Can facsimiles be used on invoices?

The ancestor of the modern facsimile can be considered an ancient sign (often with an image of an animal) that our ancestors placed on property or livestock to indicate their ownership.

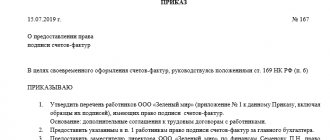

This helped in resolving disputes and disagreements regarding the determination of the owner of any material value. Director of Household Appliances LLC Konstantinov R.P., due to his job responsibilities, is forced to sign hundreds of documents every day (contracts, agreements, invoices, invoices, acts, etc.). To reduce his labor costs for signing a mountain of documents, he ordered himself a facsimile and began to use it. In addition, when leaving on a business trip, he left it in the accounting department so that the papers would not accumulate in his absence, but would be signed in a timely manner.

Facsimile on invoices 2019

The Supreme Court ruling dated August 3, 2015 No. 303-KG15-8444 clearly states that the use of facsimiles on invoices contradicts the requirements set out in Art. 169 of the Tax Code of the Russian Federation states that the invoice must be signed by an authorized person in person.

A facsimile is an exact reproduction of a document or signature by means of photography or printing, conveying all the details of the original. In other words, it is a type of printing. In the context of everyday document flow, the use of a signature imprint (facsimile) of a manager or chief accountant seems very convenient, but is fraught with consequences (

What is a facsimile signature

Facsimile translated into Russian as “do like this” is a reproduction of an identical copy of the signature of the authorized person or the person signing the documents.

This option of turning an original into a copy or reproducing a copy of any graphic original (seal, stamp, drawing, monogram, drawing, manuscript, engraving, signature) is a useful assistant for managers of state-owned enterprises, officials, and businessmen. Additional Information! Using facsimiles, you can restore ancient drawings and manuscripts, make copies of any graphic elements (words, numbers, letters, drawings, personal signatures, symbols). However, you cannot create a model, reduce a copy of an architectural structure, or burn the original piece of music to a CD.

Invoice 2021:

- From October 1, 2021, a strict requirement for the addresses of the seller and buyer is in force: now they must be indicated in accordance with the Unified State Register of Legal Entities. This means that the addresses are given in full on the new invoice form. If previously it was possible to confine oneself to an abbreviated entry, now this threatens the deprivation of a tax deduction.

- From October 1, 2021, new storage rules apply. Now documents must be stored in chronological order, by date of issue or receipt, for the relevant period. The storage period has not changed - invoices are still required to be stored for at least four years.

Comments and opinions

However, as already indicated, according to paragraph 6 of Art. 169 of the Tax Code of the Russian Federation, an invoice issued on paper must be certified by the signature of the head and chief accountant of the company or the signatures of other persons authorized to do so by an order (other administrative document) for the organization or a power of attorney on behalf of the organization.

If the document is drawn up on behalf of an individual entrepreneur, it can be signed either by the entrepreneur himself, or by any other person authorized to do so by the entrepreneur’s power of attorney.

However, the use of invoices signed with a facsimile signature is not provided for in the Tax Code of the Russian Federation. Therefore, invoices drawn up using a facsimile signature are recognized as being drawn up in violation of the established procedure and cannot be the basis for the deduction of VAT amounts presented to the buyer by the seller. The same position can be found in letters from the Ministry of Finance of Russia dated 08/27/15 No. 03-07-09/49478 and dated 06/01/10 No. 03-07-09/33.

Facsimiles are contraindicated for tax returns and calculations

By signing a tax return or calculation, the taxpayer or his representative thereby confirms the accuracy and completeness of the information specified therein (paragraph 2, paragraph 5, article 80 of the Tax Code of the Russian Federation). The instructions on the procedure for filling out declarations for most taxes indicate that the head of the organization puts a personal signature on the declaration, the date of its signing and certifies his signature with the seal of the organization. It turns out that only the personal signature of the manager or other authorized person on the declaration serves as confirmation of the information contained in it. According to the Ministry of Finance of Russia, replacing a personal signature with its facsimile reproduction cannot be adequate confirmation of this information (letter dated October 26, 2005 No. 03-01-10/8-404). The courts also note that the declaration, certified by the facsimile signature of the head of the organization, does not comply with the requirements of the tax legislation of the Russian Federation (resolution of the Federal Antimonopoly Service of the North-West dated November 2, 2011 No. A56-66090/2010 and Volgo-Vyatsky dated April 11, 2008 No. A11-2499/2007- K2-24/126 districts). Therefore, the inspectorate is not obliged to accept it. As a result, the tax authority may consider that the taxpayer did not submit a declaration or calculation in a timely manner, and fine him at least 1,000 rubles. (clause 1 of article 119 of the Tax Code of the Russian Federation). In general, the penalty for this violation is 5% of the unpaid amount of tax subject to payment or additional payment on the basis of the declaration, for each full or partial month from the day established for its submission. In this case, the amount of the fine cannot exceed 30% of the specified amount. In addition, administrative liability is also provided for violation of the deadlines for submitting a declaration to the inspectorate. An administrative fine in the amount of 300 to 500 rubles may be imposed on taxpayer officials. (Article 15.5 of the Code of Administrative Offenses of the Russian Federation).

Facsimile on invoice

The right to deduction will have to be challenged in court, based on the fact that the norms of the Tax Code of the Russian Federation do not determine the procedure for reproducing signatures of officials on an invoice. The invoice is signed by the head and chief accountant of the organization or other persons authorized to do so by an order (other administrative document) for the organization or a power of attorney on behalf of the organization (clause 6 of Article 169 of the Tax Code of the Russian Federation).

It is definitely necessary to deduct value added tax, especially if the goods are going to participate in activities subject to VAT, are accepted for accounting and the buyer has a supplier invoice (Clause 1 of Article 171 of the Tax Code of the Russian Federation). However, if the supplier's invoice on behalf of the director or chief accountant is signed using a facsimile, the taxpayer will definitely have problems, since the tax authorities, during the audit, will challenge the legality of the deduction. The Ministry of Finance of the Russian Federation has repeatedly given explanations to taxpayers about the impossibility of applying VAT deductions on facsimile invoices, referring to the fact that the norms of the Tax Code of the Russian Federation do not provide for the use of invoices signed with a facsimile signature.

Facsimile leads to the risk of confirming the accuracy of information

In the resolution of the Federal Antimonopoly Service of the North-Western District dated December 2, 2011 No. A56-66090/2010, the following provisions are mentioned as an argument “against facsimiles”. Facsimiles are not allowed to be used on powers of attorney, payment documents and other documents with financial implications.

Tax legislation allows the possibility of submitting tax returns electronically using an electronic digital signature in accordance with Federal Law No. 1-FZ of January 10, 2002. However, this law does not apply to relations arising when using other analogues of a handwritten signature. Also, the legislation on accounting and taxes and fees does not provide for the use of facsimile reproduction of a signature when preparing primary documents and invoices.

Moreover, the judges state that the interpretation of paragraph 2 of paragraph 5 of Article 80 of the Tax Code in the sense that it allows signing a tax return by affixing a facsimile stamp of the original signature would lead to the emergence in tax relations of unjustifiably high risks of confirming the completeness and reliability of information, indicated in tax returns by improper persons.

Moreover, negative property consequences in this regard could arise both for the state and for the taxpayers themselves.

Therefore, the courts proceeded from the discrepancy between the tax return, in which the signature of the head of the company was affixed by facsimile, and the requirements of tax legislation and the absence of an obligation on the part of the tax authority to accept it and verify it. Such a tax return does not confirm the validity of the information specified in it by the taxpayer.

Special rules

Facsimiles are not allowed to be used on powers of attorney, payment documents, or other documents that have financial implications.

However, not everything is so hopeless, and taxpayers have a good chance of deducting or refunding VAT on invoices containing a facsimile signature, judging by court practice.

Can facsimiles be used on invoices?

Facsimiles of invoices may deprive the buyer of a tax deduction. In our article we will tell you how to avoid this trouble, what to do to ensure that the facsimile does not complicate a businessman’s life, as well as other interesting details about the use of this sign.

Gradually, the seals acquired a more civilized appearance; instead of signs and pictures, personalized coats of arms began to appear on them, identifying the identity of the owner of the seal. They were used for certification of various documents. Seals of this type, to which we are all accustomed, first appeared in the Ancient East, where trade was well developed - they were used to seal trade agreements.

Similarities and differences between seal, stamp and facsimile

A stamp is a carrier of information that is important for the company in its work. It is used to stamp similar entries in documents, but does not give the paper legal force.

Seal – round, triangular, rectangular attribute with information on the company organization (IIN, logo, OGRN). The documents certified by her become legally significant.

The similarity of a facsimile to a seal is that it gives the paper legal force. The difference is in the area of use. A stamp is placed on the financial documentation upon signing. Facsimiles are not used on them.

Facsimile on invoices 2021

Nowadays, conventional typographic fonts are giving way to their computer predecessors. A similar process can be observed in all sorts of industries, including the field of facsimile production on invoice. That is why, to order facsimiles on invoices, you need to get acquainted in particular with typefaces, as well as with the typefaces used in digital technology.

Almost all stamps have inscriptions. At least, every facsimile on invoices is not produced without inscriptions. After all, the inscription should provide information about the name of the company, as well as its details. Then the question arises, what font is used to make these inscriptions? And when it comes to the urgent and immediate production of such stamps, this question can drive almost any person into a dead end, because very few people think about such things.

Is a stamp placed on the invoice?

However, we must not forget: the seller’s stamp must be in the delivery note or in the act. If there is no stamp, the controllers will refuse the deduction - they will recognize the “primary” document as improperly executed. But note that the law “On Accounting” does not require stamping a document. That is, the tax authorities’ claims are illegal. However, this position is guaranteed to get you into the courtroom.

If a traveler's air ticket was purchased electronically, a security-stamped boarding pass is required, among other things, to verify travel expenses for "revenue" purposes. But what to do if it is not customary to put such marks at a foreign airport?

What is facsimile signature reproduction?

Reproduction of a signature is a stamp or seal on which the original signature of the person responsible for the endorsement of documents is cut out. This is usually the signature of the head of the organization.

It is allowed to reproduce the signature if there is an existing protocol for approving the agreement of any other contracts to be concluded in the future. The agreement places importance on the documentation that will be signed in facsimile. You can also draw up an additional agreement to an already concluded contract and sign it with your own signatures of the parties.

The agreement will be considered concluded and signed by the persons upon completion of the transaction if it contains a facsimile signature, but only if signed by both parties and supported by the original round seal.

Even an invoice will be considered legally significant if:

- directed by one of the parties;

- paid by the other party;

- reflects the terms of the contract;

- supported by an additional agreement.