Errors in VAT accounting

Error types can be divided into two parts:

- those related to the calculation of VAT directly

- technical, identified when filling out a VAT return.

To identify the former, you should use a tool such as an express accounting check. Essentially, this is the company's "internal auditor".

To use the tool, in the “Reports” menu in the “Accounting Analysis” section, select “Express Check”. In the window that opens, select a period, for example, the 4th quarter of 2021, and click “Show settings.”

In the settings, check the boxes “Maintain a sales ledger for value added tax” and “Maintain a purchase ledger for value added tax.” Then perform the check by pressing the button of the same name.

The program generates errors separately for the purchase book (CP) and for the sales book (KPR). By clicking on the icon next to the corresponding lines, information about the detected inaccuracies should be revealed.

The example reveals a miscalculation when analyzing the formation of advance invoices in the presence of received prepayments. Now we recommend clicking on the icon next to the line and revealing the details of the mistake made.

The result of the analysis and the cause of the error are indicated here, as well as recommendations for action. To correct this, you need to click on the hyperlink “Registration of advance invoices”.

In the window that opens, set the period, select an organization, and click “Fill.”

The table will be filled with information about unregistered documents. Click the “Run” button. A message will appear indicating that the s/f registration has been completed.

It is important to check the completeness of the personal statement; the program will show which document is missing or not posted. Such accounting errors are also possible as a result of the human factor. And as a result of incorrect data transfer, for example, from “Trade and Warehouse” to “Accounting 8.3”.

Consequently, when generating a declaration, the counterparty will have information about the document. But your company does not, which will lead to tax audits and additional assessments.

Care should be taken to identify compliance in the accounting of sales revenue with accrued tax (account 90), incl. for other income (account 91). For example, fines are not subject to VAT, however, the program mistakenly took into account fines.

Thus, using the tool in question, check how your real activity is reflected in the system.

The meaning of account 76AB in accounting

Good morning. Subaccount 76.AB is used to reflect VAT when receiving an advance from the buyer (customer). If you are a VAT payer, then upon receiving an advance you are required to issue an invoice for the advance and pay tax to the budget (clause 1 of Article 168 of the Tax Code of the Russian Federation). When an advance is received, you make entries in accounting D 51 K 62.02 (based on a bank statement, reflecting your debt to the buyer for the advance received) and D 76.AV K 68.02 (by issuing an invoice and reflecting your debt to the budget in terms of VAT calculation) . Further, after the shipment of goods (performance of work, provision of services), on account of which the advance has been received, you have the right to apply a VAT deduction from the previously issued invoice for the advance (Article 171, Article 172 of the Tax Code of the Russian Federation) and make an entry in the purchase book D 68.02 K 76.AB. That is, subaccount 76.AB serves as a “storage” of information about advances received in the analytics of invoices issued. Subaccount 76.VA is used similarly (VAT on advances issued), when you pay an advance to the supplier, apply a deduction from this advance, and subsequently restore VAT upon shipment. By the way, this numbering (precisely 76.AB and 76.BA) is suggested by the developers of accounting programs in their built-in charts of accounts. Based on the Chart of Accounts (approved by Order of the Ministry of Finance of the Russian Federation of October 31, 2000 N 94n), organizations develop a working chart of accounts containing a complete list of synthetic and analytical accounts necessary for accounting in a particular organization. Therefore, when reflecting the above operations, you can in your working chart of accounts have the necessary subaccounts with a different numbering, for example, 76.10, 76.11, if these numbers are not occupied, 76.AP (advance received), 76.AB (advance issued), etc. ., the main thing is that the possibility of ensuring completeness of accounting is provided.

Account 76 of accounting is an active-passive account “Settlements with various debtors and creditors”, accumulates information on settlements on transactions with debtors and creditors not related to accounts 60-75, for example, on amounts that the organization withholds from wages of employees on the basis of executive documents. Using standard postings and illustrative examples, we will consider the specifics of using account 76, its subaccounts 76.05, 76.09 and 76 AB, as well as the features of reflecting transactions on account 76: accounting for VAT on prepayments, housing and communal services and the sale of an apartment to an employee.

Incorrectly formed records

Similarly, according to the CP, it is necessary to check the completeness of receipt of the tax return, the compliance of the amounts of tax taken for deduction when offsetting advances, in accounting and the VAT accounting subsystem. And also check everything related to the accounting and distribution of tax on purchases.

In our example, during an express check of LLC Trading House "Complex" for the first quarter of 2021, an error was identified in the presence of the document "Creating purchase book entries." We talked about this regulatory operation in the article about purchase and sales books.

By clicking on the icon next to the line, you can expand the details.

Do not forget that before submitting a tax return, two regulatory documents must be generated:

- generating purchase ledger entries;

- generating sales ledger entries.

In the case described above, one of the most common inaccuracies in the CP is an incorrectly formed entry.

When creating entries in the CP, the accounting employee presses the “Fill in” button while on the “Purchased Assets” tab. And he forgets to go to the “Advances Received” tab.

Accordingly, the tax on prepayments received does not fall into the CP.

To correct it, you need to go to the next tab and also click “Fill”.

In the example below, only a single entry related to tax restoration is generated according to the CPR.

A similar situation occurs, for example, when your company made an advance payment to the supplier, and according to the presented s/f, VAT was accepted for deduction. Further, when the contractor supplies goods, work or services, your organization’s accountant must restore the tax previously accepted for deduction.

Restoration is automatically carried out using the routine operation “Creating sales ledger entries”.

Accounting for tax on advances

In general, one of the common mistakes associated with this tax is the incorrect generation of invoices for advance payments. Here it is necessary to clearly understand how such operations are formalized. Upon receipt of an advance payment, an advance payment account is issued, and VAT is taken into account. Further, when goods or services are received, the document reflects the full cost, respectively, when accepting the SF for the goods or tax for accounting. To prevent this from happening, a “reverse” recording is carried out. Tax accepted for accounting from an advance payment is “returned” to the previous account.

For example, at the time the advance payment is received, entry D76.AV K68.02 is generated for the amount of VAT payable on the advance payment of RUB 15,200.

At the time of shipment, posting D62 K90.1 is generated. VAT on sales of 76,000 rubles has been assessed for payment to the Federal Tax Service. – D90.3 K68.2. And the creation of entries in the CP creates posting D68.02 K76.AV in the amount of 15,200 rubles. (restoration of VAT on advances).

In the same way, transactions are made for prepayment and receipt of goods from the supplier.

For example, at the time of payment of the advance and receipt of the SF from the counterparty, entry D68.02 K76.AV is generated for the amount of VAT deductible 22,300 rubles.

At the moment of goods receipt, posting D41 K60 is generated. VAT on sales of 101,000 rubles has been assessed for payment to the Federal Tax Service. – D19 K60. And the creation of entries in KPR will create posting D76.AV K68.02 in the amount of 22,300 rubles. (restoration of VAT on advances).

It is the creation of entries in the books of purchases and sales that allows you to correctly take into account the tax on advances.

How to reflect VAT on advances in the balance sheet

According to the rules of the Tax Code, an organization on OSNO that is not exempt from VAT, when receiving an advance on account of upcoming deliveries of products, works, services upon receipt of them, must calculate VAT (clause 2, clause 1, Article 167 of the Tax Code). Let's do this: VAT payable = 141,600 / 118 * 18 = 21,600 rubles.

At the moment when the clothes are sewn and shipped, Moda LLC needs to charge VAT again - already on the cost of the shipped products: VAT payable = 141,600 / 118 * 18 = 21,600 rubles. And VAT accrued earlier on the advance payment is accepted for deduction (clause 1, clause 1 and clause 14 of Article 167, clause 8 of Article 171 and clause 6 of Article 172 of the Tax Code).

A deduction is made if, after receiving an advance payment, the terms of the contract are changed or terminated and the corresponding amounts of advance payments are returned (clause 5 of Article 171 of the Tax Code). But in our example, we have only received an advance. How to reflect its receipt and the accrual of VAT on advances received in accounting?

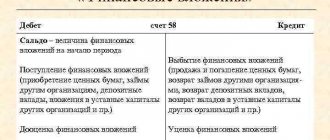

To do this, they usually use one of the subaccounts to account 76:

Technical errors

To identify technical errors, you should use the “VAT Accounting Data Reconciliation” service. It allows you to reconcile invoices with counterparties. It will reflect discrepancies between the other party's invoice information and your organization's.

Accordingly, it will be possible to send a message to the buyer so that he makes corrections, or to correct errors in the SF from the supplier.

To do this, go through the “Administration” menu, “Organizer” section, and follow the “System account setup” hyperlink in the Mail subsection. Here in the window that opens you need to enter your email address, password and check the appropriate boxes.

Next, in the “Purchases” or “Sales” menu, select “Reconciliation of VAT accounting data” in the calculation block.

In order to receive data from the supplier, you need to click on the “Supplier Requests” hyperlink. Next, select those with whom you plan to reconcile and click the “Request registers” button.

In order for the supplier to send the register, the employee must click on the “Customer Requests” hyperlink in his program on his part. Select your organization and click the “Reply” button. Consequently, reconciliation can only be carried out with those companies that also have 1C: Accounting 8.3 installed.

In the reconciliation window, click the “Reconcile” button to create a reconciliation of SF data between your organization and suppliers.

If everything is in order, a message will be displayed that no discrepancies were found. If there are technical inaccuracies, they will be reflected in the generated report. Let's assume that discrepancies are found in this version. According to your company, there is invoice No. 500 dated 02/02/2020 for the amount of 72,000 rubles, but according to the contractor there is no such invoice. However, your company does not have it, but the contractor displays SF No. 50 dated 02/02/2020 in the amount of 72,000 rubles. Accordingly, we can conclude that the accountant made a mistake; instead of number 50, number 500 was entered.

If you do not correct this oversight, you will receive a notification from the Federal Tax Service about a data discrepancy. Therefore, this determination of the correctness of accounting must be approached with all attention and care.

By clicking on the erroneous SF, you can make corrections to your document.

Additional “manual” check

There are often situations when no errors are found during the express check. Next, you should generate “VAT reporting” through the “Reports” menu. Set a period, select an organization and see if all regulatory operations are ticked. If this is so, then the program believes that there are no errors in tax accounting. If there is no checkmark against any of the operations, then it needs to be performed.

Let's assume that all operations are completed and the express check is passed, however, manual analysis will be able to find additional distortions. Therefore, when checking VAT, we recommend that you independently reconcile the indicators for accounts 76.AB and 62.02, for example.

You need to create a balance sheet for account 19, click in the “Reports” menu, in the “Standard Reports” section, on the “Account balance sheet” hyperlink. Set the quarter, in our example this is the 1st quarter of 2021. Select account 19 and the name of the organization. In the settings, set the details for invoices received and check the “By subaccounts” checkbox.

Account 19 is value added tax on purchased assets. If account 19 reflects the balance at the end of the period, it means that your organization did not accept some part of the VAT for deduction. Consequently, there is input tax, but it is not accepted for deduction.

Analysis of account 76

Analytical accounting is maintained separately for transactions. Postings to account 76 form the final balance for each fact of mutual settlements with debtors and creditors. On account 76, subaccounts have many meanings, the most used among them are the following:

- 76.01 - calculations for property and personal insurance. This takes into account operations on life and health insurance of employees and contracts on insurance of enterprise property. Voluntary (within permissible limits permitted by law) and compulsory insurance are taken into account.

- Account 76.02 is used to generate cash flows for claims that have arisen, including the accrual of fines, penalties, and penalties for unfulfilled obligations. Account 76 of subaccount 02 can be applied both in relation to agreements with counterparties and in the event of an outstanding tax debt.

- Using subaccount 76.03, accrued and paid dividends to the founders of the organization are recorded based on the results of the financial year.

- Subaccount 76.04 shows reserved funds for unpaid salaries.

- Account 76.5 in accounting assumes the reflection of other settlements with suppliers and contractors that are not related to the main activities of the enterprise. Account 76.5 includes amounts such as settlements with a notary and the accrual of duty payments. Analytical accounting of account 76.5 is formed separately for each case.

- Account 76.09 in accounting is other settlements with various debtors and creditors, also not related to the main activities of the company. Account 76.09 forms transactions for settlements with auditors, third-party law firms, and reflects the amounts of sponsorship and charitable payments.

- Calculations for third-party debts of employees based on writs of execution, for example, alimony payments, are made using subaccount 76 41.

- Account 76.49 is intended for settlements with the employee for other deductions in accordance with the rules of the organization. Provided that these deductions do not apply to the main ones. Such amounts may include costs for mobile communications and assets purchased within the enterprise.

- Subaccounts 76.AB and 76.VA contain VAT amounts on advances issued and received, respectively. The used account 76 VAT allocates separately from the amounts of advance payment received or on the transferred advances against future deliveries.

The list of presented subaccounts can be supplemented, depending on the nature of the activity and operating conditions of the enterprise, not limited to the movement of funds through subaccount 76.09.

Standard entries to account 76 are used to record transactions that are not involved in the main activities of the enterprise and are of an irregular nature. On the contrary, the balance sheet for account 76 gives an idea of the status of settlements under individual contracts. To simplify the analysis of mutual settlements with other counterparties, the use of various sub-accounts is allowed, including account 76.05 or 76.09 (account for mutual settlements with other counterparties).

Reasons for inaccuracies under Article 19

This may be done on purpose in order to apply deductions later, in the next reporting period, or it may simply be a miscalculation. For example, when posting a receipt, there is no invoice information. If indeed it has not yet been received, then everything is in order. There is no original, but it will appear in the future, for example, in the next quarter. In the same period, the tax will be deducted.

Sometimes it happens that you forgot to register an invoice. In this case, looking at the balance on account 19 in the context of documents, you need to open the document and see what inaccuracies it contains. If the invoice is not registered, but came from the contractor, then you need to enter the information into the system.

It happens that the operator who prepares documents from companies delivering goods or providing services does not understand the difference between the date of issue and the date of receipt. Accordingly, the SF could be issued in the reporting period, but received in the next one.

For example, the date SF is 03/28/2020, but it was received on 04/05/2020, while the operator o.

Indeed, the date of receipt may differ from the date of the invoice. This happens, for example, with a late “primary”. Let's assume that the report is generated when the s/f has already been received. Then, you need to decide whether it is worth leaving a reflection of the deduction by the date of receipt or not. If the company is not going to transfer the deduction to the next period, then this miscalculation needs to be corrected. For example, set the receipt date to 03/31/2020.

As you can see, errors occur that cannot be detected when automatically detected, so you should check the reflection of data on account 19, identify inaccuracies and correct them manually.

Subconto analysis

If routine operations have been completed, an express check has been carried out, everything is in order with account 19, you can look in the “Subconto Analysis” report in the “Reports” menu.

In the window that opens, you need to set the period. Click the “Show settings” button in the “Grouping” tab. In the “Types of subconto” tab, select “Counterparties and “Agreements”. Generate a report by clicking on the button of the same name.

It is necessary to check whether there is a cross-balance for any clients, primarily for account 62. In the example presented, it can be seen that the receipt was made under the agreement “With the buyer” (account 62.01), and the payment was made under the agreement “Untitled” (account 62.02) . Accordingly, at the end of the period, the balance is reflected in both debit and credit, that is, we have both prepayment and debt under different agreements.

In such cases, the program registers invoices for advance payments and takes into account VAT on prepayments. Then the sale takes place and the tax payable is calculated again. If these are really two different agreements under which mutual settlements are carried out, then everything is in order. If this is a mistake, and judging by the name of the agreement “Untitled”, this is what it is, then adjustments need to be made.

Most likely, the wrong contract was selected when entering the document. Or, when downloading a bank statement, the program automatically entered the wrong agreement. Accordingly, mutual settlements are currently reflected incorrectly.

Having indicated the agreement “With the buyer” in the bank statement, it is clear that the cross-balance for the store has disappeared.

Next, after the changes have been made, it is necessary to re-carry out the regulatory operations for generating records of purchase and sales books, depending on what was corrected.

Account 76 av

Receipt of goods from suppliers with invoices has been established. 2. Shipments to customers with invoices have been initiated. 3. Advance invoices have been made for the buyers' prepayments. We begin to study Operations - Closing the period - VAT Accounting Assistant.

There is also a useful summary report in 1C, see. Reports - Analysis of VAT accounting If payment and shipment (receipt) are in the same period, then everything is taken into account very simply: all my documents “Receipts of goods” in the invoice received have a checkbox “Reflect the VAT deduction in the purchase book by the date of receipt.”

Those. here we immediately make entries for VAT refund (68.02 Thus, the document creating the purchase book and sales book are almost empty. And all sorts of advances and other evil spirits got there, which makes the life of an accountant bright and eventful. The problem is that if you spit and don’t understand with advances, then all this will come out anyway.

Therefore, we are looking for algorithms for checking advances.