organization - tax agent:

- TIN, checkpoint;

- code of the Federal Tax Service with which the organization is registered;

- name of company.

- TIN;

- FULL NAME.;

- type and details of the identity document;

- Date of Birth;

- citizenship;

- address of residence in the Russian Federation;

- address in the country of residence.

- Taxpayer status (resident or non-resident).

Residents are recognized as individuals who stay in the Russian Federation for at least 183 calendar days over the next 12 consecutive months (Clause 2 of Article 207 of the Tax Code of the Russian Federation). The tax rate that will be applied to his income depends on the status of the person. For example, remuneration under an employment contract of a citizen of the Russian Federation is taxed at a rate of 13%, and the income of a non-resident individual under the same contract must be taxed at a rate of 30%, with the exception, for example, of the income of highly qualified non-resident specialists.

For more information about the correct determination of status, see the material “How to correctly determine the period required to give a citizen the status of a tax resident”.

Basic information ↑

Personal income tax is a tax that ranks next after profit tax and VAT. Therefore, it is worth understanding all the nuances of taxation.

Let's consider who, when and how should calculate the amount of tax and pay it to the budget. Let's turn to the regulatory framework, which contains all the necessary data.

Tax Basics

Personal income tax is a tax on the income of an individual, which is a direct payment made by the population of the Russian Federation.

Payers of this tax are citizens of Russia and other persons who receive profit within Russian territory (foreigners and stateless persons).

Payers can be residents and non-residents. The rate used in income tax calculations will depend on your status.

It is possible to determine whether a person is a resident or non-resident by calculating the number of days of stay in the Russian Federation. If the total number for 12 months exceeds 183, the person is considered a resident (Article 207 of the Tax Code).

Object of taxation:

| Profit from a source located within the state or abroad | For residents |

| Profit from a source located within the Russian Federation | For non-residents (Articles 208, 209, 217 of the Tax Code of the Russian Federation) |

Article 217 also contains a list of types of profit that are not taxed. Personal income tax can be paid by individuals themselves or their tax agents.

An agent is a company, individual entrepreneur, notary, lawyer, or a separate division of a foreign enterprise operating within the Russian Federation from which profit is received.

Calculations of personal income tax are carried out by the tax agent on an accrual basis at the end of each month.

Tax base – receipt of profit in money or in kind, which may be reduced by a tax deduction provided for in Art. 218, 219, 219.1, 220, 221 NK.

Deductions are allowed only in cases where income is subject to personal income tax at a rate of 13%. In other situations, benefits of this type are not provided (Articles 210, 211, 212, 213, 214 of the Tax Code).

Let's list the possible rates (Articles 217, 214 of the Tax Code):

| 9% | When calculating amounts from dividend payments made to residents |

| 13% | The general rate used by residents, as well as foreign highly qualified specialists (regulatory document of Russia dated July 25, 2002 No. 115-FZ) |

| 15% | From dividends received by non-residents |

| 30% | When calculating the amount of tax by non-residents who received profit within the territory of Russia |

| 35% | When receiving a prize, gift, winnings, etc. |

Deadlines for transferring calculated taxes:

| For tax agent | No later than the day when funds are received from banks for payments to the employee; no later than the next day after payment is made to an individual |

| For persons who are not tax agents | On the 15th of July, October and January of the following year after the end of the tax period |

Payment is made to the territorial tax office where the company is registered, or where the payer himself lives (when transferring personal income tax for himself).

Required Documentation

Tax agents and individual individuals must submit a declaration drawn up in Form 3-NDFL.

Citizens must submit this type of reporting in two cases:

- when there is a need to independently calculate and transfer personal income tax amounts to government agencies (when receiving income from the sale of property, winnings, as well as in relation to income from which tax was not withheld by the agent);

- if you wish, receive tax deductions, that is, reimburse part of the tax paid from the budget.

The declaration must be submitted by the end of April next year after the end of the tax period. Forms may be filled out electronically or by hand.

In addition to the declaration, it is necessary to prepare the following certificates:

- 2-NDFL - a form that reflects the income of a specific employee that was received during the tax period. If such a report is not submitted in a timely manner, the person will pay a fine under Art. 126 NK. In case of violation of the filing procedure or distortion of information in the document, the rules described in Art. 15.6 Code of Administrative Offences. The obligation to prepare 2-personal income tax must be fulfilled by the tax agent who transfers the amount of earnings or other funds to the employee.

- If a citizen wishes to receive a child deduction, it is worth submitting a corresponding application (Letter dated September 5, 2012 No. 03-04-05/8-1064).

- Application for refund of overpaid tax (if necessary).

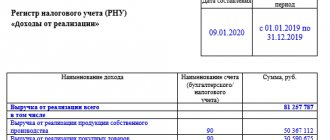

- Tax register is a document that reflects the income of the personal income tax payer, the amount of taxes withheld from him, and the deductions provided.

This is interesting: Labor benefits for a parent with many children in Russia

Normative base

According to Art. 230 clause 1 para. 1 of the Tax Code, tax agents must maintain a tax register to carry out personal income tax calculations.

The income that a citizen who is not a tax agent received when selling property or property rights is also indicated.

The same applies to individual entrepreneurs (Article 226, paragraph 2, Article 227, Article 228 of the Tax Code). The same is stated in the document of the Ministry of Finance dated December 29, 2010 No. 03-04-06/6-321.

If a company does not keep records of an employee’s income using a tax register, a representative of the authorized body will issue a fine of 1 thousand rubles.

In cases where violations have been recorded for several years in a row, the fine may be 30 thousand.

If violations lead to an underestimation of the tax base, the amount of the fine will be calculated as 20% of the underpaid personal income tax, but not less than 40 thousand (Article 120 of the Tax Code of Russia). Officials will be fined 300-500 rubles.

Frequency of preparation of the tax accounting register for personal income tax

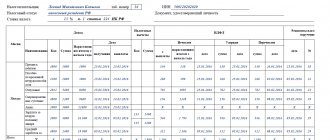

A special place in the form of the tax accounting register for personal income tax is occupied by data on income on which tax is calculated. They are formed in the document by types and deductions with the assignment of the corresponding code.

When assigning a code, you must refer to the order of the Federal Tax Service of Russia “On approval of codes for types of income and deductions” dated September 10, 2015 No. ММВ-7-11 / [email protected] , where each type of income is assigned a corresponding code. For example, when indicating a salary, code 2,000 is used, and if a deduction is provided for the first child under 18 years of age, code 126 is indicated.

A separate register is maintained for each employee. It indicates all payments made, even if the tax percentage rate differs (from 13 to 35%). But they are all reflected separately, for example in different sections of the document. A similar system is used in 2-NDFL certificates, in which each rate has its own section.

The frequency of the personal income tax register is established by the taxpayer. As a rule, a personal income tax register for an employee is opened every year so that income to which a 13% rate is applied, as well as tax deductions, are reflected in it both monthly and on an accrual basis from the beginning of the year. Income to which other rates apply is sufficient to indicate only monthly.

Income that is not subject to personal income tax may not be included (for example, maternity benefits).

Income, the amount of which is limited when calculating personal income tax, must be indicated in the register to monitor compliance with such a limit. One of such income is material assistance, which will not be subject to personal income tax until its amount reaches RUB 4,000.00. per year (clause 28 of article 217 of the Tax Code of the Russian Federation).

What is form 6-NDFL

From 01/01/2016, tax agents are required to fill out a new reporting form - 6-NDFL, which was approved by order of the Federal Tax Service of the Russian Federation dated 10/14/2015 No. ММВ-7-11 / [email protected] (in the same document you can find the procedure for filling it out).

From 2021, regardless of the form of reorganization, the successor is obliged to submit a 6-NDFL calculation for the reorganized organization if it has not fulfilled this obligation (Clause 5 of Article 230 of the Tax Code of the Russian Federation, Law dated November 27, 2017 No. 335-FZ). In order to implement this obligation, form 6-NDLF was adjusted by order of the Federal Tax Service dated January 17, 2018 No. ММВ-7-11/ [email protected] It is officially used starting from March 26, 2018.

6-NDFL current form can be found here.

What are the features of this report:

- 6-NDFL is filled out not in the context of data for each taxpayer, but for all individual taxpayers to whom income was paid by the tax agent as a whole (clause 1 of Article 80 of the Tax Code of the Russian Federation).

- Data on income withheld and paid to individuals is recorded on an accrual basis from the beginning of the year (clause 1 of Article 230 of the Tax Code of the Russian Federation).

- Delivery frequency is quarterly.

- The basis for filling out the form is tax accounting data contained in the registers (Clause 1, Article 230 of the Tax Code of the Russian Federation).

For information on where and how to fill out this form online, read the article “Is it possible to fill out form 6-NDFL online?” .

What day is considered the date of payment of income and what is the deadline for paying personal income tax?

The last day of the month for which the salary was accrued is recognized as the actual date of its receipt (Article 223 of the Tax Code of the Russian Federation). If the employment relationship is completed on a day that is not the last in a given month, then the date of receipt of salary will be the last day of going to work.

When reflecting vacation pay amounts, you must follow the instructions of the letter of the Ministry of Finance of the Russian Federation dated 06.06.2012 No. 03-04-08/08-139: the date of receipt will be the day of payment. It is advisable to use this approach when indicating the date of payment of benefits for sick leave. Transfer personal income tax to the budget from vacation and sick leave benefits in accordance with clause 6 of Art. 226 of the Tax Code of the Russian Federation should be no later than the last day of the month in which these payments were made.

On the issue of determining the date of income in the form of vacation pay, see the material.

Labor legislation obliges employees to pay wages at least every half month (Article 136 of the Labor Code of the Russian Federation). But, despite the advance received, the employee does not generate income, and the obligation to the budget is formed on the last day of the month, so the date of transfer of the advance does not need to be reflected.

See here for details.

In paragraph 6 of Art. 226 of the Tax Code of the Russian Federation states that the organization is obliged to transfer the withheld personal income tax no later than the next day after the date of repayment of the debt to employees.

According to the new regulations of the Federal Tax Service, bonuses should be divided into labor and one-time bonuses. The date of receipt of income will be different for each, therefore, the deadline for transferring personal income tax is set separately.

Read about the nuances here.

General rules for maintaining a register

RULE 1. A separate register must be created annually for each employee. 216, paragraph 1, art. 230 Tax Code of the Russian Federation. It must reflect all income paid to the employee, regardless of the rate at which they are taxed. Income taxed at different rates (9, 13, 15, 30 or 35%) must be reflected separately, for example, in different sections of the register. 1, 3 tbsp. 226, art. 224, paragraph 1, art. 230 Tax Code of the Russian Federation. By the way, this is exactly the principle that applies when filling out 2-NDFL certificates (for each rate - separate sections 3-5) section. II Recommendations.

RULE 2. In the register, all income paid to the employee, taxed at a rate of 13%, and deductions provided are reflected both monthly and on an accrual basis from the beginning of the year. After all, personal income tax on these incomes is calculated on an accrual basis from the beginning of the year based on the results of each month, minus personal income tax withheld in the previous months of the current year. 3 tbsp. 226 Tax Code of the Russian Federation.

But income taxed at other rates can only be reflected monthly. In this case, personal income tax is calculated separately for each amount of income without providing deductions. 3, 4 tbsp. 210, paragraph 3 of Art. 226 Tax Code of the Russian Federation.

RULE 3. If an employee was hired not from the beginning of the year, then the following information can be indicated at the beginning of the register.

| Amount of income taxed at the rate of 13% at the previous place of work, rub. |

The amount of income is taken from the 2-NDFL certificate from the previous place of work. 3 tbsp. 218 Tax Code of the Russian Federation. This information is needed to decide whether to give the employee deductions for children or not. After all, if income from the beginning of the year exceeds 280,000 rubles, then deductions are no longer provided. 4 paragraphs 1 art. 218 Tax Code of the Russian Federation.

If the employee has the right to child deductions, then it is better to make another sign at the beginning of the register.

| F. and. O. baby | Date of Birth | Child category (first, second, third, etc., disabled) |

It will immediately be clear from which month you should start providing deductions and when to stop doing so, what deduction amount to provide and what deduction code to assign.

RULE 4. The register does not have to reflect income that is not subject to personal income tax in full, for example, maternity benefits, monthly child care benefits up to one and a half years old. 217 Tax Code of the Russian Federation.

But income that is not subject to personal income tax within the established limit (for example, daily allowances over 700 rubles, material assistance and gifts taxable in excess of 4,000 rubles per year, etc.) must be reflected in the register. 3, 28 art. 217 Tax Code of the Russian Federation; Letter of the Ministry of Finance dated July 20, 2010 No. 03-04-06/6-155. Moreover, in the register, income must be reflected in the full amount, and the deduction code must be indicated for the non-taxable amount. Letter of the Ministry of Finance dated 03/02/2012 No. 03-04-06/9-54.

RULE 5. If an organization has separate divisions, then tax registers for personal income tax must be maintained in each OP separately.

And if an employee simultaneously receives income from both the GP and the OP, then two personal income tax registers must be opened for him. In this case, for the correct calculation of personal income tax, it is more convenient to provide deductions for children in one place - either in the state enterprise or in the OP.

It is necessary to maintain registers in each OP so that there are no problems with the transfer of personal income tax and the submission of 2-personal income tax certificates. After all, personal income tax withheld from the income of employees of an individual enterprise must be transferred to the budget precisely at the location of each individual enterprise. 7 tbsp. 226 Tax Code of the Russian Federation. And as the Ministry of Finance and the Federal Tax Service have repeatedly explained, 2-personal income tax certificates must be submitted to where personal income tax is transferred. Letters of the Federal Tax Service dated May 30, 2012 No. ED-4-3/ [email protected] ; Ministry of Finance dated 08/07/2012 No. 03-04-06/3-222, dated 03/23/2012 No. 03-04-08/8-58. That is, 2-NDFL certificates on the income of SE employees must be submitted to the Federal Tax Service at the location of the SE, and 2-NDFL certificates on the income of SE employees - to the Federal Tax Service at the location of OPrazd. II Recommendations.

RULE 6. Personal income tax amounts are reflected in the register in whole rubles, and all other amounts are reflected in rubles and kopecks. 4 tbsp. 225 Tax Code of the Russian Federation.

RULE 7. It is better to approve the personal income tax register form by order of the manager.

Personal income tax register form: where is 2020, sample and example of how to fill it out

Taking into account the requirements described in this article, it is recommended to create your own sample of filling out the tax accounting register for personal income tax. It should reflect all the information necessary for the correct calculation of personal income tax for a specific employee.

We recommend the personal income tax register for 2021 at the following link.

This document is taken as a basis and then used not only for the 2-NDFL certificate, but also for calculating 6-NDFL.

In addition to the form itself, taxpayers can register the personal income tax tax register for 2021 on our website. It was created for the calculation of 6-NDFL and gives an idea of the rules for filling out the document. You can download it from this link.

ConsultantPlus experts explained how a tax agent should reflect a professional deduction in the personal income tax register. Get trial access to the system and upgrade to the Ready Solution for free.

Tax registers

All tax agents performing their duties in relation to employees to transfer personal income tax amounts to the budget are required to maintain tax registers.

In most cases, all registers are contained in computer accounting programs. However, not all companies and entrepreneurs keep records automatically. As a result, there is a need to use tax registers of a different format.

All tax agents are given the right to develop and independently approve income tax registers. The accepted sample tax register of companies and entrepreneurs must be approved by order of the head.

However, before drawing up a register, it is necessary to determine for what purpose tax authorities strongly recommend using them when making payments to personnel:

- To correctly calculate personal income tax, which should be withheld from employee income.

- Using the information provided in the registers, you can generate certificates in form 2-NDFL, which the Federal Tax Service inspectorate requires to be provided at the end of each one.

- If tax officials, when conducting an on-site audit, require registers for inspection, the tax agent will be able to provide them and thereby avoid penalties from the inspectorate.

Despite the fact that personal income tax agents have the opportunity to draw up registers on their own, taking into account the needs of their accounting system, this document must include mandatory details. Details that must be included in the register include:

- Information about income tax payers, that is, employees of the employer acting as a tax agent for personal income tax (TIN, full name, passport details). Reflecting this information in this document will save time on preparing the 2-NDFL tax report.

- Taxpayer category (tax status).

- The basis for paying the tax, that is, what types of income were received by the employee.

- Tax deductions for income taxes.

- Total values of income and deductions.

- Dates the employee received income.

- Income tax withholding date.

- Date of transfer of tax to the federal budget.

- Details of the payment order for the transfer of tax payments.

Having decided what information must be provided by the income tax register, you should proceed to filling it out directly. The tax agent has the right to draw up this document in both paper and electronic form.

When compiling personal income tax registers, it is necessary to be guided by rationality. Federal Tax Service employees recommend assigning responsibility for entering tax information into registers to responsible persons. It is the signatures of these employees that must certify the information indicated in the tax document.

Having organized high-quality income tax accounting and developed a tax accounting register, authorized persons are obliged to organize storage systems for this document, allowing not only to keep the register intact, but also to prevent unauthorized adjustments by third parties.

In the event that a specific situation still requires making any adjustments to the information contained in the register, only the responsible employee has the right to do this, indicating the date of the amendments, signature and necessary comments.

Results

Thus, the main tasks in developing a tax register for personal income tax in 2021 are to fully reflect reliable information and group indicators to obtain analytical data. A sample personal income tax register developed by our specialists for 2020 can serve as a guide for the enterprise.

Sources: Tax Code of the Russian Federation

You can find more complete information on the topic in ConsultantPlus. Free trial access to the system for 2 days.