Who must submit 2-NDFL for 2016

Organizations and individual entrepreneurs that are recognized as tax agents for personal income tax must withhold and transfer to the personal income tax budget from income paid to individuals. In addition, tax agents are required to report this to the Federal Tax Service at the end of each year. For these purposes, 2-NDFL certificates are annually submitted to the tax inspectorates.

It is worth noting that from 2021, another type of income tax reporting has been introduced - quarterly calculations of 6-NDFL. However, they do not replace reporting in the form of 2-NDFL certificates. The fact is that in 6-NDFL calculations, data is grouped as a whole by tax agent. The 2-NDFL certificate, in turn, is of a purely individual nature, since the certificate must be filled out personally for each individual who received income. Also see “Annual calculation of 6-NDFL for 2021: filling samples.”

When you can not submit 2-NDFL

There is no need to submit 2-NDFL certificates in 2021 if during 2016 the organization or individual entrepreneur did not pay income to individuals for which they are tax agents. So, for example, you don’t have to report on employees for whom the organization did not pay wages or make any other payments from January to December 2021. There is no need to submit 2-NDFL with zero indicators. There is simply no point in zero 2-NDFL certificates.

Deadline for submitting 2-NDFL and procedure for submitting the form. .

After a year, the tax agent must provide information about the income received and payments made on it, providing a 2-NDFL certificate within the following deadlines:

- If the certificate is filled out with the attribute “1”, in the case of calculating the total amount of income, indicating the tax base and calculated income tax for an individual, the deadline for submitting the certificate is no later than April 1.

- When filling out a certificate with attribute “2”, if it is not possible to withhold tax from an individual (for example, citizens who are not employees were given gifts worth more than 4 thousand rubles, in accordance with the Tax Code of the Russian Federation, Article 226, clause 5) – The deadline for submission is no later than March 1.

If the number of employees in the organization does not exceed 25 people, then the reporting can be submitted to the relevant Federal Tax Service on paper; if more, then it must be sent only in electronic form (Tax Code of the Russian Federation, Art. 230, clause 2, paragraph 2).

.

Deadline

Organizations and individual entrepreneurs are required to submit 2-NDFL certificates about income and withheld personal income tax to the Federal Tax Service no later than April 1 of the year following the reporting year (clause 2 of Article 230 of the Tax Code of the Russian Federation). However, April 1, 2021 is a Saturday. In this regard, the deadline for submission is moved to the next working day. Accordingly, most tax agents need to submit 2-NDFL certificates for 2016 with “sign 1” no later than April 3, 2021 (inclusive).

Also, information must be submitted to the Federal Tax Service on Form 2-NDFL in relation to individuals to whom the tax agent paid income in 2021, but personal income tax was not withheld from this income. For example, if in 2016 an organization gave a gift worth more than 4,000 rubles to a citizen who is not its employee. The deadline for submitting such certificates is no later than March 1 of the year following the reporting year (clause 5 of Article 226 of the Tax Code of the Russian Federation). Accordingly, if you paid income to individuals in 2021 from which personal income tax was not withheld, then no later than March 1, 2021 (this is Monday) you need to submit 2-NDFL certificates to the Federal Tax Service Inspectorate for these individuals with the “2” order. Moreover, within the same period, the “physicist” himself must be notified about the unwithheld tax. See “2-NDFL due date: important dates.”

Presentation method

It is possible to submit 2-NDFL certificates “on paper” only if in 2016 the number of individuals who received income from a tax agent is less than 25 people (Clause 2 of Article 230 of the Tax Code of the Russian Federation). If 25 or more people received income, then they must report electronically via telecommunications channels through an electronic document management operator.

Expert opinion

Natalia Morozova, methodologist at BDO Unicon Outsourcing, comments: “The Federal Tax Service of Russia has prepared a project informing about the beginning of the development of changes to the Federal Tax Service order dated September 10, 2015 No. ММВ-7-11/ [ email protected] “On approval of codes for types of income and deductions.” This project is published on the website www.regulation.gov.ru and is under discussion. The need for amendments is due to the fact that significant changes were made to Chapter 23 “Individual Income Tax” of the Tax Code of the Russian Federation from January 1, 2021. In particular: the procedure for determining the date of actual receipt of income has been clarified (clause 1 of Article 223 of the Tax Code of the Russian Federation), the procedure for calculating and transferring personal income tax has changed (Article 226 of the Tax Code of the Russian Federation), and the obligation to submit quarterly form 6-NDFL has been introduced (clause 2 of Art. 230 of the Tax Code of the Russian Federation). Why is this necessary? The fact is that the dates of actual receipt of income, the procedure for calculating and transferring personal income tax affect the filling out of the tax accounting register, on the basis of the data of which the calculation in form 6-NDFL and certificate 2-NDFL are generated. As for the income and deduction codes themselves entered into the reporting form, it is assumed that they will be used from January 1, 2021.”

New form: approved or not

The form of a certificate of income for an individual 2-NDFL and the procedure for filling it out were approved by order of the Federal Tax Service of Russia dated October 30, 2015 No. ММВ-7-11/485. At the same time, a new form of 2-NDFL certificate for reporting for 2016 was not developed or approved. The new form simply does not exist. In 2021, you need to fill out the form that was used before when reporting for 2015 was submitted. See “Certificate 2-NDFL in 2021: current form.”

The composition of the current form of certificate 2-NDFL is as follows:

| Help 2-NDFL in 2021: composition | |

| Section 1 | Tax agent information. |

| Section 2 | Data about an individual |

| Section 3 | Income taxed at the rate (the rate must be specified). |

| Section 4 | Standard, social, investment and property deductions. |

| Section 5 | Total income and tax amounts (total information). |

You can download the current 2-NDFL certificate form using this link.

How to fill out 2 personal income taxes in 2021

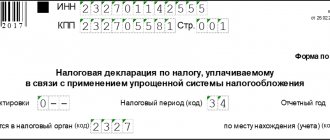

The procedure for filling out 2nd personal income tax is specified in the appendix to the order of the Federal Tax Service of Russia dated November 17, 2010 No. ММВ-7-3/ [email protected] Thus, the title page of 2nd personal income tax must indicate the year for which the certificate is being filled out, the serial number and the date of preparation of the certificate.

In the “Certificate Attribute” field you should put:

- number 1 – if information is submitted on the income of an individual and the amounts of accrued, withheld and transferred tax;

- number 2 – if information is provided about the impossibility of withholding personal income tax.

Also in the header part of the certificate you should indicate the four-digit code of the inspection to which form 2-NDFL is being submitted.

Section 1 provides information about the tax agent.

Section 2 of the personal income tax certificate 2 records information about the individual who is the recipient of the income.

In section 3 of certificate 2, personal income tax reflects the income of an individual by type and month of the tax period.

Section 4 of the personal income tax certificate 2 is filled out only on the page of the certificate on which income is indicated at a rate of 13%. It records information about standard tax deductions, property and social tax deductions.

Section 5 of the personal income tax certificate 2 “Total amounts of income and tax based on the results of the tax period” is intended to reflect the total amounts of income paid, calculated and withheld taxes for the tax period.

After Form 2 of personal income tax is completed, it must be submitted to the tax office in electronic form. In paper form - only possible if the number of citizens to whom the company paid income did not exceed 25 people.

Filling out the certificate: useful samples

Next, we will explain the procedure and features of filling out 2-NDFL certificates for 2016 using specific examples. We will also provide a final sample of the filling, which can be downloaded as a visual example.

Formatting the title

In the title of the certificate for 2021, in the “attribute” field, mark 1 if the certificate is provided as an annual report on income and withheld amounts of income tax (clause 2 of Article 230 of the Tax Code of the Russian Federation). If you are simply informing the Federal Tax Service that it was impossible to withhold tax in 2021, then indicate the number “2” (clause 5 of Article 226 of the Tax Code of the Russian Federation).

In the “Adjustment number” field, show one of the following codes:

- 00 – when preparing the initial certificate;

- 01, 02, 03, etc. – if you fill out a corrective certificate (that is, if in 2021 you “correct” previously submitted information”);

- 99 – when filling out a cancellation certificate (when you need to completely “cancel” the information already submitted before).

In the “In the Federal Tax Service (code)” field, mark the tax office code, indicate the year “2016” in the title, and also assign a serial number and date of generation to the certificate. As a result, the title of the 2-NDFL certificate for 2021 may take the following form:

Section 1: enter information about the tax agent

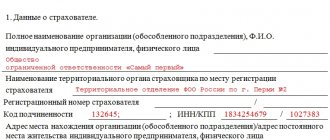

In section 1 of the form, provide basic information about the organization: name, tax identification number, checkpoint, contact telephone number. However, keep in mind that individual entrepreneurs indicate only the TIN, and they put a dash in the checkpoint field.

If the income of an individual was paid by the head office of the company in 2021, then in the 2-NDFL certificate you need to show the TIN, KPP and OKTMO at the location of the head office. If the income was received from a separate division, then mark the checkpoint and OKTMO at the location of the “separate division”.

In the “OKTMO Code” field, indicate the code of the territory in which the tax agent is registered. You can recognize this code by the Classifier approved by order of Rosstandart dated June 14, 2013 No. 159-st. However, if the 2-NDFL certificate is generated on behalf of an individual entrepreneur, then the approach when filling out should be as follows:

- indicate OKTMO at the place of residence of the entrepreneur according to the passport (except for individual entrepreneurs on UTII and on the patent taxation system);

- if the individual entrepreneur is on “imputed” or “patent”, then reflect OKTMO at the place of business in the appropriate tax regime.

Section 2: fill in information about the recipient

In section 2, enter the details of the individual to whom the income was paid. So, in particular, indicate your full name and tax identification number, date of birth. We will explain in more detail how to fill out section 2 of the 2-NDFL certificate for 2021 in the table:

| Filling out the fields in section 2 of the 2-NDFL certificate | |

| Field | What to indicate |

| "TIN in the Russian Federation" | Identifier specified in the TIN certificate of an individual. |

| "TIN in the country of residence" | TIN or its equivalent in the country of citizenship of the foreign employee. |

| "Taxpayer status" | One of the following codes: • 1 – for tax residents; • 2 – for non-residents (including for citizens of the EAEU: the Republic of Belarus, Kazakhstan, Armenia and Kyrgyzstan); • 3 – for non-residents – highly qualified specialists; • 4 – for employees who are participants in the state program for the voluntary resettlement of compatriots living abroad; • 5 – for foreign employees who have refugee status or have received temporary asylum in the Russian Federation; • 6 – for foreign employees working on the basis of a patent. |

| "Citizenship (country code)" | Code of the country of permanent residence of the person. The code, for example, of Russia is 643 (according to the Classifier, approved by Resolution of the State Standard of Russia dated December 14, 2001 No. 529-st). |

| “Identity document code” | Code from the reference book “Document Codes” (Appendix 1 to the order of the Federal Tax Service of Russia dated October 30, 2015 No. ММВ-7-11/485). |

| “Residence address in the Russian Federation” | Address of permanent residence of an individual according to a passport or other document confirming such address. |

| Subject code | Directory code “Codes of subjects of the Russian Federation and other territories (Appendix 2 to the order of the Federal Tax Service of Russia dated October 30, 2015 No. ММВ-7-11/485). |

Section 3: grouping income

In the table of section 3 of the 2-NDFL certificate for 2021, show the amount of income received for 2021, the codes of income and deductions and the tax rate. Please fill out this table monthly. At the beginning of the table, show the tax rate at which the income reflected in this section is taxed. If in 2021 an individual was paid income taxed with personal income tax at different rates, then fill out section 3 several times - at each rate.

Let us remind novice accountants that each type of income and each type of tax deductions are assigned individual codes, for example:

- for income in the form of wages - code 2000;

- when paying remuneration under other civil contracts (except copyright) – code 2010;

- when paying benefits for temporary disability - code 2300;

- if there is no separate code for income - code 4800. That is, for example, under code 4800 you can show above-limit daily allowances, compensation for unused vacation, severance pay in excess of three times the average earnings, etc. (letter of the Federal Tax Service of Russia dated September 19, 2021 No. BS- 4-11/17537).

If we talk about the most common case, then if an employee in the period from January to December 2021 received only wages under an employment contract, then section 3 of the 2-NDFL certificate for 2021 with sign “1” may look like this:

Also, in section 3 of the 2-NDFL certificate for 2021, you need to reflect the codes of deductions provided to individuals and the amount of such deductions. However, do not get confused: in section 3, reflect only professional tax deductions (Article 221 of the Tax Code of the Russian Federation), deductions in the amounts provided for in Article 217 of the Tax Code of the Russian Federation and amounts that reduce the tax base on the basis of Articles 214.1, 214.3, 214.4 of the Tax Code of the Russian Federation. The corresponding deduction code must be indicated opposite the income for which this deduction is applied.

New income codes from 2021

In 2-NDFL certificates, separately show the bonuses that employees received in 2016 for production results as part of their remuneration. For such bonuses, code 2002 has been in effect since 2021. If bonuses were issued at the expense of net profit, then show them with code 2003. Note that until 2021, bonuses were not allocated with a separate code: for bonuses for labor, the same code was indicated as for salary in cash – 2000.

Standard, social, investment and property tax deductions should not be reflected in section 3 of 2-NDFL certificates. The following section of the 2-NDFL certificate is provided for them.

Section 4: highlighting deductions

In section 4 of the 2-NDFL certificate, show the standard tax deductions provided in 2021 (Article 218 of the Tax Code of the Russian Federation), social (Article 219 of the Tax Code of the Russian Federation), investment, as well as property deductions for the purchase (construction) of housing (subclause 2 p. 1 Article 220 of the Tax Code of the Russian Federation). The code that must be entered in the “Deduction Code” column can be determined from Appendix 2 to the order of the Federal Tax Service of Russia dated September 10, 2015 No. ММВ-7-11/387. In the “Deduction Amount” column, enter the deduction amount corresponding to the specified code.

Some social and property deductions are provided by employers to their employees. In this regard, in the lines “Notification confirming the right to a social tax deduction” and “Notification confirming the right to a property tax deduction,” the accountant needs to note the number and date of the corresponding notification and the code of the Federal Tax Service that issued the notification.

Changes to deduction codes from 2021

From January 1, 2021, the Federal Tax Service has updated the codes for standard tax deductions. Of the codes that were in force in 2021, only two remained the same: 104 and 105. In addition, the previously valid deduction codes for children 114–125 do not apply from January 1, 2021. They were excluded from the directory. Instead, use the new “children’s” codes from 126 to 149. For more information, see “New income and deduction codes for 2-NDFL certificates from December 26, 2021.”

You can also find a complete list of income and deduction codes that may be required to generate a 2-NDFL certificate for 2021 in the material: “Personal income tax codes and amounts of deductions in 2021: table with explanation.”

Let's assume that the employee was provided with the standard tax deduction for the first child in 2021. This deduction in 2017 corresponds to deduction code 126. The deduction amount was 16,800 rubles. In this case, an example of filling out section 4 of the 2-NDFL certificate for 2021 will look like this:

Show all indicators in the certificate for 2021 (except for the personal income tax amount) in rubles and kopecks. However, reflect the amount of tax (personal income tax) in full rubles (do not take into account amounts up to 50 kopecks, amounts of 50 kopecks or more - round up to the nearest whole ruble). For example, if the tax is 15.78 rubles, then show 16 whole rubles on the certificate.

Section 5: summing up

In section 5 of the certificate, summarize the total amount of income of an individual and personal income tax at the end of 2021 for each tax rate. If, during the tax period, the tax agent paid an individual income taxed at different rates (for example, 9%, 13%, 15%, 30%, 35%), then for each of them it is necessary to create sections 3 - 5 of certificate 2 -NDFL. Below in the table we will explain the general procedure for filling out the 2-NDFL certificate for 2021.

| General procedure for filling out the 2-NDFL certificate for 2016 | ||

| Help field | Filling | |

| 2-NDFL with sign 1 | 2-NDFL with sign 2 | |

| "Total Income" | Total income at the end of 2021 (excluding deductions). | The total amount of income in 2021 from which personal income tax was not withheld. |

| "The tax base" | The tax base from which personal income tax is calculated in 2021. | Tax base for calculating personal income tax |

| "Tax amount calculated" | The amount of calculated personal income tax (the tax base is multiplied by the tax rate). | The amount of personal income tax that has been calculated but not withheld. |

| “Amount of fixed advance payments” | The amount of fixed advance payments by which the personal income tax should be reduced (data taken from the notification of the Federal Tax Service). | 0 |

| "Tax amount withheld" | The amount of personal income tax withheld from the income of an individual. | 0 |

| “Tax amount transferred” | The amount of personal income tax transferred for 2021. | 0 |

| “Amount of tax over-withheld by the tax agent” | The excess amount of personal income tax not returned by the tax agent, as well as the amount of overpayment of personal income tax due to a change in tax status. | 0 |

| “The amount of tax not withheld by the tax agent” | The calculated amount of personal income tax not withheld in 2016. | |

Here is an example of filling out section 5 of the 2-NDFL certificate for 2021. Let's assume that the income of an individual for 2021 was 549,200 rubles. After applying tax deductions, the tax base amounted to 457,500 rubles. The tax rate is 13 percent. This means the personal income tax amount is 59,475 rubles (457,500 x 13%). This amount was calculated and withheld by the employer at the end of 2021. And I filled out section 5 of the help like this:

As a result, after filling out all the above sections, a sample 2-NDFL certificate for 2021 with sign “1” may look like this:

What does the modified form 2-NDFL look like from 2016

Heading – added adjustment field:

- 00 – in case of filling out the certificate initially.

- 01, 02… – correction number.

- 99 – code is indicated if it is necessary to provide a cancellation certificate.

Section 2, it became possible to indicate the TIN of foreign employees, so additional codes were introduced to the previously existing ones:

- 4 – If the employee is a participant in the state. voluntary resettlement programs for compatriots living abroad.

- 5 – If a foreign employee has received temporary asylum in the Russian Federation or is a refugee.

- 6 – for foreign employees working on the basis of a patent.

An addition has been made for foreign workers - now the address of the place of registration or his place of residence is indicated in the Address field of his place of residence in the Russian Federation.

Section 4 on deductions has been amended as follows:

- We have provided a field for indicating the notification details for receiving social deductions.

- The section now also reflects investment deductions, and not just social and property deductions.

Section 5 can now reflect information about fixed advance payments, and there is also a field for indicating the details of the notification, which confirms the right to reduce the tax by the amount of fixed payments.

In the document codes directory, instead of code 18, code 19 will be indicated for the certificate of temporary asylum.

The region codes now include Sevastopol (92) and Crimea (91).

When calculating and paying income to an individual, which is taxed at different rates, sections 3-5 must be completed for each of them. Those. all types of income must be in one certificate and sections 3-5 are filled out at different rates.

From January 1, 2021, in accordance with the Tax Code of the Russian Federation, Art. 226 clause 6 Personal income tax, which was withheld from vacation and sick pay, is transferred to the budget no later than the day of the month of their payment.

Note: It is allowed to indicate the full name of foreign citizens in Latin letters.

Please note that starting from 2021, new 6-NDFL reporting will be introduced, which is submitted quarterly, unlike 2-NDFL. You can familiarize yourself with the procedure for filling it out by following the link, as well as download the required form.

Responsibility of tax agents

If you do not submit a certificate in form 2-NDFL for 2021 to the Federal Tax Service on time, the tax authorities will have the right to impose a fine on the organization or individual entrepreneur under Article 126 of the Tax Code of the Russian Federation: 200 rubles.

Also, for failure to submit or for late submission of the annual 2-NDFL certificate, at the request of the Federal Tax Service, the court may impose administrative liability in the form of a fine in the amount against the manager or chief accountant: from 300 to 500 rubles. (Article 15.6 of the Code of Administrative Offenses of the Russian Federation).

In addition, if inspectors from the Federal Tax Service identify errors in 2-NDFL, they may regard them as “unreliable information.” And then the tax agent can be additionally fined 500 rubles for each “unreliable” document. If there are a lot of erroneous certificates, then the fine may increase.

Read also

19.01.2017

New form 6-NDFL. Calculation according to form 6-NDFL

This year, employers will have to submit not only 2-NDFL certificates every quarter, but also a personal income tax calculation, which will show the amount of income paid, deductions provided, and calculated and withheld personal income tax.

. Calculation of the amounts of personal income tax calculated and withheld by the tax agent (Form 6-NDFL). Order of the Federal Tax Service of Russia dated October 14, 2015 No. ММВ-7-11/ [email protected]

Form 6-NDFL appeared on October 14. 2015 by order of the Federal Tax Service of Russia. This certificate must be submitted quarterly, no later than the last day of the month following the expired quarter, that is, May 3, August 1, October 31, 2021, and the annual certificate must be submitted no later than April 1, 2017.

Failure to submit the form will result in a fine of 1,000 rubles for each full or partial month overdue. If the certificate is delayed for more than 10 days, the inspectorate has the right to freeze transactions on the current account.

Like 2-NDFL, you can submit form 6-NDFL in paper and electronic form. It should be remembered that from 2021, paper certificates are possible if employers paid income for the year to less than 25 individuals. Last year the limit was 10 people.