Quit Statement

To leave the LLC, the founder (participant) must submit a written application to the organization (clause 1 of Article 94 of the Civil Code of the Russian Federation, Resolution of the Presidium of the Supreme Arbitration Court of the Russian Federation dated January 18, 2005 No. 11809/04).

From the date of submission of this document, the participant’s share will pass to the organization (clause 2 of article 94 of the Civil Code of the Russian Federation, clauses 6.1, 7 of article 23 of the Law of February 8, 1998 No. 14-FZ).

The day of filing an application is one of the following dates:

- the day of its transmission to the board of directors (supervisory board), the head of the company or an employee of the organization, whose duties include transmitting the application to a competent person;

- the day on which the company received the application sent by mail.

This is stated in subparagraph “b” of paragraph 16 of the resolution of the Plenums of the Supreme Court of the Russian Federation and the Supreme Arbitration Court of the Russian Federation dated December 9, 1999 No. 90/14.

An example of an application for withdrawal of a participant from an LLC

The authorized capital of Torgovaya LLC is 100,000 rubles. It is divided into shares between three participants. One participant – A.S. Glebova - decided to leave the founders, as he wrote in a statement.

On July 16, Glebova sent a statement to Hermes by mail with acknowledgment of receipt. The society received the statement on July 23. The date of receipt of the application by Hermes is confirmed by the imprint of a calendar stamp on the notification.

How to calculate the actual value of a share when a participant leaves the Company?

The company is obliged to pay the participant who submitted an application to leave the company the actual value of his share in the authorized capital within three months from the date the corresponding obligation arises (unless a different period or procedure for such payment is provided for by the company’s charter).

With the consent of this participant, the company has the right to give him in kind property of the same value, in case of incomplete payment of his share in the authorized capital of the company - the actual value of the paid part of the share (Clause 6.1, Article 23 of the Federal Law of 02/08/1998 No. 14-FZ “On Limited Liability Companies”, hereinafter referred to as Law No. 14-FZ).

Starting from January 1, 2021, a participant’s application to leave the company requires notarization (Article 3 of the Federal Law of March 30, 2015 No. 67-FZ).

APPLICATION FOR WITHDRAWAL OF A PARTICIPANT: SAMPLE

EXIT OF A PARTICIPANT FROM THE SOCIETY: TAX ASPECTS

Change of charter

If the founder (participant) left the LLC before the company’s charter was brought into compliance with the new edition of Law No. 14-FZ of February 8, 1998, then it is necessary to proceed as follows. Simultaneously with registering the transfer of shares, changes to the charter must be registered. This was stated in the letter of the Federal Tax Service of Russia dated June 25, 2009 No. MN-22-6/511.

Within a year from the date of filing the application for withdrawal, the organization must find new owners of the share of the founder (participant) who left the company. It can be distributed among other founders (participants), sold to one of them, sold to third parties, etc. This is stated in Article 24 of the Law of February 8, 1998 No. 14-FZ.

The new composition of the organization's participants must be reflected in the list of company participants. In addition to information about each participant, this document must contain information about the size of his share, its payment, the size of shares belonging to the company itself, the dates of their transfer to the company, etc. (Clause 1 of Article 31.1 of the Law of February 8, 1998 No. 14-FZ).

Exit order

The charter of a corporation may contain certain specifics. For example, the charter may allow exit:

- only to some participants,

- under certain circumstances,

- solely on the basis of the permission of all other participants.

After studying the charter, if you have the opportunity to leave the company, contact a notary. He will certify your application, send it to the appropriate authorized body, and a copy to your company.

Attention! After making changes to the Unified State Register of Legal Entities, your share passes to the Company, and you lose all the rights and obligations of a participant; you remain: the right to receive the documentation necessary to calculate the share, and the obligation to make an additional contribution if a decision on this was made before your withdrawal.

Payment of the share to the withdrawing participant

The organization is obliged to pay the founder (participant) the actual value of his share (clause 6.1 of Article 23 of the Law of February 8, 1998 No. 14-FZ).

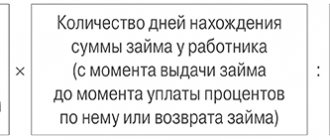

Calculate the actual value of the share of the founder (participant) retiring from the LLC using the formula:

| Actual value of the founder's (participant's) share | = | Nominal value of share | : | Authorized capital | × | Net assets |

This calculation procedure is established by paragraph 2 of Article 14 of the Law of February 8, 1998 No. 14-FZ.

The procedure for assessing net assets was approved by order of the Ministry of Finance of Russia dated August 28, 2014 No. 84n.

Situation: what data must be used to calculate the actual value of the founder’s (participant’s) share?

Estimate the actual value of the redeemed share of the founder (participant) based on the market value of the property reflected in the balance sheet.

The actual value of the founder's (participant's) share corresponds to part of the value of the company's net assets, proportional to its nominal share. As a general rule, when buying out a share (when a participant leaves the company), this indicator is determined on the basis of the Balance Sheet data for the last reporting period before the founder (participant) approached the company with such a requirement (application). In this case, the indicators for calculating the actual value of the share must be taken from the reporting that is closest to the date of filing the participant’s request (application) to leave the company. This can be not only annual, but also interim (monthly or quarterly) reporting. This procedure follows from the provisions of paragraph 2 of Article 14, paragraphs 2 and 6.1 of Article 23 of the Law of February 8, 1998 No. 14-FZ and is confirmed by judicial practice (see, for example, the decisions of the Seventh Arbitration Court of Appeal of April 6, 2015 No. 07AP -871/2015, Arbitration Court of the West Siberian District dated August 6, 2015 No. F04-21575/2015).

Thus, from the literal interpretation of these norms it follows that the only document on the basis of which an organization must calculate the actual value of the founder’s (participant’s) share is the balance sheet. Consequently, other methods for determining the value of a company’s assets, including based on the market value of property, cannot be used.

However, it should be taken into account that the financial statements must reliably reflect the financial position of the organization (clause 6 of PBU 4/99). Subject to this rule, the book value of the property corresponds to its market value.

The withdrawing participant has the right to challenge in court the amount of the actual value of the share calculated by the company (subclause “c” of paragraph 16 of the resolution of the plenums of the Supreme Court of the Russian Federation and the Supreme Arbitration Court of the Russian Federation dated December 9, 1999 No. 90/14).

If a dispute arises between a participant and the company, the courts determine the actual value of the share taking into account the market value of the company's property. In this case, the balance sheet data is used to establish the composition of the company’s property (resolutions of the Presidium of the Supreme Arbitration Court of the Russian Federation dated June 7, 2005 No. 15787/04, dated September 6, 2005 No. 5261/05).

The rulings of arbitration courts adopted after this were overwhelmingly based on this position (see, for example, the rulings of the Supreme Arbitration Court of the Russian Federation dated March 5, 2010 No. VAS-1880/10, dated November 22, 2007 No. 14448/07, decisions of the FAS Western Siberian District dated June 24, 2010 No. A75-5643/2009, Ural District dated May 12, 2010 No. Ф09-3177/10-С4, dated March 18, 2010 No. Ф09-1603/10-С4, Far Eastern District dated March 23, 2010 No. 1365/2010, Volga District dated February 12, 2010 No. A72-4275/2008, dated February 12, 2010 No. A72-4272/2008, Central District dated February 5, 2010 No. F10-6286 /09, dated March 30, 2009 No. F10-714/09(2), North-Western District dated December 23, 2009 No. A26-3413/2008, North Caucasus District dated December 11, 2009 No. A32-16337 /2007, Volga-Vyatka District dated May 28, 2008 No. A28-278/2008-9/9).

In this situation, the organization will have to independently resolve the issue of assessing the actual value of the founder’s (participant’s) share being purchased from him. However, taking into account the established arbitration practice, the company will not violate the requirements of the law, but will avoid litigation if it evaluates the actual value of the redeemed share of the founder (participant) based on the market value of the property reflected in the balance sheet.

An example of calculating the actual value of a share when a founder leaves an LLC. The book value of the organization's net assets corresponds to their market value

The authorized capital of Torgovaya LLC is 100,000 rubles. It is divided into shares between three participants:

- A.V.'s share Lvov – 25,000 rubles;

- share of E.E. Gromovoy – 25,000 rubles;

- share of V.K. Volkova – 50,000 rubles.

Gromova decided to leave the founders. Hermes received a statement about Gromova’s release on July 16. To pay the share, the Hermes accountant calculated its actual value according to the balance sheet. According to the balance sheet for the first half of the year, the value of the organization’s net assets is 1,080,000 rubles.

The actual value of Gromova’s share, which is payable, is equal to: 25,000 rubles. : 100,000 rub. × 1,080,000 rub. = 270,000 rub.

An example of calculating the actual value of a share when a founder leaves an LLC. The book value of the organization's net assets does not correspond to their market value

The authorized capital of Torgovaya LLC is 100,000 rubles. It is divided into shares between three participants:

- A.V.'s share Lvov – 25,000 rubles;

- share of E.E. Gromovoy – 25,000 rubles;

- share of V.K. Volkova – 50,000 rubles.

Gromova decided to leave the founders. In this regard, the organization conducted an expert assessment of the market value of real estate listed on its balance sheet.

Hermes received a statement about Gromova’s release on July 16. To pay the share, the Hermes accountant calculated its actual value based on the balance sheet and expert assessment. According to the balance sheet for the first half of the year, taking into account the market value of property, the value of the organization’s net assets is 5,100,000 rubles.

The actual value of Gromova’s share, which is payable, is equal to: 25,000 rubles. : 100,000 rub. × 5,100,000 rub. = 1,275,000 rub.

General provisions

First, let's look at what the actual size of the share is when the founder leaves. Essentially, this is part of the price of the organization's net assets, which is proportional to the size of the share. The final result is presented as a percentage or in fractional expression. Often, the actual value is presented as the difference between the price of the structure's net assets, as well as the amount of the authorized capital. If the resulting difference is small, the company is forced to reduce the amount of capital by the required amount.

The transfer of a share into the ownership of a company is possible in the following situations:

- The company received a request from the founder to purchase a share.

- The period in which the share in the LLC management company must be paid or the period for issuing compensation has ended.

- The company received a statement from the founder about leaving the company. This is possible if such action is permitted by the company's articles of association.

- The decision of the court to exclude the founder of the LLC from the company has come into force or the decision to transfer the share of the organization has begun to take effect.

- One of the founders refused to give consent to the transfer of the share or part thereof to the legal successors or heirs of the LLC participants.

- The company makes payment of the actual price (in respect of all or only part of the share) owned by the founder, at the request of creditors.

Accounting: payment of shares

You can settle accounts with the founder (participant) either with money or with property (with his consent). This must be done within three months from the date the participant submits an application to leave the company, unless a different period is provided for in the charter (clause 6.1 of Article 23 of the Law of February 8, 1998 No. 14-FZ).

Reflect the payment of the actual value of the share by posting:

Debit 75 subaccount “Participant” Credit 51 (50) – the actual value of the participant’s share was paid minus the withheld personal income tax.

This follows from the Instructions for the chart of accounts.

An example of payment of the actual value of a share when the founder leaves the LLC. The book value of the organization's net assets corresponds to their market value

The authorized capital of Torgovaya LLC is 100,000 rubles. It is divided into shares between three participants:

- A.V.'s share Lvov – 25,000 rubles;

- share of E.E. Gromovoy – 25,000 rubles;

- share of V.K. Volkova – 50,000 rubles.

Gromova decided to leave the founders. Hermes received a statement about Gromova’s release on July 16. To pay the share, the Hermes accountant calculated its actual value. According to the balance sheet for the first half of the year, the value of the organization’s net assets is 1,080,000 rubles. The actual value of Gromova’s share is 270,000 rubles. (RUB 25,000 : RUB 100,000 × RUB 1,080,000).

On July 16, the accountant reflected the transfer of Gromova’s share to the company:

Debit 81 Credit 75 subaccount “Gromov’s Participant” – 270,000 rubles. – reflects the transfer of Gromova’s share to the organization.

On August 20, the Hermes cashier paid Gromova the amount due to her. Gromova is a resident of Russia. On this day, the accountant made the following entries:

Debit 75 sub-account “Gromov Participant” Credit 68 sub-account “Personal Income Tax Payments” – 35,100 rubles. (RUB 270,000 × 13%) – personal income tax is withheld from the actual value of Gromova’s share;

Debit 75 subaccount “Gromov's Participant” Credit 50 – 234,900 rub. (270,000 rubles – 35,100 rubles) – the actual value of his share in the authorized capital was paid to the participant.

Situation: is it necessary to pay the actual value of the share to the founder (participant) leaving the LLC if the net assets of the organization are negative?

No no need.

If a founder (participant) leaves the company, the organization is obliged to pay him the actual value of his share. The acquisition of a share is paid for by the company from the difference between the value of net assets and the size of the authorized capital.

This follows from paragraphs 6.1 and 8 of Article 23 of the Law of February 8, 1998 No. 14-FZ.

The actual value of the share of the founder (participant) of the company corresponds to part of the value of the company’s net assets in proportion to the size of its share (paragraph 2, paragraph 2, article 14 of the Law of February 8, 1998 No. 14-FZ).

Consequently, if the value of the company’s net assets is negative, then there are no grounds for paying the actual value of the shares.

A similar conclusion was made in the resolution of the Presidium of the Supreme Arbitration Court of the Russian Federation dated November 14, 2006 No. 10022/06, the determination of the Supreme Arbitration Court of the Russian Federation dated December 18, 2012 No. VAS-16959/12, resolutions of the Federal Antimonopoly Service of the Ural District dated January 24, 2013 No. F09-13828/ 12, Moscow District dated October 29, 2012 No. A41-30190/10, Central District dated February 9, 2012 No. A14-3376/2011.

It should be noted that a company whose net assets will be less than its authorized capital at the end of two financial years in a row (starting from the second financial year) is obliged to make a decision to reduce the authorized capital to an amount not exceeding the value of the organization’s net assets (clause 4 Article 90 of the Civil Code of the Russian Federation, paragraph 4 of Article 30 of the Law of February 8, 1998 No. 14-FZ). In this case, the authorized capital can be reduced by reducing the nominal value of the shares of all participants or by extinguishing the shares owned by the company (Clause 1, Article 20 of the Law of February 8, 1998 No. 14-FZ).

An example of how to reflect in accounting the transfer of a participant's share upon leaving an LLC. The actual share is not paid because the net assets are negative

The authorized capital of Torgovaya LLC is 100,000 rubles. It is divided into shares between three participants:

- A.V.'s share Lvov – 25,000 rubles;

- share of E.E. Gromovoy – 25,000 rubles;

- share of A.S. Glebova – 50,000 rubles.

Glebova decided to withdraw from the participants. The application for Glebova’s release was received by Hermes on July 16. As a general rule, when Glebova leaves the membership, Hermes must pay her the actual value of the share within a month. However, according to the balance sheet for the first half of the year, taking into account the market value of the property, the value of net assets turned out to be negative (-250,000 rubles).

Based on this, calculation and payment of the actual value of the share upon Glebova’s withdrawal from the LLC’s membership are not made. Within the period established by law (i.e., until November 17), Glebova did not declare her reinstatement as a member of the LLC.

In this case, the nominal value of Glebova’s share is distributed among the remaining participants in proportion to their shares in the authorized capital (by decision of the general meeting of participants).

Since Lvov's and Gromova's shares are the same, Glebova's share is distributed equally between them.

On July 16, the accountant reflected the transfer of the nominal share to the LLC with the following entries:

Debit 81 Credit 75 subaccount “Glebov’s Participant” – 50,000 rubles. – reflects the transfer of Glebova’s share to the organization at nominal value.

On November 17, the deadline for Glebova to apply for reinstatement as a participant expired:

Debit 75 subaccount “Glebov’s Participant” Credit 91 – 50,000 rub. – the nominal value of Glebova’s share is included in other income.

The accountant reflected the distribution of shares in the authorized capital of the company among the remaining participants with the following entries:

Debit 75 subaccount “Participant Lviv” Credit 81 – 25,000 rubles. (RUB 50,000: 2) – according to the decision to redistribute the share of the withdrawing participant, the transfer of the nominal share to Lvov is reflected;

Debit 75 subaccount “Gromov's Participant” Credit 81 – 25,000 rubles. (RUB 50,000: 2) – according to the decision to redistribute the share of a retired participant, the transfer of the nominal share to Gromova is reflected;

Debit 80 subaccount “Participant Glebova” Credit 80 subaccount “Participant Lvov” – 25,000 rubles. (RUB 50,000: 2) – reflects the change in the composition of participants;

Debit 80 sub-account “Glebov’s Participant” Credit 80 sub-account “Gromov’s Participant” – 25,000 rubles. (RUB 50,000: 2) – reflects the change in the composition of participants.

Since the remaining participants do not pay for the shares distributed in their favor, the amount reflected in the debit of account 75 is written off from the appropriate sources:

Debit 84 Credit 75 subaccount “Participant Lviv” – 25,000 rubles. (50,000 rubles: 2) – the nominal value of the share in the part transferred to Lvov through redistribution was written off;

Debit 84 Credit 75 subaccount “Gromov’s Participant” – 25,000 rubles. (50,000 rubles: 2) – the nominal value of the share in the part transferred to Gromovaya through redistribution was written off.

When the share of a retired participant is distributed among the remaining participants, they will have income subject to personal income tax. Since no payments are made to participants, the organization reported to the inspectorate that it was impossible to withhold tax.

EXAMPLE FROM JUDICIAL PRACTICE

In the resolution of the Presidium of the Supreme Arbitration Court of the Russian Federation dated November 14, 2006 No. 10022/06, the court indicated that the value of the company’s net assets was minus 1,943,000 rubles. and there were no grounds for paying the plaintiff the actual value of the share. The actual value of a share or part of a share in the authorized capital of a company is paid out of the difference between the value of the company's net assets and the size of its authorized capital. If such a difference is not enough, the company is obliged to reduce its authorized capital by the missing amount. If a decrease in the authorized capital of a company may lead to its size becoming less than the minimum amount of the authorized capital of the company determined in accordance with Law No. 14-FZ on the date of state registration of the company, the actual value of the share or part of the share in the authorized capital of the company is paid out of the difference between the value of the company's net assets and the specified minimum amount of the company's authorized capital.

POSITION OF THE COURT

The presence of a negative value of the company's net assets excludes the payment of the actual value of the share to a company participant upon his/her withdrawal from the company.

— Resolution of the Seventeenth Arbitration Court of Appeal dated 02/07/2013 No. 17AP-14149/2012-GK.

Payment of actual value of property

The cost of the share can be paid with property in the following cases:

- at the request of the participant;

- in case of lack of funds to pay the share.

It is controversial whether such a transaction is recognized as a major transaction and whether approval is required when paying a share to a participant in property. And the courts are ambiguous on this issue.

Accounting: transfer of the participant's share to the organization

Upon receipt of an application for the withdrawal of a founder (participant) from the company, make the following entry in accounting:

Debit 81 Credit 75 subaccount “Participant” - reflects the transfer of the participant’s share to the organization.

This conclusion follows from the Instructions for the chart of accounts.

An example of reflecting in accounting the distribution of the share of a retired participant among the remaining participants

The authorized capital of Torgovaya LLC is 100,000 rubles. It is divided into shares between three participants:

- A.V.'s share Lvov – 25,000 rubles;

- share of E.E. Gromovoy – 25,000 rubles;

- share of V.K. Volkova – 50,000 rubles.

Volkov decided to withdraw from the membership. On July 16, his resignation letter was received by the organization. The actual value of Volkov's share is 220,000 rubles.

The following entry was made in the organization's accounting:

Debit 81 Credit 75 subaccount “Participant of Wolves” – 220,000 rubles. – reflects the transfer of Volkov’s share to the organization.

By decision of the general meeting of participants, the share of the withdrawing participant is distributed among the remaining participants in proportion to their shares in the authorized capital. Since the shares of Lvov and Gromova are the same, the share of the eliminated participant is distributed equally between them.

In accounting, the accountant reflected the redistribution of shares in the authorized capital with the following entries:

Debit 75 subaccount “Participant Gromov” Credit 81 – 110,000 rubles. (RUB 220,000: 2) – reflects the transfer of the share to Gromova based on the decision to redistribute the share of the withdrawing participant;

Debit 75 “Participant Lviv” Credit 81 – 110,000 rub. (RUB 220,000: 2) – reflects the transfer of the share to Lvov by decision on the redistribution of the share of the withdrawing participant;

Debit 80 subaccount “Participant Volkov” Credit 80 subaccount “Participant Gromov” – 25,000 rubles. (RUB 50,000: 2) – reflects the change in the composition of participants;

Debit 80 subaccount “Participant Volkov” Credit 80 subaccount “Participant Lviv” – 25,000 rubles. (RUB 50,000: 2) – reflects the change in the composition of participants.

Since the remaining participants do not pay for the shares distributed in their favor, the amount reflected in the debit of account 75 is written off from the appropriate sources:

Debit 84 Credit 75 subaccount “Gromov’s Participant” – 110,000 rubles. – the actual value of the share in the part transferred to Gromova through redistribution was written off;

Debit 84 Credit 75 subaccount “Participant Lviv” – 110,000 rubles. – the actual value of the share in the part transferred to Lvov through redistribution was written off.

When the share of a retired participant is distributed among the remaining participants, they will have income subject to personal income tax. Since no payments are made to participants, the organization reported to the inspectorate that it was impossible to withhold tax.

An example of reflecting in accounting the sale by a company of a share of a retired participant to a third party

The authorized capital of Torgovaya LLC is 100,000 rubles. It is divided into shares between three participants:

- A.V.'s share Lvov – 25,000 rubles;

- share of E.E. Gromovoy – 25,000 rubles;

- share of V.K. Volkova – 50,000 rubles.

Volkov decided to withdraw from the membership. On July 16, his resignation letter was received by the organization. The actual value of Volkov's share is 220,000 rubles.

The following entry was made in the organization's accounting:

Debit 81 Credit 75 subaccount “Participant of Wolves” – 220,000 rubles. – reflects the transfer of Volkov’s share to the organization.

By decision of the general meeting of participants, the share of the withdrawing participant will be sold to a third party at its actual value (RUB 220,000)

In accounting, the accountant reflected the sale of a share in the authorized capital with the following entries:

Debit 75 subaccount “New participant” Credit 91-1 – 220,000 rubles. – the share of the withdrawing participant is sold to the new participant;

Debit 91-2 Credit 81 – 220,000 rub. – the actual (actual) cost of the share being sold is written off;

Debit 50 (51) Credit 75 – 220,000 rub. – the share was paid by the new participant;

Debit 80 sub-account “Wolf Participant” Credit 80 sub-account “New Participant” – 50,000 rubles. – reflects the change in the composition of participants.

Situation: what value of the founder’s (participant’s) share in the authorized capital of the LLC - nominal or real - is written off in accounting when he submits an application to leave the company?

When a founder (participant) leaves the company, write off the actual value of his share in accounting.

In the debit of account 81 “Own shares (shares)”, reflect the amount of actual expenses - the amount that needs to be paid to the founder (participant) (Instructions for the chart of accounts). The LLC must pay the founder (participant) the actual value of the share (clause 6.1 of Article 23 of the Law of February 8, 1998 No. 14-FZ). Therefore, debit account 81 “Own shares (shares)” with the actual value of the share.

An example of how settlements with a participant when he leaves an LLC are reflected in accounting

The authorized capital of Torgovaya LLC is 100,000 rubles. It is divided into shares between three participants:

- A.V.'s share Lvov – 25,000 rubles;

- share of E.E. Gromovoy – 25,000 rubles;

- share of V.K. Volkova – 50,000 rubles.

Volkov decided to withdraw from the membership. On July 16, his resignation letter was received by the society. The actual value of Volkov's share is 220,000 rubles.

The following entry was made in the organization's accounting:

Debit 81 Credit 75 subaccount “Participant of Wolves” – 220,000 rubles. – reflects the transfer of Volkov’s share to the organization.

How is exit from an LLC carried out?

Any of the participants has the right to decide whether to leave the society or not. To implement this task, the participant must take into account a number of points (Federal Law No. 14):

- Such a possibility should be reflected in the charter of the LLC.

- In case of leaving the organization, at least one more member must remain in it.

To leave the society, you need to fill out an application (drawn up in free form). It acts as confirmation that the founder plans to leave the LLC. The process is considered completed when the head of the company, the board of directors, and an authorized employee have received this paper.

In addition, the founder can be removed from the membership in the following cases:

- The exit applicant voted against some big deal and is now forced to leave at the request of the other founders.

- The founder died, but relatives demand the due share.

- The person was expelled at the meeting by vote.

There may be other reasons that are prescribed at the legislative level. It is interesting that payments to the founder of the LLC in the event of his exit are made regardless of the reasons. This obligation arises for the company at the moment of transfer of the share.

Please note that a company cannot pay a share if at that moment it shows signs of bankruptcy.

Claiming a share in court

If you are not paid on time, file a claim with the arbitration court at the location of the company. For corporate disputes, a mandatory claim procedure is not established by law.

The defendant in the claim will be the company.

Statement of claim for reclaiming a share

In your claim please indicate:

- details of the plaintiff and defendant,

- information about leaving society,

- the amount of the share that you must pay,

- interest under art. 95 GK for the entire period of delay.

Attach to the claim:

- extract from the Unified State Register of Legal Entities,

- documents confirming your participation in the society before leaving,

- the company’s financial statements, an extract from the Unified State Register of Real Estate, an appraiser’s report and other documents confirming the actual value of the share,

- calculation of the cost of the share,

- documents confirming payment of state duty,

Attention! The state duty is calculated based on the amount of the claim; you can use the online calculator on the official website of the arbitration court. You can also download a sample payment document there.

- a receipt for sending the claim to the defendant.

The provisions of the law on the procedure for paying shares are mandatory and cannot be changed by agreement, including a settlement agreement.

Resolution of the Court of Justice of the West Siberian District dated May 31, 2017 in case A75-15560/2016. The ruling on approval of the settlement agreement concluded between the participant and the LLC was canceled in a higher court, since the court did not check its compliance with the law, did not involve other former participants in the case who had not yet received payments, and therefore was not convinced of that the rights of third parties are not violated.

Calculation of net asset value

The mechanism for calculating the value of net assets was established by the Ministry of Finance only for joint-stock companies. However, the financial statements of an LLC are prepared according to the same principles, so this calculation procedure can also be used by limited liability companies. The Ministry of Finance agrees with this position, as evidenced by its letter dated December 7, 2009 No. 03-03-06/1/791.

The formula for calculating net assets is as follows:

NA = final indicator of section III of the balance sheet + deferred income - debt of participants to pay contributions to the management company.

NOTE: the company should not pay a share to a participant if the value of his net assets is negative.

Thus, the only document that is used in calculating the actual value of a share is the financial statements. The cost indicators on the basis of which the value of the share is calculated are taken from the corresponding lines of the balance sheet.

However, there is another position, which is based on the need to take into account the market value of the company’s assets when determining the actual value of the exiting participant’s share. This position often becomes the cause of corporate disputes affecting the procedure for calculating the value of a share.

Note! According to clause 16 of the joint resolution of the Plenums of the Supreme Court of the Russian Federation and the Supreme Arbitration Court of the Russian Federation dated December 9, 1999 No. 90/14 (hereinafter referred to as Resolution No. 90/14), a company participant who does not agree with the size of the share determined by the company, if there is evidence, can apply to the arbitration court with a requirement to verify the validity of the calculations made by the company. The basis of the evidence base in this case will be an independent examination.

Withholding personal income tax from the actual value of the individual participant's share

Withholding personal income tax

The procedure for determining the tax base for calculating personal income tax is not specifically prescribed in the legislation. Accounting expert8 is guided by a more cautious position and believes that:

- income in the form of an excess of the paid actual value of the share over the cost of its acquisition is equated to dividends and is subject to personal income tax (clause 1, clause 1, article 208 of the Tax Code of the Russian Federation).

- income within the nominal value is also subject to personal income tax in the general manner (Article 209 of the Tax Code of the Russian Federation, clause 1 of Article 210 of the Tax Code of the Russian Federation).

Personal income tax is calculated on the date of receipt of income, i.e. on the date of their payment (clause 4 of article 226 of the Tax Code of the Russian Federation).

The deadline for transferring personal income tax is the next day after payment of income (clauses 4, 6, article 226 of the Tax Code of the Russian Federation).

To reduce his expenses, a participant can (clause 1, clause 1, clause 2, clause 2, clause 7 of Article 220 of the Tax Code of the Russian Federation, clause 1 of Article 226 of the Tax Code of the Russian Federation):

- submit a 3-NDFL declaration and receive a property deduction in the amount of expenses for acquiring a share in the management company;

- receive a property deduction in the amount of RUB 250,000 if there is no evidence of acquisition of a share

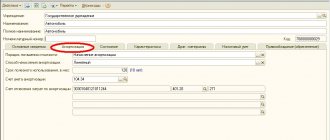

There is no standard document for this operation in 1C, so reflect the withholding of personal income tax through the document Operation, entered manually in the Operations - Operations section.

Please indicate:

- Date – date of transfer of the actual value of the share.

In the postings:

- Debit – 75.02;

- Subconto – exited participant;

- Credit – 68.01;

- Subconto – exited participant;

- Amount – personal income tax amount.

Reflection of personal income tax withholding in registers

Because Personal income tax is withheld by a manual operation, then to reflect it in the personal income tax registers and further generate reports on it, additionally enter the document Personal Tax Accounting Operation in the section Salaries and Personnel - All documents on personal income tax - Create button.

Please indicate:

- Transaction date – the date the data is reflected in the personal income tax registers.

- Income tab : Date of receipt of income - date of payment of the actual value of the share;

- Revenue code – 1542;

- Type of income – Other income ;

- Amount of income – paid actual value of the share, taking into account personal income tax;

- The date of receipt of income is the date of payment of the actual value of the share;

- The date of receipt of income is the date of payment of the actual value of the share;

tab for all rates ; movements in the personal income tax registers for its payment will be registered when personal income tax is paid to the budget.

Step-by-step instruction

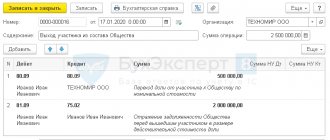

The authorized capital of the Organization is 1,000,000 rubles, where the shares of participants are:

- Ivanov Ivan Ivanovich – 500,000 rubles. (50%);

- Druzhnikov Georgy Petrovich – 300,000 rubles. (thirty%);

- LLC "Zarya" - 200,000 rubles. (20%).

As of December 31 last year, the value of the company's net assets was RUB 4,000,000.

January 17 Ivanov I.I. submitted an application to resign from the Company.

On March 23, the Company transferred to Ivanov the actual value of his share minus personal income tax to his bank card.

On the same day, the Organization paid the personal income tax withheld for this operation to the budget.

Let's look at step-by-step instructions for creating an example. PDF

| date | Debit | Credit | Accounting amount | Amount NU | the name of the operation | Documents (reports) in 1C | |

| Dt | CT | ||||||

| Withdrawal of a participant from the Company | |||||||

| January 17 | 80.09 | 80.09 | 500 000 | Transfer of a share from a participant to the Company at nominal value | Manual entry - Operation | ||

| 81.09 | 75.02 | 2 000 000 | Reflection of the company's debt to the withdrawing participant in the amount of the actual value of the share | ||||

| Transfer of the actual value of the share to the withdrawing participant | |||||||

| March 23 | 75.02 | 51 | 1 740 000 | Transfer of the actual value of the share to the withdrawing participant | Write-off from current account - Other write-off | ||

| Withholding personal income tax from the actual value of the individual participant's share | |||||||

| March 23 | 75.02 | 68.01 | 260 000 | Withholding of personal income tax from the amount of the actual value of the share of the withdrawing participant | Manual entry - Operation | ||

| — | — | 2 000 000 | Reflection of an individual's income for personal income tax | Personal income tax accounting operation - Income tab | |||

| — | — | 260 000 | Reflection of calculated personal income tax on the actual value of the share | ||||

| — | — | 260 000 | Reflection of withheld personal income tax from the actual value of the share | Personal income tax accounting operation - Tab Withheld for all rates | |||

| — | — | 260 000 | Reflection of personal income tax paid on the actual value of the share | Personal income tax accounting operation - Tab Listed for all rates | |||

| Payment of personal income tax to the budget | |||||||

| March 23 | 68.01 | 51 | 260 000 | Payment of personal income tax to the budget | Debiting from a current account – Tax payment | ||

When is it necessary to determine the value of a share?

An assessment of the value of housing is required when the owner wants to sell his property. It is good if the owner has access to the property and can evaluate it at least preliminary. However, it often happens that a citizen who has a share in an apartment not only does not live in this residential premises, but practically does not visit it. Then a professional real estate appraisal becomes even more important.

Another common situation in which such an assessment is required is the desire of the owner or a group of owners to forcibly buy out a negligible share of a co-owner. This practice is used if shareholders who decide to sell the entire apartment are faced with the disagreement of only 1 owner to carry out the transaction.

Conflicts of this type are resolved in courts, but in order for the case to be considered on its merits, the parties will need to assess the value of the disputed share. If the claims are satisfied, the owner who initiated the legal proceedings will have to pay the defendant compensation (the full cost of a negligible share), and in return, receive his part of the property.

The assessment of the share can be carried out either at the stage of preparation for filing a claim, or during the actual trial.

Determining how much a share in a residential property costs will also be necessary in the following situations:

- carrying out alienation transactions (not only purchase and sale, but also inheritance, exchange, etc.);

- division of property between spouses or heirs;

- property insurance;

- leaving a share of housing as loan collateral;

- using the housing share as the authorized capital of the company.