Basic elements of accounting method

Accounting problems are solved through the use of various methods and techniques, the totality of which is called the accounting method, which includes the following main elements:

Documentation is a written certificate of a completed business transaction, giving legal force to accounting data;

Valuation is a way of expressing funds and their sources in monetary terms;

accounting accounts - a method of grouping the current reflection of property, liabilities and transactions;

Double entry is an interconnected reflection of business transactions on accounting accounts, when each transaction is simultaneously recorded as a debit to one account and a credit to another account for the same amount;

Inventory – checking the availability of property listed on the balance sheet of an organization, carried out by counting, describing, weighing, mutual reconciliation, evaluation of identified funds, and comparing the obtained data with accounting data;

Calculation – calculation of the cost per unit of products, works, services in monetary terms, that is, calculation of the cost;

Principles for recording them in accounting

All financial transactions must be recorded in accordance with the time of their occurrence and monetary value. The moment of the operation shows:

- redistribution of ownership of a certain product, work, service

- making payments

- processing credit loans, etc.

Each financial entity is displayed in accounting as a double entry, since it has a parallel impact on the asset and liability of the balance sheet. The correspondence of accounts represents the dependence of debit and credit. Dt shows the volume of the enterprise’s property, and Kt shows the sources of its formation. The creation of the necessary postings is carried out during the conduct of operations.

Each account has its own number. The double entry method ensures that changes in debit and credit are equivalent and helps determine the nature of the posting. If different values of assets and liabilities are revealed, then there is an error in accounting.

What are business transactions?

A business operation (HO) is a specific action that changes either the composition of property, or its location, or the sources of its formation. POs may also be associated with changes in budget formation, the company’s ownership structure, equity and borrowed funds, and reserve capital. The fact of a business transaction is the basis for creating an accounting entry. The posting is generated on the basis of documents confirming the operation.

A certain event entails a change in indicators. For example, capital and the volume of property may change. Values can either increase or decrease. Changes in capital cause changes in the balance sheet currency. Consequently, the amount of assets and liabilities also changes.

Examples of business transactions in accounting

Let's look at examples of operations and their approximate structure:

- Supply.

Examples of business operations: receipt of raw materials, transfer of funds to the supplier, input of raw materials into production. - Implementation.

Examples of financial expenses: expenses for sales of products, receipt of revenue, sale of goods. - Production.

Examples of financial assets: payment of salaries to employees, depreciation of fixed assets, acceptance of the work of a contractor, transfer of funds to a contractor.

These are the most common types of business transactions.

Types of business transactions

Let's look at the table with the classification of business transactions:

| Impact on balance | Debit correspondence | Loan correspondence |

| Change in Assets | Active | Active |

| Changing Liabilities | Passive | Passive |

| Increasing assets and liabilities | Active | Passive |

| Decrease in assets and liabilities | Passive | Active |

These are four types of transactions, which are classified according to the way they affect the balance sheet.

Let's take a closer look at the types of transactions (A is an asset, P is a liability, O is turnover):

- 1 type

Entries that reduce one asset item by increasing another. Examples of type 1: goods have arrived at the warehouse, money is sent from the account to the cash register. In this case, the structure of the property changes, but the final amount remains the same.This type has the following formula: A balance + O on the debit of account 1 – O on the credit of account 2 = P balance.

- Type 2

Postings changing liability items. Examples of type 2: multiplying reserve capital by changing the amount of profit. In this case, the chemical enterprise causes a change in the structure of sources of funds, but the final assessment remains the same.This formula belongs to this type: A balance = P balance + O for the credit of account 1 – O for the debit of account 2.

- Type 3

Actions that increase the value of a company's assets and liabilities. Example: operations for the sale of fixed assets, obtaining a loan. Postings change the balance sheet currencies.Formula: A balance + O on the debit of account 1 = P balance + O on the credit of account 2.

- Type 4

Actions that reduce the value of liabilities or the amount of equity capital by reducing the amount of assets. Example: payments to suppliers. In the process, both assets and liabilities are reduced.Formula: A balance – O on the debit of account 1 = P balance – O on the credit of account 2.

Operations are also classified according to their content:

- Material.

Movement of inventory items is expected. - Financial.

Assume the movement of funds. - Calculated.

Settlements with counterparties.

The type of transaction determines the features of its reflection in accounting.

Main stages of the organization's work

In the course of the enterprise’s activities, 3 processes can be distinguished, which are taken into account by separate operations: (click to expand)

- Supply - takes into account the receipt of goods and materials from third-party companies, repayment of transport and procurement costs.

- Production - inventory items are released into production, wages and taxes are calculated.

- Sales - the revenue received from the sale of goods (provision of services) to counterparties is recorded, the corresponding costs are written off, and profit is determined.

The organization's assets are constantly involved in the production process. To determine their value and economic analysis for a specific date, the accountant draws up a balance sheet. It includes a system of parameters that qualify the financial status of the company, the condition and size of its assets and sources in the same monetary equivalent.

Examples of household items operations

Here are some examples of business transactions in accounting:

- First type:

- D43 – K20 – release of finished goods from production.

- D94 – K10 – a shortage of valuables was identified during the inventory.

- Second type:

- D80 – K84 – the size of the capital decreased to the size of the company’s net assets.

- D96 – K70 – accrual of vacation pay from the reserve.

- Third type:

- D76 - K91 - charging a fine for violating the conditions specified in the contract.

- D08 – K70 – calculation of wages for workers installing an OS facility.

- Fourth type:

- D91 – K52 – negative difference in exchange rates for a foreign account. currency.

- D91 – K63 – formation of a reserve for doubtful debts.

The order and nuances of their reflection

In accordance with the principle of double entry, accounting transactions cannot violate the identity of the amount of assets and liabilities. That is, any transaction can either change the total value of both sides of the balance sheet, or move funds within one of the sections.

The effects that transactions have on the balance sheet are of two types:

- modification

, that is, an increase or decrease in the balance sheet currency, while the posting involves both an asset and a liability; - permutation

, that is, the absence of changes in the balance, while the operation is carried out within one of its sides.

Reducing modification

This type is characterized by a simultaneous decrease in assets and liabilities

. The cost of property and its sources decreases, but the balance sheet currency remains unchanged.

Most often, this type includes transactions related to the repayment of previously incurred obligations, for example, payment of loans or debts to suppliers.

The interaction between asset and liability can be represented here as a formula:

A - I = P - I

, Where

- A – asset;

- P – passive;

- And – change in debit and credit accounts.

This type includes wiring similar to the following:

The essence of these operations is that the organization, in paying off its obligations, spends its own funds. For example, when paying debts to suppliers, the amount stored in the current account decreases, but at the same time the total amount of liabilities decreases.

Modification increasing

A feature of this type is the increase in items simultaneously in the assets and liabilities

of the balance sheet. At the same time, the equality of the currency is maintained, and the total value of property and liabilities increases.

Postings of this type are most often associated with the acquisition of materials, fixed assets, calculation of wages and similar actions.

The interaction formula is as follows: A + I = P + I

. This type includes the postings presented in the following table:

The essence of these operations is that the organization, by acquiring property, simultaneously increases the volume of its obligations. That is, for example, when purchasing materials, the debit balance of account 10 increases, as well as the balance on the credit side of account 60.

Permutation active

Transactions of this type affect only one side of the balance sheet

. This type includes transactions that reduce a certain item of an asset while simultaneously increasing the value of another line. At the same time, the total value of all property ultimately remains unchanged.

Transactions here most often involve invoices or receivables. The interaction formula looks like this:

A + D – K = P

, Where

- D – change in debit;

- K – change on loan.

This type includes wiring similar to those presented:

| Operation | Debit | Change | Credit | Change |

| Money has arrived at the cash register from the current account | 50 | + | 51 | – |

| Payment received from debtors | 51 | + | 62 | – |

| Return of unspent accountable amounts | 50 | + | 71 | – |

| Materials released into production | 20 | + | 10 | – |

| Finished products have arrived at the warehouse | 43 | + | 20 | – |

| Finished products were shipped to the buyer | 45 | + | 43 | – |

Their essence is that when carrying out certain operations, one type of property is replaced by another. For example, when paying receivables, the amount in the current account increases and at the same time the amount of obligations of the counterparty company decreases.

Permutation passive

This type is characterized by the fact that during operations, some liability item increases and another decreases

. In this case, the source of property formation arises from one of the existing ones. These include entries recorded in connection with the withholding of taxes from employee salaries and redirection of profits.

The interaction of asset and liability can be expressed by the formula: A = P + D – K

.

Signs of passive permutation have the following wiring:

The essence of the operations is that when one of the sources of property formation decreases, the other increases.

Types of business transactions by impact on the balance sheet.

The balance is drawn up on a certain date - the 1st day of the month, quarter, year, and this is like a momentary reflection of the funds. But already on the first day of the new month, the balance of funds in the balance sheet changes significantly under the influence of business transactions (receipt of funds, their release into production, receipt of finished products, their sale, settlements with other organizations, etc.).

There are a lot of business transactions carried out during the day and month, and all of them change the balance of funds or their sources.

Based on the nature of these changes, business operations can be divided into four types:

To the first type of operations

These include those that result in the movement of only funds available in the organization (balance sheet assets). In this case, some funds increase and others decrease by the same amount. The amount of one item of an asset increases, and the amount of another item decreases. In this case, the balance sheet does not change (A+; A-).

For example, cash was received from the current account by check to the organization’s cash desk in the amount of 20 million rubles. In this case, the funds in the current account decrease (-), and in the cash register they increase (+) by the same amount.

To the second type of operations

These include those that result in the movement of sources of formation of economic assets (equity capital and balance sheet liabilities). In this case, there is a decrease in one balance sheet item and an increase in another by the same amount. The balance sheet will not change (P+; P-).

For example, bank loans for 100 million rubles were received. and are aimed at repaying debts to suppliers. There will be an increase in debt on bank loans (+) and at the same time a decrease in debt to suppliers (-).

To the third type of operations

include those that result in an increase in economic assets. Since the increase occurs due to certain sources, business transactions of this type cause an increase in the total amount of assets and equity and liabilities of the balance sheet, i.e. the amount under the asset item increases and the amount under the equity and liabilities item increases. The balance sheet also increases (A+; P+).

For example, materials were received from a supplier for 3,000 rubles. and these materials have not yet been paid for. For this operation, there is an increase in materials (+) in the balance sheet asset, and an increase in debt to suppliers (+) in equity and balance sheet liabilities.

To the fourth type of operations

These include those that result in a downward change in the balance sheet total, that is, the amount under the asset item decreases, and the amount under the equity and liabilities item also decreases (A-; P-).

For example, wages to workers and employees of 1 million rubles were issued from the cash register. Here there will be a decrease in funds in the cash register (-) in the balance sheet asset, and a decrease in the debt to personnel for wages (-) in equity and balance sheet liabilities.

The first and second types of business transactions do not change the total of assets and equity and liabilities of the balance sheet, but the third and fourth lead to an increase or decrease in the totals of assets and equity and liabilities of the balance sheet by the same amount.

However, no matter what the business transactions are, and no matter what changes they cause in the balance sheet, the equality between the asset and equity capital and liabilities always remains. Such constant preservation of equality as a result of comparison of the organization’s funds (property) with the sources of their (its) formation is the main content of the balance sheet generalization

.

These formulas are of great importance not only for reflecting the influence of various types of business transactions on the balance sheet, but also for the organization of accounting and analysis of the financial and economic activities of the organization, assessment of its financial and property status in the conditions of using various computer equipment.

9. Purpose and structure of accounting accounts.

An accounting account is the main unit of information storage, which, after summarizing all accounting information, is necessary for making management decisions. decisions.

Accounting accounts are a method of current interconnected reflection and grouping of property by composition and location, according to the sources of its formation.

Each account is a two-sided table: the left side of the account is debit (“should”), the right side is credit (“believe”). For some accounts, a debit means an increase, a credit means a decrease, and for others, on the contrary, a debit means a decrease, and a credit means an increase. Depending on the contents of accounting accounts, they are divided into active, passive and act-pass.

Accounts are active by:

· economic content – these are those accounts that are intended to account for property by availability, composition and location;

· balance sheet – when accounts (items) are located in the active part of the balance sheet;

· balance (remaining) – if accounts have a debit balance.

Accounts are considered passive by:

· economic content – when accounts reflect the accounting of property by sources of its formation;

· balance sheet – if accounts (items) are located in the passive part of the balance sheet;

· balances are those accounts that have a credit balance.

In addition to active and passive accounts, in accounting practice, active-passive accounts are used, which can have a debit or credit balance at the same time.

The structure of active and passive accounts and the procedure for recording transactions in them are regulated by the following rules:

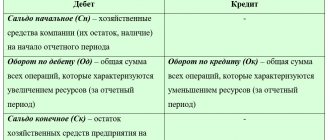

1) for active accounts. At the beginning of the reporting period, accounts are opened on which there are balances (initial debit balance - SND). Data to be recorded on accounts is taken from the active part of the balance sheet and recorded on the debit side of the accounts. This procedure means: open accounts and record the initial balance. Increases and receipts are reflected on the debit side, and decreases, expenses and disposals are reflected on the credit side of the accounts. At the end of the reporting period, the turnover for all accounts is summed up: first by debit, and then by credit. The amount of the initial balance is not included in the totals of turnover on debit accounts; This includes only amounts for transactions in the reporting period. The final debit balance (SCD) for active accounts for the reporting period is determined as follows: the totals of debit turnovers are added to the initial debit balance (Snd) and the totals of credit turnovers are subtracted (OK). The final balance can be either debit or equal to zero: Skd = Snd + Od + Ok .

Thus, for active accounts, a debit means an increase, and a credit means a decrease;

2) for passive accounts, accounts are opened in which the initial balance of the loan is recorded. It is taken from the passive part of the balance sheet in the context of items for which there are balances. Increases, receipts and receipts are reflected as a credit, and decreases, expenses and disposals are reflected as a debit. At the end of the reporting period, the turnover is summed up for each account, first by credit and then by debit. The results of loan turnover do not include the initial balance, but only the amounts of transactions that arise during the reporting period. The ending balance (Skp) is determined as follows: the credit turnover (Ok) is added to the initial balance (Snk) and the debit turnover (Od) is subtracted. The final balance can be either a credit balance or equal to zero: Skp = Snk + Ok - Od .

Therefore, for passive accounts, a debit means a decrease and a credit means an increase.

Double entry.

Each household the transaction causes a change in the balance sheet for two items. Balance sheet items to account for changes are replaced by corresponding accounts, so each business transaction must be reflected in two accounts. Such simultaneous recording of transactions on the debit of one account and the credit of another in the same amount is called double entry.

Double entry is an entry as a result of which each business transaction is reflected in the accounting accounts twice: in the debit of one account and at the same time in the credit of another account associated with it for the same amount.

The double entry method determines the existence of such concepts as correspondence of accounts and accounting. wiring. Correspondence of accounts is a connection that has arisen between accounts as a result of double entries on them, for example, between accounts 50 “Cash” and 51 “Cash Accounts”, or 70 “Settlements with personnel for wages” and 50 “Cash” (D-t. 50 "Cashier" - Set account 51 "Cash accounts" - 10 rubles; D-t account 70 "Settlements with personnel for wages" - Set account 50 "Cash desk" - 10 rubles). Indicating two corresponding accounts and the amount of a business transaction is called an accounting entry. Accounting entries can be simple or complex. A simple one is an accounting entry that involves two accounts: one for debit, the other for credit. An accounting entry in which one debit account corresponds with several credit accounts or one credit account with several debit accounts is called complex.

An example of a simple transaction - cash from the cash register is deposited into a current account, the amount is 9 rubles. This operation will be reflected by a simple posting to two accounts: “Current account in the bank” and “Cash”: D-t “Current account” 9 rub. – K-t “Cash desk” 9 rubles.

An example of a complex transaction - 8.5 rubles were transferred from the current account, including a tax of 2.5 rubles. and the money was transferred to the supplier 6 rubles. -D-t “Calculations for taxes and fees” 2.5 rubles. –D-t “Settlements with suppliers and contractors” 6 rubles. – Settlement “Current account” 8.5 rubles.

In addition to the cost amount, the posting may contain data on the natural volumes of material assets, currency value, and others.

The procedure for recording transactions using the double entry method:

– an operation of the first type is reflected in the debit and credit of the active account;

– the operation of the second type is reflected in the debit and credit of the passive account;

– an operation of the third type is reflected in the debit of the active account and the credit of the passive account;

– a fourth type transaction is reflected in the debit of the passive account and the credit of the active account.

Using double entry, one account is debited and the other account is credited with the same amount. If the posting of transactions across accounts is done correctly, then the sum of the debit turnovers of all accounts and the sum of the credit turnovers of all accounts will be equal. If the amount on the corresponding account is mistakenly changed or the entry is made on the same side of the corresponding accounts (the balance is transferred incorrectly), then the identified inequality of debit and credit turnover on the accounts means an error in the amount or in the nature of the recorded transaction.

Double entry has educational value, as it shows where the funds came from and where they are going. Entries in accounts are made on the basis of documents, therefore all accounting documents are subject to accounting processing, one of the stages of which is the recording of corresponding accounts for each transaction reflected in the document. The use of double entry ensures constant self-monitoring of the correctness of the amount posted to the accounts and the legality (economic content) of the transaction performed.

Previous3Next

Didn't find what you were looking for? Use Google search on the site:

Main tasks of accounting

The main task of accounting is the generation of complete and reliable information (accounting statements) about the activities of the organization and its property status, necessary for internal users of financial statements - managers, founders, participants and owners of the organization’s property, as well as external users - investors, creditors and other users of financial statements , on the basis of which it becomes possible:

prevention of negative results of the organization’s economic activities;

identification of internal reserves to ensure the financial stability of the organization;

monitoring compliance with legislation when the organization carries out business operations;

control of the feasibility of business operations;

control of the availability and movement of property and liabilities;

control over the use of material, labor and financial resources;

monitoring compliance of activities with approved norms, standards and estimates.

Registration of a business transaction

To record chemical weapons at enterprises of all forms of ownership and with any production volumes, special journals are used. They record every transaction carried out by the company. The following data must be recorded in the log:

- XO number

- the moment of its implementation

- information from primary documentation about chemical equipment

- operation description

- posting in accounting

- its monetary value

Some aspects of registration in different organizations may differ, but the basic principle remains the same:

- Each subsequent registration of a chemical enterprise is carried out from a new line

- the transaction number in order, the date of its completion and description are indicated

- the numbers of the corresponding accounts and the transaction amount are displayed

- the number of the identification document is indicated

Primary documentation for recording

With the help of this documentation, you can certify the fact of the accomplishment of the chemical act and ensure the reliability of your employees. Some types of primary documents are unified, others are created by payers personally.

Primary documentation, reflecting the implementation of the economic organization and being the basis for creating accounting entries, can be generated both by the accounting service and by management, middle managers, and so on. These documents must contain certain information:

- Name

- signatures of officials

- information about the responsible employee

- deal name

- information about business entities involved in the transaction

- information about the entity of the enterprise

- date of registration of documentation

Thus, all financial entities in accounting must be accompanied by postings, which are the basis for reporting. The latter, in turn, allows you to analyze the financial results of the company. In addition, it contributes to the development of correct management decisions.

Write your question in the form below

Features of reflection

The completed business transaction is documented on paper or electronic media. Through these documents, the initial registration of events is carried out. Registration is carried out in the sequence in which the operations were performed. This order allows:

- Maintain continuous, comprehensive records of objects.

- Justify entries made in accordance with documents that have evidentiary value.

- Use reporting for operational management and ongoing monitoring of the enterprise’s activities.

In addition, compliance with financial discipline at the enterprise is ensured, since primary documentation acts as the main source of information for further supervision over the appropriateness, correctness, and legality of each operation.

How to set the operation type

To determine the type of transaction, you need to analyze which accounts were used in the transactions and what changes in the balance sheet currency were made. The following information will help make the determination easier (A – active, P – passive):

- Active XO. Correspondence: both accounts A. Dt increases, and Kt decreases. The balance does not change.

- Passive XO. Correspondence: both accounts P. Dt decreases, Kt increases. The balance does not change.

- Mixed XO for an increase. Correspondence: Dt - A, Kt - P. Dt and Kt increase. The balance increases.

- Mixed XO for reduction. Correspondence: Dt - P, Kt - A. Dt and Kt indicators are decreasing. The balance will be reduced.

To accurately establish the type of transaction, you need to have information about the chart of accounts and balance sheet structure.

FOR YOUR INFORMATION! An asset is the company's property, and a liability is the sources of this property. There are mixed forms in both assets and liabilities.

How to determine the type of operation?

To understand which of the four types discussed above a transaction belongs to, you need to determine which accounts are involved in the posting and what happens to the balance sheet currency.

| Type of transaction | Corresponding accounts | Changes in Debit and Credit values | Balance sheet |

| Active | Both active | Dt increases, Kt decreases | Doesn't change |

| Passive | Both are passive | Dt decreases, Kt increases | |

| Mixed to increase | Dt - active, Kt - passive | Dt and Kt increase | Increases |

| Mixed on decline | Dt - passive, Kt - active | Dt and Kt decrease | Decreases |

To have a good understanding of the types of accounts, you need to know their layout and balance sheet design. An asset refers to the company's property, and a liability refers to sources. There are mixed type accounts that can be present in both the assets of the balance sheet and the liabilities. It depends on the state of the settlements. These include: 40, 60, 62, 68, 69, 71, 73, 75, 76, 79, 84, 90, 91, 99.

Recognizing types of operations

The accounting system distinguishes 4 types of financial assets, characterized by their impact on assets and liabilities:

- A – balance sheet asset

- P – balance sheet liability

- Od – debit turnover

- Ok – loan turnover

- sch. - check

Type 1 is represented by transactions reflecting a decrease in a balance sheet asset (one item is reduced due to transformations of another). For example, if goods are delivered to the warehouse, money is transferred to the cash register from the current account. These operations are characterized by transforming the structure of property objects and maintaining balance:

Type 2 is characterized by postings relating to the liability. For example, the profit received was used to increase reserve capital. The result of financial accounting in accounting will be an adjustment to the sources of financing and obligations of the company, that is, the final indicators will remain unchanged:

Type 3 of entries reflects a parallel increase in liabilities and the value of property, which is due to changes in the final indicators. An example is the acquisition of fixed assets and the issuance of a loan:

Type 4 is represented by enterprises that contribute to a decrease in total indicators due to entries reflecting a decrease in the equity capital or liabilities of the enterprise due to a decrease in the share of assets:

CWs can also be classified according to their essence. According to this criterion, there are 3 types of them:

- transactions with funds (cash)

- movement of inventory items (material)

- settlement transactions with counterparties (settlement)

Primary accounting documentation is classified using the same method.

Video about business transactions in accounting:

The second type of business transactions “Changes exclusively in the liabilities side of the balance sheet”

Also, an organization may have typical business transactions that affect the structure of only the passive part of the balance sheet. For example, an organization as of March 1, 2021 has balances that are reflected in the balance sheet asset:

- retained earnings RUB 2,589,741.

- reserve capital 896,500 rub.

On March 2, 2021, the organization experienced an increase in reserve capital due to part of the enterprise’s retained earnings in the amount of RUB 550,100. Thus, the line “Retained earnings” is reduced by the amount of deductions, and the line where “Reserve capital” is increased by the same amount:

- retained earnings 2589741 – 550100 = 2039641 rub.

- reserve capital 896500 +550100 = 1446600 rub.

Too lazy to read?

Ask a question to the experts and get an answer within 15 minutes!

Ask a Question

Similar changes occur in other business transactions that affect only the structure of the balance sheet liability.

Double entry

The formation of an information connection between synthetic accounts that arises in the process of registering the facts of a company’s economic activity is called correspondence in the nomenclature of the plan. It is worth saying that it also reflects the legal relations between the subjects. Correspondence may be systematic or chronological. Facts of economic activity are reflected in accounts using the principle (rule) of double entry. Its essence is that any event is registered twice. Information is reflected in the debit and credit of the account. This record has a control value.

The total of debit turnover on synthetic accounts for a month should be equal to the amount of credit. If the values do not match, it means that an error was made when reflecting events. In accordance with the principle of double entry, the information connection that arises between accounting objects can be shown in different ways. For example, the formula image reflects the name of the corresponding accounts. In this case, the numerical value of the record is indicated. Reflection of corresponding accounts in primary documentation is called account assignment.

Documentary evidence of records

Entries in accounts are made according to documents, so all papers received by the accountant are subject to processing. Documents are established for homogeneous groups of operations. For each action, they create correspondence accounts. The text indicating the correspondence and amount is called a posting. It is compiled directly on the document, in a statement, or in a special journal.

To facilitate data entry, each account is assigned a number. The control function of double entry of information is to check the equality of debit and credit turnover for the period. Inequality indicates the presence of an error in the wiring. The cognitive function of double registration is that it is easy to formulate the content of the operation using correspondent accounts.

Example 3. Formulation of the contents of correspondent accounts

The entry is given: Dt 69 Kt 51 in the amount of 15,300 rubles.

Explanation:

Dt sch. 69 - passive, a decrease in the sources of the company’s funds is recorded;

Kt sch. 51 - active, the cost of funds is decreasing.

The values in these accounts decrease, which means that the operation belongs to the fourth type.

The content of the posting will be as follows: “reflects the transfer of funds to extra-budgetary funds in the amount of 15,300 rubles.”

A business transaction in accounting is...

The current accounting legislation does not contain a definition of a business transaction. At the same time, the Federal Law of December 6, 2011 No. 402-FZ “On Accounting” gives the concept of a fact of economic life.

A fact of economic life is understood as a transaction, event, operation that has or is capable of influencing the financial position of the organization, the financial result of its activities or cash flow (clause 8 of Article 3 of the Federal Law of December 6, 2011 No. 402-FZ). In essence, a business transaction is a fact of economic life and is the same object of accounting.

At the same time, business processes and business operations are also closely related to each other, because business processes in accounting are a set of business transactions.

Main types of operations

There are four types of business transactions:

- Operations of the first type affect the composition of property assets, that is, only the balance sheet asset. No changes are made to obligations.

- When carrying out operations of the second type, the sources from which the company's property is formed change. This means that only the passive part changes. This does not apply to balance sheet currency.

- Operations of the third type affect both the company's property and capital. Changes are being made in a big way. Both in terms of liabilities and assets, the balance sheet currency is growing.

- When carrying out operations of the fourth type, both the active and passive parts of the balance sheet are reduced (and by an equal amount).

The importance of balance

It is important to comply with all of the above requirements when drawing up a balance sheet. It clearly reflects the financial condition of the organization, shows who invested the funds, how they were allocated and how the loans were secured

By analyzing the balance sheet over several periods, you can imagine the dynamics of the organization’s development and determine whether resources are being used rationally. The presence of a correctly compiled report allows the manager to think about all the consequences of the organization’s activities, consciously manage the economy, and search for internal reserves.

As a reporting document, the balance sheet contains important information. The organization reports to them to governing bodies, tax administration, statistics, and credit institutions. Based on the information in the balance sheet and other reporting forms, the net profit indicator is calculated, the amount of taxes, mandatory contributions and payments is established.

The balance sheet in scientific research is a summary of accurate, systematized data on the property status, economic activity, statics and dynamics of individual farms. Without a comprehensive study and careful study of such reports, it is impossible to practically work out effective ways to develop and boost the economy of the country in general and a specific organization in particular.

Definition of business transactions

In addition, economic entities participate in the formation of the company’s own, reserve and borrowed capital, and influence the company’s budget. Any enterprise must be registered in the accounting department with the appropriate posting. Justification will require documentation proving its necessity.

Economic change entails the transformation of some parameters, for example, the size of property and capital may change upward or downward. Equity conversions ultimately result in asset and liability adjustments.

A business operation (HO) means a specific act that led to transformation:

- the composition of the organization’s property or the procedure for its placement;

- sources that form the property mass of a business entity;

- company budget;

- fixed and reserve funds;

- ownership structures.

Figure 1. Balance sheet items

Determining the type of economic manipulation includes several sequential steps. The initial stage involves the collection and verification of primary documents.

Each event in the financial and economic activity of a company has a dual nature. This feature is manifested in the fact that any enterprise is displayed in 2 accounting positions.

Figure 7. Double entry in accounting

To establish the type to which this or that fact of the economic life of an organization belongs, it is necessary to analyze:

- what accounts are reflected in the accounting entries;

- how the balance sheet currency has changed.

| Group | Debit | Credit | Balance |

| I | rises | is decreasing | without changes |

| II | is decreasing | rises | without changes |

| III | rises | rises | increases |

| IV | is decreasing | is decreasing | decreases |

What are they, their types

A business transaction is a fact that reflects information about calculations made, changes in the composition of property, its own and borrowed sources of education. It should be considered as an event that serves as the basis for drawing up accounting entries.

A prerequisite for recognition of the fact of the commission of an action is the presence of all necessary supporting documents.

Any operation performed by an enterprise changes one or both indicators simultaneously:

- size of property;

- composition and volume of sources of its formation.

Values can either decrease or increase. These movements directly affect the balance sheet currency, that is, the total identical amount of assets and liabilities.

Depending on how exactly property and sources interact with each other, there are 4 types of operations:

- permutation active;

- permutation is passive;

- increasing modification;

- reduction modification.

Classification into one of these types depends on how this action affects the composition of the assets and liabilities of the balance sheet.

Instructions for generating these operations are presented in the following video:

Features of registration of postings

Recording of events in the financial and economic sphere with the help of corresponding accounts is carried out in the form of accounting entries. Manipulations affect the assets and liabilities of the enterprise. The debit value demonstrates the existing property mass of the business entity, and the credit indicator shows the sources of ownership.

Figure 8. Features of accounting records

As examples, consider the following wiring:

- As a result of the transaction for the shipment of goods, an amount of 7,600 rubles was received into the account of Radif OJSC. This operation is reflected by the posting: Dt 51-Kt 62, the amount of XO is 7,600 rubles. The final balance sheet indicators will remain unchanged, while the value of the current account will increase by 7,600 rubles, and the “Settlements with customers” account will decrease by the same amount.

- Raw materials worth 3,800 rubles were shipped to warehouse storage at Radif OJSC. This operation caused an adjustment to the balance sheet totals with the following posting: Dt 41-Kt 60, amount - 3,800 rubles.

- If, based on the results of production activities, the company made a profit and management needs to determine interest in the amount of 15,600 rubles, then the financial statement will be recorded by posting: Dt 84-Kt 75, amount 15,600 rubles. The changes will affect the liability, but the total values will remain the same.

- OJSC Radif paid the supplier for raw materials, the transaction amount was 5,400 rubles. A posting is created: Dt 60-Kt 51, amount 5,400 rubles.

A ΔИ – ΔИ = П, where

A - balance sheet asset;

P - passive;

ΔИ - change in property due to economic action.

Passive operations affect the sources of formation of assets, i.e., the liability side of the balance sheet. The result is constant. Such operations include: deductions from earnings, the formation of reserves or the accrual of dividends from profits for distribution, replenishment of the authorized capital from additional funds, etc.

A = P ΔI – ΔI.

Active-passive increasing - increase the asset, liability and currency by an identical amount. These include: repayment of debt on deposits in the authorized capital, accrual of depreciation of fixed assets, advances from buyers, receipt of borrowed funds, etc.

A ΔI = P ΔI.

Active-passive decreasing - reduce the asset, liability and balance sheet total by the same amount. This is the payment of earnings, payment of debts to creditors.

Based on bills and bank statements, 214 thousand rubles were transferred to the supplier. for the materials received. The result of the operation will be a change in two items: the asset account will decrease. 51 by 214 thousand rubles, in liabilities the account will decrease. 62 for 214 thousand rubles. The asset and liability totals changed by an equal amount. The balance identity is preserved.

Consideration of four types of business transactions led to the following conclusions:

- Each fact of activity is reflected in at least two balance sheet items;

- Changes to the asset (types 1, 2) do not change the currency of the document;

- Changes in assets and liabilities (types 3, 4) change the currency by the same amount;

- Any operations maintain equality of balance sheet totals.

Table. Examples of postings by type of operation.

| Debit | deviation | Credit | deviation | |

| Type 1. | ||||

| Raw materials transferred to production | 20 | 10 | — | |

| Payment received from buyer | 51 | 60 | — | |

| Received money in cash | 50 | 51 | — | |

| Type 2. | ||||

| Personal income tax withheld from salary | 70 | — | 68 | |

| The reserve is replenished from profits to be distributed | 84 | — | 82 | |

| Advance paid to supplier using borrowed funds | 60 | — | 66 | |

| Type 3. | ||||

| Received materials from supplier | 10 | 60 | ||

| Salary accrued | 20 | 70 | ||

| The loan amount has been credited to the account | 51 | 66 | ||

| Type 4. | ||||

| Loan repaid | 66 | — | 51 | — |

| Employees' salaries transferred | 70 | — | 51 | — |

| Payment has been made to the supplier for the goods | 51 | — | 60 | — |

Transactions are reflected on accounts at the time of their occurrence, i.e., as they are completed. Double entry reveals the opposite nature of the asset and liability accounts, linking them to the form of the balance sheet. On the left they reflect the balances of the property (debit), on the right - the sources of its appearance (credit).

Contents of the operation: materials worth 85 thousand rubles were received from the supplier.

The changes affected two accounts: account. 10 — balances of inventory items and invoices increased. 60 - the debt to the supplier has increased.

Account 10 - active, takes into account assets, growth is put in Dt;

Account 60 - passive, height - according to Kt.

Features of reflecting accounting entries

Each production action must be documented. Changes arising from the operation are of a dual nature and occur in two interrelated accounting objects. A characteristic feature of the operation is that it is shown on the accounts twice: in debit and credit. This relationship represents the correspondence of accounts.

Transactions are reflected on accounts at the time of their occurrence, i.e., as they are completed. Double entry reveals the opposite nature of the asset and liability accounts, linking them to the form of the balance sheet. On the left they reflect the balances of the property (debit), on the right - the sources of its appearance (credit).

Correspondent accounts and balance form a single system, connected by double entry, which is based on three principles: (click to expand)

- Duality of reflection;

- Fixation of amounts for Dt and Ct accounts;

- In both accounts, changes are shown in the same amount.

For control, the registration of the action in accounting is repeated twice. First of all, it is reflected as a fait accompli confirmed by documents, then - by the distribution of amounts among correspondent accounts.

Example 2. Posting

Contents of the operation: materials worth 85 thousand rubles were received from the supplier.

Reasoning:

The changes affected two accounts: account. 10 — balances of inventory items and invoices increased. 60 - the debt to the supplier has increased.

Account 10 - active, takes into account assets, growth is put in Dt;

Account 60 - passive, height - according to Kt.

The increase in assets and liabilities corresponds to operations of the third type. The posting is written as follows: Dt 10 Kt 60.

Business transactions in accounting: examples

Let us consider, as an example, the list of business operations of an enterprise engaged in the assembly and sale of wristwatches. In April, a batch of goods was assembled: the cost of components was 284,000 rubles, wages for assemblers were 110,000 rubles. The product was sold for RUB 655,018. (including VAT RUB 99,918).

Correspondence of accounts and content of business transactions: table

| № | Contents of a business transaction | Sum | D-t | Kit |

| 1. | Components are written off for production | 284 000 | 20 | 10 |

| 2. | Payments to production employees were accrued | 110 000 | 20 | 70 |

| 3. | Insurance premiums accrued | 33 220 | 20 | 69 (according to subaccounts) |

| 4. | The cost of a batch of watches has been formed | 427 220 | 43 | 20 |

| 5. | Personal income tax withheld from salary | 14 300 | 70 | 68-1 “NDFL” |

| 6. | Transferred to the personal income tax budget | 14 300 | 68-1 “NDFL” | 51 |

| 7. | Insurance premiums transferred to the budget | 33 220 | 69 (according to subaccounts) | 51 |

| 8. | Salaries issued from the cash register | 95 700 | 70 | 50 |

| 9. | A batch of goods has been sold | 655 018 | 62 | 90-1 “Revenue” |

| 10. | The cost of the sold batch was written off | 427 220 | 90-2 “Cost” | 43 |

| 11. | VAT charged | 99 918 | 90-3 "VAT" | 68-2 "VAT" |

Samples of postings for business transactions

As examples, consider the following wiring:

- As a result of the transaction for the shipment of goods, an amount of 7,600 rubles was received into the account of Radif OJSC. This operation is reflected by the posting: Dt 51-Kt 62, the amount of XO is 7,600 rubles. The final balance sheet indicators will remain unchanged, while the value of the current account will increase by 7,600 rubles, and the “Settlements with customers” account will decrease by the same amount.

- Raw materials worth 3,800 rubles were shipped to warehouse storage at Radif OJSC. This operation caused an adjustment to the balance sheet totals with the following posting: Dt 41-Kt 60, amount - 3,800 rubles.

- If, based on the results of production activities, the company made a profit and management needs to determine interest in the amount of 15,600 rubles, then the financial statement will be recorded by posting: Dt 84-Kt 75, amount 15,600 rubles. The changes will affect the liability, but the total values will remain the same.

- OJSC Radif paid the supplier for raw materials, the transaction amount was 5,400 rubles. A posting is created: Dt 60-Kt 51, amount 5,400 rubles.

The first type of business transactions “Changes exclusively in the balance sheet asset”

There are standard business transactions that affect the structure of only the active part of the balance sheet. For example, an organization as of March 1, 2021 has balances that are reflected in the balance sheet asset:

- reserves 158,200 rub.

- work in progress RUB 236,844.

On March 2, 2021, materials worth RUB 125,100 were released into production. Thus, the line “Inventories” is reduced by the amount of materials released into production, and the line where work in progress is reflected is increased by the same amount:

Too lazy to read?

Ask a question to the experts and get an answer within 15 minutes!

Ask a Question

- inventories 158200 - 125100 = 33100 rub.

- work in progress 236844+125100 = 261944 rubles.

Note 1

Similar changes occur in other business transactions that affect only the structure of the balance sheet asset.

Basic balance postings

Postings for some business activities are presented in the table.

| Debit | Credit | |

| Wage | ||

| 20 (25) | 70 | Salaries accrued to the main workers (administration) |

| 70 | 68 | Personal income tax withheld from employees' earnings |

| 76 | Child support withheld from salary | |

| 50, 51 | Salary paid | |

| 20 (25) | 69 | Contributions to extra-budgetary funds accrued |

| 68, (69) | 51 | Personal income tax (insurance contributions) transferred |

| Cash desk and bank | ||

| 50 | 51, (52) | Money has been received from the account to the cashier |

| 62 | Advance received from buyer | |

| 70 | Refund of excess amounts paid for salaries | |

| 71 | Return of the balance of accountable money | |

| 75 | Contribution to the authorized capital has been received | |

| 70 | 50 | Salary paid |

| 71 | Money was issued for reporting | |

| 94 | The lack of money in the cash register has been taken into account | |

| 73 | A loan was issued to an employee | |

| 51 | Proceeds handed over to the bank | |

| 51 | 62, (76) | Paid for goods by buyer (debtor) |

| 66, 67 | Loan received | |

| 75 | 51 | Dividends paid |

| 60 | Money was transferred to the supplier for the goods | |

| 66, 67 | Loan interest paid off | |

| 81 | Shares purchased | |

| 91.2 | Payment to the bank for cash management services | |

| Fixed assets (FPE) and intangible assets (IMA) | ||

| 08 | 60, 71, 75, 76 | Received OS (intangible assets) |

| 01, (04) | 08 | Assets were accepted for accounting (intangible assets were put into operation) |

| 20, 23, 25, 26, 44 | 02, (05) | Accrued depreciation on fixed assets (intangible assets) |

| Inventories | ||

| 10, (11) | 60, 75, 76 | Received MPZ (animals) |

| 20, 23, 29 | Production waste has arrived | |

| 20, 23, 25, 26, 44 | 10 | MPZ written off |

| 90, 91 | MPZ sold | |

| 08 | 11 | Young cattle were transferred to the main herd |

| 20, 23, 29 | Costs of slaughtering animals are taken into account | |

| Expenses | ||

| 20 | 23, 25, 26, (28) | The costs of other production (losses from defects) are distributed among the main products |

| 21 | Own semi-finished products were released into production for processing | |

| 20, 23, 25, 26, 44 | 60, 76 | Works (services) of third-party organizations are reflected |

| 68, 69, 70 | Taxes and salaries accrued | |

| 21 | 20 | Semi-finished products (own) are taken into account |

| 90 | 44 | Sales expenses are written off to the cost of products sold |

| Calculations | ||

| 62 | 90 | Products sold |

| 20, 25, 44 | 66, 67 | Interest accrued on the loan |

| 10, 20, 41 | 71 | Accountable amount spent |

| 73 | 94 | The shortage is attributed to the culprit |

| 75 | 80 | Authorized fund accrued |

| 10, 51, 50,11, 41 | 75 | Funds contributed to the contribution to the authorized capital |

| Capital | ||

| 81 | 50, 51 | Securities purchased |

| 84, 75 | 82 | The reserve fund has been replenished |

| 82 | 84 | Losses are covered using reserve capital funds |

| 75 | 83 | Increased price of securities |

| 75 | 80 | Authorized fund accrued |

| 83 | 75 | Additional capital is distributed among the participants of the JSC |

| 50, 51 | 86 | Special-purpose financing |

| Financial results | ||

| 90 | 10, 21, 41, 43 | The cost of inventory items is written off |

| 62 | 90 | Sales revenue taken into account |

| 90 | 68 | VAT charged on products sold |

| 20, (44) | Actual sales expenses are written off (cost of sales) | |

| 99 | Sales profit taken into account | |

| 40 | The deviation of the actual cost from the planned cost is reflected | |

| 99 | 90 | Loss on sales by main activities |

| 91.2 | 10 | Spare parts written off for repairs |

| 03 | The value of property leased is written off | |

| 20 | Main production services written off | |

| 94 | Shortage written off (no culprit) | |

| 99 | Profit from sales written off | |

| 99 | 91.2 | Other expenses written off at the end of the year |

| 10 | Spare parts from car disassembly are taken into account | |

| 20, 23, 91 | 96 | A reserve has been created for future expenses |

| 99 | 68 | Profit tax accrued |

| 84 | 99 | Uncovered loss identified |

| 99 | 84 | The final result of the work is reflected - profit |

The essence of the business transaction

HO can reflect changes in the assets and liabilities of the balance sheet simultaneously or separately in each of them. Each enterprise must be registered electronically or in paper form for the initial recording of changes. When registering operations, it is necessary to adhere to the order of their occurrence and record events according to this order. Thanks to this technique, the accountant is given the opportunity to:

- maintaining permanent and complete records of all property of the company

- confirmation of each completed transaction with relevant documentation

- application of accounting data for ongoing control activities over the work of the company and for operational management purposes

Primary accounting also maintains financial order in the enterprise, because this information is used to control the legality of ongoing operations and their rationality.