What law governs cash transactions?

The procedure for conducting cash transactions has changed several times. At the time of writing, Bank of Russia Directive No. 3210-U dated March 11, 2014 is in effect. The directive approved a new procedure for conducting cash transactions with banknotes and coins of the Bank of Russia on the territory of the Russian Federation by legal entities (except for banks), as well as a simplified procedure for conducting cash transactions by individual entrepreneurs (IP) and small businesses. When conducting cash transactions, recipients of budget funds are guided by Directive No. 3210-U, unless otherwise specified by a regulatory legal act regulating the procedure for conducting cash transactions by recipients of budget funds. The document was registered with the Ministry of Justice of Russia on May 23, 2014 (No. 32404) and published in the “Bulletin of the Bank of Russia” No. 46 (1524) dated May 28, 2014. Directive No. 3210-U came into force on June 1, 2014, with the exception of the requirements for software and hardware for accepting Bank of Russia banknotes, which will be in effect from January 1, 2015. From the date of entry into force of Directive No. 3210-U, Bank of Russia Regulation No. 373-P dated October 12, 2011 “On the procedure for conducting cash transactions with banknotes and coins of the Bank of Russia on the territory of the Russian Federation” became invalid.

Is it possible to issue money on account for long periods?

The law does not prohibit giving money to accountants not only for a few days or months, but also for several years. At the same time, it is worth understanding that excessively long periods of time for funds to remain with the accountable must be justified by production necessity, and the funds themselves must be spent on targeted expenses. Otherwise, there may be a risk that regulatory authorities will reclassify accountable amounts as income or an interest-free loan, which entails the need to withhold personal income tax from income (or material benefits).

Such requalification can only be challenged in court. At the same time, arbitration practice on this issue is ambiguous and largely depends on the conditions accompanying a particular situation involving accountable funds.

IMPORTANT! Pay attention to the letter of the Ministry of Finance of Russia dated January 14, 2013 No. 03-04-06/4-5, in which the department reports that until the management approves the advance report, it is impossible to unambiguously determine whether the employee will have income subject to personal income tax and what the amount of this income will be

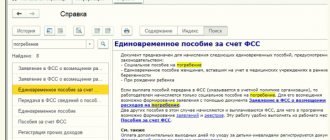

Is it possible to issue accountable amounts in 2021 if there is no report on previous amounts received under account, find out from the article.

How much money can be issued for reporting?

The maximum amount of accountable money is not limited by law. Also, the legislation does not establish a maximum period for which accountable funds are issued. But you need to understand that, according to the Directive of the Bank of Russia dated 07.10.2013 N 3073-U, cash payments in the Russian Federation between legal entities, as well as between a legal entity and an individual entrepreneur, between individual entrepreneurs related to their business activities, within one agreements concluded between these persons may be made in an amount not exceeding 100 thousand rubles. Therefore, if funds are issued for settlement under a contract, then it is logical not to exceed the limit of 100 thousand rubles.

How to receive the money

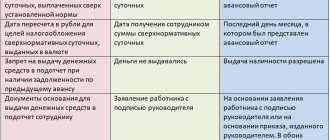

Until August 19, 2017, in order to receive money on account, an employee had to send an application to the accounting department or human resources department, which indicated the required amount and an explanation of what it would be spent on.

However, since August 19, it has become easier to issue reports. The amendments are provided for by Directive of the Central Bank of the Russian Federation dated June 19, 2017 No. 4416-U. It is not necessary to submit an application from this date. To issue money, an order from the director or another administrative document of the company is sufficient. The form of such a document is arbitrary. But it must contain the following details:

- FULL NAME. accountable person;

- document registration number;

- about the amount of cash;

- about the period for which cash is issued;

- about appointment (optional);

- director's signature and date.

Below are the new reporting samples from August 19th.

Application from an employee

Download

Order on accountable persons

Download

Is it possible to transfer accountable amounts to an employee’s salary card?

Can. The Russian Ministry of Finance recommends using this method of settlements with accountable persons (letter of the Ministry of Finance dated October 5, 2012 No. 14-03-03/728). Transferring funds to employees' accounts opened with credit institutions for settlements using payment (debit) cards is comfortable and simplifies the procedures for the employer to fulfill its obligations to reimburse travel expenses made by the employee, and also increases the efficiency and reliability of payments. But so that the tax authorities do not regard the amounts transferred to the employee’s card as wages, when transferring funds, indicate in the purpose of the payment “for travel expenses” or “for business needs.”

Suspicious transactions with accountants

As you can see, there are no obvious restrictions on the maximum amount to be reported in 2021. But this does not mean that advances from the cash register can be issued in any amount.

Tax inspectors may really not like some transactions with accountable persons:

- “Circulation” of cash in the cash register through expense reports. This trick - when money from the cash register is daily issued for reporting, returned, issued again, etc. - will clearly hint to controllers that they are trying to disguise excess cash in the cash register, which is supposed to be handed over to the bank.

- Issuing a significant amount of money to an employee for a long period of time instead of concluding a loan agreement. If the tax authorities prove that it was in fact an interest-free loan, companies can charge additional personal income tax on the material benefit received by the employee.

- Issuing amounts that significantly exceed the company's average expenses for the corresponding period.

- The advance paid is greatly inflated compared to the expenses for which it was issued, or was spent for purposes other than those for which it was received.

Despite the fact that the maximum reporting amount (2020) is not regulated by regulatory documents, we recommend not to abuse the absence of such a requirement. Issuing money exclusively for the purposes of the company’s business activities, matching the goals of a specific advance with actual expenses, and reasonable amounts of funds issued will help your company avoid unnecessary questions during tax audits.

How to correctly report the accountable amount

The accountable person is obliged, within a period not exceeding three working days after the expiration date for which cash was issued on account, or from the date of return to work, to present to the chief accountant or accountant, and in their absence, to the manager, an advance report with attached supporting documents. Checking the advance report by the chief accountant or accountant, and in their absence - by the manager, its approval by the manager and the final settlement of the advance report are carried out within the period established by the manager.

Features of issuing money for reporting to the director

The director is the main person in the company, but from the point of view of labor legislation, he is exactly the same employee as the rest of its employees. Therefore, all the above rules for issuing money on account also apply to the manager.

IMPORTANT! Relations arising as a result of election, appointment to a position or confirmation in a position are labor relations. In this case, the fact of concluding an employment contract with the general director does not matter (Articles 16–19 of the Labor Code of the Russian Federation). Therefore, the company can issue accountable funds to the director - the only founder.

The only peculiarity of issuing money for reporting to the director is that he cannot write an application for reporting and endorse it himself. Therefore, in this case, you should use not a statement, but an administrative document.

The director must comply with all other rules given in the previous section of the article, including the obligation to draw up an advance report, compliance with deadlines for submitting documentation to the accounting department confirming expenses incurred.

What is the responsibility for issuing an accountable amount to an employee who has a debt?

Tax inspectors use two options:

- There is a practice of recognizing the accountable amount received and not returned as income. Tax inspectors assess personal income tax and insurance premiums. There are court decisions supporting tax authorities: resolutions of the Federal Antimonopoly Service of the North-West District dated 06/04/2007. No. Ф04-3478/2007(34785-А46-43), FAS ZSO dated November 14, 2005. No. Ф04-8038/2005(16759-А27-25). More recent judicial practice says that the money issued was and remains accountable; ownership of it has not transferred. Cash does not become an employee’s income as long as there is a possibility of returning it to the cash desk on a voluntary basis (resolution of the Federal Antimonopoly Service of the Eastern Military District dated November 12, 2008 No. A43-3598/2008-6-65, Federal Antimonopoly Service of the North-West District dated November 7, 2008 No. A66-4549/2007 , FAS UO dated February 20, 2008 No. Ф09-516/08-С2, FAS North Caucasus Region dated December 11, 2006 No. Ф08-5708/2006-2386А).

- Most often, tax inspectors document a violation of the procedure for conducting cash transactions. Liability is provided under Article 15.1 of the Administrative Code in the amount of 4000-5000 rubles. for officials, 40,000-50,000 rubles. for legal entities.

More on the topic: Changes in the procedure for conducting cash transactions from June 1, 2014

Firm maker Accounting services for LLC, December 2014 Anna Sheshenina (Luksha) When using the material, reference is required

What does the tax office see in this?

As soon as, when checking the procedure for conducting cash transactions, the tax inspectorate sees the issuance of funds to the head of the company for reporting and the return of this money in a day or two to the cash desk of the enterprise, then it is considered that the enterprise thus stores excess cash.

Tax authorities base their arguments on the basis that:

- money is not spent at all, including on the needs of the enterprise;

- the advance report is not submitted;

- in the application for receiving funds from the cash register (if there is such an application at all) a fictitious purpose is indicated. And the application itself is needed only for formal compliance with the requirements of the Directive of the Bank of the Russian Federation No. 3210-U.

And even if a zero advance report is submitted, the tax authority will focus on the absence of actual expenditure of accountable money . It is this fact that will serve as the main evidence that the actions of the head of the company have replaced the obligation of the enterprise to keep excess money in a bank account.

Especially if several tens or hundreds of thousands of rubles are “issued” for the report, and this amount increases from time to time. As a result, it is immediately clear that the entire procedure for the return and subsequent issuance of cash for reporting is fictitious!

Moreover, the tax authority may question the actual availability of these funds . After all, very often, in order to avoid paying extra taxes on the income of the founders, the payment of dividends to them is hidden behind the issuance of endless reporting.

In addition, during an on-site audit, tax authorities may consider substantial accountable amounts that the head of the company does not spend at all as income, with all the ensuing problems. Those. calculate personal income tax on this amount! Moreover, there is judicial practice that favors the tax authorities.

Representatives of extra-budgetary funds can do the same when conducting their audit - charge insurance premiums for these amounts.

How to avoid such problems? First of all, you need to find a way to reset the existing infinite sub-report and find a way to avoid it altogether, using completely different operations.

When do you need to report for accountable funds?

According to Art.

According to clause 6.3 of the Instructions of the Central Bank of the Russian Federation dated 03/11/2014 No. 3210-U, until 08/19/2020 it was impossible to issue money on account if the employee did not provide a report on previously received amounts. But the Central Bank made changes to the report.

137 of the Labor Code of the Russian Federation, the accountant has the right to withhold the amount of debt from the employee’s salary and return it after delivery and acceptance by the JSC.

To do this, the manager must issue a special deduction order, but no later than one month from the moment the debt was formed. In cases where the advance is not repaid due to the fact that the statute of limitations on the accountable amounts has expired or the employer has forgiven the receivables to the employee, the day the employee of the institution receives income in the form of unreturned funds issued under the account will be the date from which such collection has become impossible, or the date of adoption of the corresponding decision (letter of the Ministry of Finance of the Russian Federation dated September 24, 2009 No. 03-03-06/1/610).

Consequently, an unreturned advance will be taxed in accordance with clause 1 of Art. 224 of the Tax Code of the Russian Federation, at a personal income tax rate of 13%.

Required information

To do this, the employee must specify in his application that the money should be transferred to his salary card.

Accountants often make a fatal mistake by not filing a refund to the company's cash desk. Even more often, employees simply do not return funds out of ignorance or on purpose.

An accountant or other authorized person checks the report and confirms that the funds were spent without violations.

Therefore, the issuance of money from the cash register of an enterprise may be regarded by the tax authorities as a serious violation of the procedure. What to do if the employee has not returned the remaining money?

But you should know that you must adhere to the following rules:

- obtain the employee’s consent to deduct funds from wages ();

- no later than a month later, issue a corresponding order;

- Be sure to familiarize the employee with this document.

If he does not give his consent to deduct the debt from his salary, this issue should be resolved in court. Also, do not delay with the order, otherwise you will also have to go to court.

It is believed that such a document can guarantee the company a full refund. In fact, when issuing money on account, this procedure is completely useless. Money can still be withheld from wages.

Definitions

Accountable funds are money that is issued to an accountable person for expenses related to the activities of the enterprise.

These expenses mean:

- economic needs;

- business trips;

- entertainment expenses.

An accountable person is an employee of the enterprise who receives money for certain expenses. Previously, funds could only be issued to full-time employees. True, in some cases, accounting departments of organizations circumvented this rule.

First of all, they relate to spending money according to its intended purpose. This must be documented. Failure to return money or inappropriate spending leads to serious consequences.

Grounds for extradition

Naturally, the organization keeps track of all expenses, including unplanned ones. And everything must be documented.

It is first necessary to check whether the employee has any debt for funds previously issued to him. If it is available, then funds are not issued to such an employee.

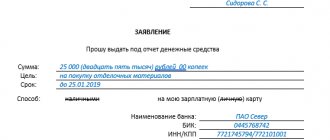

Most often this document looks like this:

If the manager of the enterprise needs the funds, he is also obliged to write a statement.

This is necessary even if the general director of the company requests the release of funds. By following the established procedure, you can avoid problems with the tax authorities in the future.

Consequences of unjustified issuance of amounts on account

For none of the reasons listed in the previous section, a company (or individual entrepreneur) cannot be held liable. And although the Code of Administrative Offenses contains Art. 15.1 entitled “Violation of the procedure for handling cash and the procedure for conducting cash transactions, as well as violation of the requirements for the use of special bank accounts”, liability for it can only arise in the following situations:

- cash settlements with legal entities in excess of the established limit;

- non-receipt of cash to the cash desk;

- violation of the procedure for storing cash;

- violations committed by payment agents.

The established amount of penalties for these violations is 4,000–5,000 rubles. for officials and 40,000–50,000 rubles. - for legal entities. There are no sanctions for other situations.

However, irresponsible issuance of funds to the account can be even more expensive - for example, if tax authorities reclassify a large amount issued to the director for a long period as an interest-free loan and charge personal income tax on the material benefit.

It is also not a difficult task for controllers to establish that the endless issuance and return of funds from the subaccount is used to disguise exceeding the cash register limit.

IMPORTANT! Even if the auditors understand the true meaning of the operations carried out by the business entity with the funds issued for accountability, they will have to defend their point of view in court. Arbitration practice in this area is very heterogeneous (for example, the decisions of the 7th Arbitration Court of Appeal dated March 26, 2014 in case No. A67-5875/2013 and the FAS of the Volga District dated March 13, 2014 No. A65-15313/2013 were adopted in favor of the company, and decision of the Moscow City Court dated 08/14/2013 in case No. 7–1920/2013 and resolution of the Federal Arbitration Court of the North Caucasus District dated 07/05/2012 No. F08-3500/12 in case No. A53-8405/2011 - in favor of the Federal Tax Service).

For more information about liability for violations committed when handling cash, read the article “Cash discipline and liability for its violation.”

What you need to know

It is important to understand that the issuance of money is a transfer of the company’s own funds, which remain so. Therefore they are not subject to income tax and insurance premiums

Interestingly, the law allows not only full-time employees to issue money on account, but also employees on civil agreements. Moreover, there are no procedural differences. The Central Bank of the Russian Federation fully supports this conclusion.

In addition, it is permissible to transfer money to regular salary cards. The main thing is to spell out this point in the internal rules.

Also see “Example of an advance report form, where can I download it?”