Author: Ivan Ivanov

In the balance sheet, the accounting accounts are arranged in a tabular form in ascending order. The accountant enters data at the end of each month from journals, in which daily business activities are conducted, expressed in monetary terms. The table is filled out, displaying the balances at the beginning and end of the reporting period, indicating the total turnover that has passed during this time.

As a result, a financial document is generated for any period necessary for analysis. It can be in the form of a monthly, quarterly, annual time period, providing a working picture of the enterprise, the turnover of funds to management, and any interested party.

Some General Rules and Observations

I assume, reader, that you remember that accounting accounts collect and store information about the activities of a business. All information is separated according to certain criteria. So, the code and name of the accounting account serves as a separation criterion. As a result, OSV shows all the accounting accounts involved in our enterprise. From the OSV we see what information has been collected.

However, the balance sheet collects business information in a different way.

Firstly , the balance sheet divides information into ASSETS and LIABILITIES.

Secondly , within ASSET and LIABILITY, information is divided into certain groups. Each such group is an economic indicator.

Ultimately, SALT is simply regrouped on the balance sheet.

- All debit balances, and these are accounts with characteristic A, go to the “ASSET balance” section

- All credit balances, and these are accounts with characteristic P, go to the “LIABILITY” section of the balance sheet.

- Accounts with the AP characteristic are transferred to the balance sheet as follows: if there is a debit balance, it goes to an ASSET, if there is a credit balance, it goes to a LIABILITY.

The amount received in ASSET or LIABILITY is entered into the specific name of the economic indicator. The basis for including the amount in the economic indicator will be the name of the accounting account, or, when it is not clear, we will use the law on filling out the balance sheet. Well, we will start filling out the balance very soon.

Why do you need a completed document?

Every organization requires reporting, which is maintained by officials responsible for this type of activity. The report contains information showing balances, cash flows in each account and between them during the reporting period. Filling of the OSV occurs after:

- depreciation charges;

- write-off of production costs;

- tax assessments;

- formation of a financial report.

With the help of this document, items are formed in the balance sheet. He controls the correctness of the transactions made and systematizes the information expressed by them. Based on the “turnover”, facts are visible that influenced the changes that occurred in qualitative and quantitative form in the balance sheet registers. According to the data from the SALT, the digital values of various areas of activity are compared, from which it is clear what influenced the financial result of this institution.

An example that determines why a negotiable accounting instrument is needed can be presented in the following diagram:

- The enterprise is working.

- Accounting records business transactions in primary documents.

- In special journals, transactions are carried out on transactions using ledger accounts.

- Each register accumulates the same type of information.

The results of calculations are posted in standard reports, presented as balance sheets. The work of the chief accountant and the entire accounting department is not limited to this. SALT is a convenient settlement form for enterprise financiers, which they need to work with every day.

Using a table:

- analyze the company's activities;

- monitor results;

- identify and eliminate errors caused by postings.

For the head of any organization, it is necessary not only to be able to competently fill out the form, a leading economist will do this, but also to know how to read and decipher each thesis presented.

Fixed assets and intangible assets when filling out the balance sheet

Fixed assets are inextricably linked with such a concept as depreciation (accounted for in account 02). Depreciation is a gradual decrease in the initial cost of an asset associated with the operation of the asset. The depreciation process for fixed assets occurs over a certain period of time, but more than a year. As a result, everything will come to the point that the amount of depreciation will be equal to the original cost of the operating system.

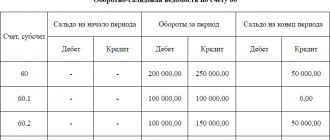

Look at SALT . Account 01 records the amounts of all fixed assets at their original costs. Account 02 takes into account the depreciation amounts of these fixed assets. Now you are asking yourself, what does this have to do with the balance sheet?

It would seem that according to the rules for posting amounts from SALT to the balance sheet, we must send the amounts from the 01st account to the ASSET, and send the amounts from the 02nd account to the LIABILITY of the balance sheet. However, there is an exception for Fixed Assets.

Its essence is that before sending the amount to the balance sheet, we take the amounts from 01, subtract the amounts from 02 and send the resulting amount to where????

IN THE ASSET balance. Because depreciation can never be more than the original cost of the asset, and therefore the difference between 01-02 will always be a debit. 01 account (A) > 02 account (P). Well, in extreme cases, it will be 0.

Exactly the same situation with accounts 04 and 05. This takes into account the assets of an enterprise that do not have a physical object, like a machine or a machine. Account 04 takes into account such assets of the enterprise as licenses, the exclusive right to a patent, the exclusive right to software, etc. Their period of use is also more than 12 months and they are not intended for resale. Everything is the same as with the OS. Depreciation of Intangible Assets (IMA) is accounted for on account 05.

To finish this article, I propose to do a practical task. We'll work a little with the numbers from the OS. The task is:

- divide your sheet in a notebook or notepad into two columns: “Asset” and “Passive”

- from SALT we will work with the column “Balance at the beginning of the period”

- according to all the rules studied in this article - write out the accounting accounts and amounts, what can be classified as “Asset” and what can be classified as “Liability”

- In each column, calculate the total of all amounts

- compare the total amount of “Asset” and the total amount of “Liability”

To complete the task, you already have previously downloaded OSV. If you haven't downloaded it yet, download it here.

Perhaps now we are ready to fill out the balance sheet. We will do this in the next article. I invite you.

Formation procedure

Purchasing a form to keep track of the movement of funds is not a problem.

They are freely available:

- on financial sites;

- in stores selling office supplies.

You can easily create such a table yourself using Excel spreadsheets.

Software systems allow you to use SALT for general accounts and with each account separately, which simplifies the accounting task. Although specialists almost never use manual labor to fill out financial papers, it is better for novice entrepreneurs to start with a fountain pen. By manually filling out the statement, you will gain a deep understanding of the essence of the operation being carried out, for which double entry is carried out. Financiers use different registers, the choice depends on the area to be analyzed and the way the data is presented.

An example is synthetic accounts. To account for them, take the initial balance with turnover, and as a result, calculate the balance at the end of the billing period.

The total amount in a correctly prepared statement consists of three parts:

- equality between income and expense, where the debit balance reflects the value of the organization at the initial stage and the receipt of assets in the credit register;

- the equivalence of debit and credit turnover is achieved by double entry, in which money entered in debit to one of the accounts is credited to the other;

- the last column consists of the equality obtained as a result of calculations, this is the price of the asset, the amount at the end of the period.

The calculator clearly monitors pairs of numerical values. If a difference is detected in at least one case, it means the register is formed incorrectly or a simple arithmetic error has occurred. Based on the synthetic accounts included in the “turnover”, the balance sheet is processed, in which the names of the sections are often the same as the accounts.

Analytical accounts in SALT are formed depending on their purpose and the characteristics of specific parameters:

- nomenclature;

- quantitative;

- categories.

This part of the reporting is not equal in terms of turnover, because cash movements occur in the same register. The balance at the beginning of the month and at the end can be in the debit or credit column, which depends on the passivity or activity of the account. For example, you can give a salary account of 70.

The types of accounts include chess OSV from synthetic accounts. “Chess” receives data from operational logs in compliance with the final equations.

This type of financial table can be described with the following description:

- Debit accounts go vertically, credit values are written in the horizontal line;

- the completed lines and columns are equal to the accounts used with the opening balance and cash flows in the reporting period;

- the accountant posts accounts according to their opening balances;

- an angular calculation is performed from the summation of income and expense;

- values for all business transactions are transferred, the amount is indicated at the intersection of interacting accounts;

- circulating numbers are also calculated with their output in the corner of the table;

- The end of the ending balance calculation is the angular total.

The balance of digital definitions is the coinciding debit turnover with the credit one. In this case, the economist correctly posted all business transactions and made correct calculations, which makes it possible to proceed to the main document.

We fill out the balance sheet according to the turnover balance sheet

The goal is clear - to lead you, the reader, to filling out the balance. Make sure you are as prepared as possible for this action. And, although I have to try to make the explanation understandable, there is still something missing in this article.

I understand that there will still be questions, but I want to keep them to a minimum. I think that I will answer some of these questions in advance. Before we start filling out the balance sheet form , I suggest working a little more with SALT.

This is what we need to do.

- we continue to work with the first column of SALT - “opening balance”

- write down the invoices that you believe collect information about our company's debts. You can immediately start writing out those bills that you know are in SALT. You can go the opposite way - cross out those accounts that are responsible for the company’s property, for what you can touch. The remaining bills are what you need.

- Issued invoices have amounts in “Debit” or “Credit”, or even both. Write out the invoice, each amount, and write what kind of debt it is - “Should our

- Remember what is called “Our Debt” in accounting. In parentheses for these names, write accounting terms for each amount. For tips, read this article.

Once you do it, compare it with what I got.

Methodology for preparing a balance sheet

Preparing a balance sheet is the most important element of the work of any accountant. A completed balance sheet of an enterprise is not only a document for reporting to the Federal Tax Service. It is also a source of data for analyzing the current activities of the enterprise and making forecasts. Let's consider what rules determine the procedure for filling out the balance sheet .

To be presented as official reporting, the balance sheet has a specific form. For the internal needs of an organization, it can have many modifications depending on the purpose and the type of data for its compilation:

· data can be taken either on specific dates (balance sheet) or by turnover for a period (turnover balance);

· source data can be either only accounting, or only inventory, or accounting that is confirmed by inventory results;

· data can be taken into account either with the inclusion of regulatory items (depreciation, reserves, markup) or without them;

· a balance sheet can be drawn up in relation to only one of the types of activities of the enterprise;

· the balance sheet can have either a full or abbreviated form;

· the balance sheet can be drawn up in the form of equality between assets and the sum of capital and liabilities, or it can be in the form of equality between capital and the difference between assets and liabilities;

· a balance sheet can be made for one organization or include data for several enterprises (consolidated and consolidated balance sheets);

· in relation to an event, there may be opening, liquidation, separation, and unification balance sheets;

· the balance can be preliminary, forecast, interim, final.

And this is not a complete list of possible options for drawing up a balance sheet for an organization to solve its internal problems.

How to collect a balance from a turnover balance sheet

However, the fundamental approaches to filling out this form remain the same regardless of the way the source data is reflected in it.

Recommended reporting forms for submission to the Federal Tax Service were approved by Order of the Ministry of Finance of the Russian Federation dated July 2, 2010 No. 66n.

The full form of the balance sheet contains the entire list of items that are recommended to be highlighted in the appropriate sections of the balance sheet. However, an enterprise can exclude items from the balance sheet for which it does not have data, and, conversely, include additional items in it if this increases the reliability of the reports prepared.

The full form has a box to display notes for each article. The enterprise decides for itself whether it needs to use this column. Obviously, it becomes necessary for any deviation from the standard recommended form.

The basic rules governing the procedure for drawing up a balance sheet for official reporting purposes are contained in PBU 4/99, approved by Order of the Ministry of Finance of the Russian Federation dated July 6, 1999 No. 43n. They boil down to the following:

· the source of information for drawing up the balance sheet is accounting data;

· accounting data must be generated according to the rules of the current accounting regulations and in accordance with the accounting policies adopted by the enterprise;

· credentials must meet the requirements of completeness and reliability;

· an enterprise that has branches draws up a single balance sheet for the organization;

· data reflected in the balance sheet must be neutral and correlated with data from previous periods;

· the allocation of items in the balance sheet sections is carried out according to the principle of materiality;

· the reporting period for the balance sheet is a calendar year;

· assets and liabilities reflected in the balance sheet should be divided into short-term and long-term (existing for less than and more than 12 months, respectively);

· offset between items of assets and liabilities is not made if it is not provided for by the PBU;

· property is valued at its “net” value (less regulatory items);

· accounting data of the annual report must be confirmed by inventory.

The balance sheet is filled out on the basis of information about the balances in the accounting accounts as of the reporting date. These balances are reflected in the balance sheet in accordance with the objectives assigned to a specific report.

In relation to data on the financial result (retained earnings/uncovered loss), the current balance sheet is prepared, as a rule, by including in the reporting period the full number of months of the year for which it is formed. This is due to the fact that financial results accounts are generally closed on a monthly basis.

Data in the balance sheet are most often shown in thousands, less often in millions of rubles.

The division of assets and liabilities into long-term and short-term is provided for by the structure of the balance sheet. In his assets, two sections are allocated for this: non-current assets (long-term) and current assets (short-term). The liability is divided into three sections, two of which are sections on obligations, divided by the time of circulation (long-term and short-term). The third liability section reflects data on equity, which occupies a special position in the structure of the balance sheet.

Reflecting information on specific balance lines has its own characteristics:

· data on the cost of fixed assets (including those intended for rental) and intangible assets are shown, as a rule, minus depreciation;

· information on R&D, tangible and intangible exploration assets is filled in only if such assets are available, while exploration assets are reflected net of depreciation;

· data on financial investments, which are loans issued, cash investments in banks (deposits), deposits in other organizations, in securities, are divided depending on their maturity into long-term and short-term and are shown, respectively, in different sections of the asset, when in this case, the amounts are reflected minus the created reserve for depreciation of financial investments;

· information about deferred tax assets and liabilities present in the asset (non-current assets) and liability (long-term liabilities) lines of the balance sheet is filled out only by those organizations that apply PBU 18/02;

· data on inventories, including balances on accounts for materials (with inventory items), goods, finished products, work in progress, RBP, are reduced by the amount of created reserves for depreciation of goods and materials and the amount of trade margin, if goods are accounted for with it;

· accounts receivable and payable, which are amounts that someone owes the company and that the company owes to someone (counterparties, budget, funds, employees), are shown in detail and are reflected, respectively, in the assets and liabilities of the balance sheet as part of short-term liabilities; in this case, accounts receivable are reduced by the amount of created reserves for doubtful debts and data recorded on other balance sheet lines (financial investments);

· VAT on advances may be reflected in the balance sheet differently, depending on the accounting policy adopted by the enterprise;

· cash (cash, non-cash, foreign currency) are shown in the total amount minus deposits accounted for in the lines of financial investments;

· the amount of additional capital, if present in accounting, is divided into two lines, depending on whether it is related to the revaluation of property;

· financial result (retained earnings or uncovered loss) in the annual balance sheet represents the result of activities for a finite number of years (after balance sheet reform), and in interim reporting it consists of two figures (financial result of previous years and financial result of the current period), while outside depending on the reporting period, it may be a negative value;

· data on borrowed funds are divided into long-term and short-term liabilities according to the remaining period of their repayment and are shown in different sections of liabilities, while accrued interest on long-term loans is included in short-term debt;

· in a similar manner, depending on the remaining period of use, estimated liabilities are divided into long-term and short-term liabilities reflected in different sections of liabilities, which correspond to the amounts of created reserves for future expenses;

· data on future income additionally includes information on the amounts of targeted financing;

· all sections of the balance sheet, with the exception of the “Capital and Reserves” section, have a line for reflecting other assets or liabilities, intended for entering into it data that does not find a place in other lines of the corresponding section, or for those data that the organization decided to show separately .

· To fill out balance sheet items, data on balances formed as of the reporting date is taken from specific accounting accounts. In relation to the current version of the chart of accounts of accounting, approved by order of the Ministry of Finance of the Russian Federation dated October 31, 2000 No. 94n, when filling out the full balance sheet form, the balances on the following accounts are used:

· for the article “Intangible assets” - the final balance on account 04 minus the total on account 05, while for account 04 the data falling in the line “Results of research and development” is not taken into account, and for account 05 – figures related to intangible search results assets;

· for the article “Results of research and development”, data on R&D costs reflected in the balance on account 04 is selected;

· for the articles “Intangible exploration assets” and “Tangible exploration assets”, data on the costs of developing natural resources is taken from account 08 minus depreciation related to these assets, taken into account, respectively, on accounts 02 and 05;

· for the item “Fixed assets”, the data is determined as the difference between the balances of accounts 01 and 02 (account 02 does not take into account figures related to material exploration assets and profitable investments in tangible assets), to which is added the amount of capital investment costs accounted for accounts 07 and 08 (except for the figures included in the lines “Intangible search assets” and “Tangible search assets”);

· for the article “Profitable investments in assets”, the difference between the balances of accounts 03 and 02 in relation to the same objects is taken;

· for the item “Financial investments” in non-current assets, data on long-term amounts (with a repayment period of more than 12 months) in accounts 55 (for deposits), 58, 73 (for loans issued to employees) is selected, which are reduced by the amount of reserves for long-term investments (account 59);

· for the item “Deferred tax assets” the balance of account 09 is taken;

· for the item “Inventories”, the amount is formed by adding the balances on accounts 10, 11 (both accounts minus the reserve recorded on account 14), 15, 16, 20, 21, 23, 28, 29, 41 (minus account 42, if accounting of goods is carried out with a markup), 43, 44, 45, 46, 97;

· for the article “Value added tax on acquired assets”, the balance of account 19 is taken;

· for the item “Accounts receivable”, the debit balances on accounts 60, 62 (both accounts minus the reserves formed on account 63), 66, 67, 68, 69, 70, 71, 73 (minus the data recorded under the item “ Financial investments"), 75, 76;

· for the article “Financial investments (except for cash equivalents)” in current assets, data on short-term amounts (with a repayment period of less than 12 months) in accounts 55 (for deposits), 58, 73 (for loans issued to employees) is selected, which reduced by the amount of reserves for short-term investments (account 59);

· for the item “Cash and cash equivalents” the amount is obtained by adding the balances of accounts 50, 51, 52, 55 (except for deposits), 57;

· for the article “Authorized capital (share capital, authorized capital, contributions of partners)” the data is taken as the balance of account 80;

· for the item “Own shares purchased from shareholders”, the balance of account 81 is taken;

· for the article “Revaluation of non-current assets”, data on balances on account 83 related to fixed assets and intangible assets are selected.

· for the item “Additional capital (without revaluation)” the data is formed as balances on account 83 minus data relating to fixed assets and intangible assets;

· for the item “Reserve capital”, the balance of account 82 is taken;

· for the article “Retained earnings (uncovered loss)”, the balance of account 84 is included in the annual balance sheet, and when preparing interim reporting, two balances are added up: account 84 (financial result of previous years) and 99 (financial result of the current period of the reporting year), in this case, the sum can be formed both by addition and by subtraction;

· for the item “Borrowed funds” in the section “Long-term liabilities”, long-term (with a remaining maturity of more than 12 months) debt on loans and borrowings is selected from the balances on account 67, while interest on long-term borrowed funds must be taken into account as part of short-term accounts payable ;

· for the item “Deferred tax liabilities”, the balance of account 77 is taken;

· for the article “Estimated Liabilities” in the “Long-Term Liabilities” section, from the balances on account 96, data on long-term reserves, the useful life of which exceeds 12 months, is selected;

· for the item “Borrowed funds” in the section “Short-term liabilities”, the balances on account 66, interest on long-term borrowed funds taken into account in the balances on account 67, and that debt on long-term loans and borrowings (account 67), which at the time of drawing up the report, are summed up has become short-term (less than 12 months left until its maturity);

· for the item “Accounts payable”, credit balances on accounts 60, 62, 68, 69, 70, 71, 73, 75, 76 are summed up;

· for the item “Deferred income”, the balances of accounts 86 and 98 are added up;

· for the article “Estimated Liabilities” in the “Short-Term Liabilities” section, from the balances on account 96, data on short-term reserves, the useful life of which is less than 12 months, is selected.

Rules and technique of compilation

The balance sheet shows the balance of funds for a certain time. The accounting accounts display the work of the enterprise in monetary terms; values are set from the new results obtained, which are transferred to the table.

The formation of a simplified balance sheet using a balance sheet occurs according to the following activities:

- processing of account data is carried out in order to carry out incoming and outgoing transactions to display final balances;

- a graphological system is compiled, in which the turnover of each account is recorded line by line under debit and credit;

- calculate all the figures for income and expenses, which are equated as a result;

- the total represents an inventory of all account balances;

- check the correctness of the final values, add active current accounts to the initial balance upon receipt, subtract all the values that are posted on the loan;

- for passive accounts, take the credit balance, add its current assets and subtract the values for the debit turnover;

- the resulting figure must be identical to the posting from the accounts.

The overall result consists of the final values:

- initial;

- final;

- negotiable

All amounts are recorded under the balance sheet. Its working form represents the result obtained from the total of debit balances, which is equal to the credit balance, they are withdrawn from all financial accounts.

The full balance sheet form consists of the entire list of items recommended for allocation in a specific section. Financiers of organizations are allowed to remove from the reporting those designations that are not involved in the activities of the institution, or, conversely, add information for complete reliability.

Balance sheet (form No. 1). Instructions, rules and filling procedure

Balance sheet

- this is a way of generalizing and grouping the assets of the economy and the sources of their formation - liabilities - at a certain date in monetary value. Balance sheet indicators characterize the financial position of the organization as of the reporting date.

The main task of the balance sheet

– show the owner what he owns or what capital is under his control. The balance sheet allows you to get an idea of material assets, the amount of reserves, the state of payments, and investments.

Synthetic and analytical accounting

Accounts that are intended for a generalized reflection of economic assets and their sources are considered synthetic. This type is used to account for company funds in a single monetary value.

Synthetic accounting is used:

- to fill out reports,

- to fill the balance,

- analysis of the financial and economic activities of the company.

To control the safety of valuables, you need to know not only their total value, but also other data necessary for identification. If a company has accumulated debt, along with finding out its total volume, it is necessary to determine the reason for its occurrence.

Analytical accounts allow you to keep records in both physical and monetary terms. They open in addition to synthetic ones. Recording transactions with category accounts is called analytical accounting. Its implementation is necessary to control and ensure the safety of inventory items.

How to fill out a balance sheet example

Balance sheet data is widely used for subsequent analysis by the organization's management, tax authorities, banks, suppliers and other creditors.

The balance sheet consists of 2 main parts - assets

and

passive

. The asset represents the organization's resources, and the liability represents the sources of their formation. A distinctive feature of the balance sheet is the equality of the totals of assets and liabilities. This is due to the double entry principle used in accounting.

Assets

The balance sheet contains 2 sections:

- I. Non-current assets;

- II. Current assets.

Passive

The balance sheet consists of 3 sections:

- III. Capital and reserves;

- IV. Long term duties;

- V. Short-term liabilities.

Each asset and liability element of the balance sheet is called a balance sheet item

. Asset items reveal the nature of resources, their use and magnitude. Liability items characterize the sources of resource formation, namely: from what source this part of the assets was created, for what purpose they are intended and their value.

When preparing a balance sheet, keep the following in mind:

- the balance sheet data at the beginning of the year must correspond to the data at the end of last year (taking into account the reorganization);

- offset between items of assets and liabilities, items of profit and loss is not allowed, except in cases where such offset is provided for by the relevant Accounting Regulations;

- the corresponding balance sheet items must be confirmed by inventory data of property, liabilities and settlements.

The standard form of the balance sheet is regulated by the Ministry of Finance (order No. 67n dated July 22, 2003). However, organizations can independently develop a balance sheet form, using the standard one as a template. In this case, the general requirements for accounting reporting must be observed.

When developing and adopting the balance sheet form (Form No. 1), it is recommended to use the total line codes and line codes of sections and groups of items given in the sample balance sheet form. If a transcript is provided for any indicator in a balance sheet developed by an organization independently, then the articles in this transcript are coded by the organization itself.

The balance sheet contains the following mandatory details

:

- the reporting date as of which the balance sheet is presented;

- full name of the organization in accordance with the constituent documents;

- taxpayer identification number (TIN);

- the main type of activity of the enterprise with the OKVED code;

- organizational and legal form/form of ownership (according to the OKOPF and OKFS classifiers);

- unit of measurement - thousand rubles. (OKEY code 384) or million rubles. (OKEY code 385);

- location (address);

- date of approval (indicates the established date for the annual financial statements);

- date of sending/acceptance (the specific date of postal, electronic and other sending of financial statements or the date of their actual transfer according to ownership is indicated).

Total figures for balance sheet items are given in thousands of rubles without decimal places. Organizations with significant sales turnover, liabilities, etc. can provide data in millions of rubles (without decimal places).

Indicators on certain types of assets, liabilities, income, expenses and business transactions may be presented in the balance sheet as a total amount with disclosure in the notes to the balance sheet, if each of these indicators individually is not significant for the assessment by interested users of the financial position of the organization or the financial results of its activities.

Let's consider the procedure for filling out Form 1 “Balance Sheet”

.

In the column “ At the beginning of the reporting year

» shows data at the beginning of the year (opening balance sheet), which must correspond to the data in the column “At the end of the reporting period” of the previous year (closing balance sheet), taking into account the reorganization carried out at the beginning of the reporting year, as well as changes in the assessment of financial reporting indicators associated with the application of the Regulations on accounting and financial reporting in the Russian Federation and the Accounting Regulations “Accounting Policy of the Organization” PBU 1/98.

In the column “ At the end of the reporting period

» shows data on the value of assets, capital, reserves and liabilities at the end of the reporting period (month, quarter, year).

You can form No. 1 in the following formats:

Central moments

Features of compilation

There are several types of statements:

- according to analytical account;

- according to synthetic account;

- chess.

The statement can be drawn up only after the account entries have been made.

When the data preparation is completed, you can proceed to filling out the table.

It consists of 2 columns:

- Account number;

- account name;

- balance at the beginning of the month;

- turnover for this month;

- balance at the end of this month.

The last 2 columns are filled in the same way. The result needs to be verified. To do this, you need to add up the data from all columns. If the document was drawn up correctly, the debit and credit results in each column will match in pairs.

Requirements for chess content

The chess sheet is a type of synthetic sheet. However, unlike the last paper, the “checkerboard” data is entered using the transaction journal, and not according to accounting accounts. To compose a chess OCB in 2021, you need to follow certain rules.

To fill out the document, you must carefully list the account numbers

It is important not to skip data. Next, at the intersection of the columns, you need to post the amounts that correspond to the subaccount numbers

If problems arise with the manipulation, you can use a ready-made example.

The number of horizontal and vertical columns is not limited. It must correspond to the total number of accounts. When the sheet is completed, you need to calculate the results horizontally and vertically. In this case, the final numbers must coincide.

If the results differ horizontally and vertically, an error was made when filling out the document. The completed table will have to be checked completely. Only then will it be possible to generate a balance sheet.

Types and method

Highlight:

According to synthetic accounts

The document contains the balance at the beginning of the period and data on account turnover. By making calculations, the accountant can determine the balance at the end of the period

When compiling a statement, it is important to make sure that the manipulation is carried out correctly. If all steps are performed correctly, you will get 3 equalities - the balance of credits and debits, the turnover of credits and debits, the value of liabilities and assets at the end of the period. If there is a discrepancy even by 1 digit, an error was made

To identify it, you will have to carry out all the calculations again.

According to analytical account

Data is entered into the document according to account nomenclature, quantitative indicators and categories. The statement reflects the ongoing movement within the account. There is no equality of turns. The account itself can be either credit or debit.

Chess

The document is an advanced synthetic statement. It is filled in based on the transaction log. The document is considered completed correctly if equality of indicators is maintained.

Varieties of documents can be compiled over a year or a shorter period.

Where can I download it?

The form and sample filling can be downloaded on the Internet. Guided by the ready-made material, the accountant will simplify the procedure for preparing the document and minimize the likelihood of making mistakes. The paper form can be downloaded in World or Excel. However, experts recommend filling out the paper in the 1C 8.3 program. Using specialized software will speed up data entry and calculation.

Mini-instructions for calculating the balance sheet

Fill out the header of Form 1 , or enter the data into a computer accounting program.

Fill out the first section of the asset - non-current assets . This takes into account: fixed assets of the enterprise that can be invested in construction, whether it is completed or not, in material assets, and various assets. This data is entered into the corresponding lines of the finished balance sheet form.

Complete the second asset section – current assets. This takes into account: various inventories of the enterprise, amounts of VAT not yet accepted for deduction, accounts receivable, investments of the enterprise invested for a short period, free finance and other assets.

Complete the third liability section – capital and reserves. Here, such types of capital as authorized and additional capital are taken into account. Data on reserve capital is indicated, for example, set aside for future planned expenses. Retained earnings should also be indicated in this paragraph.

Complete the fourth liability section - long-term liabilities. This takes into account: long-term loans, for example, loans. At this stage, obligations to the tax authorities are indicated that have been deferred for a number of reasons, as well as other obligations for payments on behalf of the enterprise.

Complete the fifth liability section - short-term liabilities . This takes into account: loans and credits taken out for a short period of time, debt on such, debt to the founders. Planned incomes are included in the balance sheet, as well as expenses and finances that are reserved for them. Short-term liabilities must also be indicated.

The balance is considered consolidated when the total amount for assets fully matches the total amount for liabilities.

The easiest way to prepare a balance sheet is to use specialized accounting software.

What do the main abbreviations mean?

In accounting, abbreviations are often used that are understandable to specialists and unclear to beginners. Typically, the decoding represents the name from the first letters and indicates the working area, the name of the current funds or the economic activity of the unit. Such an abbreviation can be represented as:

- expenses for transport and procurement of materials - TZR;

- assets belonging to fixed assets - OS;

- intangible assets - intangible assets;

- production that is in an unfinished stage - work in progress;

- expenses for future periods - RBP;

- inventory items - goods and materials.