Justification of the legality of a loan from the founder

The founder of a legal entity (individual or organization) has the right to provide borrowed funds to the entity created by him, since the provisions of par.

Chapter 1 42 of the Civil Code of the Russian Federation allows this to be done without establishing any restrictions on such actions for the founders. Moreover, the essence of these provisions was not affected by the adjustments made by the Law “On Amendments...” dated July 26, 2017 No. 212-FZ, by virtue of which Ch. 42 of the Civil Code of the Russian Federation acquired a new edition as of June 1, 2018. The advantages of a loan provided by the founder are obvious, since the question of obtaining it:

- resolved promptly;

- does not require preliminary approvals and systematic provision of data for control, as in the situation with a loan issued by a bank;

- can be accepted on very favorable terms for the borrower (with a longer repayment period or lower interest rate than when applying for a loan from a bank);

- may result in debt forgiveness.

Why does the founder providing the loan agree to such conditions? Because he himself is interested in ensuring the successful operation of the organization in which he has a stake and from which he expects to receive income.

How to take into account the receipt and repayment of an interest-free loan from the founder - a legal entity? The answer to this question is in ConsultantPlus. Learn the material by getting trial access to the system for free.

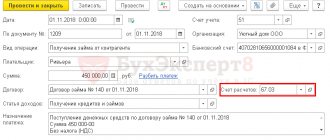

Loan repayment

To conduct a transaction correctly, you need not only to correctly draw up the contract and take into account the current laws of 2021, but also to avoid mistakes regarding the return of funds.

There are two situations. In the first case, the return period is specified in the contract; in the second case, this information may not be contained in the documentation. In such a situation, the return of funds (or other valuables) must occur after a written request from the creditor. The maximum waiting period after receiving the letter is 30 days.

It is impossible to return a loan that was repaid in cash with material assets, without additional financial losses in the form of taxes. If you borrowed money, it must be returned; if material assets, you need to return similar material assets. If, however, the return is made using material means, the organization will pay tax, since such an operation will be treated as a sale. Tax is paid in accordance with the chosen taxation system.

Loan agreement from the founder: registration

Relations arising in relation to a loan received by a legal entity, regardless of who the lender is and what the amount lent to him, must be formalized in writing, that is, by concluding an agreement (Clause 1 of Article 808 of the Civil Code of the Russian Federation).

It is in this document that you need to indicate:

- data of both parties;

- information about what exactly is being loaned (cash, things or securities) and what is the amount (or value) of the transferred;

- conditions for using borrowed funds (period, purpose, interest rate, availability of collateral);

- the procedure for the transfer and return of borrowed property (including early return) and payment of interest;

- other rights and obligations of the parties;

- types of liability arising from violation of the terms of the contract;

- rules that come into force in force majeure circumstances;

- procedure for resolving disputes.

In relation to the items and securities to be transferred, you will additionally need to draw up an inventory containing indications of the specific characteristics of the items being transferred.

Read more about drawing up a loan agreement in the following articles:

- “Ordinary and gratuitous loan agreement from the founder”;

- “Sample interest-free loan agreement from the founder.”

How to get the required amount?

If we are talking about a loan given by the owner of a company, it makes sense to consider a limited liability company as a subject of loan relations. There is no limit to the amount of funds that the founder transfers to his company. But it is impossible to make such a transfer of funds without official confirmation (if we are talking about legal borrowing relationships). This is why it is important to have a written contract, which must be in writing on official letterhead. If the company focuses only on the payment order and receipt order, without drawing up an agreement that the loan is received for a certain period, the court may refuse to recognize the fact that a loan relationship exists between the parties. But there is no point in taking such risks for the enterprise and its founder.

Key points of the borrowing agreement

There are a number of points that are of particular importance for the tax consequences of a loan agreement with the founder. Among them is the ability to make an agreement:

- Provides for the payment of interest at a frequency convenient for its parties. The absence of reservations in this regard will require monthly interest accrual (clause 3 of Article 809 of the Civil Code of the Russian Federation).

- Interest-free (in the case of loaning things, the absence of interest becomes mandatory - clause 4 of Article 809 of the Civil Code of the Russian Federation). In order for an agreement to be considered interest-free, the condition of non-accrual of interest must be fixed in the text of the document, since the absence of such a condition will entail the need to calculate interest on the key rate of the Bank of Russia (clause 1 of Article 809 of the Civil Code of the Russian Federation).

- Targeted. For this situation, the contract will have to provide for a procedure for monitoring the use of what was loaned and a procedure for returning it if misuse is identified (Article 814 of the Civil Code of the Russian Federation). Accordingly, interest accrued on borrowed funds used for other purposes will not be taken into account to reduce the tax base for profits or the simplified tax system; It will also be impossible to take into account the negative exchange rate difference on a loan issued by a foreign founder in foreign currency.

- Does not contain an indication of the repayment period or makes it dependent on the moment of reclaiming the loan from the lender. Under such conditions, the debt must be repaid no later than the 30th day from the date of the demand from the lender, unless a different period is specified in the text of the agreement (clause 1 of Article 810 of the Civil Code of the Russian Federation). Moreover, the date of return (unless otherwise provided by the agreement) will be considered the day of actual receipt of the debt by the lender (clause 3 of Article 810 of the Civil Code of the Russian Federation).

In order to avoid undesirable consequences, it is recommended to stipulate each of the listed points in detail in the text of the loan agreement.

Interest-bearing loan: tax implications

Quite often, a loan agreement, even one concluded with the founder, provides for the payment of interest on it. What tax consequences will an interest-bearing loan from the founder bring in 2021?

The interest amounts received by the lender will become his taxable income. The founder-individual (both Russian and foreigner) will have to pay personal income tax from them at a rate of 13% (clause 1 of Article 224 of the Tax Code of the Russian Federation) or 30% (clause 3 of Article 224 of the Tax Code of the Russian Federation), respectively, and withholding tax on income will be carried out by the borrower (clause 1 of Article 209 of the Tax Code of the Russian Federation). And the founder - a legal entity of Russian origin, upon receipt of interest, will be the payer of income tax (clause 6 of Article 250 of the Tax Code of the Russian Federation) or the simplified tax system (clause 1 of Article 346.15 of the Tax Code of the Russian Federation) at rates of 20% (clause 1 of Article 284 Tax Code of the Russian Federation) and 15% or 6% (clause 1 of Article 346.20 of the Tax Code of the Russian Federation), respectively. On the income of the founder, who is a foreign organization, when paying interest to him, the borrower will also have to withhold tax himself (clause 1 of Article 310 of the Tax Code of the Russian Federation) at a rate of 20% (subclause 1 of clause 2 of Article 284 of the Tax Code of the Russian Federation). Under certain conditions, part of the interest accrued in favor of a foreign founder is equated to dividends (clause 6 of Article 269 of the Tax Code of the Russian Federation) and is taxed at the corresponding rate of 15% (clause 3 of Article 224 and clause 3 of Article 284 of the Tax Code of the Russian Federation) .

From what base will the tax be calculated: from interest, the amount of which is provided for in the borrowing agreement, or from those that correspond to the real market level of such income? This question arises because the parties to the loan agreement may be mutually dependent. Let us recall that the interdependence between the founder and the legal entity in which he participates is directly related to the share of such participation (both direct and taking into account indirect contribution). For a dependence to arise, it is enough for the share to slightly exceed 25% (subclauses 1, 2, clause 2, article 105.1 of the Tax Code of the Russian Federation).

Thus, in relation to an interest-bearing borrowing agreement, the following situations are possible:

- There is no dependency. Then the prices agreed upon by the parties to the transaction are considered market prices (clause 1 of Article 105.3 of the Tax Code of the Russian Federation), and there is no need to revise them.

- There is a dependence. Its consequences will be different for resident founders and non-resident founders. In the first case, transaction prices will be controlled only when the amount of all transactions between the parties for a calendar year exceeds 1 billion rubles. (Subclause 1, Clause 2, Article 105.14 of the Tax Code of the Russian Federation). In the second case (with a non-resident), the transaction will always be controlled.

The recipient of the loan has the right to accept interest accrued in accordance with the terms of the agreement as a reduction in the profit base (subclause 2, clause 1, article 265 of the Tax Code of the Russian Federation) or the simplified tax system, the base of which is determined taking into account expenses (subclause 9, clause 1, article 346.16 Tax Code of the Russian Federation). However, in relation to a controlled transaction with a foreign founder, the determination of the amount of interest included in expenses occurs in a special order (Article 269 of the Tax Code of the Russian Federation), and it is here that, if the maximum permissible amount is exceeded, the question arises of equating interest to dividends for tax purposes .

Business complained about tax authorities' claims against loans from shareholders

RBC sent a request to the Federal Tax Service.

Why do businesses need foreign loans?

Read on RBC Pro

Shiva in the sack: why companies fell in love with multi-armed employees Paying sick leave and maternity leave: what has changed for employers How to deal with client excuses and ultimately convince him: 10 ways Virgin Galactic has driven the market crazy. Here are two more powerful space stocks

The need for cross-border loans is due to the specifics of the work of suppliers, Anton Zykov, partner and head of Deloitte’s tax dispute resolution group, explained to RBC. For example, distributors purchase goods from foreign manufacturers and resell them on the local market, while retail chains and stores seek significant deferments from them - up to 6-8 months. When purchasing goods, wholesale suppliers pay factories immediately and receive money from their partners much later. As a result, cash gaps arise, to cover which suppliers need loans.

“In itself, the situation of such a gap occurring and covering it with borrowed funds is common, and therefore should not be recognized by default as unreasonable or unlawful,” RATEK emphasizes in its letter. If, instead of a loan, the distributor increases the deferred payment, the price of the product itself will rise.

In the opinion of businesses, the tax office should not refuse to take into account interest expenses solely due to interdependence with the creditor. It is necessary to prove intent to evade taxes on interest income, for example through the artificial use of low-tax jurisdictions.

The problem of assessing debt financing lies in the instability of the positions of the courts, Ermolaev stated. Inspections, “not wanting to understand the activities of each specific company, equate the difference in payment terms with dishonesty and force taxpayers to justify themselves, explain why they borrowed money and whether they could build their business in such a way as to operate without loans,” says Zykov. In a good way, tax authorities must prove that the company acted recklessly or with malicious intent, taking into account irrational expenses in expenses, he adds.

Why is the tax office unhappy?

Cross-border and domestic Russian loans between related parties always raise questions from the tax authorities - for example, if a company borrows from its shareholder, says Ermolaev. “The state, in order to replenish the budget, is interested in foreign companies investing directly in the authorized capital of Russian companies, rather than issuing loans,” adds Zykov. Tax amounts vary greatly when an investor invests money in the authorized capital and when he issues a loan. In the case of a capital contribution, the company then pays dividends, which are taxed; in the case of a loan, when the money is returned to the founder, “the state does not receive a penny,” he explains.

As the head of the Federal Tax Service, Daniil Egorov, stated at the Tax Forum at the Chamber of Commerce and Industry, borrowings and loans cannot but be considered as particularly attractive institutions for aggressive tax planning. “Imagine: one organization generates net profit, pays all taxes, then transfers dividends and pays taxes on dividends. At this time, another organization creates debt obligations and reduces income by the amount of interest paid,” said the head of the Federal Tax Service.

The affiliation of the borrower and the lender in itself should not lead to an increase in tax liabilities. During inspections, inspectors evaluate:

- loan size (it should not be unreasonably large);

- conditions (interest rate, payment terms, etc.) should not differ from market ones;

- the presence of a business purpose (for example, covering cash gaps, the occurrence of which was not influenced by the parent company or other related party);

- whether the loan agreement corresponds to the real economic meaning (for example, issuing a loan to an existing enterprise, and not to one being built from scratch; the amount of interest paid does not coincide with the amount of retained earnings or unpaid dividends; interest is paid on time).

If an independent lender (for example, a bank) would not have provided a similar “inadequately large” loan on market terms, the tax authority may suspect a “scheme.” Suspicions arise that cross-border loans contribute to the transfer of profits abroad, explains Zykov. In this case, the company will exclude the recorded costs of paying interest on the loan from expenses and will be charged additional income tax.

The situation tends to escalate at the end of the year, when tax inspectors across the country determine which company to conduct an on-site audit, continues the Deloitte partner. The statute of limitations for prosecution is three years. Therefore, for example, if the tax office does not begin an audit in December 2021, it will no longer be able to calculate taxes for 2021. Since October, large taxpayers begin to receive requests from tax inspectorates, says Zykov.

The court did not see the point in a loan from abroad

One of the landmark cases was the case of the tire wholesaler Continental Tires Rus. The company provided its customers (retailers) with deferred payments for goods. To cover the cash gap, the company took out loans from the parent company in Germany, Continental AG.

To repay borrowed funds, the company transferred large sums of money from Russia to Germany, and deducted interest costs from profits, reducing the tax base.

The court concluded that Continental Tires Rus did not have the right to reduce profits. The companies added an additional 106 million rubles. income taxes, penalties and fines. According to the tax authorities, she could not have borrowed money, but agreed with the parent company to defer payments for the tires supplied and pay when she received the money from her customers.

How it is proposed to solve the problem

“It is unacceptable to label intra-group financing as ‘vicious’. It is necessary to examine the circumstances of each specific case,” says Ermolaev. At the same time, the business itself, carrying out transactions within the group, collects documents to confirm the validity of the transactions.

In August, the Federal Tax Service issued a letter “On certain issues of taxation of intragroup services”, where it limited the powers of inspectors when checking the cost of transactions. RATEK believes that similar approaches are applicable to the assessment of borrowing relationships. For example, in this letter, issues of assessing the marketability of the price of services were attributed to the competence of the Federal Tax Service when checking controlled transactions according to the rules of transfer pricing, and not to the powers of territorial tax authorities. This approach, according to the association, is also valid for cross-border loans, since the terms of payment under intragroup agreements must be taken into account when assessing the relationship of the parties in the context of determining transfer prices.

According to business, when assessing the validity of loans, one must proceed from the following point: if alternative solutions would lead to similar financial results, then debt financing cannot be considered unreasonable.

In the letter, the business expressed the hope that the Federal Tax Service will raise this problem at the site of the Service Advisory Council and issue similar clarifications on the taxation of cross-border loans, formulating “clear and unambiguous criteria.”

The head of the Federal Tax Service, answering a question at the All-Russian Tax Forum, promised to work on this problem: “We have already formed a team to study such issues both on behalf of taxpayers and audit companies, and on our part. Let us see where points of certainty can be found in order to provide legal clarity.”

Loan without interest: what taxes are possible

What tax consequences does an interest-free loan from the founder have? For a loan taken without interest, the issue of taxation also turns out to be related to the presence of mutual dependence between the parties to the transaction and whether the founder is a resident or non-resident. The situations here are:

- There is no dependency. In this case, the lack of taxable income in the form of interest from the lender is completely legal (Clause 1, Article 105.3 of the Tax Code of the Russian Federation). Accordingly, the borrower has no expenses.

- There is a dependency. For her, the inclusion of the founder as a resident becomes significant. If the founder is the founder, then the transaction to provide an interest-free loan is not recognized as controlled (subclause 7, clause 4, article 105.14 of the Tax Code of the Russian Federation). If the founder turns out to be a non-resident, then the absence of interest on the loan makes the transaction not subject to control, since in this case the conditions for him, provided for in Art. 269 of the Tax Code of the Russian Federation.

Thus, an interest-free loan will not have tax consequences in any case.

Read about the reflection of a loan in accounting in the material “Accounting for loans and borrowings in accounting.”

Options for terminating the borrowing agreement

The loan agreement with the founder can end in the usual manner: at the end of its term or ahead of schedule - by returning the borrower with payment of the due interest, if any was provided for.

Read how to return the loan to the founder on the card here.

However, it is not uncommon for a loan taken from the founder to have the debt forgiven. This opportunity is provided by Art. 415 of the Civil Code of the Russian Federation. True, it is impossible to provide for it in an agreement (just like issuing a loan for an unlimited time). The forgiveness will have to be completed in a separate document.

See also “Procedure for writing off a loan agreement (nuances)”.

What are the tax consequences of a loan from the founder ending in forgiveness in 2021? The loan amount transferred free of charge into the ownership of the borrower will become his income, which, as non-operating income, will fall under the income tax or simplified tax system. However, there are exceptions that allow such income not to be considered taxable. They relate to a situation where the founder’s share exceeds 50% of the contribution to the authorized capital (clause 11 of Article 251 of the Tax Code of the Russian Federation). In this case, non-monetary funds cannot be transferred by the borrower to a third party during the year.

How to borrow money without interest?

On the one hand, the company has the right to take a certain amount from the founder without interest. With his consent, of course. But in this case, the question arises: will the founder receive profit in this case, and how does the legislation of the Russian Federation “look” at this situation? Of course, if we consider the situation from an “everyday” point of view, the founder, if he gives a loan without interest, will not receive a profit. But the Tax Code looks at this situation differently. It turns out that the founder could receive direct profit, but deliberately refuses this. And if we are talking about income (even if only estimated), then the question of tax on this income immediately arises. The situation is clarified by letter from the Ministry of Finance No. 03-01-18/29936.

This letter concerns only the situation when we are talking about a transaction between related parties that may be controlled. To decide whether your transaction (loan) is just that, you need to answer two questions: are you related parties, and is the transaction itself controlled?

According to Art. 105 of the Tax Code of the Russian Federation, interdependent persons can be both individuals and legal entities. If we talk about the relationship between an individual and an organization, it is necessary to pay attention to the share of participation of this person. If it is more than 25%, it means that the persons will be interdependent, and therefore you may act to the detriment of “personal” interests.

According to Article 105 of the Tax Code, a transaction is controlled if the income from transactions that were concluded by related parties during the year exceeded 1 billion rubles. Thus, if you are interdependent persons, but the founder lends less than 1 billion rubles, you don’t have to worry about the tax on the income that you did not receive. In this case, the tax service will not have any additional questions.

If you are interdependent persons, but the founder lends less than 1 billion rubles, you don’t have to worry about the tax on the income that you did not receive.

Also, the tax base will not be increased for the organization itself if the founder borrows a certain amount without interest. On the one hand, in this situation there is a benefit for the organization. On the other hand, the procedure for increasing the tax base in the event of receiving an interest-free loan is not specified (you will not find this information in Chapter 25 of the Tax Code of the Russian Federation), and therefore it will not take place.

There is another situation that concerns a reverse loan. If the LLC lends a certain amount to the founder, it turns out that the individual is in an advantageous position due to the absence of interest. In this case, the material benefit is taxed. The positive thing is that the tax is minimal and not comparable to what would be charged in the case of a bank loan.

Results

A loan from the founder is an operation not prohibited by current legislation. Its provision must be accompanied by the execution of an agreement, a number of conditions of which should be treated with special attention. The interest stipulated by the agreement will be the lender's income and the borrower's expense. With an interest-free loan, there are no tax consequences. A loan forgiven by the lender will become non-operating income of the borrower if the share of the founder in its authorized capital does not exceed 50%.

Sources: civil code of the Russian Federation

You can find more complete information on the topic in ConsultantPlus. Free trial access to the system for 2 days.