Personal income tax: payment deadline for sick leave in 2020-2021

According to paragraph 1 of Art.

217 of the Tax Code of the Russian Federation, temporary disability benefits should be subject to income tax. However, there is also a rule based on which personal income tax is not withheld from maternity benefits, despite the fact that sick leave is issued in this case too. All deadlines that the employer must comply with when issuing sick leave and payments for them are defined in the law “On compulsory social insurance in case of temporary disability and in connection with maternity” dated December 29, 2006 No. 255-FZ (clause 1, article 15) .

Important! Starting from 2021, the employer calculates and pays benefits only for the first three days of illness and withholds personal income tax from this amount. The employee receives the rest directly from the Social Insurance Fund. The fund withholds the tax from its part. You will find a reminder on the new rules for working with benefits on our website. Further in the article, the PVN is the entire amount of benefits for payments in 2021, and payment for the first 3 days of illness is for 2021.

You can view a sample of filling out a sick leave certificate when paying for sick leave in a new way in ConsultantPlus. Trial access to the system is provided free of charge.

Now let’s move on to the actual reflection of sick leave in 6-NDFL.

On the day when income in the form of personal income tax is actually paid, it is considered received for personal income tax purposes (subclause 1, clause 1, article 223 of the Tax Code of the Russian Federation) and personal income tax is calculated and withheld from it (clauses 3, 4 of article 226 of the Tax Code of the Russian Federation) ). Thus, there is a fundamental difference between personal income tax and salary in determining the date of receipt of income for reflection in form 6-NDFL:

- for wages, it corresponds to the last day of the month for which it was accrued (clause 2 of Article 223 of the Tax Code of the Russian Federation);

- for PVN it coincides with the day of payment, and the fact that the actual calculation of the benefit amount was made earlier does not matter (letter of the Federal Tax Service of Russia dated January 25, 2017 No. BS-4-11 / [email protected] , dated August 1, 2016 No. BS- 4-11/13984).

The tax payment deadlines will also be different (clause 6 of Article 226 of the Tax Code of the Russian Federation):

- Salary taxes must be transferred on the next working day following payment;

- for payment of tax on personal income tax, the deadline corresponds to the last day of the month of benefit payment.

Thus, the personal income tax can be paid simultaneously with the payment of wages (i.e., with its payment for the 1st or 2nd half of the month), but the dates of receipt of income and the deadlines for paying tax on benefits and wages will be determined according to different principles.

ConsultantPlus experts explained how to reflect various payments in 6-NDFL. Get free trial access to the system and move on to the Ready-made solution.

To learn how it is legitimate to call a salary paid for the first half of the month an advance, read the article “How an advance is paid - new rules and payment procedures.”

In what cases is sick leave reflected in 6-NDFL?

The amounts of accrued benefits for temporary disability are subject to inclusion in the 6-NDFL declaration. Exceptions include maternity benefits, which are not subject to income tax. It is important to remember that the date of receipt of income on sick leave in 6-NDFL is the day the money is transferred to the employee, in contrast to wages, for which such a date coincides with the last day of the month. The organization must pay the tax by the end of the month, otherwise, during the inspection, the Federal Tax Service will charge penalties.

How to fill out sick leave according to the new rules

From December 14, you need to work with sick leave in a new way!

The rules were changed by Order of the Ministry of Health No. 925n dated September 1, 2020. ConsultantPlus experts have prepared an overview of the amendments and new instructions. Use it for free.

Rules for filling out lines 6-NDFL: reflecting operations for processing sick leave

We will show you how to reflect sick leave in 6-NDFL, linking the actions taken to the lines of the report form for 2021.

Important! ConsultantPlus warns With reporting for the first quarter of 2021, you need to submit a 6-NDFL calculation using a new form. As part of it, you need to submit a certificate of income and tax amounts of an individual (now it is 2-NDFL). In the appendix to the order approved by the Federal Tax Service, there is also a form of income certificate that is issued to employees. More information about all changes in forms 6-NDFL and 2-NDFL from 2021 can be read in the Review from ConsultantPlus. Trial access to the system is provided free of charge.

| Line | Action | Deadline | Norm of the Tax Code of the Russian Federation |

| 020 | We accrue income | On the day of payment | Art. 223 |

| 040 | We calculate personal income tax | On the day of payment | Clause 3 Art. 226 |

| 100 | Worker receives money | On the day of payment | Art. 223 |

| 070, 110 | We withhold personal income tax | On the day of payment | Clause 4 art. 226 |

| 120 | We transfer personal income tax to the budget | The last day of the month in which funds were paid. If it coincides with a weekend, it is transferred to the next working day (Clause 7, Article 6.1 of the Tax Code of the Russian Federation) | Clause 6 Art. 226 |

Personal income tax on benefits: we withhold and transfer

The benefits of residents of the Russian Federation are subject to personal income tax at a rate of 13%, non-residents of the Russian Federation - at a rate of 30%.

The tax is withheld directly upon the actual payment of income to the employee, i.e. when the sick leave benefit is transferred to his bank card or issued from the enterprise's cash desk (clause 4 of Article 226 of the Tax Code of the Russian Federation, clause 1 of clause 1 of Article 223 of the Tax Code of the Russian Federation).

But personal income tax is transferred to the budget no later than the last day of the month in which benefits were paid (paragraph 2, clause 6, article 226 of the Tax Code of the Russian Federation). That is, the tax can be accumulated during the month, and at the end of the month it can be paid to the budget in a single amount.

Note! Personal income tax from wages is transferred maximum the next day after settlements with personnel for wages (paragraph 1, clause 6, article 226 of the Tax Code of the Russian Federation).

That is, despite the fact that sick leave is paid along with salary , each of these types of income has its own tax payment deadline. We must reflect this feature in 6-NDFL .

Filling out 6-NDFL with sick leave: example

Let's translate the table into a practical plane and see how actions with sick leave will be reflected in 6-NDFL, in specific figures.

Example 1

An employee of the organization was ill from October 12 to October 25, 2021. He began performing his work duties on October 26 and on the same day he gave his sick leave to his accountant.

Based on the results of the calculations, on October 26, 2020, he was awarded an allowance in the amount of 24,500 rubles. The payment was made on the next day of payment of wages - November 10 of the same year.

All these actions will be reflected in the report for the 4th quarter of 2021 (that is, the annual report) and in relation to its lines will look like this.

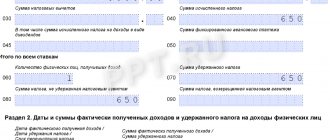

In section 1, the manual will include the following lines:

| Line | Meaning |

| 020 | 24 500 |

| 040 | 3 185 |

| 070 | 3 185 |

And in section 2 it will be reflected like this:

pp. 100 - 11/10/2020;

pp. 110 - 11/10/2020;

pp. 120 - 30.11.2020;

pp. 130 - 24,500;

pp. 140 - 3,185.

Features of rolling sick leave: reflected in the 6-NDFL declaration

Differences in income recognition procedures result in:

- Salary data, as a rule, turns out to fall into different months, since it is accrued in one month and usually paid in another. At the border of the reporting periods, as a result, salary data for the last month of the reporting quarter will fall into section 1 (i.e., accruals), and in section 2 (by date of payment) will be shown only in the next period.

- Data on military goods most often turn out to be tied to one reporting period. This is due to the fact that the deadline for paying taxes is legally linked to the month of payment of income in the form of benefits.

However, for the terms of payment of sick leave tax, transitions to another month are also possible, including at the border of reporting periods. This occurs in cases where the last day of the month turns out to be a day off. Postponement to the next working day following the weekend (according to the rule established by clause 7 of Article 6.1 of the Tax Code of the Russian Federation) automatically means a shift in the payment deadline to another month, and if this month belongs to the next reporting period, then to another reporting period. This is due to the fact that the date of completion of the income payment transaction is considered to be the last of the dates related to it (letter of the Federal Tax Service of Russia dated July 21, 2017 No. BS-4-11 / [email protected] ).

Thus, if the deadline for tax payment is postponed, the data on personal income tax entered in lines 100–140 of section 2 will appear in the report relating to the next period. But in section 1 they should be shown in the period of actual payment by entering the corresponding figures in lines 020, 040 and 070 (letter of the Ministry of Finance dated March 13, 2017 No. BS-4-11 / [email protected] ).

S. N. Shalyaeva, 1st class State Civil Service Advisor, answered some of the taxpayers’ questions.

Get trial access to ConsultantPlus and find out the official’s answer to this question for free.

Example 2 (conditional)

A company employee was absent from work due to illness from December 17 to December 27. He went to work on December 28 and on the same day he gave his sick leave to the accounting department.

On the same day, he was accrued benefits in the amount of 20,500 rubles. Let’s assume that December 31 is a day off, and the benefit was paid along with the December salary on the last working day - December 30.

The deadline for paying tax on benefits expires on a weekend, so it is postponed to the first working day of the next year, for example, January 11.

This operation will have to be reflected in 2 reports:

- For the current year. There, data on personal income tax will appear only as part of the lines for calculating and withholding tax (in the 2021 form this is section 1, in the 2021 form - section 2).

- For the 1st quarter of next year. Data on personal income tax in this report will be included in the section where personal income tax payable is reflected (in the 2021 form this is section 2, in the 2021 form - section 1).

For an example of reflecting “carryover” vacation pay, for which the same tax payment rules apply as for sick leave, see the article “How to correctly reflect vacation pay in Form 6-NDFL?”

6-NDFL upon dismissal: difficulties of section 2

Filling out 6-NDFL upon dismissal has specifics. Section 1 is filled out in the general order, but Section 2 may have some special features. In particular, due to the fact that for different “dismissal” amounts the Tax Code of the Russian Federation provides for different dates for receiving income or deadlines for paying personal income tax to the budget. Let's try to understand the nuances using the example of 6-NDFL for 2019.

The general procedure for filling out 6-NDFL upon dismissal is described in this article.

Find out more about calculating and paying wages upon dismissal.

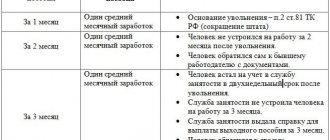

Situation 1. On the day of dismissal, the employee received a salary and compensation for unused vacation

Let's start with a standard situation. As expected, on the last day of work (let it be December 16), you paid the employee a salary of 25,000 rubles. and compensation for vacation 22,000 rubles. The date of receipt of income for salary upon dismissal is the day of dismissal, and compensation for vacation is the day of payment. The deadline for transferring personal income tax for both amounts is the day following the payment. In this case, the dates and deadlines coincide. Therefore, both of these payments can be reflected in one block of lines 100–140 of section 2.

Read more about reflecting compensation for unused vacation in Form 6-NDFL in this article.

Find out also how to calculate compensation upon dismissal.

Situation 2. Along with dismissal pay, the employee was paid sick leave

Let’s add to the first example and assume that on the day of dismissal the employee was still paid for December sick leave in the amount of 7,000 rubles.

We talked about whether sick leave is subject to personal income tax in this article.

The date of receipt of this income will coincide with the above (payment day), but the deadline for paying personal income tax will be different. Therefore, the hospital payment will go to a separate block of lines.

Here you need to keep in mind the following point. 12/31/2019 is a working day. Therefore, sick leave fell into 6-personal income tax for the year. If it had been a weekend, we would have shown it in section 2 already for the 1st quarter of 2021.

See also an example of filling out 6-NDFL for the 1st quarter of 2020 with sick leave.

Situation 3. After dismissal, the employee received a production bonus

By the end of the year, let’s say December 30, 2019, having already been fired, the employee received a bonus for work results in the amount of 40,000 rubles. For personal income tax purposes, such a bonus is equivalent to salary. This means that the date of receipt of income will be the day of dismissal. But the date of deduction of personal income tax and the period for its transfer from salary payments will differ. Therefore, in section 2, the premium must be shown in a separate block of lines 100–140.

Find out more about paying a bonus after an employee leaves.

Situation 4. Salary and vacation compensation were issued on the eve of dismissal

Now let’s assume that the employee in example 1 received his dismissal notice not on the last day of work, but on the day before, December 13, 2019. We remember that for salary, the date of receipt is the day of dismissal, and for vacation compensation, the date of payment. This means that the calculation will also have two blocks of lines 100–140.

NOTE! In this case, personal income tax must be transferred from the salary no later than the day of dismissal.

Situation 5. Salary and vacation compensation were issued late

This also happens. Let’s say the employee received the money only on December 25th. We will not evaluate the employer’s actions from the point of view of violation of the employee’s labor rights. We are interested in the tax aspect and filling out 6-NDFL. Taking into account the difference in the date of receipt of income, there will again be two blocks of lines 100–140.

Look for materials on how other payments to individuals are reflected in 6-NDFL in our section “Calculation of 6-NDFL”.

Sources:

- Tax Code of the Russian Federation

- Order of the Federal Tax Service of Russia dated October 14, 2015 No. ММВ-7-11/ [email protected]

You can find more complete information on the topic in ConsultantPlus. Free trial access to the system for 2 days.

Results

Sick leave payments are reflected in 6-NDFL in the reporting period in which the sick leave was actually paid. A special feature is that personal income tax on such payments is transferred to the budget no later than the last day of the month of payment.

If the last day of the month is a holiday, then the tax payment deadline is shifted to the next month and may fall into the next quarter. In the latter case, data on personal income tax is divided into 2 reports: during the benefit payment period they are entered in section 1, and in section 2 they are shown in the next period.

Sources:

- Tax Code of the Russian Federation

- Federal Law of December 29, 2006 N 255-FZ “On compulsory social insurance in case of temporary disability and in connection with maternity”

You can find more complete information on the topic in ConsultantPlus. Free trial access to the system for 2 days.

Disability payment

If the sick leave benefit is paid by the employer (this happens in most cases), then personal income tax must be withheld from its amount. Sick leave payments are not included in the list of exception payments not subject to income tax. Therefore, tax must be withheld regardless of the reason for which the benefit is assigned.

Let us remind you that sick leave benefits must be assigned within 10 calendar days after the employee brings a correctly completed sick leave certificate to the administration. The benefit must be paid to the employee on the day the salary is issued closest to the day the benefit is assigned (Part 1, Article 15 of Federal Law No. 255-FZ of December 29, 2006).

It is also necessary to act as a tax agent if the employee himself gets sick, or his child gets sick, or the employee is injured, including at the workplace (letter of the Ministry of Finance dated April 29, 2013 No. 03-04-05/14992).

When reflecting sickness benefits, you must adhere to the following algorithm for filling out the form:

- line 100 – date of payment of benefits;

- line 110 – the same date as on line 100;

- line 120 – the last day of the month in which sickness benefits were issued;

- line 130 – the amount of sickness benefits issued;

- line 140 – the amount of personal income tax withheld from the payment on line 130.

Reflecting the situation when sick leave is paid with a salary of 6 personal income tax, you need to remember that the date of receipt of income and the period when personal income tax should be transferred to the budget are different for wages and vacation pay. Therefore, regardless of the fact that the money was issued on the same day, you need to fill out separate blocks of lines 100 - 140 in section 2 of the 6-NDFL calculation.

Read also

17.12.2018