Four types of operations

IMPORTANT! Information on changes in balance currency balances from ConsultantPlus is available at the link

In the process of activity of a legal entity, there is a permanent change in the structure and volume of property/sources of its appearance. These changes are carried out under the influence of various chemical agents.

The latter lead to balance adjustments.

There are four types of business transactions. Chemical agents are divided into types depending on their impact on the balance. Any type of transaction affects both an asset and a liability. HOs change the structure of the balance sheet, but they may not affect the values within the accounting framework. The balance sheet often remains unchanged. That is, the principle of equality is not violated.

Typical balance changes directly depend on what type of transaction is performed. Let's take a closer look at all 4 types.

First type

Schematically, the change can be expressed as follows: A+ A-. That is, one asset is multiplied, the other is reduced. Decrease/increase is performed by the same amount. The changes apply exclusively to assets. The operation in this case will apply only to objects that are on the farm.

Examples of type 1 chemical weapons:

- Exploitation of valuables.

- Manufacturing process.

- Release of finished goods.

- Shipment of goods.

- Covering accounts receivable.

The first type displays adjustments to asset items.

Example No. 1. Let's look at the postings used in type 1 operations:

- DT50 KT51. Transfer of money from the account to the cash desk.

- DT20 KT10. Direction of materials for production needs.

- DT43 KT20. Release of goods into production.

- DT94 KT10. Recording shortages of materials based on inventory results.

- DT58 KT51. Providing a loan that involves accrual of interest.

- DT01 KT10. Release of materials into production.

Example No. 2. The release of materials into production has been completed. They will be used to organize the stage. Materials were supplied in the amount of 20,000 rubles. In this case, the asset “Spending in unfinished production” will be increased by 20,000 rubles.

At the same time, the asset “Raw materials and materials” decreases in the amount of 20,000 rubles. The balance sheet remains the same.

Second type

Schematically, the change can be expressed as P+ P-. One direction of the liability increases, the other decreases. The decrease/increase occurs by the same amount. Adjustments affect only the liability. That is, only the sources of funds change. As a result of operations, the movement of financial sources begins. The second type includes these chemical weapons:

- Transfer of premiums from the consumption fund.

- Deductions from salary.

- Increase in reserve fund.

Example No. 1. At the meeting of the founders, it was decided to direct the profit in the amount of 50,000 rubles. to increase the reserve fund. The basis of the operation is the minutes of the meeting. In this case, the “Reserve Fund” liability will be replenished by 50,000 rubles. The liability “Unused profit” is reduced by the same amount.

Let's look at the postings used in operations of the second type:

- DT84 KT82. Reserve capital increases due to retained earnings.

- DT70 KT68. Tax on personal income.

- DT80 KT84. The authorized capital was reduced to the amount of net assets.

- DT96 KT70. Accrual of vacation pay from the reserve.

- DT91 KT66. Receiving interest on a short-term loan.

The basis for the postings is the minutes of the meeting at which a decision was made to replenish the fund.

Third type

Schematically, the change can be expressed as follows: A+ P+. Both assets and liabilities are multiplied. The balance currency and its total are also multiplied. Examples of third type operations:

- An increase in the volume of founding contributions made through the accrual of money.

- Depreciation on, intangible assets.

- Payroll accrual.

- Social security payments.

- Lending.

- Advances from customers.

The 3rd type of financial assets involves multiplying assets/liabilities while maintaining the same indicators. The balance currency will be increased.

Example. Raw materials worth RUB 200,000 arrived from the supplier. It was entered into the warehouse. In this case, both the asset “Raw Materials” and the liability “Accounts Payable to Suppliers” increase by a similar amount. The total in both directions (asset/liability) increases by 100,000 rubles.

Example of entries for type 3 transactions:

- DT20 KT70. Calculation of salaries for employees employed in the main production.

- DT51 KT66. Obtaining a short-term loan (money issued by the bank).

- DT76 KT91. Accrual of a fine for violation of the terms of the contract.

- DT08 KT70. Calculation of salaries for employees who are involved in the installation of OS objects.

- DT41 KT60. Shopping.

- DT51 KT67. Obtaining long-term loans.

Primary documents: agreements with banks, counterparties.

Transactions affecting the value of the balance sheet currency

Transactions affecting the value of the balance sheet currency

List of used literature

The activities of organizations consist of a number of processes representing the movement of economic funds and property in various forms. In turn, each process consists of many operations, which are separate moments of the movement of economic assets.

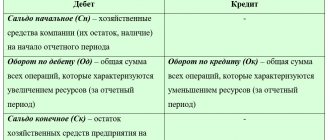

Each business transaction occurring in an organization changes either the size of the property, or the size of the sources of its formation, or at the same time both the size of the property and its sources of formation. In this case, changes can be either upward or downward; the balance sheet currency also changes.

Since the balance reflects the state of funds, each operation will affect the balance and change any of its items. Therefore, in the process of economic activity, there is a constant and continuous change in balance sheet items, which ultimately leads to a change in the totals of sections and totals of both assets and liabilities.

To do this, you need to look at the impact of individual transactions on the balance sheet.

The work consists of an introduction, main part and bibliography.

Types of changes in the balance sheet.

The variety of business transactions carried out in organizations affects the amount of property and the sources of its formation.

Some operations change the composition of funds, others change the sources of these funds, others simultaneously increase both the composition of funds and their sources, and others simultaneously reduce both. This is reflected in changes in balance sheet items.

The first type of business transactions causes changes only in the balance sheet asset: one of its items increases, another decreases by the amount of the business transaction, i.e. the composition of business assets and their placement change. The balance sheet remains unchanged:

A – X + X = P.

Example 1. For previously shipped goods, money was received from the buyer to the bank account - 100,000 rubles. Consequently, in the balance sheet under the item “Current accounts” the amount will increase, and under the item “Settlements with buyers and customers” it will decrease (the debt will decrease).

Operations of the first type include all operations involving the use of material assets in the production process, the release of finished products from production, their shipment, the repayment of accounts receivable, the receipt of funds in cash from a current account, etc.

The second type of business transactions causes changes only in the liability side of the balance sheet: one of its items increases, another decreases, i.e., the sources of economic funds change. The balance sheet remains unchanged:

A = P + X – X

Example 2. Income tax in the amount of 1,300 rubles was withheld from accrued wages. In the balance sheet under the item “Settlements with personnel for wages” the debt will decrease, and under the item “Settlements for taxes and fees” the debt will increase.

The second type includes operations for the distribution of profits, withholding taxes from wages, etc.

The third type of business transactions causes changes in the assets and liabilities of the balance sheet simultaneously in the direction of increasing its items. The balance sheet total also increases by the amount of the business transaction for the asset and liability:

A + X = P + X.

Example 3. Materials worth 100,000 rubles were received from a supplier, payment for which was not made. The balance sheet asset item “Inventories” and the liability item “Accounts payable to suppliers” will increase by the amount of the cost of materials.

This type of operations includes operations for calculating depreciation on fixed assets, depreciation on intangible assets, social insurance contributions, payroll and bonuses included in the cost of production, etc.

The fourth type of business transactions causes changes in the assets and liabilities of the balance sheet simultaneously towards a decrease in its items. The balance sheet total will also decrease by the amount of the business transaction:

A – X = P – X.

Example 4. Payments to the budget in the amount of 6,000 rubles were transferred from the current account. The asset item of the balance sheet “Current accounts” and the liability item of the balance sheet “Debt on taxes and fees” are reduced by 6,000 rubles.

This type includes all transactions for payment of all types of accounts payable (to the budget, extra-budgetary funds, lessors, suppliers, workers and employees).

Practical task.

Specify the type of balance changes

| Contents of a business transaction | Amount, rub. | Type of changes |

| The cost of the computer received from the supplier is reflected | 50 000 | III |

Increasing the balance sheet asset item “Investment in non-current assets”

(account 08 chart of accounts)

Increase in the balance sheet liability item “Settlements with suppliers and contractors”

(account 60 of the chart of accounts)

| Contents of a business transaction | Amount, rub. | Type of changes |

| Value added tax (VAT) on the received computer is taken into account | 9 000 | III |

Increasing the balance sheet asset item “VAT on purchased assets”

(account 19 of the chart of accounts)

Increase in the balance sheet liability item “Settlements with suppliers and contractors”

(account 60 of the chart of accounts)

| Contents of a business transaction | Amount, rub. | Type of changes |

| The cost of the computer was paid to the supplier from the current account | 59 000 | IV |

Decrease in the balance sheet asset item “Current account” (account 51 of the chart of accounts)

Decrease in the balance sheet liability item “Settlements with suppliers and contractors” (account 60 of the chart of accounts)

| Contents of a business transaction | Amount, rub. | Type of changes |

| The capitalized computer was put into operation | 50 000 | I |

Increase in the balance sheet asset item “Fixed assets” (account 01 of the chart of accounts)

Decrease in the balance sheet asset item “Investment in non-current assets”

(account 08 chart of accounts)

| Contents of a business transaction | Amount, rub. | Type of changes |

| Money has been received from the current account at the cash register for the payment of wages. | 200 000 | I |

Increase in the balance sheet asset item “Cash” (account 50 of the chart of accounts)

Decrease in the balance sheet asset item “Current account” (account 51 of the chart of accounts)

| Contents of a business transaction | Amount, rub. | Type of changes |

| Salaries issued from the cash register | 200 000 | IV |

Decrease in the balance sheet asset item “Cash” (account 50 of the chart of accounts)

Decrease in the balance sheet asset item “Settlements with personnel for wages”

(account 70 of the chart of accounts)

| Contents of a business transaction | Amount, rub. | Type of changes |

| Salaries issued from the cash register | 200 000 | IV |

Increase in the liability item of the balance sheet “Authorized capital” (account 80 of the chart of accounts)

Decrease in the balance sheet liability item “Retained earnings”

(account 84 chart of accounts)

Selfeducation:

Prepare for the home test by mastering Lecture 3 and solving a similar problem.

LECTURE 4. Accounting and double entry

Lesson plan:

1. Accounting accounts. Account structure. Active and passive accounts.

2. Double entry method.

3. Synthetic and analytical accounts.

4. Turnover statements.

5. Chart of accounts.

Types of business transactions

For this purpose, accounting accounts are used, which display information about transactions.

Lecture 8. Classification of balance sheets

Classification of balance sheets

Classification of balance sheets is carried out on the following main grounds:

1) By structure;

2) By the presence of regulations;

3) By the method of evaluating articles;

4) According to the intended purpose.

According to the balance sheet structure.

According to its structure, i.e. According to the order of arrangement of articles and presentation of information, balances are divided into horizontal and vertical.

Horizontal balances are characteristic of the continental school of accounting; they are compiled in Western European countries and the Russian Federation.

In horizontal balance sheets, the Asset is located on the same level as the Liability, i.e. (horizontally), as shown below:

The horizontal balance equation is as follows:

Active = Liability

Vertical balance is characteristic of the Anglo-Saxon school of accounting.

It consists of countries that were once part of Great Britain, namely the USA, Great Britain, Australia, New Zealand, India, Canada.

The vertical balance equation is as follows:

Asset – Borrowed funds = Own funds.

In a vertical balance sheet, Liability is located below Asset:

The vertical balance sheet in its final line provides users with very important information about the amount of own funds , therefore, for investors - individuals, such reporting will be more understandable.

Since in countries that use a vertical balance sheet, and, above all, in the USA and Great Britain, there are a significant number of investors on the stock market - individuals , this type of balance sheet is the most acceptable for them.

In countries that use horizontal balance, large capital is more present in the stock market .

Specialists of such organizations are well versed in accounting statements, including balance sheets, so the horizontal balance sheet is clear to them and quite satisfactory to them.

The impact of business transactions on the balance sheet currency

Every day, in the process of economic activity, each organization carries out many business transactions. They have a direct impact on the value of balance sheet items, but the equality of assets and liabilities is not violated. At the same time, the balance sheet currency can change: it can increase and decrease due to changes in asset and liability items.

Business transactions can affect:

– asset items, causing a regrouping of resources;

– liability items, causing a regrouping of the sources of formation of these resources;

– asset and liability items, causing an increase or decrease in these resources.

This occurs due to the fact that each business transaction simultaneously affects two balance sheet items: only in assets, only in liabilities, or in assets and liabilities. Depending on the impact of business transactions on the state of balance sheet items, they can be divided into four types.

Operations of the first type make changes to the composition of the organization’s property, i.e. only asset items are affected.

For example, finished products worth 50,000 rubles are released from production and put into storage.

The impact of business transactions on the balance sheet currency

rub., and under the item “Current accounts” - decreased (- I) by 5 thousand rubles, i.e. e. there was a movement of funds within the balance sheet asset and, in general, the balance sheet currency did not change.

If we denote the total of the balance sheet asset as “A”, the total of the balance sheet liability as “P”, the changes occurring in the balance sheet under the influence of a business transaction as “I”, then the influence of business transactions of the first type can be expressed in the form of the following formula:

1) ∑ A +

I - I = ∑ P, ᴛ.ᴇ. ∑ A + 5 – 5 = ∑P

Operations of the second type change the sources of formation of the organization’s property, i.e., they affect only the liability side of the balance sheet. In this case, the balance sheet currency does not change.

For example, due to a short-term bank loan, debts to suppliers in the amount of 100 thousand rubles were repaid. This business transaction affects the following balance sheet liability items: “Short-term bank loans” and “Suppliers and contractors,” which characterize the sources of formation of the organization’s property, are located in section V of the balance sheet liability “Short-term liabilities.” Carrying out this business transaction means that under the article “Short-term bank loans” the amount is 100 thousand rubles. increased, and under the item “Suppliers and contractors” - decreased by 100 thousand rubles, i.e. there was a movement of amounts within the balance sheet liabilities and, in general, the balance sheet currency did not change. Using the previous notation, the impact of a business transaction of the second type can be written as the following formula:

2) ∑ A = ∑ P + I - I, ᴛ.ᴇ. ∑ P + 100 – 100 = ∑ A

Operations of the third type simultaneously change the amount of property and the sources of its formation, and the changes occur in the direction of increase. Moreover, the balance sheet currency for assets and liabilities increases by an equal amount.

For example, a short-term bank loan in the amount of 200 thousand rubles was credited to the organization’s foreign currency account.

This business transaction affects two balance sheet items: “Cash,” (this item is located in the 2nd asset section of the balance sheet, “Current assets,” and “Loans and credits,” (this item is shown in the 5th liability section, “Current liabilities”).

The implementation of this business transaction causes an increase in the item “Cash” by the amount of 200 thousand rubles. and at the same time, an increase in the organization’s debt on a short-term loan received from a bank, i.e. the item “Loans and credits” also increased by 200 thousand rubles.

The balance sheet currency for both assets and liabilities increased (+I) by 200 thousand rubles.

The impact of a business transaction of the third type on the balance sheet can be written as the following formula:

3) ∑ A + I = ∑ P + I, ᴛ.ᴇ. ∑ A + 200 = ∑ P + 200

Operations of the fourth type simultaneously change the amount of property and the sources of its formation, while the changes occur in the direction of decrease. Moreover, the balance sheet currency for assets and liabilities decreases by an equal amount.

For example, a salary to the organization’s employees in the amount of 50 thousand rubles was issued from the cash register.

This business transaction affects two balance sheet items: “Cash”, which is located in section II of the balance sheet asset “Current assets”, and “Accounts payable to the personnel of the organization”, which is shown in section V of the balance sheet liability “Current liabilities”.

Carrying out this business transaction means that under the item “Cash” the amount decreased by 50 thousand rubles, but at the same time the amount under the item “Accounts payable to the personnel of the organization” decreased by 50 thousand rubles, since when paying wages the organization’s debt workers decreases. The balance sheet currency for both assets and liabilities decreased (-I) by - 50 thousand rubles.

The impact of a fourth type of business transaction on the balance sheet can be expressed as the following formula:

4) ∑ A - I = ∑ P - I, ᴛ.ᴇ. ∑ A - 5 = ∑ P - 5.

As can be seen from the above formulas, the equality of the currency of the asset and liability of the balance sheet is preserved under the influence of any type of business transaction.

These formulas are of great importance for reflecting the influence of various types of business transactions not only on the balance sheet, but also on the organization of accounting and analysis of the financial and economic activities of the enterprise, assessment of its financial and property status in the conditions of using various means - computer technology.