Features of tax deductions

Only an officially employed person who is a resident can apply for a tax benefit. He must receive a salary and pay tax on it in the amount of 13%.

A tax deduction is an amount that reduces total income, forming the final tax base. Sometimes this concept refers to the return of part of previously paid tax. For example, when purchasing residential real estate, training or treatment. In this case, you can not return the entire amount, but only the money that was paid to the budget.

The employer annually generates a special form of certificate for all employees and sends it as a general report to the inspectorate. In addition, the employee himself may need it; the accountant is obliged, upon the employee’s application, to issue it within three days. When dismissing a person, the employer must also issue this document along with the work book.

The title of the certificate determines its content. It contains information for the year on a monthly basis.

Approved Revenue Codes

For convenience and uniform reflection of income in accounting and tax accounting, certain codes are used. In certificate 2 - personal income tax, separate cells indicate codes by which you can determine the name of the earnings received. The classifier approved by law includes codes consisting of four digits. All income is distributed by codes from 1010 to 4800.

Quite often, when assigning a code, an accountant may doubt the correctness of the chosen cipher. Then they assign it to code 4800. There are no penalties in the law for incorrectly assigning income in certificate 2 - personal income tax. However, this does not mean that codes do not need to be given attention. Different types of income have their own individual code. Incorrect classification may lead to a distortion of the tax base. Accordingly, the tax will be calculated incorrectly.

There are several basic income codes that are used by employers:

- 2000 - salary

- 2012 - vacation pay

- 2300 - disability benefits

- 2400 — rental profit

- 2760 - financial assistance from the enterprise

- 2720 - gifts

- 2730 - prizes

- 4800 - other income

If the directory does not contain the required code for attributing income, it should be designated as code 4800.

It is important to correctly attribute income according to the codes; this will help not to distort the tax base, but accordingly correctly calculate the tax. Nowadays, almost all accounting departments are automated, so problems with incorrect assignments are rare.

Main deduction codes

In addition to income codes, the Tax Code provides codes for tax deductions related to personal income tax. Let's look at the most common ones.

Standard deductions are indicated by:

- 114 - for the first child

- 115 - for the second child

- 116 - for the third and subsequent offspring

- 117 - for disabled children

- 311 - expenses for the acquisition or construction of residential real estate

- 312 - interest expenses on loans

- 320 — expenses for personal training

- 321 - expenses for education of children

- 324 - expenses for medical services

To provide any of the benefits, you need to collect a certain package of documentation and write a corresponding application in the employer’s accounting department. People exempt from paying personal income tax cannot take advantage of such benefits.

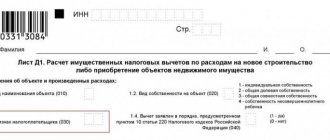

How to put deduction code 501 in the 3 personal income tax declaration for 2021

- a social deduction has been introduced for the costs of undergoing an independent assessment of one’s qualifications for compliance with the requirements for it (Law No. 251-FZ dated 07/03/2021);

- an investment deduction has been established in the amount of a positive financial result from the sale of securities traded on the organized market (Law No. 420-FZ dated December 28, 2021);

- the specifics of taxation of personal income tax on income from the sale of real estate are regulated (Law dated November 29, 2021 No. 382-FZ).

- standard (personal or children's) or social expenses for treatment, training, if the person did not use them at the place of work;

- social (for charity, for contributions to a non-state pension fund or additional contributions to the Pension Fund), which are provided only by the Federal Tax Service;

- investment (for securities), if it is not used in full by tax agents;

- property (for the sale of property, receipt of compensation for real estate, purchase of housing and interest on a mortgage), in relation to some of which submission of a declaration to the Federal Tax Service is mandatory.

What does deduction code 501 mean?

The 501 deduction is applied when an employee receives a gift or prize. For such income, a certain tax calculation scheme is used. When the gift amount is less than 4,000 rubles, it is not included in the tax base. But if the value of the prize exceeds this limit, it is subject to tax. It will be calculated on income minus benefits.

The features of this benefit are as follows:

- The amount of the deduction cannot be higher than 4,000 rubles.

- If the value of the prize is more than four thousand rubles, the difference between the price and the deduction will be taxed at 13%.

Let's look at how this happens with an example.

Suppose a person received a gift worth 8,000 rubles. This amount will be indicated on the certificate; below, the deduction will be indicated with code 501 in the amount of 4,000 rubles. Thus, the tax will be calculated on the amount of 8000 - 4000 = 4000 rubles. And it will be 4000 * 13% = 520 rubles.

Only residents with official income are entitled to claim this benefit.

Noticed a mistake? Select it and press Ctrl+Enter to let us know.

Deduction code 501 indicates that the taxpayer received a gift from an organization or business owner with a value not exceeding the limit. In the article we will look at when such a deduction is included in the certificate, in which section it is reflected and what amount it is.

In the article:

- What does deduction code 501 mean?

- Who is eligible for deduction code 501?

- Where in the 2-NDFL certificate the code with the 501 deduction is reflected.

What does deduction code 501 mean in the 2-NDFL certificate?

Order of the Federal Tax Service of Russia dated September 10, 2015 No. ММВ-7-11/ [email protected] (as amended by Order of the Federal Tax Service of Russia dated November 22, 2016 No. ММВ-7-11/ [email protected] ) contains a complete list of codes for deductions provided under Ch. 23 Tax Code of the Russian Federation.

In Appendix No. 2 of this regulatory act we will find a description of code 501. It looks like this:

- deduction from the value of gifts received from organizations and individual entrepreneurs.

Let us turn to the wording of the Tax Code of the Russian Federation. Article 28 217 contains a list of income exempt from taxation. Such income includes gifts from an organization or individual entrepreneur, but with a total value of up to 4,000 rubles per tax period, i.e., a calendar year.

Despite the fact that the Tax Code speaks here not about deductions, but about non-taxable income, it is this amount of non-taxable income that code 501 implies. For this reason, deduction under code 501 always appears next to income under code 2720. The amount of the deduction cannot exceed the amount income under code 2720.

You can fill out deduction codes for free in 2-NDFL for free in the Bukhsoft program.

What documents do I need to confirm my right to deduction code 501?

When transferring a gift from an organization or individual entrepreneur to an individual, the gift agreement can be concluded either in writing or orally. This follows from the provisions of Art. 574 of the Civil Code of the Russian Federation. A written form of a gift agreement is mandatory only in three cases:

- promise of a gift of movable property in the future;

- donation by a legal entity of movable property worth more than 3,000 rubles;

- donation of real estate regardless of its value (due to mandatory state registration of such an agreement).

In addition, a mandatory primary accounting document is required to reflect the transaction in the accounting records of the tax agent. Such a document could be an order from the manager regarding the presentation of gifts. A certificate of issuance of gifts or other similar documents can also serve as confirmation of the issuance of gifts. The main requirement for such documents is that they can be used to identify the donee (that is, the taxpayer), and you can also determine the value of the gift itself.

Please note that if the recipient did not sign the statement of receipt of the gift or otherwise expressed his refusal to receive the gift, then the tax base with code 2720 (and therefore the deduction with code 501) does not arise.

The right to deduction under code 501 is inherent in the very wording of clause 28 of Art. 217 Tax Code of the Russian Federation. If an employee is given a gift, then the amount up to 4,000 rubles is not subject to personal income tax.

How to fill out tax deductions in the 3-NDFL declaration

- “provide standard deductions”;

- “there is neither 104 nor 105 deduction” (which means that Stepanov I.A. has no right to a deduction of 500 or 3,000 rubles per month provided to the categories of persons specified in paragraph 1 of Article 218 of the Tax Code of the Russian Federation);

- “the number of children per year did not change and amounted to” - from the list Stepanov I.A. chose the number “1”, which means that he has an only child.

For the purposes of filling out 3-NDFL, a tax deduction is usually understood as a decrease in the income received by an individual or individual entrepreneur, on which income tax is paid. The same term denotes the return of previously paid personal income tax in situations provided for by the Tax Code of the Russian Federation (in connection with the purchase of property, expenses for training, treatment, etc.).

This is interesting: What low-income families are entitled to in Yakutsk

The nuances of reflecting deductions with code 501 in the 2-NDFL certificate

The limit on the non-taxable amount of financial assistance is imposed on the taxpayer, that is, on an individual, for one calendar year. After the total value of gifts exceeds the amount of 4,000 rubles, all subsequent income is taxed. In this case, the amount of non-taxable income is calculated as follows:

- in January, an employee was given a gift worth 2,000 rubles, the entire amount of the gift is not subject to taxation;

- in August, an employee was given a gift worth 3,000 rubles - in the current calendar year, only 2,000 rubles of the deduction were spent, which means that a deduction in the amount of 2,000 rubles can be applied to the August gift, respectively, personal income tax is withheld only from 1,000 rubles.

The position of some officials (for example, letter from the Federal Tax Service for Moscow dated March 14, 2018 No. 20-14 / [email protected] ) indicates that if income is completely tax-free, then it may not be reflected in the 2-NDFL certificate (neither the income itself, nor the deduction). And if part of the income is subject to taxation, the certificate must reflect the entire amount of income and the amount of the deduction.

That is, in the case when a gift is given in the amount of 2,000 rubles, such a gift may not be shown in tax reporting forms at all. But if a gift was given to an employee in the amount of 7,000 rubles, the reporting form must reflect income with code 2720 in the amount of 7,000 rubles and a deduction with code 501 in the amount of 4,000 rubles.

This position applies not only to filling out the 2-NDFL certificate, but also to completing the 6-NDFL reporting form.

There is one more nuance regarding the deduction with code 501. This applies to cases when it is impossible to personalize the recipients of the gift, as well as to assess the economic benefit of the gift recipients. For example, this situation may arise when giving gifts in the form of gift certificates or tickets to entertainment events. Then, according to officials, there is no tax base. And since there is no tax base, then there is no deduction either. This position can be found in the letter of the Ministry of Finance of the Russian Federation dated 09/08/2015 No. 03-07-07/51585.

Deduction codes are indicated in the 2-NDFL certificate. Each deduction has its own code. For which deductions the 501 deduction code is used, read the article.

How to fill out the 3rd personal income tax return and receive a property tax deduction

- joint property. It does not matter who is recorded in the certificate as the owner, if the apartment was purchased during marriage, the property is recognized as joint property in accordance with the Family Code of the Russian Federation (Articles 33, 34 of the RF IC). As a general rule, the deduction is distributed in equal shares (50%), but spouses have the right to redistribute it in any proportion by submitting to the tax office an Application for the distribution of shares (in any form).

For housing purchased after January 1, 2021, the total deduction is limited to RUB 2,000,000. applies to every citizen. That is, the husband can receive a deduction from 2,000,000 rubles (260,000 rubles), and the wife can receive a deduction from 2,000,000 rubles. (RUB 260,000).

This is interesting: Article 212 In 2021

Deduction code in certificate 2-NDFL

Every year, companies report the income of their employees and the amount of taxes withheld from them. To do this, use a certificate in form 2-NDFL.

During the year, an employee can contact the accounting department to obtain a 2-NDFL certificate, for example, for a bank.

When drawing up a certificate in form 2-NDFL, use the Procedure, which was approved by order of the Federal Tax Service dated October 30, 2015 No. ММВ-7-11/485. Fill out the certificate information based on information from the personal income tax registers.

Deduction codes are indicated in the table of section 3 of form 2-NDFL. Each deduction has its own code.

Income and deduction codes for personal income tax in 2021: table

- The deadline for submitting 2-NDFL with sign 1 or 3 is no later than April 1 of the year following the expired calendar year (Article 216, clause 2 of Article 230 of the Tax Code of the Russian Federation, clause 2.7 of the Procedure for filling out the 2-NDFL certificate).

- The deadline for submitting 2-NDFL with sign 2 or 4 is generally no later than March 1 of the year following the expired calendar year. During this period, you must not only submit the certificate to the tax authority, but also hand it over to the individual (Article 216, clause 5 of Article 226 of the Tax Code of the Russian Federation, clause 2.7 of the Procedure for filling out the 2-NDFL certificate).

- income that you paid to an individual in cash and in kind, as well as in the form of material benefits;

- tax deductions from these incomes provided to individuals (except for standard, social and property ones).

Please note => Quota penalties for non-compliance