Question

The company must reflect the amount of accrued benefits in the calculation of insurance premiums in accordance with the Procedure for filling out the calculation, approved by order of the Federal Tax Service of Russia dated October 10, 2016 No. ММВ-7-11/[email protected] After receiving your report, the inspectors will transfer the data to the Fund. After the FSS confirms the expenses, the tax authorities themselves will carry out the offset.

Unified calculation of insurance premiums 2020

From 01/01/2020, the correctness of calculation and payment of these mandatory payments is supervised by tax officials. Law No. 250-FZ establishes that reporting on contributions for previous years, including corrective forms, are submitted to the Pension Fund of the Russian Federation and the Social Insurance Fund of the Russian Federation in accordance with the previous rules.

- The overpayment can be offset against future payments only for the same contributions that turned out to be overpaid (clause 1.1 of Article 78 of the Tax Code of the Russian Federation);

- it is impossible to return the overpayment that was reflected in the reporting submitted to the Pension Fund and has already been taken into account for specific insured persons (clause 6.1 of Article 78, clause 1.1 of Article 79 of the Tax Code of the Russian Federation);

- If there are debts on penalties and fines for the same contributions that turned out to be overpaid, the refund will be made minus the amount of the existing debt (clause 1.1 of Article 79 of the Tax Code of the Russian Federation).

Refund from the Social Security Fund due to excess expenses in 2021

Reimbursement of expenses is made upon the application of the employer accompanied by documents confirming payments. Information on insurance premiums and their movement, necessary for the FSS to reimburse the amounts to the employer, is obtained from the calculation certificate.

How to reimburse maternity benefits from the Social Insurance Fund?

Thus, the policyholder makes it easier to compensate for his social security costs by reducing the size of the next contribution. If the amount of the policyholder’s payment exceeds the amount of the contribution, then you will have to contact the Social Insurance Fund. When submitting to the tax authority, the policyholder reflects expenses in the relevant sections and appendices of the new unified reporting form, which is already submitted to the tax authority.

- a copy of the child's birth certificate;

- a certificate stating that the benefit was not assigned to the second parent;

- divorce certificate if parents are divorced;

- an extract from the decision to establish guardianship over a child for a guardian, adoptive parent, or foster parent.

The policyholder makes it easier to compensate for his social security costs by reducing the size of the next contribution. If the amount of the policyholder’s payment exceeds the amount of the contribution, then you will have to contact the Social Insurance Fund.

Reduction of insurance premiums for benefits

Having received such a calculation, tax authorities will report data on the claimed compensation to the Federal Tax Service of Russia. Specialists from social insurance will verify the accuracy of the declared expenses by conducting a desk or on-site audit. They will report the results to the tax authorities.

The temporary disability benefit for an insured event that occurred after January 1, 2021, calculated from the minimum wage , will be: 11,280 * 24/730 = 370.85 rubles. per day with insurance experience of more than 8 years. If the length of service is less, then the following coefficient must be applied to the specified amount: 60% - for less than 5 years of experience and 80% - for 5 to 8 years of experience.

Offset (return) of contributions according to the rules of the Tax Code of the Russian Federation and the Social Insurance Fund

Since 2021, almost all types of insurance premiums (except for payments for accident insurance) have become subject to the provisions of the Tax Code of the Russian Federation, which has not only a separate chapter devoted to these charges, but also references to contributions in all general rules for working with tax payments (h 1 Tax Code of the Russian Federation). As a result of these changes, the return (offset) of insurance premiums from 2021 began to be made according to the algorithms used in similar procedures for taxes and fees (Articles 78, 79 of the Tax Code of the Russian Federation).

Why are there 2 types of rules for the return (offset) of contributions?

- contributions paid after 2021 continue to be paid separately by fund;

- contributions received by the Pension Fund are taken into account individually;

- During the 2020-2020 period (transition period), the question may arise about the return of contributions transferred there according to the rules in force until 2021.

Crediting the amount of excess expenses against insurance contributions to the Federal Social Insurance Fund of the Russian Federation

The organization is on the simplified tax system (income reduced by expenses). For January 2011, contributions to the Social Insurance Fund of the Russian Federation were accrued in the amount of 3,000 rubles. At the same time, the organization pays monthly benefits to its employees:

– for child care up to 1.5 years – 5,000 rubles;

– payment for four additional days off to care for disabled children – 2,000 rubles. (Amounts of benefits are given conditionally).

Do we have the right, guided by Art. 15 of Law No. 212-FZ and the letter of the Social Insurance Fund of June 21, 2010 No. 02-03-13/08-4917, not to transfer accrued contributions until February 15, 2011, but to offset the amount of excess expenses against upcoming payments? Or should we transfer the amount of accrued contributions, and then contact the territorial body of the Social Insurance Fund for the allocation of funds to pay insurance coverage?

According to paragraph 2 of Art. 15 of the Federal Law of the Russian Federation dated July 24, 2009 No. 212-FZ, the amount of insurance premiums

for compulsory social insurance in case of temporary disability and in connection with maternity, payable

to the Federal Social Insurance Fund of the Russian Federation, is subject to reduction

by payers of insurance contributions

by the amount of expenses incurred by them

for the payment of compulsory insurance coverage for the specified type of compulsory social insurance in accordance with the legislation of the Russian Federation.

Since before 2011

this article of the Law

did not stipulate the possibility of offsetting

expenses against upcoming payments of contributions;

Fund of the Russian Federation,

in a letter dated June 21, 2010 No. 02-03-13/08-4917

explained

that the norms of the current legislation on compulsory social insurance

do not contain a prohibition for policyholders to pay insurance coverage to the insured against

the insurer's upcoming payments for compulsory social insurance in case of temporary disability and in connection with maternity.

Therefore, according to officials, if the amount of the policyholder’s expenses for paying insurance coverage in a certain month exceeds the amount of insurance premiums accrued for the same month, the policyholder has the right to apply

to the territorial body of the FSS of the Russian Federation

for the necessary funds

in the manner established by Art.

4.6 of the Federal Law of the Russian Federation dated December 29, 2006 No. 255-FZ, and offset the amount of excess costs

for the payment of insurance coverage

against the upcoming payments

of the policyholder for this type of compulsory social insurance.

From January 1, 2011

already directly in clause 2.1 of Art.

15 of Law No. 212-FZ states that the payer of insurance premiums has the right, within the billing period, to set off the amount of excess expenses

for the payment of compulsory insurance coverage for compulsory social insurance in case of temporary disability and in connection with maternity

over the amount of accrued insurance contributions

for the specified type of compulsory social insurance towards upcoming payments for compulsory social insurance in case of temporary disability and in connection with maternity.

Since we are talking about the costs of paying compulsory insurance coverage

regarding compulsory social insurance in case of temporary disability and in connection with maternity, we will understand what belongs to the types of insurance coverage.

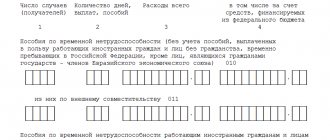

Art. 1.4 of Law No. 255-FZ establishes that the types of insurance coverage

for compulsory social insurance in case of temporary disability and in connection with maternity

the following payments are made

:

1)

temporary disability benefits;

2)

maternity benefits;

3)

a one-time benefit for women registered in medical institutions in the early stages of pregnancy;

4)

lump sum benefit for the birth of a child;

5)

monthly child care allowance;

6)

social benefit for funeral.

Payment for additional days off

provided for the care of disabled children

is not indicated

.

Since January 1, 2010

financial support for the costs

of paying for additional days off

provided for caring for disabled children in accordance with

Art.

262 of the Labor Code of the Russian Federation ,

is carried out at the expense of interbudgetary transfers from the federal budget

, provided in the prescribed manner to the budget of the Social Insurance Fund of the Russian Federation (clause 17, article 37 of the Federal Law of the Russian Federation of July 24, 2009 No. 213-FZ).

That is, these expenses are paid in full from the federal budget and do not apply to insured events.

But since money from the federal budget is transferred to the FSS of the Russian Federation, the specified payments are reimbursed to the policyholder by the FSS of the Russian Federation

.

Order of the Ministry of Health and Social Development of the Russian Federation dated November 18, 2009 No. 908n approved the Procedure for accounting for insurance contributions for compulsory social insurance

in case of temporary disability and in connection with maternity, penalties and fines,

expenses for payment of insurance coverage

and settlements for compulsory social insurance in case of temporary disability and in connection with maternity.

According to the Procedure, policyholders keep track of expenses incurred against accrued insurance premiums

for payment of insurance coverage specified in Art. 1.4 of Law No. 255-FZ.

At the same time, in accordance with clause 6 of the Procedure, policyholders also keep records of expenses against accrued insurance premiums

carried out in accordance with the legislation of the Russian Federation at the expense of interbudgetary transfers

from the federal budget

provided to the budget of the Social Insurance Fund of the Russian Federation,

including the payment of four additional days off per month for caring for disabled children

.

Consequently, expenses for paying for additional days off to care for disabled children are also considered expenses of the policyholder made against accrued insurance premiums for the payment of insurance coverage

.

So you have the right to count

the amount of excess expenses for payment of child care benefits and payment for days of care for disabled children over the amount of accrued insurance premiums for upcoming payments.

This means that, according to the conditions of your example, you reduce the amount of insurance premiums accrued for January by 3,000 rubles of expenses for paying insurance coverage.

That is, for January the amount of contributions payable is zero

.

The rest of the expenses

, exceeding the amount of insurance premiums accrued for January, you will take into account for February. And so on.

Please keep in mind that offsets are only possible within the billing period – one calendar year.

.

If you have overspending

for payment of insurance coverage, it is not carried over to the next year.

And then you will have to contact the FSS of the Russian Federation for the necessary funds

, because if the insurance premiums accrued by the policyholder are not enough to pay insurance coverage to the insured in full, the policyholder applies for the necessary funds to the territorial body of the insurer at the place of its registration (clause 2 of Article 4.6 of Law No. 255-FZ).

In private explanations, specialists from the Ministry of Health and Social Development of the Russian Federation advise that you must notify the Federal Social Insurance Fund of the Russian Federation about the test

.

Reimbursement of benefits from the Social Insurance Fund in 2021

- Name of the organization;

- legal address of the policyholder;

- last name, first name, patronymic (if the submission is made by an individual entrepreneur);

- passport data (for individual entrepreneurs);

- address of residence (for individual entrepreneurs);

- policyholder registration number;

- the amount of funds that must be reimbursed.

- When reimbursement of benefits paid to an employee as compensation for a period of incapacity for work, as well as funds spent on pregnant employees, sick leave certificates must be attached.

Reimbursement from the Social Insurance Fund in 2021

78 of the Tax Code of the Russian Federation indicates that it is impossible to offset the overpayment of one contribution (that is, one BCC) against the payment of other contributions or taxes (that is, other BCCs). One of the previous sections already contains an application form for the return of overpayments on disability insurance premiums as of 01/01/2020. There is no need to attach any documents to the application.

Thus, the application standardly contains information about the policyholder (name, legal address, insurance registration number), bank details for receiving compensation and the amount of funds required. The text of the sample application itself states that it is provided simultaneously with two applications:

Enterprise IP Novikov M.M. has a staff of hired workers, pays remuneration for labor, and pays insurance premiums. In the second quarter of 2021, the individual entrepreneur accrued the amount of wages to employees in the amount of 1,390,000 rubles, the amount of deductions for which to OSS amounted to 40,310 rubles. IP Novikov M.M. in the 2nd quarter, he made payments for social insurance expenses in the amount of 55,000 to pay for leave under the BiR, disability benefits in the amount of 79,000 rubles (including the amount of payment at the expense of the enterprise in the amount of 3,000 rubles).

Reimbursement for sick leave from the Social Insurance Fund in 2021

That is, if the amount of benefits paid for any month exceeded the contributions to the Social Insurance Fund accrued for the same month, the policyholder has the right to apply to the fund’s branch for a refund of funds for the payment of insurance coverage.

A positive or negative decision is submitted to the tax service, which must, no later than three days, transfer compensation for expenses to the bank account of the policyholder, which was indicated in the application.

Although the tax service has been refunding expenses since 2021, the Social Insurance Fund still must control where insurance premiums go. If an employer wants to return compensation for expenses from the social insurance fund, he must:

Grounds for reimbursement of expenses from the Social Insurance Fund

- Fill out and submit the uniform calculation form to your local tax office.

- Provide the Social Insurance Fund and the tax inspector with a basic and additional package of documents for reimbursement of funds.

- Wait for the test results.

- If the decision is positive, receive a refund to your bank account. An alternative option is to offset against a future contribution and. reduce future costs for mandatory insurance payments.

As you know, starting from 2021, contributions that were previously paid to the Social Insurance Fund have been transferred to the tax department. Only contributions for injuries were not affected by the changes; they are paid as before by the Social Insurance Fund. However, despite the fact that contributions are controlled by the Federal Tax Service, benefits are also checked by the Social Insurance Fund.

Documents for reimbursement of FSS expenses

Until December 31, 2016, data on accrued contributions for illness and maternity and expenses incurred were indicated in Form No. 4-FSS. Since 2017, the administration of contributions, with the exception of payments for “injuries,” has been transferred to the tax authorities, so these indicators began to be reflected in the DAM - “Calculation of Insurance Premiums,” which the policyholder is required to submit to the Federal Tax Service on a quarterly basis. The application form for reimbursement of expenses from the Social Insurance Fund in 2021 will depend on the moment the expenses arise:

- until 12/31/2016 – it is necessary to use form No. 23-FSS (approved by Order of the FSS of the Russian Federation dated 11/17/2016 No. 457, Appendix No. 3);

- after 01/01/2017 - an application is filled out according to the form from the FSS letter dated 12/07/2016 No. 02-09-11/04-03-27029.

Along with the application, the employer submits supporting documents to the Social Insurance Fund.

What documents are attached to the application?

To reimburse the costs of paying benefits from the Social Insurance Fund, the employer attaches to the application documents, the list of which is given in Order of the Ministry of Health and Social Development of Russia dated December 4, 2009 No. 951n (as amended on October 28, 2016). What you need to prepare:

- breakdown of expenses and a calculation certificate in the form from appendices 1 and 2 to the letter of the Social Insurance Fund No. 02-09-11/04-03-27029, if expenses were incurred after December 31, 2016;

- copies of documents on the basis of which benefits were assigned.

The full composition of the applications depends on the type of benefit. For example, when reimbursing expenses for sick leave, the Social Insurance Fund requires copies of:

- certificate of incapacity for work;

- work book or other documents confirming work experience;

- certificates in form No. 182n, if income from other employers was taken into account when calculating.

At the birth of a child:

- certificate from the registry office;

- a copy of the birth certificate;

- certificate of non-receipt of payment by the second parent.

The Fund’s specialists may also request other documents confirming the employee’s employment. Most often requested:

- a copy of the employment contract;

- report cards;

- staffing schedule;

- payslips;

- payment documents for the employee to receive funds;

Also, some branches of the Social Insurance Fund require you to submit a copy of the dismissal order if the employee has already received a payment, and the company does not have documents on his work experience.

The regional branch of the Foundation may develop its own list. For example, when reimbursing FSS expenses in St. Petersburg, you can be guided by the recommended list posted on ]]>the official website]]> of the St. Petersburg regional branch of the Fund.

All copies are certified with the inscription “Copy is correct” indicating the date, signed by the manager or authorized representative. If available, a stamp is placed.

Refund of contributions from the Social Insurance Fund in 2021 in case of overpayment

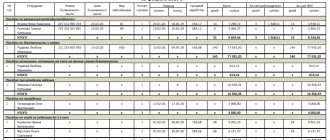

In just six months, benefits exceeded contributions by 170,000 rubles. (300,000 - 470,000 = -170,000). If we add the funds transferred to the FSS in May 2020 in the amount of 100,000 rubles, it turns out that the FSS still owes the organization 70,000 rubles. We indicate this value in line 090 with the sign “2”.

Reimbursement period

- the inscription “Copy is correct” or a record of similar meaning;

- the signature of the head of the organization or the signature of the entrepreneur;

- seal, if one is used (otherwise a letter stating that the seal is not used is required).

Important! You can submit documents to the Social Insurance Fund for reimbursement of expenses for both sick leaves at once, or separately. Documents for continuation of sick leave confirming reimbursement of expenses will be the same as for the main sick leave.

We reflect reimbursement of social insurance expenses for the last year in the RSV

You can also check the balance of social insurance settlements using a calculation certificate (Appendix 1 to the letter of the Federal Social Insurance Fund of Russia dated December 7, 2016 No. 02-09-11/04-03-27029). Such a certificate, along with other documents, is submitted to the Fund by those policyholders who want to receive compensation.

We recommend reading: Payment for the Third Child in 2021 in the Year of the Child in Khmao

Procedure for payment of benefits

- In the DAM for 2021, line 090 of Appendix 2 to Section 1 indicates the amount of 25 thousand rubles with attribute 2.

- In accounting, in the debit of account 69, the subaccount “Social Insurance Settlements” at the end of the year there remains a balance of 25 thousand rubles.

The fund will return funds for periods up to 2021, and from 2021 - the tax office. The Ministry of Labor of Russia issued an order in October 2021, which presented a package of documents according to which the Social Insurance Fund of the Russian Federation will allocate funds to employers for the payment of maternity and other benefits when applying for periods after January 1, 2021. The Foundation has developed forms for these documents; they came into effect in December 2021.

How to confirm expenses under the Social Insurance Fund under the offset system

As for reimbursement of expenses for paid child benefits, you will also need to prepare an application, a calculation certificate and attachments. In this case, the supporting documents will be:

Documents for reimbursement of child benefits

Sometimes it happens that the document is not lost, but there is simply no possibility of processing it. For example, it is not possible to obtain a certificate from the husband’s place of work stating that he has not received child benefits. In this case, the benefit is still paid. But you need to get an explanatory note from the employee and attach it to the documents submitted to the Social Insurance Fund.

The employer has the right to reduce the amount of contributions to the budget by the amount of accrued benefits. When expenses exceed deductions, a budget debt arises to the enterprise. The employer applies to the Social Insurance Fund for compensation of funds paid for insured events if an overpayment occurs.

The employer fills out that part of the document where there is a note indicating that information has been entered by the employer (“To be completed by the employer”). Thus, he must indicate information about the organization (name, registration number, etc.), personal data of the employee (full name, INN, SNILS, average earnings per day and for the billing period, insurance experience, etc.), period for which a subsidy and its size are assigned. The completed form is signed by the manager, chief accountant. Insurance premiums in 2021 are considered paid on the day when an LLC or individual entrepreneur receives a payment order to pay insurance premiums. Such an order for the payment of insurance premiums can be submitted either by the payer of insurance premiums or by any other person: an organization, an individual entrepreneur or a person who is not engaged in business (clause 1 of Article 45 of the Tax Code of the Russian Federation). Of course, there must be enough money in the current account of the organization or other person for the payment, and the order itself must be filled out correctly. In 2021, transfer insurance premiums to the budget without rounding: in rubles and kopecks (clause 5 of Article 431 of the Tax Code of the Russian Federation).

Reimbursement of expenses from the Social Insurance Fund in 2021

Timely submission of reports on insurance premiums to the relevant authorities allows entrepreneurs to avoid penalties and other problems that complicate doing business. It just seems that filling out strict reporting forms is not particularly difficult.

Individual entrepreneurs, heads of peasant farms, also, according to the new legislation, deduct a fixed amount of 26,545 rubles. “pension” contribution, 5,840 rub. – “medical” for all participants of the peasant farm, including individual entrepreneurs.

Interim report to - FSS

In order to cover the costs of payments to employees who have received injuries or occupational diseases through contributions, the employer submits an interim calculation of 4-FSS to the Social Insurance Fund of the Russian Federation. The report is drawn up only if the amount of contributions from the NSiPZ, according to the calculations of the policyholder, is less than the amount of benefits paid to employees for this period.

Reimbursement of expenses to the Social Insurance Fund in 2021

- the report is compiled as needed and therefore does not have a set date for submission;

- in the “reporting period” column of the title page, fill in the cells after the fraction, which indicate the number of the interim report, for example, an organization submits such a report for the second time, which means the period code is “02”;

- tabular values are filled in for the first or first and second months of the quarter, while the report is presented for the period from January to the month of payment of employee benefits;

- Documents are attached to the interim report: an application to the Social Insurance Fund for reimbursement, copies of documents confirming expenses (sick leave, birth certificate, etc.).

- Submit documents to the Fund branch at the place of registration of the company. This includes a free-form application indicating the amount, a copy of the calculation of payments in form - 4 FSS of the Russian Federation, copies of those documents that confirm the validity and accuracy of the costs of payments;

- Receive funds from social insurance;

- Reflect the money received in your financial statements.

As you know, starting from 2021, contributions that were previously paid to the Social Insurance Fund have been transferred to the tax department. Only contributions for injuries were not affected by the changes; they are paid as before by the Social Insurance Fund. However, despite the fact that contributions are controlled by the Federal Tax Service, benefits are also checked by the Social Insurance Fund.

The procedure for reimbursement of maternity benefits from the Social Insurance Fund in 2021 in case of issuance of a continuation of sick leave

To keep records of benefits, use our Simplified 24/7 . It prepares documents and HR reports in one click. Take a trial access to the program for 30 days. Consultation on all accounting issues is available to users 24 hours a day, 7 days a week.

sick leave; children's birth certificates; certificates from medical institutions; payroll statements; orders for admission; certificates of earnings from previous places of work; other documents confirming the legitimacy of the application for compensation of expenses, as well as confirming the settlement amounts.

We recommend reading: Transport tax for large families in Moscow 2021 for a car with a capacity of over 250 hp

In paper form, the report for each quarter is submitted by the 20th day of the month following this quarter, and the electronic form can be submitted a little later - until the 25th. It is submitted to the territorial division of the Social Insurance Fund in which the organization is registered. Late or incorrect submission of a report may result in a fine.

What documents are needed for reimbursement of maternity benefits from the Social Insurance Fund in 2021?

They will not allocate money from the federal budget to cover the deficit, but they promise that in 2021-2021 all FSS benefits will be paid as expected. This will be possible due to reserve funds and an increase in profitability on other insurance items. Of course, such a scheme will not last long.

The deadline for transferring money to the Social Insurance Fund is established by current legislation. It is 10 days from the date of receipt of the application . However, if the FSS decides to conduct an inspection, the deadline will be extended.

Online magazine for accountants

Reimbursement of expenses is made upon the application of the employer accompanied by documents confirming payments. Information on insurance premiums and their movement, necessary for the FSS to reimburse the amounts to the employer, is obtained from the calculation certificate.

Reimbursement for sick leave from the Social Insurance Fund in 2021

The FSS will be able to request information about contributions from the inspectorate (clause 2.2, part 1, article 4.2, part 1.1, article 4.7 of the Federal Law of December 29, 2006 No. 255-FZ, as amended on January 1, 2021). Reimbursement to the Social Insurance Fund in 2021: the Social Insurance Fund scheme has the right to check information about benefits and make a decision on reimbursement or refusal of credit.

- Write an application for a refund and submit this application to the Social Insurance Fund.

- Prepare a statement of calculation, as well as the necessary supporting documents and attach them to the application.

- Wait for the FSS check.

- After the FSS checks and approves the reimbursement, it will transfer the funds to the organization’s account.

To keep records of benefits, use our Simplified 24/7 . It prepares documents and HR reports in one click. Take a trial access to the program for 30 days. Consultation on all accounting issues is available to users 24 hours a day, 7 days a week.

In what cases does the right to compensation arise?

In the “pilot” regions where the “Direct Payments” project operates, the FSS makes all payments directly to insured individuals. Accordingly, the employer does not bear any additional costs. Therefore, the right to reimbursement of expenses from the Social Insurance Fund does not arise in this case.

In the constituent entities of the Russian Federation, where the credit system is still in effect, benefits are paid to employees by the employer (with the exception of sick leave issued in 2021 to employees over 65 years of age due to quarantine during the self-isolation period). The employer pays for the first 3 days of temporary disability from his own funds. Expenses incurred for the remaining period are taken into account when calculating social insurance contributions (Part 2, Article 4.6 of Law No. 255-FZ dated December 29, 2006, Clause 2, Article 431 of the Tax Code of the Russian Federation). If the amount of expenses exceeds the accrual, the employer has an overpayment, which can be:

- apply to future insurance premium payments;

- reimburse from the budget.

The Federal Tax Service is responsible for offsetting the overpayment for the following periods. To request a refund, you must contact the FSS branch at the place of registration of the policyholder.

Refund of overpayment from FSS

Be careful: if you make a mistake in the KBK, you can clarify the code only within the budget of the Federal Social Insurance Fund of Russia. If the first three digits are “393,” then the budget administrator is the Social Insurance Fund. Such an error in the KBK can be clarified if, according to the information in field 24 “purpose of payment”, it is clear that the policyholder actually made errors in the payment order.

Confirmation of expenses under the Social Insurance Fund starting from 2021 under the credit system

- Appear in person at the fund or through a representative. In this case, an application for refund of the overpayment is submitted to the territorial department of the Pension Fund or Social Insurance Fund. If a representative approaches the fund, then a notarized power of attorney must be filled out for him.

- By mail. This method involves sending a registered letter with a list of attachments and acknowledgment of delivery. In this case, you will not need to contact the fund in person, but the waiting time will increase due to postal delivery time.

- Submitting an application for a refund of amounts paid before the 17th year to the Federal Tax Service. The latter began to be responsible for contributions only from January 1, 2017. Extra-budgetary funds are responsible for payments made before the 17th year. Therefore, the application must be sent specifically to these funds.

- Submitting an application for a refund without specifying the amounts. All amounts are specified through reconciliation of calculations. In particular, the application must indicate the exact amount of the overpayment and the amount of the arrears, if any. If the reconciliation is carried out incorrectly, then a difference is formed between the amount in the application and the amount in the personal account/registration.

- The wrong application form is being used. To draw up an application to the Federal Tax Service and extra-budgetary funds, different forms are used. When choosing a form, you must also take into account what kind of contribution is planned to be returned: for temporary disability or for injury.

We recommend reading: Subsidies for Families with Two Children in the Kaluga Region