Article updated: November 25, 2021

Author of the article Marina Afanasyeva Tax consultant with 4 years of experience.

Hello. In this article, I analyzed the situations of how and when parents have the right to receive a property tax deduction for their children when purchasing an apartment. Everything was supported by articles of the Tax Code and the official positions of the tax authorities.

Speaking below about parents, I mean those who are indicated on the child’s birth certificate as father or mother and are not deprived of parental rights - Art. 47 and art. 71 RF IC, art. 3 and art. 23 of the Federal Law of November 15, 1997 N 143-FZ. The same rules for receiving deductions apply to adoptive parents, foster parents or guardians of a child who have supporting documents in their hands - clause 6 of Art. 220 Tax Code of the Russian Federation.

A small digression - if you need free legal advice, write online to the lawyer on the right, order a call using the button on the left, or call (24 hours a day, 7 days a week) (Moscow and the region); (St. Petersburg and region); 8 (all regions of the Russian Federation).

→Find out for free what deductions you are entitled to and how much money you can return. Specialists from ReturnNalog.ru will figure out what deductions you are entitled to, calculate them, prepare documents and submit them to the tax office within 24 hours. Accompaniment until receiving money.VerniteNalog.ru

First, you should understand the types of deductions and their limitations, then you will understand whether it makes sense for parents to receive a deduction for their child.

Tax deduction for home purchase by one parent and child

According to paragraph 6 of Art. 220 of the Tax Code of the Russian Federation , a parent who bought an apartment as a property with his minor child has the right to receive a property deduction not only for his share of the apartment, but also for the child’s share of the apartment.

This position is also supported by previous letters from the Ministry of Finance of Russia: dated 08/20/2013 N 03-04-05/33942, dated 02/17/2012 N 03-04-05/7-194, dated 07/19/2011 N 03-04-05/7- 523, dated July 19, 2011 N 03-04-05/7-521.

Example: Petrova A.A.

I bought an apartment worth 2 million rubles for myself and my 10-year-old son (1/2 share each). Despite the fact that half of the apartment is registered in the name of her son, Petrova has the right to receive a property deduction in the amount of the full cost of the apartment - 2 million rubles.

On the right of parents to distribute deductions for children

No one can transfer their deduction, including a child to their parents. This is not provided for by tax legislation - letter of the Ministry of Finance dated 09/07/2012 N 03-04-05/7-1090.

Parents have the right to distribute deductions for their children’s shares to themselves, thereby increasing their deductions - clause 6 of Art. 220 Tax Code of the Russian Federation. By default, deductions are distributed among owners according to the size of their shares in the property. Parents have the right to distribute in any proportion all amounts of expenses incurred for the purchase + payment of mortgage interest. Accordingly, get the maximum amounts for them. The main thing is that the child is under 18 years old at the time of purchasing the apartment.

Below I will analyze individual situations and in each I will describe how and in which documents deductions can be divided. Since it is allowed to return a maximum of 260,000 rubles, up to 2,000,000 rubles of purchase expenses can be distributed per parent.

You cannot distribute the deduction to the parent who previously received it, because he has spent his right. For example, a parent returned the maximum 260,000 rubles from another property. This means that the deduction for the child’s real estate cannot be distributed to him - clause 10 of Art. 220 of the Tax Code of the Russian Federation, Resolution of the Constitutional Court dated March 1, 2012 N 6-P and letter of the Ministry of Finance dated March 16, 2015 N 03-04-05/13747.

When distributing deductions to parents, the child does not lose his right to deduction - he can receive it for other real estate purchased by him after the age of 18 (letter of the Ministry of Finance dated September 3, 2015 N 03-04-05/50743). A child cannot count on deductions for real estate that was purchased in his name before the age of 18, even when his part was not distributed to his parents. After all, at that moment he could not bear the costs of the purchase and payment of mortgage interest; they were borne by his parents - Art. 60 RF IC, Art. 26 and Art. 28 Civil Code of the Russian Federation. It's easier to understand with the examples below.

SHOW EXAMPLES ↓ Example No. 1: Spouses Vladimir and Marina bought an apartment in 2019 for 3,000,000 rubles. The apartment was registered as shared ownership for three people - 1/3 for each spouse and 1/3 for their minor daughter Daria. The parents distributed the deduction between all the expenses for the purchase, so they received the entire deduction amount - for themselves and for their daughter’s share. Daria will not lose her entire right to deduction - she will be able to return 13% from other purchased real estate.

Example No. 2: Spouses Alexander and Svetlana bought an apartment in 2021 for 4,000,000 rubles. The apartment was registered as shared ownership for three people - 1/3 for each spouse and the same share for the minor son Artem. Both parents received deductions from other properties, so expenses cannot be allocated to them. They have lost their right.

Artem got a job at 22 and started paying personal income tax. He still will not be able to return the personal income tax for the 1/3 share of the apartment purchased in his name in 2021. The deduction is returned for the costs of purchasing real estate. Artem, due to his age, did not bear these expenses. The expenses were borne by the parents. He has the right to return 13% from other properties he purchased.

Income and expenses in the family are considered common, therefore real estate purchased during marriage is considered the common property of both spouses, even when it is registered in the name of one of them - Art. 33 and Art. 34 RF IC, art. 256 of the Civil Code of the Russian Federation. Exception: if before the transaction a marriage contract was drawn up, according to which the spouses agreed to separate property, the second spouse will not be able to count on a refund of the deduction for the share of the first spouse, because has nothing to do with this real estate - clause 1 of Art. 42 IC RF.

According to the standard, for real estate purchased during marriage, spouses can also distribute the deduction among themselves - details. Up to 100% deduction for one spouse. You cannot distribute the deduction to the spouse who previously received it from other real estate.

→Find out for free what deductions you are entitled to and how much money you can return. Specialists from ReturnNalog.ru will figure out what deductions you are entitled to, calculate them, prepare documents and submit them to the tax office within 24 hours. Accompaniment until receiving money.VerniteNalog.ru

Situation No. 1 - the apartment was purchased by one parent with a child

When purchasing an apartment while not married, the parent-owner can distribute deductions for the child’s share to himself, thereby increasing the amount of his deductions - clause 6 of Art. 220 of the Tax Code of the Russian Federation, letter of the Ministry of Finance dated August 20, 2013 N 03-04-05/33942.

The law does not establish how to document the distribution, so this remains at the discretion of the heads of district tax inspectorates. Most often, it is enough for a parent to indicate the entire amount of purchase expenses in a regular application for a deduction - or a sample. Also, in the 3-NDFL declaration, he must indicate code 14 - Order of the Federal Tax Service of October 3, 2018 N ММВ-7-11 / [email protected] Somewhere in addition to the above statements, they will also require a free-form application for distribution - or a sample.

If the apartment was purchased during marriage, both spouses can distribute deductions among themselves for both the child’s share and the share of the owner-spouse. For example, the first owner spouse receives a deduction for his share, and the second non-owner spouse receives a deduction for the child's share. The main thing is to calculate everything correctly. Examples to help.

Parents only need to submit a standard application for the distribution of deductions among themselves. For purchase costs - or a completed sample, for mortgage interest payments - or a completed sample. An additional application for the distribution of the child's share deduction between the parents is not required.

SHOW EXAMPLES ↓ Example No. 1: Marina bought an apartment for 3,000,000 rubles. No mortgage, not married at the time of purchase. She registered the apartment as shared ownership for herself and her minor daughter, 1/2 each. Marina can distribute the deduction for the child’s share to herself. In the application, she needs to indicate that her expenses amounted to 3,000,000 rubles, but she will receive a maximum of 260,000 rubles. No one can receive more than this amount, neither for themselves nor for their child. Her daughter does not lose the right to deduct when purchasing other real estate after 18 years.

Example No. 2: Svetlana bought an apartment for 2,700,000 rubles. At the time of purchase I was not married. She registered the apartment as shared ownership - 2/3 for herself and 1/3 for her minor daughter. Svetlana previously received the maximum 260,00 rubles for other real estate. Under this apartment, she will not be able to return income tax either for herself or for her daughter, because she has already spent her right.

Example No. 3: Spouses Dmitry and Olga bought an apartment in 2021 for 3,800,000 rubles. The apartment was registered as shared ownership - 2/3 for Dmitry and 1/3 for two minor children. The spouses had never received a deduction before. I remind you that the maximum you can return is 260,000 rubles.

Since the property was purchased during marriage, the spouses can distribute among themselves not only the deduction for the children’s shares, but also for Dmitry’s share. The spouses indicated in the application for distribution that each had expenses of 1,900,000 rubles. As a result, they will receive 247,000 rubles each. Or Dmitry’s expenses were 2,000,000 rubles, and Olga’s were 1,800,000. Then he will receive the maximum 260,000 rubles, and she will receive 234,000.

Example No. 4: Spouses Sergey and Olga bought an apartment in 2021 with a mortgage for 5,500,000 rubles. The apartment is in shared ownership - 5/6 for Olga, 1/6 for her minor son. The spouses had not previously received deductions.

Deduction for purchase: Spouses can distribute the deduction between themselves for the child’s share and for Olga’s share. After all, the apartment was bought during marriage. In the statement they indicated this: the cost of the purchase from Sergei was 2,750,000 rubles, and the same from Olga. Each of them will receive a maximum of 260,000 rubles.

Mortgage deduction: spouses can distribute the cost of paying mortgage interest in any proportion - 50 to 50, 60 to 40. Up to 100% for the first spouse and 0% for the second.

Example No. 5: Spouses Artem and Svetlana bought an apartment in 2021 for 3,800,000 rubles. They used maternity capital of 616,000 rubles. The apartment was registered as shared ownership for three people - 2/3 for Artem and 1/3 for two minor children. Svetlana wrote a refusal to receive a share. A deduction is not issued for the amount of financial capital, so it will be calculated from the amount of 3,800,000 - 616,000 = 3,184,000 rubles.

Spouses can distribute the deduction among themselves for Artem's share and for the children's shares. The application for distribution indicated that each spouse had expenses of 159,200 rubles. As a result, each of them will return 206,960 rubles.

Example No. 6: Spouses Vladimir and Daria bought an apartment in 2021 for 4,500,000 rubles. The apartment is in shared ownership - 5/6 for Vladimir, 1/6 for his minor son.

Vladimir previously received a deduction from other real estate, but Daria did not, so it’s worth distributing the deduction to her. Since you can return a maximum of 260,000 rubles, the application for distribution indicated that Daria’s expenses amounted to 2,000,000 rubles, and Vladimir’s expenses amounted to 2,500,000. Or all 4,500,000 rubles can be indicated as expenses for Daria, but she will still return only 260 000.

Example No. 7: Spouses Vladislav and Sophia bought an apartment in 2021 for 3,300,000 rubles. The apartment is in shared ownership - 5/6 for Vladislav and 1/6 for his minor son. Before the purchase, the spouses signed a prenuptial agreement, which established a separate ownership regime for the property.

Vladislav previously received a deduction from other real estate, but Sophia did not. Since there was a prenuptial agreement, Sophia will not be able to receive a deduction for Anton’s share, but only for her son’s share. That is, she can return only 13% * (3,300,000 * 1/6) = 71,500 rubles. Therefore, in the application for distribution they indicated that her expenses amounted to 550,000 rubles, the rest from Vladislav. Or all 3,300,000 rubles can be indicated as expenses for Sophia, but she will still return only 71,500 rubles for her son’s share.

Example No. 8: Spouses Anton and Elena bought an apartment in 2013 for 2,600,000 rubles. The apartment was registered as shared ownership for two people - 1/7 for the child and 6/7 for Elena. No one had received a deduction before and only recently learned of their right.

Since the apartment was purchased before 2014, the maximum 260,000 rubles are distributed to the entire apartment, and not to each owner. Spouses can distribute the deduction among themselves equally or in a different proportion, at least entirely to one of them. Still, they can return a maximum of 260,000 rubles.

Situation No. 2 - the apartment was purchased by both parents and a child

Parents can distribute deductions for the child’s share among themselves in any proportion or in full to one of them - letter of the Ministry of Finance dated March 14, 2013 N 03-04-05/7-223.

Now, when spouses register the purchased property as shared ownership, they are required to have a prenuptial agreement or a notarized purchase and sale agreement with elements of a prenuptial agreement - Art. 256 of the Civil Code of the Russian Federation. In this situation, spouses can receive a deduction only according to the size of their shares + distribute the deduction among themselves for the child’s share. If there was no prenuptial agreement at the time of purchase (this was previously allowed), then the spouses can distribute among themselves in any proportion both the deduction for the child’s share and for their own shares. It's easier to understand with examples.

Parents submit an application for the distribution of deductions among themselves in the established form. For the costs of purchasing real estate - or a completed sample, for paying mortgage interest - or a completed sample. An additional application for the distribution of the child's deduction between the parents is not required.

SHOW EXAMPLES ↓ Example No. 1: Spouses Alexander and Marina bought an apartment in 2020 for 3,700,000 rubles. The apartment was registered as shared ownership for three people - 1/3 for each spouse and minor son. Before the purchase, they signed a prenuptial agreement stating that the apartment was subject to the separate property regime. No one has received a deduction before.

Spouses can distribute the deduction among themselves only for the child's share. To do this, they submit a statement that Alexander’s expenses amounted to 1,850,000 rubles, and Marina’s expenses were the same. Each spouse will receive 13% * 1,850,000 = 240,500 rubles. Or Alexander’s expenses amounted to 2,000,000 rubles (he will receive the maximum 260,000), and Marina’s expenses amounted to 1,700,000 rubles (she will receive 221,000).

Example No. 2: Spouses Oleg and Svetlana bought an apartment for 2,900,000 rubles in 2021 with the help of maternity capital. The financial capital was 466,000 rubles. The apartment was registered as shared ownership for four people - 1/4 each for spouses and two minor children. Before the purchase, they signed a prenuptial agreement stating that the apartment was subject to the separate property regime. No one has ever returned a deduction before. You cannot get a deduction for the amount of financial capital; family expenses for the purchase are 13% * (2,900,000 - 466,000) = 2,434,000 rubles.

Each spouse can receive a deduction only for their share + distribute deductions for children among themselves in any proportion. For example, in the application, indicate that each spouse has expenses of 2,434,000 / 2 = 1,217,000 rubles. Then everyone will return 158,210. Or Oleg’s expenses were 2,000,000 rubles (he will return the maximum 260,000), and Svetlana’s expenses were 434,000 rubles (she will return 56,420).

Example No. 3: Spouses Vladimir and Daria bought an apartment in 2021 with a mortgage for 2,500,000 rubles. The apartment is shared ownership for three people - 1/6 for the child and 5/12 for the spouses. Before the purchase, they drew up a prenuptial agreement. None of them had received a deduction before.

Deduction for purchase: Spouses can receive a deduction for their shares + distribute the deduction for the child’s share among themselves in any proportion for both of them or for one of them. For example, in the application, indicate that each spouse has expenses of 1,250,000 rubles. Then everyone will return 162,500. Or Vladimir’s expenses are 2,000,000 rubles (he will return the maximum 260,000), and Daria’s expenses are 500,000 rubles (she will return 65,000).

Mortgage deduction: since a marriage contract has been drawn up, the spouses can distribute the cost of paying interest only according to the size of their shares + distribute the child’s share among themselves. It’s easier for them to distribute all interest costs equally.

Example No. 4: Spouses Grigory and Daria bought an apartment in 2021 for 2,600,000 rubles. We used material capital in the amount of 616,000 rubles. The apartment was registered as shared ownership for four people - 1/10 for a minor son, 1/10 for an adult daughter, 2/5 for each spouse. Before the purchase, a prenuptial agreement regarding the separation of property was drawn up. No one has ever received a deduction before. There is no deduction for the amount of financial capital, so the family’s expenses are 2,600,000 - 616,000 = 1,984,000 rubles.

The deduction for each spouse for their share will be (1,984,000 * 2/5) = 793,600 * 13% = 103,168 rubles. They can also distribute among themselves the deduction for the share of only a minor son, for whom it is (1,984,000 * 1/10) = 198,400 * 13% = 25,792 rubles. For example, equally. Then each spouse will return 103,168 + (25,792 / 2) = 116,064 rubles. They need to indicate in the application that the expenses of each spouse were (1,984,000 - 198,400) / 2 = 892,800 rubles. Of these, 198,400 is the cost of the adult daughter’s share, a deduction for which the spouses cannot return.

Or the spouses can distribute the entire share of the minor son to one of them. For example, on Gregory. Then he will return 103,168 for his share + 25,792 for his son’s share. Total 128,960 rubles. In the application, they need to indicate that his expenses were (1,984,000 * 2/5) + 198,400 = 992,000. Of these, (1,984,000 * 2/5) is the cost of his share, 198,400 is the cost of 1/ 10 of his minor son, which Gregory distributed to himself. And Daria’s expenses (1,984,000 * 2/5) = 793,600 rubles, i.e. the value of her share.

Example No. 5: Spouses Artem and Natalya bought an apartment in 2021 for 4,400,000 rubles. The apartment was registered as shared ownership for three people - the minor daughter 1/8 and the spouses 7/16. They did not draw up a marriage contract.

Artem previously received a deduction for other real estate, but Natalya did not. She can return a maximum of 260,000 rubles, so the application indicated that her expenses amounted to 2,000,000 rubles, and the rest went to Artem.

Example No. 6: Spouses Anton and Elena bought an apartment in 2013 for 2,600,000 rubles. The apartment was registered as shared ownership for three people - 1/7 for the child and 3/7 for the spouses. The spouses did not draw up a marriage contract, because there was no such requirement then. No one had received a deduction before and only recently learned of their right.

Since the apartment was purchased before 2014, the maximum 260,000 rubles are distributed to the entire apartment, and not to each owner. Spouses can distribute the deduction equally or in a different proportion, at least entirely to one of them. Still, they can return a maximum of 260,000 rubles.

Example No. 7: Spouses Dmitry and Olga bought an apartment in 2021 for 4,200,000 rubles. The apartment was registered as shared ownership for four people - 1/4 each for spouses and two minor children. The spouses did not draw up a marriage contract, because there was no such requirement then.

Dmitry previously received a deduction from other real estate, but Olga did not. In this situation, she can return the maximum 260,000 rubles, i.e. deduction for your share and for the shares of your children. In the statement, the spouses indicated that Olga’s expenses for the purchase were 2,000,000 rubles, Dmitry’s were 2,200,000. In principle, they can indicate that Olga’s expenses were all 4,200,000 rubles. It does not change anything. She will still receive only 260,000 rubles.

Tax deduction for the purchase of housing by spouses and their child(ren)

If both spouses purchase an apartment/house/share and register it as joint property with minor children, the parents or one of them can receive a tax deduction for the children’s share.

Both spouses and one of them can increase their deduction at the expense of the child’s share when purchasing housing in common shared ownership . Spouses need to decide for themselves which of them and in what amount will increase their deduction due to the child’s share in the property.

Reason: letters of the Ministry of Finance of Russia dated 03/14/2013 N 03-04-05/7-223, dated 07/05/2012 N 03-04-05/5-845, dated 07/04/2012 N 03-04-05/5-841, dated 07/03/2012 N 03-04-05/5-822, dated 02/01/2012 N 03-04-05/5-101.

The law and letters from the Ministry of Finance do not contain instructions on how parents can distribute the child’s deduction. In this case, an application for the distribution of the child’s deduction between the spouses should be attached to the documents for the tax office. It would also be a good idea to seek advice from the tax office at your place of residence.

Example : Ivanov I.I., his wife Ivanova A.A. and their minor children purchased an apartment worth 4 million rubles in 2021 as common shared ownership (1/4 share of ownership for each). Each owner of a 1/4 share has the right to count on a deduction in the amount of 1 million rubles.

The couple decided that each of them would receive a deduction for the share of one of the children. The tax deduction for the purchase of an apartment will be distributed as follows: Ivanov I.I. – 2,000,000 rub. (for her share and the share of the first child), Ivanova A.A. – 2,000,000 rub. (for your share and the share of your second child);

A deduction for the child’s share can also be claimed when other relatives, in addition to the parents and their minor children, are participants in the common shared ownership of the purchased housing. The letter of the Ministry of Finance dated 06.06.2012 N 03-04-05/9-690 discusses the situation when an apartment was acquired in shared ownership of a child, his father and grandfather.

Example : Ivanov I.I., his brother Ivanov V.I. and a minor child purchased an apartment worth 1,800 thousand rubles in 2021 as common shared ownership (1/3 share of ownership for each).

Ivanov I.I. has the right to receive a deduction not only for his share, but also for the child’s share. The deduction will be distributed as follows: Ivanov I.I. – 1,200 thousand rubles. (for your share and the child’s share); Ivanov V.I. – 600,000 rub. (only for your share);

To receive a property deduction, parents do not require the child’s consent.

Amount and maximum amount of deductions

Article 220 of the Tax Code of the Russian Federation “Property tax deductions”

When purchasing an apartment using a mortgage loan, two deductions are provided - a deduction for purchase costs + for paying mortgage interest. Accordingly, without a mortgage, only a deduction for the purchase. I will analyze each of them.

Deduction for purchase expenses . According to it, you can return 13% of the amount of expenses for purchasing an apartment (its cost) - paragraphs. 3 clause 1. art. 220 Tax Code of the Russian Federation.

There is a maximum size. If the apartment was purchased in 2014 and later, each owner can return a maximum of 260,000 rubles. This is 13% of 2,000,000 - pp. 1 clause 3. art. 220 Tax Code of the Russian Federation. You cannot receive more than this amount - neither for yourself, nor for a child or spouse (more on this below).

When purchasing an apartment before 2014, the maximum 260,000 rubles are distributed to the entire apartment, and not to each owner - para. 17 pp. 2 p. 1 art. 220 of the Tax Code of the Russian Federation in the old version. In 2014, there were changes in tax legislation - Federal Law dated July 23, 2013 N 212-FZ.

No deduction is issued for the amount of maternity capital. I advise you to read - calculation of deductions when using financial capital. Separately, the apartment was purchased with a mortgage and financial capital.

"Mortgage" deduction . Some banks provide a mortgage when purchasing real estate with a child, i.e. The child is immediately allocated a share in the property.

This deduction returns 13% of the cost of paying mortgage interest - paragraphs. 4 clause 1. art. 220 Tax Code of the Russian Federation. Mortgage payments are divided into two amounts—principal and interest. From the paid interest they return 13%.

Maximum amount: When purchasing an apartment from 2014 and later, each owner can return up to 390,000 rubles, i.e. 13% of 3,000,000 - clause 4 of Art. 220 Tax Code of the Russian Federation. If the apartment was purchased before 2014, there is no maximum amount - in Art. 220 of the Tax Code of the Russian Federation in the old edition, it was not indicated.

Both deductions are permanent - they can be returned even if the property was purchased a long time ago or has already been sold.

Does a child lose the right to deduct if a parent received a property deduction for him?

Since the deduction for the costs of purchasing property can only be received once (from January 1, 2014 - no more than 2 million rubles during a lifetime), the relevant question is whether the child will lose the right to a property deduction in the future when purchasing their own home if the parent receives deduction for it. The regulatory authorities think not.

Due to the fact that a property deduction for a child’s home (or for a share of housing) is provided to the parents, and not to the child himself, the child does not lose the right to receive a property tax deduction in the future for the costs of purchasing another home .

This position is confirmed by a number of letters from the Ministry of Finance of Russia dated 09/03/2015 N 03-04-05/50743, dated 08/29/2014 N 03-04-05/43425, dated 07/04/2012 N 03-04-05/5-841, dated 10.04 .2012 N 03-04-05/7-478.

If the marriage between parents is not registered

The Tax Code of the Russian Federation grants the right to receive a tax deduction for a child to his parent. The presence of a registered marriage is not directly taken into account.

However, if the expenses were incurred by one of the unmarried parents, it is he who has the right to apply for a tax deduction. The second parent will be denied a tax refund.

This position is confirmed by letter of the Ministry of Finance of the Russian Federation dated March 23, 2020 No. 03-04-05/22551. The Ministry of Finance indicated that in the absence of a registered marriage, there are no grounds for providing a tax deduction to the father of minor children if the price for the acquisition of shares in the children’s apartment was paid by their mother.

If the marriage is concluded, either parent can claim a tax deduction. As a general rule, property acquired during marriage, as well as expenses, are considered joint for the spouses. Therefore, it does not matter in whose name the apartment will be registered and who paid for it.

Can a parent receive a deduction for a child if he has previously received a property deduction?

If a parent has already exhausted the property deduction for another property, then he will not be able to receive a deduction for the child. This is due to the limitation of the use of property deduction. Grounds: clause 11 of Art. 220 of the Tax Code of the Russian Federation, Letter of the Ministry of Finance of Russia dated March 16, 2015 N 03-04-05/13747.

However, if a parent wants to receive a deduction for a child on the same property that he himself received in part of his share (for example, he did not know about the possibility of receiving a deduction for a child), then he has the right to do so.

To do this, you should contact the tax authority again, submitting updated declarations with a recalculation of the deduction amount. Reason: letter of the Ministry of Finance of Russia dated 02.02.2012 N 03-04-05/9-109.

If you have not yet purchased a home, we recommend our partner’s site-guide, APARTMENT-Bez-AGENTA.ru. This is an educational site for those who want to understand the rules for buying and selling apartments.

Conditions for receiving a property return

When applying for a tax benefit, you must comply with the procedure established by law. The grounds for receipt and refusal are regulated as follows :

- The benefit is provided only to taxpayers of the Russian Federation and applies to real estate acquired in Russia.

- A citizen must have a permanent official place of work in accordance with Labor legislation and a salary not lower than the established minimum wage (minimum wage).

- The refund amount to one recipient cannot exceed 260 thousand rubles.

- The benefit is provided only once in a lifetime, but allows for the transfer of lost funds to subsequent objects.

- Spouses who purchased housing during an official marriage can regulate the amount of the amount received at their discretion.

- It is prohibited to issue a property return when purchasing housing from close relatives: parents, children, spouses.

We talked about whether it is possible to legally receive a deduction when buying an apartment from relatives here.

Methods of obtaining

If the application is approved, the funds will be credited to the applicant's account. In addition, you can write an application to the accounting department at your place of work with a positive decision.

Until the entire amount is exhausted, 13% tax will not be withheld from the applicant. If one of the parents received a deduction for his share in the property and did not exhaust his limit, then he has the right to a second refund for the children.

To do this, you need to contact the Federal Tax Service and submit updated documents, including a new declaration. Upon reaching adulthood, the younger generation retains the right to tax benefits, regardless of whether their parents received this type of benefit for them.

Video

Watch the step-by-step video instructions for obtaining a property deduction:

Of course, it is worth taking advantage of this situation, since this still does not deprive the future rights of a minor who, due to his age, cannot fully manage his share of the living space.

Often people buy real estate, making their children owners as well. And then a person may have a question: is it possible to get a tax deduction for a minor child when buying an apartment? We'll talk about this today.

When should you apply?

Some parents, even knowing about the possibility of receiving a child deduction, do not take advantage of it. To make the right choice, you need to know about important nuances:

- The deduction amount for yourself and children is not cumulative . That is, if you have no children, 1 child or 5, the deduction amount will be the same - 2,000,000 rubles. Some people mistakenly believe that each child is entitled to the same amount.

- The child does not lose his right to a deduction . And this became possible precisely thanks to the previous limitation. If the deductions were summed up, it is unlikely that the child could receive this benefit for himself in adulthood.

These two rules make it possible to understand when it makes sense to issue a deduction for a child, and when it is inappropriate. Property returns for children should be made if:

- you bought inexpensive real estate (that is, if your share does not cover the maximum deduction amount, then it makes sense to get a refund for the child);

- all or most of the housing is owned by minor children;

- You can receive your child’s share before his or her 18th birthday.

Sometimes this option makes no sense. For example, if you buy an apartment for 5,000,000 rubles. for yourself and your child in equal shares, then for each you have 2,500,000 rubles. Even from your share you can get a refund only for 2,000,000 rubles. Therefore, money will not be returned for the child.

There are also more complex cases when one of the parents is not the owner of the apartment. Then it makes sense for the latter to receive a preference for children.

Read: How to write off your mortgage when you have a baby in 2021

Does the child lose the right to deduction in this case?

This question does not have a significant underlying basis that would make it possible to clearly prohibit whether a tax deduction can be obtained when purchasing an apartment for children in the future. If the legislative framework does not change before the owner reaches the age of majority , a tax deduction for the purchase of an apartment will be provided to the child at any convenient time, after :

- he will turn 18 years old;

- he will officially get a job.

The tax deduction for the purchase of an apartment for a child is based on legal norms that take into account that when purchasing real estate in the name of children, parents invest money.

When can I get it?

Additionally, requirements are imposed on the transaction being performed. So, a deduction is provided if the apartment was purchased:

- using your own funds (if you used a mortgage, you can also get a deduction for a child, but this is a different type, a larger amount and different conditions of application);

- not from close relatives (this restriction was introduced to prevent people from making fictitious real estate purchase and sale transactions, wanting to receive a tax deduction, without actually paying for anything and without receiving ownership of the apartment).

Additionally, parents are afraid that they do not always have the right to a deduction for their child. A refund can be issued for a minor if the owner is:

- Only a child . For example, you bought an apartment for 1,500,000 rubles. and registered it for the child. If you have not previously used the deduction, then you can get a full refund for the child.

- Both you and your child . For example, purchasing the same apartment for 1,500,000 rubles. ½ for each, you can get a deduction for yourself and for a child of 750,000 rubles.

If a child has several parents, then each has the right to a deduction, but in total it should not exceed the cost of the share.

For example , if for 2,700,000 rubles. you purchase housing as the property of yourself, your spouse and 1 child and each receives 1/3, then the parents can apply for a deduction for themselves in the amount of 900,000 rubles. and divide the remaining 900,000 rubles. between themselves. Moreover, this division does not have to be in half (the entire share can go to one parent, be divided in half or not in equal proportions - as agreed).

Sometimes other family members may also participate in the purchase, then their share will not be taken into account when calculating the deduction, and for the child and yourself you will return the money in proportion to the cost of your part.

Read: Double tax deduction for a child: who is eligible and how to get it

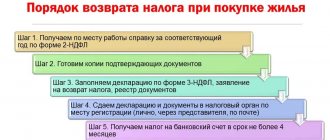

Return documentation

There are two ways to receive a tax deduction for a child when purchasing an apartment: through the tax office or the tenant. Each option has its own characteristics. When registering with the tax authorities, you will need to provide:

- Declaration completed in the prescribed form.

- Applications indicating the purchase of the child's property.

- Documentation of the purchase of living space.

- Papers about the amounts and purposes of expenses.

- Loan agreement (when purchasing with credit funds).

- Child's birth certificate.

- Documentation of guardianship or conservatorship.

This set of papers is transferred to the Federal Tax Service. The application indicates the account where the tax deduction for the apartment for the child should go. The check is carried out over the course of 3 months, and it will take about another month to transfer the money.

The second option involves creating an application for payment of a deduction to parents and collecting documentation. In this case, there is no need to fill out a declaration. The papers are submitted to the tax service, which must confirm the rights to the preference within a month. The notification is submitted to the accounting department, and the employee receives a salary from which tax is not deducted. The preference ends when the full amount of compensation has been selected.

Registration through an employer has a number of advantages:

- Rapidity.

- Simple registration without filling out a declaration.

- Possibility of obtaining from several employers.

This is important to know: How to cash out maternity capital to buy an apartment

In the latter option, the application must indicate which organizations will provide the refund and in what amounts. The notices for each place of employment will indicate the amount of the benefit, which should not be exceeded.

Employees operating on the basis of contract agreements cannot receive a refund from customers.

However, if you change jobs during the period of receiving the deduction, the process is interrupted. The notification from the inspection is targeted; a specific organization is indicated there. To continue receiving the benefit, you will have to visit the tax authorities again and get a new document.

Child deductions

Compensation for property tax payments can be obtained by figuratively comparing it with deductions for children under personal income tax. Payment of taxes for a child on property owned by the child in monetary terms is offset by the amount of personal income tax deductions provided, which are received by the employer if one of the following conditions is met:

- the child’s age does not exceed 18 years of age;

- the age is subject to extension to 23 years when studying full-time at a higher educational institution.

The amount of the deduction depends on the number of children for whom the account is provided and the total amount of income received, calculated on an accrual basis from the beginning of the calendar year. In the current year 2021, to receive a deduction, income must not exceed 350 thousand rubles, and the monthly amount is:

- 1400 rubles – for the first and second child;

- 3000 rubles – for the third and subsequent children;

- 12,000 rubles – for a disabled child raised by parents;

- 6,000 rubles – for a disabled person since childhood who is supported by guardians or trustees.

The issue of compensation for property taxes of children under 18 years of age paid by parents or guardians in the presence of disability is groundless, since childhood disability belongs to preferential categories, exempt from payments to the budget at the federal level.

According to the legislator, if you answer negatively to the question: are minor children subject to property tax, then parents or guardians, in order to evade taxation, will legally transfer property values to their children, depriving the treasury of tax revenues. At the same time, no one will compare that the child deduction provided exceeds the amount paid. However, to receive a deduction, parents must have official income in the form of wages, and if not, payments must be made from their own sources.