When hiring any employees, the employer must correctly understand that he is not only responsible for paying wages, but also for paying all kinds of insurance premiums, as well as reporting to government agencies.

In particular, each employer must submit quarterly calculations of paid insurance premiums so that government authorities can verify that the company conducts its activities in full compliance with established legal norms.

Dear readers! The article talks about typical ways to resolve legal issues, but each case is individual. If you want to know how to solve your specific problem

— contact a consultant:

APPLICATIONS AND CALLS ARE ACCEPTED 24/7 and 7 days a week

.

It's fast and FREE

!

That is why during the registration process it is important to correctly indicate the codes of the billing and reporting period in the calculation of insurance premiums in 2021, taking into account all the changes made.

Definition of terms

In 2021, control over the payment of all kinds of insurance premiums is carried out by the Tax Service, and therefore reports are now submitted specifically to the branches of this control body. At the same time, many do not know that in accordance with the latest changes in the current legislation, a new reporting form has been introduced, which will need to be submitted based on the results of the first quarter of 2021.

Starting from 2021, the payment of insurance premiums is regulated in accordance with the provisions of the current Tax Code. In particular, Article 423 of the Tax Code indicates that the legislation considers the calendar year as the calculation period for insurance premiums, while reporting must be submitted in the first quarter, half of the year, and also after nine months of the year.

For what period are penalties accrued in housing and communal services in 2021?

Readers are asking whether penalties are now being assessed for the moratorium period in 2021, that is, for the period from April 6, 2021 to January 1, 2021. Such a moratorium was introduced last year by Government Resolution No. 424.

In this regard, we remind you that the Supreme Court of the Russian Federation has already given an answer to the accruals in paragraph 7 of its Review No. 2, approved by the Presidium of the Supreme Court of the Russian Federation on April 30, 2020. The question was: For which periods of delay in 2021 is a penalty not subject to accrual in the event of untimely and (or) incomplete payment for residential premises, contributions for major repairs and utilities established by housing legislation?

In its response, the Supreme Court of the Russian Federation writes:

- The moratorium applies to penalties (penalties, fines) subject to accrual for the period of delay from April 6, 2021 to January 1, 2021, regardless of the billing period for the provision of utility services for which there was a delay in payment, including if the amount of the main debt was formed before April 6, 2021, unless a different deadline for the end of the moratorium is established by law or legal act.

- The penalty is subject to accrual and collection in the manner established by housing legislation, legislation on gas supply, electricity, heat supply, water supply and sanitation, and the terms of contracts for the entire period of delay, excluding the period of the moratorium .

- If the decision to collect the corresponding penalty is made by the court before January 1, 2021, then in the operative part of the decision the court indicates the amount of the penalty calculated for the period until April 6, 2020. Regarding claims for the collection of the penalty before the actual fulfillment of the obligation, the court rejects them as filed prematurely . At the same time, the court explains to the applicant the right to make such a claim in relation to the days of delay that will occur after the end of the moratorium.

When collecting debt, courts cite these clarifications and add that in the future, plaintiffs can apply for the collection of penalties (penalties) for the period from January 1, 2021, for example, in this way:

- “...In this regard, the accrual of penalties (fines) in the period from 04/06/2020 is unacceptable. At the same time, the plaintiff is not deprived of the right to make a further claim for the recovery of a penalty (fine) for the period from 01/01/2021, taking into account current regulatory legal acts" (Decision of the Arbitration Court of the Sverdlovsk Region in case No. A60-34485/2020 on recovery from the owner of non-residential premises owes payment for thermal energy).

The issue on which judicial practice really diverges is the calculation and collection of penalties from owners of non-residential premises.

There was an example above where the owner of a non-residential premises was released from penalties during the moratorium period. However, this does not prevent the higher court in the same region from collecting penalties from the owners of non-residential premises for the period of the moratorium:

- “the moratorium on the accrual of penalties (fines, penalties) is established only in relation to the owners of residential premises, while in the case under consideration the subject of the dispute is payment for the supplied utility resource to the non-residential premises of the defendant, and therefore, in this part, the moratorium does not apply to the defendant” (Resolutions of the Seventeenth Arbitration Court of Appeal in cases No. A60-5216/2020, No. A50-7642/2020, No. A50-7770/2020, etc.).

Some other courts (we can’t vouch for all of them) take into account the moratorium period to determine the amount of the penalty in relation to the owners of non-residential premises (Resolution of the Eleventh Arbitration Court of Appeal in case No. A55-25264/2019 on the collection of debt for services for the management, maintenance and routine repairs of common property of an apartment building ; Seventh Arbitration Court of Appeal in case No. A27-9838/2020 on debt collection for housing and communal services).

If you are the owner of non-residential premises in an apartment building and you need to justify to the resource supplying organization why exemption from penalties also applies to non-residential premises, take the Resolution of the Eighteenth Arbitration Court of Appeal dated November 26, 2020 in case No. A76-25179/2020 on debt collection under an energy supply contract. There, the plaintiff indicated in his complaint that the owner is not subject to the moratorium, and the court described in great detail why he thinks otherwise. Briefly it will be like this:

- As directly follows from the name and content of Resolution No. 424, its provisions apply to the provision of utility services to owners and users of premises in apartment buildings and residential buildings, that is, to both owners of residential and owners of non-residential premises.

- Paragraph 1 of Resolution No. 424 concerns the suspension of the provisions of legislation, and paragraph 2 of Resolution No. 424 concerns the application of the provisions of contracts containing provisions for the provision of public services, taking into account the suspension of certain regulations during the period of such suspension.

- The provisions of paragraphs 1 and 2 of Resolution No. 424 apply to the owners of non-residential premises of apartment buildings (in this case, the defendant in the case); on the provision of public services in such premises (including the supply of heat and electricity), including public services for the management of municipal solid waste.

- Disputed legal relations are not subject to the provisions of paragraph 5 of Resolution No. 424, since this paragraph concerns payment for residential premises and utilities and contributions for major repairs for such premises, and the defendant is the owner of non-residential premises. When stating the arguments of the appeal, the plaintiff reasonably indicated that the provisions of paragraph 5 of Resolution No. 424 were not applied to the controversial situation, however, the possibility of applying paragraphs 1 and 2 of Resolution No. 424 to them, taking into account the above, was not assessed.

- The appellate court agrees with the conclusions of the first instance court that there are grounds for suspending the collection of penalties from 04/06/2020 on the basis of Resolution No. 424, since such grounds are established in accordance with paragraphs 1 and 2 of Resolution No. 424.

Instructions for filling out the document

The new calculation form combines the previously existing documents 4-FSS and RSV-1, and therefore the following information is required when submitting reports:

- calculated contributions for social, pension and health insurance;

- a complete list of benefits paid;

- personalized information about company employees.

It is worth noting the fact that in this calculation it is not necessary to indicate information about insurance contributions made, and they will need to be reported to the Social Insurance Fund by filling out an abbreviated form.

In the new calculation form, you need to include only the calculated payments and the insurance contributions that are made from them for each employee. There are no lines in which the listed amounts are written, as well as the balances present at the beginning or end of the period, in the statements.

In this regard, there is no need to indicate in this documentation any information related to overpayments or arrears in contributions that remained at the end of previous periods.

Thus, the new calculation contains a fairly large amount of information, but filling out the entire report is optional.

Calculation of bonuses for the last year: recalculating vacations and sick leave

When calculating average earnings, bonuses based on the results of work for the year are taken into account regardless of the date of their accrual. In this regard, if, after calculating average earnings (vacation, illness, business trip, other reasons), an annual bonus was accrued relating to the billing period, it is necessary to recalculate the accrued amounts.

When recalculation is made, premiums for the previous period are taken into account if:

- they are accrued at the end of the year;

- this year refers to the billing period.

Example 2

Let's add the conditions of the first example. In April 2021 Semenov S.S. paid annual bonuses: for 2021 - 5,000 rubles, for 2021 - 30,000 rubles. Since the bonus for 2021 does not relate to the holiday pay calculation period, it does not need to be taken into account when recalculating. But the bonus for 2021 should be included in the calculation of average earnings in full:

Average earnings have increased, which means Semenov needs to pay extra vacation pay.

Time limits have been established for the recalculation of wages in case of underpayment. Unpaid accruals must be paid to the employee no later than the next payday after the changes are made.

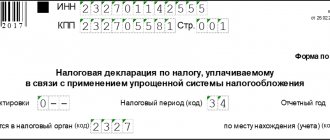

Codes of the billing and reporting period in the calculation of insurance premiums in 2021

Submission of a single calculation for insurance premiums is carried out every quarter, and this is done before the 30th day of the month that follows the reporting period. In this case, it is necessary to indicate the code of a particular period, taking it in Appendix No. 3, which is published to the adopted Procedure for the preparation of such documents.

The codes themselves look like this:

It is worth noting the fact that these are not all the codes that need to be indicated in the process of preparing such documentation. In addition, when preparing a single settlement, you will also have to fill out the codes for the category of the insured person, codes for the types of various papers, as well as a number of other numbers assigned in accordance with certain regulations.

Procedure and form of submission

The calculation must be submitted, as mentioned above, before the 30th day of the month following the first, second and third quarter. These deadlines are approved by current legislation and are specified in paragraph 7 of Article 431 of the Tax Code, which came into force in 2021.

Thus, due to the introduction of new legislation after the first quarter, reporting must be submitted:

All companies and entrepreneurs whose activities involve more than 25 people must send documentation exclusively in electronic form using telecommunication channels. If the total number of employees is less than 25 people, then in this case reporting is submitted exclusively on paper. This feature of filing a single calculation is prescribed in paragraph 10 of Article 431 of the Tax Code.

The Tax Service will accept the calculation in accordance with the new form, and it must be submitted to the branch that is located at the location of the company or at the place of registration of a private entrepreneur.

If the company has any separate divisions that make payments to individuals, then in this case they will also have to submit reports, but to those tax departments that are located on their territory. Moreover, in this situation there is no difference whether the branch has its own current account or a separate one.

The first section of the document must be completed by all persons who pay funds to individuals. In particular, you need to provide here summary information on the amounts that must be paid during the billing period for pension, social and medical contributions.

It is also in this section that you need to indicate a list of amounts that are sent to the Pension Fund in accordance with the additional tariff, as well as those contributions that are made in order to provide employees with additional social insurance. Each such value must initially be indicated in its entirety, and only then is it indicated for the last three months, broken down by all months.

In addition, for each individual type of contribution, a specific budget classification code will be required, and this is a mandatory requirement, thanks to which Tax Service employees can record debts under certain codes on the payers’ personal account.

It is also necessary to fill out the second section indicating personalized information for all insured persons, while filling out the second section is mandatory only for those entrepreneurs who operate in the field of organizing farms.

Responsibility for failure to meet deadlines

In case of failure to comply with the established deadlines for the first quarter, the Tax Service has the right to bring the company or private entrepreneur to administrative liability, imposing an appropriate fine on it. Today, the standard fine amount is 5% of the total amount of insurance premiums that must be paid, but it is worth noting the fact that when calculating this fine, the tax authorities will remove the amount that was transferred on time.

Over time, the 5% will continually increase, increasing over and over again each month, but ultimately the amount cannot add up to more than 30% of the amount due. On the other hand, current legislation also establishes a minimum threshold for such fines, and it is 1000 rubles.

If, within the established time frame, the entrepreneur pays only a certain part of the contributions, then in this case the amount of the fine is calculated as the difference between the total amount specified in the documentation and the one that was actually transferred to the budget.

Vladimir Ilyukov

Determining the billing period is the first task that the accountant must solve when calculating vacation or in other cases of maintaining average earnings. All cases when an absent (non-working) employee retains the average salary are established in different places of the Labor Code of the Russian Federation. Here are some of them.

- Annual paid leave, Art. 114 Labor Code of the Russian Federation.

- Compensation for unused vacation, Art. 126-127 Labor Code of the Russian Federation.

- Additional study leaves, Art. 173-174, 176 Labor Code of the Russian Federation.

- Business trips, art. 167 Labor Code of the Russian Federation.

- Downtime due to the fault of the employer, Art. 157 Labor Code of the Russian Federation.

- Advanced training, Art. 187 Labor Code of the Russian Federation.

- Donation of blood and its components (donor days), art. 186 Labor Code of the Russian Federation.

- Severance pay in connection with dismissal due to liquidation of the organization, reduction of staff (number) of employees, conscription of the employee for military service; Art. 178 Labor Code of the Russian Federation.

- And other.

To determine the amount of average wages (average earnings) for all these cases, a single procedure has been established, Art. 139 Labor Code of the Russian Federation. At the same time, according to paragraph. 7 tbsp. 139 of the Labor Code of the Russian Federation, the specifics of calculating average earnings are regulated by Decree of the Government of the Russian Federation dated December 24, 2007 No. 922 “On the specifics of the procedure for calculating average wages”, hereinafter Resolution No. 922.

Upon superficial analysis, it seems that the phrase “... or for a period exceeding the billing period

"seems unnecessary, erroneous, and illogical. This conclusion can be reached if by “period exceeding the billing period” we mean months outside the base billing period. If you count from the month of the occurrence of the event in which the average earnings are saved, then this is the 13th, 14th or other month.

This is a misunderstanding. Here, a period exceeding the main billing period means the entire period preceding the period of maintaining average earnings

. Let's consider a fairly typical situation for a female employee of an organization.

- 06.2016

. Employment date. - 11.2016 to 16.04.2017

. Maternity leave period; 140 calendar days. The child was born on 02/07/2017. - 04.2017 to 08.07.2018

. The period of parental leave is up to 1.5 years. We believe that the employee did not take out maternity leave for a child under three years of age. - 08.2018

. From this date, the employee goes on another paid leave.

The example data is illustrated in the following figure.

In this figure, the months of the main billing period are shown on a yellow background. This is the period from 08/01/2017 to 07/31/2018. The period that exceeds the main billing period is the period from November 1, 2016 to July 31, 2018. The hexagons representing the months of this period are filled with gray.

The calculation period for calculating the employee’s annual leave includes the months from 11/01/2015 to 10/31/2016. They are indicated by blue hexagons.

Situation 4: accruals are available only in the month of going on vacation

Verbatim quote, paragraph 7 of Resolution No. 922.

“If the employee did not have actually accrued wages or actually worked days for the billing period and before the start of the billing period, the average earnings are determined based on the amount of wages actually accrued for the days actually worked by the employee in the month of occurrence of the event that is associated with maintaining the average earnings"

For example, an employee was hired on April 10 of the current year, and on April 25 he was given paid leave in advance. A more realistic situation is when an employee goes on a business trip, for example, on the day he is hired. The billing period is equal to the period from April 10 to April 24 inclusive.

Situation 5: no billing period

Clause 8 of Resolution No. 922 provides for a rather rare situation.

“If the employee did not have actually accrued wages or actually worked days for the pay period, before the start of the pay period and before the occurrence of an event that is associated with maintaining the average earnings, the average earnings are determined based on the tariff rate established for him, salary (official salary) "

It is difficult to imagine a case where an employee goes on another vacation on the day he is hired, but theoretically it is possible. A more realistic situation is when an employee goes on a business trip, for example, on the day he is hired. In this case, there is no billing period.

Conclusion

The article discusses situations in relation to the standard duration (12 calendar months) of the billing period. However, everything said is also true for any other duration of the billing period. It is only important to remember that if an organization applies a calculation period of a duration other than 12 calendar months, then the corresponding decision must be reflected in the collective agreement or in a local act, paragraph. 6 tbsp. 139 Labor Code of the Russian Federation.

It is not necessary that all months of the billing period be fully worked out. When calculating annual leave or compensation for unused leave, the average monthly number of calendar days in the calculation period is used to determine average earnings. A separate article will be devoted to this issue.

If necessary, the billing period is shifted by 12 months only if there are no accruals in the base billing period; situation 2. In other cases, it is shifted back to the first month inclusive, in which there are accruals taken into account in the average earnings, situation 3.

When insurance premiums were transferred under the control of tax authorities in 2021, a new chapter 34 was added to the Tax Code of the Russian Federation, regulating their calculation and payment procedure. It reveals the concepts that define both reporting periods and billing periods in relation to insurance premiums. In this article we will tell you about the billing period for insurance premiums in 2021, and consider the payment deadlines.

Wherein:

- The reporting period is a quarter, half a year, etc.;

- and the calculated year is the calendar year.

During the billing period, accounting forms the basis for future accruals for insurance premiums. Each billing period is represented by four reporting periods, based on the results of which interim results can be summed up, as well as reporting can be submitted to the tax authority.

What time is excluded from the billing period?

Exclude from the billing period:

- periods during which the employee, by law, retained his average earnings (except for breaks to feed the child). For example, the time spent on a business trip (Article 167 of the Labor Code of the Russian Federation);

- time of illness;

- maternity leave time;

- period of leave without pay;

- the time when the employee was provided with additional paid days off to care for disabled children and people with disabilities since childhood;

- the period when the employee did not work due to downtime due to the fault of the organization or for reasons beyond the control of the organization and the employee (for example, due to the suspension of the organization or workshop);

- the time when the employee did not participate in the strike, but due to it could not perform work;

- other periods when the employee did not work for reasons provided for by law.

This procedure is provided for in paragraph 5 of the regulation approved by Decree of the Government of the Russian Federation of December 24, 2007 No. 922.

An example of determining the billing period for calculating average earnings. During the billing period, the employee was sick, on a business trip and on vacation at his own expense

Organization employee A.S. Kondratyev went on a business trip on January 15, 2015. For the time when the employee was on a business trip, the organization retains his average earnings (Article 167 of the Labor Code of the Russian Federation).

The calculation period for determining average earnings for business trip days is from January 1 to December 31, 2014. Kondratiev did not work it out completely:

- from March 14 to March 24, 2014, he was on a business trip;

- from June 1 to June 29, 2014 – on vacation at your own expense;

- from August 28 to September 5, 2014 – I was sick.

The time when the employee was sick, on vacation or on a business trip, the accountant excluded from the billing period. Thus, the accountant determined the average salary retained by Kondratiev for the duration of the business trip based on the billing period, which includes the time:

- from January 1 to March 13, 2014;

- from March 25 to May 31, 2014;

- from June 30 to August 27, 2014;

- from September 6 to December 31, 2014.

Situation: is it necessary to exclude absenteeism from the calculation period for calculating average earnings?

Answer: no, it is not necessary.

As a general rule, the duration of the billing period is 12 calendar months preceding the month in which the employee retains his average earnings (Part 3 of Article 139 of the Labor Code of the Russian Federation).

In the list of periods excluded from the calculation period, there is no time when the employee did not come to work of his own free will. Only periods when the employee was released from work in accordance with the law or with the knowledge of the organization’s administration are excluded from the billing period (clause 5 of the regulation approved by Decree of the Government of the Russian Federation of December 24, 2007 No. 922). Therefore, absenteeism should not be excluded from the calculation period. This point of view is shared by representatives of the Russian Ministry of Labor and the Russian Ministry of Health.

Situation: is it necessary to exclude from the calculation period when determining average earnings the time when the employee worked part-time while maintaining the right to child care benefits?

Answer: no, it is not necessary.

As a general rule, the duration of the billing period is 12 calendar months preceding the month in which the employee retains his average earnings (Part 3 of Article 139 of the Labor Code of the Russian Federation).

It is necessary to exclude from the billing period, in particular:

– periods in which the employee, according to the law, retained his average earnings;

– other periods when the employee did not work for reasons provided for by law.

This procedure is provided for in paragraph 5 of the regulation approved by Decree of the Government of the Russian Federation of December 24, 2007 No. 922.

If during maternity leave an employee worked part-time, then she retained the right to a child care benefit for up to 1.5 years and a compensation payment until the child reaches the age of 3 years in the amount of 50 rubles. per month.

That is, at that time the employee received:

– child care allowance up to 1.5 years;

– compensation payment until the child reaches the age of 3 years in the amount of 50 rubles. per month;

- salary.

This procedure follows from Part 3 of Article 256 of the Labor Code of the Russian Federation.

While working part-time, the employee continues to be on maternity leave (Article 256 of the Labor Code of the Russian Federation). However, this period does not fall under any of the items in the list of periods excluded from the calculation period, since the employee actually worked. Therefore, the time when the employee worked part-time while on maternity leave does not need to be excluded from the calculation period.

At the same time, the amount of benefits for child care up to 1.5 years and compensation payment until the child reaches the age of 3 years in the amount of 50 rubles. per month do not include in the calculation of average earnings. Take the salary amount into account when determining average earnings. This approach is specified in paragraph 5 of the regulations approved by Decree of the Government of the Russian Federation of December 24, 2007 No. 922.

An example of determining the billing period when calculating average earnings during a business trip. During the billing period, the employee was on maternity leave and worked part-time

Ivanova I.A. has been working in the organization since 2009. From January 1, 2014, the employee was granted maternity leave, during which from March 1, 2014 to January 26, 2015, she worked part-time (6 hours a day) while maintaining child care benefits up to 1. 5 years.

On January 27, 2015, the employee interrupted her maternity leave and returned to work full time. From January 28 to February 2, Ivanova was sent on a business trip.

The billing period is 12 calendar months preceding the month the business trip began, that is, the period from January 1 to December 31, 2014 inclusive. During this period:

– the period of time from January 1 to February 28, 2014 (inclusive) is excluded from the calculation period, since then the employee did not work due to maternity leave;

– the period of time from March 1 to December 31, 2014 (inclusive) is taken into account in the billing period, since during this time Ivanova worked part-time.

Calculation and reporting period for insurance premiums

The reporting period is recognized as:

- first quarter;

- half year;

- nine month;

By the way, for entrepreneurs who carry out their activities independently, without hiring employees and pay contributions only “for themselves,” there is no reporting period. In addition to entrepreneurs, such taxpayers include lawyers, notaries, etc. There are no specific deadlines for paying contributions during the year; they can pay the entire amount no later than December 31 of the accounting year.

If entrepreneurs have hired employees, they make deductions in the same manner as for organizations and submit reports at the end of each reporting period.

When an organization registered as a legal entity after the beginning of the year, the first billing period is set to the period from the date of registration to the end of the year.

Example 1.

Continent LLC received a certificate of registration of a legal entity on April 13, 2021. Thus, the billing period for Continent LLC will be as follows: from April 13, 2021 to December 31, 2017. And the subsequent billing period will be equal to the full 2020 calendar year.

If the liquidation (reorganization) of a company occurs before the end of the calendar year, the end of the billing period will be the day the liquidation of the company or its reorganization is completed.

Example 2.

Romashka LLC filed documents for liquidation. On November 18, 2017, Romashka LLC received an extract from the Unified State Register of Legal Entities. Accordingly, the billing period for insurance premiums will be as follows: from January 1, 2017 to November 18, 2021 inclusive.

In the event that the creation of a legal entity occurred after the beginning of the year, and liquidation or reorganization occurred before its completion, the calculation period should be recognized as the period from registration to liquidation.

Example 3.

Premier LLC received a certificate of registration on April 5, 2017, and an extract from the Unified State Register of Legal Entities on liquidation on November 1, 2021. The calculation period for strass contributions will be as follows: from April 5, 2021 to November 1, 2021 inclusive.

Thus, in the billing period, at the end of each month, contributions are calculated based on the results of each month, based on the salary or other remuneration paid to employees. In this case, payments are taken into account from the beginning of the billing period to the end of the reporting month. The calculation is made taking into account the tariff rate, existing allowances or benefits to the tariff rate, subtracting the amount of the insurance payment calculated from the beginning of the billing period until the previous month.

Example 4.

Continent LLC paid salaries and bonuses to employees:

- January 2021 – 120,000 rubles

- February 2021 – 140,000 rubles

- March 2021 – 130,000 rubles

At the end of January, the accountant calculated and paid contributions to compulsory pension insurance at a rate of 22%:

- 120,000 x 22% = 26,400 rubles

Based on the results of February, the accountant made the following calculation:

- (120,000 + 140,000) x 22% – 26,400 = 30,800 rubles

At the end of March, the accountant made the following calculation:

- (120,000 + 140,000 + 130,000) x 22% – (26,400 + 30,800) = 28,600 rubles

Deadlines for submitting reports on insurance premiums

At the end of each reporting period, organizations are required to submit reports on insurance premiums to the tax authority. It is submitted no later than the 30th day of the month following the reporting period. That is, the report for the 1st quarter must be submitted no later than April 30. In the event that the last day of delivery falls on a weekend, the deadline is moved to the first next working day. So, in 2021, April 30 is a day off, and May 1 is a holiday, then the deadline for delivery is postponed to May 2.

The report is provided electronically or in paper form, it depends on the average headcount of the organization for the previous year. For example, if in 2021 it was more than 25 people, then the report will need to be submitted only in electronic form. Otherwise, the company will face penalties of 200 rubles. If the average headcount is less than 25 people, the company itself chooses the method of reporting. There will be no penalty for providing the report in non-electronic form.

How to calculate wages using a salary system

The salary system is a type of time-based wage system. It implies that in the case of a fully worked month, the employee receives a fixed amount of money, that is, a salary. As a rule, office workers work under such conditions: managers, administrators, accountants, etc.

If the month is not fully worked, then the employee is paid a portion of the salary proportional to the time actually worked.

Example 1

The employee's salary is 45,000 rubles. November was not fully worked out: from November 12 to 18, the employee went on vacation, and from November 27 to 30, he took sick leave.

The accountant saw that according to the time sheet, the employee was on duty for 12 working days. There are a total of 21 working days in November. Thus, the employee’s salary for November, not counting vacation pay and sick pay, is 25,714 rubles (45,000 rubles: 21 days x 12 days).

Responsibility for violations in reporting

If, when checking the report, the inspector finds an error, the company will be notified of its elimination in electronic or paper form. At the same time, the period established for eliminating the error is 5 working days when sending an electronic notification and 10 when sending by mail. If the company, for any reason, ignores the inspector’s requirement, the calculation receives the status of unrepresented. For this, the company will be fined in the amount of 5% of the calculated insurance premiums for each month of delay.

The amount of the fine cannot exceed 30% of contributions, but it cannot be less than 1000 rubles.

The legislative framework.

A debit card is a convenient tool for everyday payments. To get the maximum benefit from its use, you need to know some concepts that will allow you to adjust your actions, fulfill the bank’s conditions and receive bonuses.

The calculation of bonuses, such as free service, cash back, accrual to the balance, etc., for the Tinkoff card product is based on payment transactions for a certain period.

When does the billing period begin?

The start date of this period is individual for each client. It depends on the day on which the statement is generated. You can find out the date by calling the customer service center, in your online bank or in the statement you have already received. The date indicated after the phrase “for the period from...” will be the beginning of the settlement period. In some cases, it may begin at the beginning of a new month.

This date can be changed by calling the bank's hotline (the offer is considered individually).

What is the billing period for?

The debit card billing period for calculating the annual service.

The cost of servicing a TKS debit card account is 99 rubles. per month. However, if during the spending period the cardholder opened a deposit, had an active cash loan in rubles or an account balance of 30,000 rubles or more, then this money will not be charged from him.

For the first month, the client will be charged the cost of service. For subsequent months, this will depend on compliance with the specified conditions.

It turns out that if you simply keep at least 30,000 rubles in your account, you can use it for free. Another advantage is that if you make a deposit, you can also receive interest. It is important to know that this balance will be taken into account at the end of each day, and if on one day the required amount turns out to be less than even a penny, then the client will be charged a service charge of 99 rubles.

There was no income before the billing period

It is possible that even before the payroll period the employee did not actually have days worked (accrued wages). Then, when calculating, take into account the days worked in the month of the occurrence of the event, which is associated with the preservation of average earnings before the occurrence of this event. This rule is enshrined in paragraph 7 of the regulations approved by Decree of the Government of the Russian Federation of December 24, 2007 No. 922.

An example of determining the billing period for calculating average earnings. The calculation period consists entirely of the time that needs to be excluded. Before this, the employee had no actual days worked

Economist A.S. Kondratyev has been working in the organization since August 13, 2015. From October 22 to October 30, 2015, he was on a business trip. During the business trip, he retains his average salary (Article 167 of the Labor Code of the Russian Federation).

The calculation period for determining average earnings for business trip days is from August 13 to September 30, 2015.

During the entire billing period, Kondratiev did not work:

- from August 13 to August 31, 2015, he was on a business trip;

- from September 1 to September 30, 2015 - was on study leave.

The accountant excluded this time from the billing period. The accountant cannot take the period preceding the settlement period, since Kondratyev did not work in the organization at that time. The average salary that an employee retains during a business trip was determined by the accountant for the period from October 1 to October 21, 2015.

The calculation period for calculating interest on the account balance.

You can receive additional interest without even opening a deposit. If during the expendable period the user has from 0 to 300,000 rubles stored on the card account, then TKS charges 8% (now the income has been increased to 14%).

If the amount turns out to be more than 300,000 rubles, then the client will be able to receive only 4% on the balance. The bank will charge the same interest on the balance if no payment transactions were made on the card account during the billing period. It is worth knowing that only transactions of purchasing goods using plastic or its details are taken into account. Transactions such as payments for mobile communications, Internet, transfers to electronic accounts and other transfers will not be counted. If the transaction has gone through, but has not yet been processed by the bank, then it is also not protected.

Accrued interest is paid on the date the statement is generated.

Calculation period for accruing the cash back bonus.

Cash back is credited on each last day of the spending period. At the same time, its size cannot exceed 3,000 rubles. (everything higher is burned). If the client has several cards and the total cash back exceeds this threshold, then it will be credited in proportion to the money spent.

Cash back is calculated based on:

- 1% for all payment transactions during the settlement period (max. RUB 3,000)

- 5% for increased bonus categories (they change at the discretion of TKS, for example, in October, November and December 2014 - gasoline, automobile services, pharmacy chains, transport) (max. RUB 3,000)

- Up to 30% on special offers from bank partners (you can activate them in your online account or in the application for your mobile device). If a refund was made under a special offer, and the client has already received a reward, the bank will write off the accrued bonuses from the account. The maximum bonus amount can be 6,000 rubles. If a client has several TKS cards, and the total amount of bonuses for them exceeds this threshold, then bonuses will be awarded in proportion to 6,000 rubles. on all cards.

For example, if you spend about 10,000 rubles per month on a card. and have a balance of 30,000 rubles, then in a year you can return about 4,700 rubles.

There was no earnings in the billing period

In practice, it happens that the entire billing period consists of time that needs to be excluded. In this case, for calculation, take the previous period of time equal to the calculated one (clause 6 of the regulation approved by Decree of the Government of the Russian Federation of December 24, 2007 No. 922).

An example of determining the calculation period for calculating average earnings, when it consists of time that needs to be excluded

Secretary E.V. Ivanova has been working in the organization since 2009. From October 21 to October 23, 2015, she underwent a medical examination. During the medical examination, her average earnings are retained (Article 185 of the Labor Code of the Russian Federation).

The calculation period for determining the average earnings for the days of passing the medical examination is the time from October 1, 2014 to September 30, 2015.

During the entire billing period, Ivanova did not work:

- from February 21 to July 10, 2014, she was on maternity leave;

- from July 11, 2014 to October 10, 2015 – on parental leave.

The time when the employee was on maternity leave and child care leave was excluded from the accounting period by the accountant. Thus, the entire calculation period consists entirely of the time that needs to be excluded. The average salary that Ivanova retains during the medical examination was determined by the accountant for the period from February 1, 2013 to January 31, 2014.

Billing and reporting periods

Billing period

for insurance premiums, in general,

the calendar year

(read about exceptions below)

- clause 1 of Art.

10 of the Law of July 24, 2009 No. 212-FZ. For example, from

January 1 to December 31, 2010

Reporting periods

are recognized (see

paragraph 1 of Article 10 of the Law of July 24, 2009 No. 212-FZ):

· first quarter;

· half a year;

· nine months of the calendar year;

· calendar year.

In some cases (when an organization is created, liquidated and/or reorganized within a calendar year), the reporting period is determined differently.

Features (rules) of determining the billing period in individual cases

If the organization was created after the beginning of the calendar year, the first billing period for it is the period from the date of creation until the end of this calendar year (Clause 3, Article 10 of Law No. 212-FZ of July 24, 2009).

For example, if an organization was created on March 15, 2010, then the first billing period for it will be the period from March 15 to December 31, 2010.

If the organization was liquidated or reorganized before the end of the calendar year, the last billing period for it is the period from the beginning of this calendar year until the day the liquidation or reorganization was completed (clause 4 of article 10 of the Law of July 24, 2009 No. 212-FZ).

For example, the liquidation of the organization ended on November 17, 2010 ,

therefore, the last billing period for it will be the period from January 1 to November 17, 2010.

If an organization created after the beginning of the calendar year is liquidated or reorganized before the end of this calendar year, the calculation period for it is the period from the date of creation to the day the liquidation or reorganization is completed (Clause 5 of Article 10 of the Law of July 24, 2009 No. 212-FZ) .

Example: an organization was created on February 8, 2010 and reorganized on September 23, 2010. In this case, the billing period for this organization is the period from February 8 to September 23, 2010.

Please note that according to paragraph 6 of Art. 10 of the Law of July 24, 2009 No. 212-FZ

These rules do not apply to organizations from which one or more organizations are separated or joined.

What has changed compared to the unified social tax?

The period, which for the purpose of calculating the unified social tax was called the tax period, for the purpose of calculating insurance premiums is called the billing period.

LiveInternetLiveInternet

Your main task at this stage is to study, study and study again. You read product guides, attend lectures, and communicate with more “senior” friends. In general, you will learn a lot of new and interesting things.

And then one fine day, you decide to buy a jar of some cream or balm - for yourself. You should try it yourself to see if the cosmetics that are being praised so much are really good. And this, by the way, is a very important rule of network marketing: always use the products you distribute yourself.

You come to the warehouse, open the price list and find the product you like there. Then look at the price indicated in the “Warehouse price” column. Now please note that each product, in addition to the ruble cost, also has a so-called “points” price.

What are Distributor Points (points for purchases)

When you come to the warehouse and make a purchase, Distributor Points are entered into the computer using your registration number. They are subsequently used to calculate rewards.

To better understand what you are about to read, let's draw a table like this.

| APRIL | |||||

| Registration number | Qualification | LO | GO | RO | NRO |

| Your registration number | Consultant | 50 | 50 | 50 | 50 |

Table of parameters for your work in April.

We will write down your registration number and Qualification in the first and second columns. Now let's start filling out the four remaining columns.

What is a billing month?

Let's assume that in April you personally purchased products worth 50 points. The month for which your remuneration will be calculated is called the billing month. However, the billing month is not always equal to the calendar month. July-August and December-January are considered one billing month. Thus, in a calendar year there are not 12, but 10 billing months.

In the future, unless otherwise specified, by month we mean the billing month, and not the calendar month.

What is Personal Volume (PV)

The volume of product purchases (in points) made by you personally in the billing month is called Personal Volume (PV). So, for the billing month of April you purchased products for 50 points, therefore, your LO was 50. Let’s enter this number in the LO column.

What is a tree (network)

You already know that a Distributor can attract other people to distribute products, and they, in turn, can do the same.

An organization consisting of Distributors who were recruited by you personally and all your Distributors is called your tree (network). The people you personally signed make up your first generation. People who were signed by your first generation Distributors are your second generation and so on. Generations are sometimes also called levels .

Who is a Sponsor

When filling out the Agreement, in the “Your direct sponsor” column, you enter the name and registration number of the Distributor from whom you learned about the products offered and the marketing plan. Distributors of your first generation, when filling out the Agreement, will indicate you as a Sponsor, because it was you who told them about Mirra-Lux. Since your remuneration as a Distributor depends on sponsorship activities, you are interested in learning more about the product, how to use it, distribution rules, and transfer this knowledge to the Distributors you recruit.

Why is the person who signed me my Sponsor, because he didn’t give me any money?

Here we are talking about information sponsorship. He gave you a more valuable thing - information where you can earn this money. As the hero of one famous work would say, he gave you “the key to the apartment where the money is.”

Is it possible to change my Sponsor?

No. The Mirra-Lux marketing plan does not provide for the possibility of changing the Sponsor.

What is a personal group

A personal group is all the Distributors whom you yourself recruited to work and of whom you are a direct Sponsor. In other words, your personal group is your first generation.

What is group volume (GO)

Group volume (GP) is the sum of the Personal Volume (PV) of the Distributor himself and the PV of his first generation of Distributors.

But if a Distributor has a LO < 50 in a given month, then the sum of the LO of Distributors of his first generation goes into the LO of a higher-level Distributor with a LO greater than or equal to 50 points.

Since you do not yet have your own Distributors, your Group Volume is equal only to your Personal Volume. In the GO column of the table of parameters of your work in April, we enter 50 points.

What is a reward system

Any Distributor has the opportunity to purchase products from the company’s warehouses at wholesale prices, which are on average 30% less than recommended retail prices. The recommended retail price is also indicated in the price list, and this is the price at which the company recommends that you sell the product.

What does it mean, the company recommends? Why can't I sell at a higher price?

If you find someone willing to pay 100 rubles for a jar of cream that costs 30, please sell it! But you should not sell products at prices lower than those recommended by the company, because by doing so you undermine the business of other Distributors. We will talk more about the Rights and Responsibilities of an Independent Distributor later.

This means that your income, at a minimum, includes that same 30% of the cost of the products you sold (this is income from retail sales). But if this were the only point of your income, everything would be very simple and uninteresting: “bought cheaper - sold more expensive.” In network marketing, income from retail sales is by no means the only one: there is a developed system of rewards that are awarded based on the results of work for the billing month.

The Mirra-Lux marketing plan considers the following types of remuneration:

- PLP

– Bonus for fulfilling a personal implementation plan;

- PRG

- PRG – Prize for the development of a personal group;

- LVM

– Master’s Leadership Reward;

- SB

– Sponsorship Bonus;

- IS

– Integral Bonus.

The first two types of income can be received by any Distributor, the last three - only by Masters. All listed rewards are calculated by a computer once per billing month according to strictly defined rules.

What is a personal plan

The Company does not require its Distributors to make a certain monthly volume of purchases. However, in a marketing plan there is such a thing as a personal plan.

A personal plan is a volume of personal purchases for which you can qualify for accrual of rewards. Each Distributor is given a personal plan of 50 points per month. That is, in order to receive a reward, you need to have a Personal Volume equal to or exceeding 50 points in the billing month.

Any rewards are awarded to the Distributor provided that his Personal Volume (PV) is at least 50 points. Otherwise, the Distributor's remuneration in the billing month is zero.

When calculating all rewards, the Distributor's Qualification recorded at the beginning of the billing month is used.

These two points are very important, so read them again and try to remember them.

What remuneration does the Consultant receive?

If you have fulfilled your personal plan, your remuneration consists of the Personal Sales Premium (PLP) and the Group Development Bonus (PDG).

| PLP | 5% of your LO* |

| PRG | 5% from LO First Generation Consultants |

* - note: the Consultant’s PLP does not include the very first 50 points of his Personal Volume (PV).

Let's go back to the example and calculate your remuneration. In April, your LO was 50 points. Since while you are working alone and you do not yet have first-generation Consultants, your reward will be 5% of 50 points (PLP), which is equal to 2.5 bonus points. Just don’t forget that since these are the very first 50 points from the moment you started working at Mirra-Lux, you will not receive PLP from them. For all subsequent points you will certainly receive a Personal Selling Award (PSA).

What are reward points

Do not confuse distributor points (points for purchases) and premium points.

Premium points are the points in which the reward accrued to you is expressed. The cost of one bonus point is five rubles. Feel free to multiply 2.5 bonus points by 5 rubles. It turns out 12 rubles 50 kopecks.

What is Rank Volume

The Rank Volume (RO) of a Consultant is the monthly volume of distributor points accumulated by you and all Distributors of your first generation.

For now, just take note, and we will definitely return to this issue: The Rank Volume of the Manager and Director is calculated a little differently. The Rank Volume of an Executive also includes points scored by Distributors of his second generation, and for a Director, the Rank Volume also includes points scored by Distributors of his third generation.

However, if your Personal Volume (PV) in the billing month is less than 50 points, then your Rank Volume is equal only to PV, and the sum of PV of your first generation Distributors goes to the PV of a higher-level Distributor with PV greater than or equal to 50 points.

Your PO for April was 50 points, and you do not yet have first-generation Distributors, so your PO for April is 50 points. We will note this in the table of parameters for your work in April.

What is Accumulated Rank Volume

There was one column left blank in the table of parameters of your work in April - NRO (Accumulated Rank Volume). Accumulated Rank Volume is your piggy bank, where your Rank Volume (RO) is deposited every month.

Accumulated Rank Volume (AVR) is the amount of RO for all months of your work as an independent Distributor of Mirra-Lux.

The accumulated Rank Volume does not in any way affect the accrual of rewards in the billing month, but the increase in your Qualification depends on it.

In our example, since you have only been working for the first month and have no savings yet, your NRO is equal to the RO for April and is 50 points. Let's put this number in the table. Next month (May) the Rank Volume for May will be added to these 50 points.

Is it possible to work alone

It is possible, and the marketing plan allows for this option. But the question is different: in this case, will you be able to effectively use all the wealth of opportunities provided by the very idea of network marketing? Let's look at a simple example, and you can answer this question for yourself. Precisely for himself, because in MLM everyone determines for themselves what they want to achieve. Perhaps it is enough for you that you simply have the opportunity to buy good cosmetics for yourself and your family members, and at a wholesale price. This is your complete right. But let's return to our question.

Let's assume that you work alone, and every month you buy 50 points worth of products. Having the Consultant Qualification, you receive a reward - a Personal Sales Award in the amount of 2.5 bonus points monthly (12 and a half rubles). However, I would like to note that in April you will not receive the Personal Sales Award, since it does not include the very first 50 points of the Distributor’s Personal Volume.

Now let's see how things will go if you invite five assistants in May. Agree, it’s not so difficult to find five people by looking in your notebooks and remembering your friends. Now you have your own network.

For the convenience of calculations, let’s assume that they start working the same way as you, and in May each of them purchased products worth 50 points. You yourself, like in April, also made a purchase for 50 points. Let us now fill out your May table.

| MAY | |||||

| Registration number | Qualification | LO | GO | RO | NRO |

| Your registration number | Consultant | 50 | 300 | 300 | 350 |

| 1 | Consultant | 50 | 50 | 50 | 50 |

| 2 | Consultant | 50 | 50 | 50 | 50 |

| 3 | Consultant | 50 | 50 | 50 | 50 |

| 4 | Consultant | 50 | 50 | 50 | 50 |

| 5 | Consultant | 50 | 50 | 50 | 50 |

Table of parameters for your work in May.

In the Personal Volume (PV) column – points scored by you personally in May (50). In the Group Volume (GO) column we enter the number of points scored by you and your first generation Distributors (50+50+50+50+50+50=300). Your Rank Volume for May, since you are a Consultant, includes the points accumulated by you and your first generation Distributors (50 + 50 + 50 + 50 + 50 + 50 = 300). In the NRO column (Accumulated Rank Volume) we enter the Rank Volume for May (300 points) plus 50 points that were already in your “piggy bank” (NRO based on the results of April).

Now let's calculate your remuneration in May. In addition to the Personal Sales Award (2.5 bonus points), you will receive another 5% of the LP of each Consultant of your first generation (Group Development Award). It will amount to 12.5 bonus points. So, in May you earned 15 points, which is already noticeable - 75 rubles. And this is far from the limit. We have already noted that with each step up the career ladder, your remuneration will increase. The next step is the Leader.

How to become a Manager

As soon as your Accumulated Rank Volume reaches 500 points, you will immediately be awarded the Manager Qualification (of course, based on the results of the billing month).

I received an “Individual Report...” and I can’t understand how the GO and RO were calculated for me. Can you explain please. My network is shown in the picture.

First, let's deal with your Group Volume (GO). It consists of your (K1) Personal Volume (LO) and the LO of Distributors K2, K3, K4, K5, K6. In addition, since Distributor K2 did not fulfill his personal plan (his LO<50), the sum of the LO of the Distributors of his first generation (K7 and K8) goes to your GO (since you are a higher-ranking Distributor with a LO greater than or equal to 50 points). In turn, Distributor K8 also did not fulfill his personal plan, so the amount of LO of Distributors of his first generation (K11 and K12) also goes to your GO. In other words, we can say that all these people ( K7, K8, K11 and K12) seem to be rising into your first generation, but only in the calculations of a given month! So, your GO = 203 + 27 + 15 + 50 + 37 + 16 + 38 + 23 + 60 + 6 = 475.

Your Rank Volume (PV) as a Consultant includes your Personal Volume (PV) and the PV of your first generation Distributors. For the same reason as in the GO calculations, in addition to the LOs of Distributors K2, K3, K4, K5, K6, your RO also includes the LOs of Distributors K7, K8, K11 and K12. Therefore, your Rank Volume is 475 points.

To avoid a misleading impression, I will note that Group Volume (GV) is not always equal to Rank Volume (RV), although this is indeed true for Consultants.