Calculation of fines: postings

In case of violation of tax laws, the accrued amounts of penalties are charged to the profit and loss account. In accordance with Order of the Ministry of Finance dated October 31, 2000 No. 94n, a subaccount 99.09 “Other profits and losses” is opened to account 99 “Profits and losses”. This sub-account records fines assessed for violation of tax laws in correspondence with the corresponding tax account. In general, the entry for calculating penalties for violation of the law looks like this: Dt 99.09 Kt 68 (69).

Examples of postings for violation of tax laws:

- Dt 99.09 Kt 68.01 - for non-payment of personal income tax;

- Dt 99.09 Kt 68.02 - for violation of the procedure for submitting reports electronically;

- Dt 99.09 Kt 69.01 - for failure to provide reports.

To calculate all other penalties, including traffic police fines and penalties under business contracts, you should use account 91 “Other income and expenses” in correspondence with account 76 “Settlements with other debtors and creditors.”

The organization's expenses for paying penalties are reflected in the debit of account 91.02 as part of other expenses (clause 11 of PBU 10/99).

The organization's income from receiving fines due under business contracts is reflected in the credit of account 91.1 as part of other income (clause 7 of PBU 9/99, Order of the Ministry of Finance dated October 31, 2000 No. 94n).

Accounting for fines under contracts in the 1C program: Enterprise Accounting 8 edition 3.0

Published 07/28/2016 15:27 Author: Administrator Unfortunately, it is not always possible to pay obligations to suppliers or customers on time. It happens that an organization has financial problems and is unable to pay off its debts on time. And sometimes violations of the terms of the contract occur, for example, failure to meet delivery deadlines, damage to property, or downtime due to the fault of the counterparty. And in this case, penalties often have to be assessed. Let's figure out how to correctly accrue and pay off fines in the 1C: Enterprise Accounting 8 rev 3.0 program.

In this article we will look at two options for accounting for a fine.

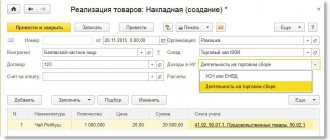

First, we are suppliers of goods and our buyer made a delay in payment under the contract. We reflected the fact of the sale in the program with the document “Sale of Goods”; a buyer’s debt arose on account 62.01, which was not repaid within the period established by the contract. In order to calculate penalties, open the tab “Operations”, “Accounting”, “Operations entered manually”

Create a new document and click the “Add” button. We fill in the empty fields, on debit we indicate account 76.02 “Settlements on claims”, on credit account 91.01 “Other income”

Now, to receive payment from the buyer, we create a document “Receipt to the current account”. Open the tab “Sales”, “Sales (acts, invoices)”

Select the document “Sales (acts, invoices)”, which reflects the fact of sale, click the “Create based on” button and create the document “Receipt to the current account”

Fill in the input. number, date, agreement, DDS article, purpose of payment.

We post the document and look at the postings that repay the debt on account 62.

In the event that you automatically download bank statements into the program, just make sure that when you post the document “Receipt to the current account”, the debt is repaid correctly according to the required document (we select the debt repayment method “By document” and the required document in the table or leave the option “Automatically”, if this counterparty has a debt under only one sales document). Now we will create a document to pay off penalties. Open the tab “Bank and cash desk”, “Bank”, “Bank statements”

Click the “Receipt” button and fill out the opened document “Receipt to the current account”. Enter the date, number, amount, DDS article, select settlement accounts 76.02 “Settlements for claims”. If you download statements into the program from a client bank, make sure that invoice 76.02 and automatic debt repayment are entered in the downloaded document.

We post the document and look at the postings

The second option for accounting for fines is that we are the buyer and did not pay the debt for the delivery of goods to the supplier on time. The supplier charges us a fine, which we must pay. The fact of receipt of goods is reflected in the program by the corresponding document; account 60.01 shows the debt to the supplier. As in the first case, we first charge penalties for late payments by filling out the document “Operations entered manually”

We fill in the fields in the document that opens - date, content, amount. For debit we indicate the account 91.02, for credit the account is 76.02.

I would like to draw your attention to the subconto that we choose for accounts 91.01 and 91.02 in both situations considered. In this case, the directory element “Other income and expenses” is used, which must be configured correctly. We take into account fines under business contracts in income and expenses for the purpose of determining the tax base when calculating income tax, so the element in the directory must have a checkbox “Accepted for tax accounting.”

But if we are talking about fines to government agencies (fines for taxes, for violating traffic rules, etc.), then we cannot accept such fines in tax accounting. Therefore, it is recommended to create two different elements of the “Other income and expenses” directory, choosing the appropriate one for each fine. Next, we pay the supplier the debt and the amount of the fine. To do this, we will generate documents “Write-off from the current account”. We download documents from the bank or open the “Purchases”, “Receipts (acts, invoices)” tab, and find the purchase document.

And based on the document “Receipt of goods” we create a “Write-off from the current account”

In the document that opens, fill in the date, number, agreement, and DDS article.

We post the document and look at the postings

Now we will generate a document for payment of penalties. Go to the tab “Bank and cash desk”, “Bank”, “Bank statements”

And click the “Write-off” button to fill out the document “Write-off from the current account.” The type of operation will be “Payment to the supplier.” We indicate the date, recipient, amount of the fine, agreement, settlement account 76.02, article.

Now we carry out the document and look at the received transactions

Did you like the article? Subscribe to the newsletter for new materials

Add a comment

Comments

0 Zhanna 09.30.2020 19:09

Quote

Update list of comments

JComments

Administrative fine: accounting entries

Depending on the type of offense, the administrative fine can reach 60 million rubles.

| Type of offense | Amount of administrative penalty, rub. | Debit | Credit |

| A fine was assessed for work without using a cash register. | 30 000 | 99.09 | 76.02 |

| A fine was paid for working without a cash register | 30 000 | 76.02 | 51 |

Postings for fines to the Pension Fund for late submission of the report

For example, if the SZV-M report was not submitted at all, then the organization is subject to a fine of 500 rubles * number of employees.

If the company employs 30 people, then the fine for not passing the SZV-M will be 500 * 30 = 15,000. What if there are 200 or 300 employees? These are very large amounts, so it is worth submitting all documents to the relevant regulatory authorities in a timely manner. VAT dt 19.03 kt 60 VAT is reflected on acquired works (services) used for the production of goods (works, services) subject to VAT dt 19.04 kt 60 VAT is written off VAT is written off on acquired inventories used for the production of goods (works, services) , not subject to VAT dt 20, 23, 25, 29 kt 19.03 VAT on purchased works (services) used for the production of goods (works, services) not subject to VAT dt 20, 23, 25, 29 kt 19.04 VAT restoration Previously restored VAT claimed for reimbursement from the budget on acquired inventory items used for the production of goods (works, services) not subject to VAT dt 20, 23, 25, 29 kt 19.03 Restoration of VAT previously claimed for reimbursement from the budget on purchased works (services) used for the production of goods (works, services) not subject to VAT.

Accounting for claims from the supplier

If the buyer returns goods that he has already managed to capitalize, then, according to the Ministry of Finance and the Federal Tax Service, this operation refers to reverse sales. The reason for returning the goods does not matter. During this operation, the buyer is obliged to issue a tax return for the returned goods.

The buyer may make the following demands:

- refund of advance payment for unfulfilled obligations;

- issue a replacement or return of defective goods;

- eliminate defects;

- reduce the contract price;

- pay fines or penalties.

Upon receipt of a claim, the seller organization has the right to either recognize it or refuse recognition. Unrecognized claims do not affect income tax calculations.

If a claim is accepted, its consideration depends on the nature of the claim.

Failure to comply with the terms of the contract

If the terms of the contract are violated by the buyer, for example, they were not paid after shipment of the goods, then the seller has the right to demand that the buyer pay a penalty or interest for late payment. Moreover, the law does not provide for the simultaneous collection of both penalties and interest, except in cases where this is specified in the contract.

In April 2015, Podmoskovnye Prostori LLC sold a batch of materials to Podsolnukh LLC for the amount of 138,000 rubles, incl. VAT 21051 rubles. The buyer “Sunflower” was 9 days late in payment. The amount of the penalty for late payment is 0.15% of the payment amount for each day of delay.

Podmoskovnye Prostori LLC submitted a claim to the buyer for the amount of the penalty:

- 138000*0.15% *9 =1863 (rubles).

Postings at Podmoskovnye Prostori LLC:

| Dt | CT | Operation description | Sum | Document |

| 76.2 | 91.1 | Recognition of a penalty | 1863 | Claim letter |

| 76.2 | Payment of penalties by the buyer | 1863 | Payment order |