In what cases is it necessary to draw up

The seller or contractor, having received an advance (partial payment) from the buyer, must draw up an invoice and register it in the sales book. This rule applies when receiving any advances - for the supply of goods, performance of work, provision of services, transfer of property rights. In addition, an invoice must be drawn up even if the advance was received in kind. Such rules are established by paragraph 17 of Section II of Appendix 5 to the Decree of the Government of the Russian Federation of December 26, 2011 No. 1137.

Attention: for the lack of invoices for advance payments (partial payment), the organization may be fined.

The absence of invoices is a gross violation of the rules for accounting for income, expenses and the object of taxation. If the organization did not draw up invoices for only one quarter, the inspectorate has the right to fine the organization in the amount of 10,000 rubles. If a violation is discovered over several tax periods, the fine will increase to RUB 30,000.

If the lack of invoices led to an underestimation of the tax base, the fine will be 20 percent of the amount of unpaid tax, but not less than 40,000 rubles.

This procedure is provided for in Article 120 of the Tax Code of the Russian Federation.

When you don't need to issue an invoice

Do not draw up an invoice if you have received an advance payment for the supply of the following goods (work, services, property rights):

- the manufacturing period of which exceeds six months (clause 13 of article 167 of the Tax Code of the Russian Federation). The list of such goods (works, services) was approved by Decree of the Government of the Russian Federation of July 28, 2006 No. 468;

- which are not subject to VAT or are taxed at a rate of 0 percent (Articles 146, 149, 164 of the Tax Code of the Russian Federation).

In addition, if you are exempt from paying VAT under Article 145 of the Tax Code of the Russian Federation, do not draw up invoices when receiving advances for the supply of any goods (work, services, property rights).

This procedure is provided for in paragraph 17 of Section II of Appendix 5 to the Decree of the Government of the Russian Federation of December 26, 2011 No. 1137.

Situation: is it necessary to issue advance invoices if shipment against the received amount occurs in the same tax period within five calendar days from the date of receipt of money?

An invoice may not be drawn up in this case, but this may lead to disputes with the tax office.

As a general rule, an invoice must be drawn up no later than five calendar days from the date of receipt of the advance (clauses 1 and 3 of Article 168 of the Tax Code of the Russian Federation). In practice, the seller can ship goods (work, services, property rights) against the received advance payment after a short period of time. If this period does not exceed five calendar days from the date of receipt of the advance payment and if the receipt of the advance payment and shipment occur in the same quarter, then the seller (executor) may not issue an invoice for the received advance amount. The validity of this conclusion is confirmed by letters of the Ministry of Finance of Russia dated October 12, 2011 No. 03-07-14/99 and dated March 6, 2009 No. 03-07-15/39, and Resolution of the Presidium of the Supreme Arbitration Court of the Russian Federation dated March 10, 2009 No. 10022/ 08. At the same time, the Presidium of the Supreme Arbitration Court of the Russian Federation explained that if payment and sale occurred in the same tax period, then such payment is not recognized as an advance. The judges justified their position with the provisions of paragraph 1 of Article 54 of the Tax Code of the Russian Federation. According to this norm, the tax base for VAT is determined based on the results of the tax period. In this regard, the seller (performer), who received an advance payment in the same quarter and shipped goods (work, services) against the received amount, does not have the obligation to issue an invoice for the advance payment.

However, representatives of the tax service have a different point of view on this matter. Letter No. KE-3-3/354 of the Federal Tax Service of Russia dated February 15, 2011 states that the seller (executor) who has received an advance payment must issue an invoice in any case - regardless of when the shipment occurs against the received advance payment. This position is based on a literal interpretation of the provisions of paragraph 3 of Article 168 of the Tax Code of the Russian Federation, which does not contain any exceptions in relation to advances, the obligations for which are repaid by the seller (executor) within five calendar days.

Since a unified approach to resolving this issue has not been developed, it is possible that refusal to issue invoices for advances will lead to disputes with inspectors. But taking into account the position of the Presidium of the Supreme Arbitration Court of the Russian Federation, the organization has a high chance of defending its position in court.

If the receipt of the advance and the shipment occur in the same quarter, then in the VAT return for this quarter indicate:

- tax base - twice (in the amount of the advance payment received and the cost of shipped goods (work, services));

- tax deduction – once (in the amount of VAT accrued on the prepayment).

This is stated in letters of the Ministry of Finance of Russia dated October 12, 2011 No. 03-07-14/99 and the Federal Tax Service of Russia dated March 10, 2011 No. KE-4-3/3790.

Situation: Should the seller issue invoices for the difference between the payment he received for the entire month and the cost of all products shipped that month to the buyer? The agreement provides for continuous long-term supplies.

Yes, I should.

The difference between the cost of the shipped products (services, works) and the payment received in this case is considered an advance against future deliveries. And the supplier (contractor) must issue an invoice to the buyer for the amount of the advance (clauses 1 and 3 of Article 168 of the Tax Code of the Russian Federation). This must be done no later than the 5th day of the next month, but always in the same quarter when the funds were received. Register the invoice in the sales ledger.

Such clarifications are contained in the letter of the Ministry of Finance of Russia dated March 6, 2009 No. 03-07-15/39.

An example of how to draw up invoices when advances are received under an agreement for the long-term provision of communication services

The organization entered into an agreement in January for the continuous long-term provision of communication services. Under the contract, the organization provides communication services upon receipt of an advance payment from the buyer. In this case, the difference between the payment received during the month and the cost of services provided in the same month is counted towards payment for services provided by the organization in the next month. As services are provided, VAT accrued on the amount of advances is deductible.

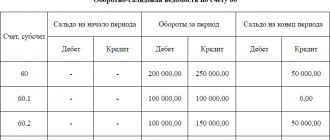

The amounts of advance payments received from the buyer, the cost of communication services provided, as well as the procedure for issuing and registering invoices issued by the organization during the first quarter are presented in the table:

| Month | Amount of advance received, rub. | Cost of communication services provided, rub. |

| January | 1000 | 900 |

| On January 31, the organization’s accountant registered in the sales book: – an invoice for the cost of services sold in the amount of 900 rubles; – invoice for advance payment in the amount of 100 rubles. (1000 rub. – 900 rub.) | ||

| February | 2700 | 2500 |

| On February 28, the organization's accountant registered. In the sales book: – an invoice for the cost of services sold in the amount of 2,500 rubles; – invoice for advance payment in the amount of 300 rubles. ((2700 rub. + 1000 rub.) – (2500 rub. + 900 rub.)). In the purchase book: – an invoice for an advance payment in the amount of 100 rubles, registered in the sales book on January 31 | ||

| March | 1500 | 1000 |

| On March 31, the organization's accountant registered. In the sales book: – an invoice for the cost of services sold in the amount of 1000 rubles; – invoice for advance payment in the amount of 800 rubles. ((1500 rub. + 2700 rub. + 1000 rub.) – (1000 rub. + 2500 rub. + 900 rub.)). In the purchase book: – an invoice for an advance payment in the amount of 300 rubles, registered in the sales book on February 28 | ||

| April | 0 | 800 |

| On April 30, the organization's accountant registered. In the sales book: – an invoice for the cost of services sold in the amount of 800 rubles. In the purchase book: – an invoice for an advance payment in the amount of 800 rubles, registered in the sales book on March 31 | ||

Have you received an advance payment? How to deal with an invoice...

Probably, almost every company has at least once received payment for the upcoming delivery of goods (works, services). For some sellers, working according to the “advance” scheme is a tradition. As is known, the recipient of the advance payment must issue one copy of the invoice for such prepayment. Due to the fact that many issues related to the preparation of invoices when receiving an advance are not regulated by the Tax Code of the Russian Federation, questions in this area do not end. Let's look at some of them...

Marina Ozerova, especially for the news agency Clerk.Ru When to draw up an invoice?

Taxpayers who receive a large number of advances from their counterparties are often interested: is it possible, when receiving several advances during one tax period (month), to issue one invoice at the end of the month for all advances received? After all, this will not affect the calculation of VAT in any way, and issuing a separate invoice for each advance received is quite labor-intensive. Moreover, the 5-day period for issuing invoices is established by the Tax Code of the Russian Federation only for the shipment of goods (performance of work, provision of services).