First page design

- First of all, on the title page you must indicate the full name of the enterprise (in accordance with the registration documents), as well as the structural unit for which the statement is being drawn up (if there is one).

- Next, you need to enter the code according to the general classification of organizations and the number 70 in the “Corresponding account” column.

- Then the validity period of this statement is indicated, which must be at least 5 days from the moment of its signing (Regulation of the Bank of Russia No. 373-P dated 10/12/2011).

- It is imperative that the total amount accrued to employees for the calculated period be entered in the corresponding line of the first page of the payroll, both in digital and written form.

- After this, you must indicate the date of preparation of the payroll, as well as its serial number according to the internal document flow.

- The last thing that needs to be written on the title page of Form T-53 is the period for which the payment is made. Here you need to indicate specific dates.

Now visually:

Why do you need a payroll slip?

From January 1, 2013, it is not necessary to use this form (in accordance with Federal Law No. 402-FZ of December 6, 2011). However, it is quite convenient for optimizing accounting document flow.

Any payments made by the company must be recorded. This also applies to remuneration for work. If there are only a few employees, you can get by with incoming and outgoing cash orders. But in large organizations this is inconvenient.

The payroll form accumulates information on payments to all employees. This eliminates confusion and makes the accountant's work easier.

Filling out the second sheet

The size of the payroll directly depends on the number of employees working at the enterprise - the more there are, the longer this document will be. The number of payroll sheets must be indicated in the appropriate column.

- The first column of the main table of the statement is reserved for the serial numbering of employees.

- The second is for entering a personnel number (this data is stored in the personal cards of the organization’s employees).

- The third contains the full names of the salary recipients (it is better, in order to avoid possible confusion, to do this with a full decoding of the name and patronymic).

- In the fourth column, the enterprise accountant enters the amount of funds accrued for disbursement for each individual person (in numbers).

- In the fifth column, each employee must sign for receipt of wages.

- The sixth column is intended for entering references to documents for cash settlements (this could be powers of attorney, statements from employees, etc.) If there are no separate notes on employees, then this column can be crossed out.

In the line below the table, you must once again indicate in numbers and in words the total amount of funds accrued for issuance

Where can I find form T-53 and how to fill it out?

The unified form T-53 was approved by Decree of the State Statistics Committee of the Russian Federation dated January 5, 2004 No. 1. You can download it on our website:

The first page of form T-53 contains information about the company or individual entrepreneur and the structural unit. For the company indicate:

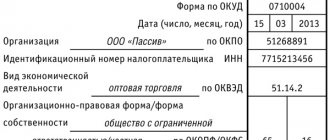

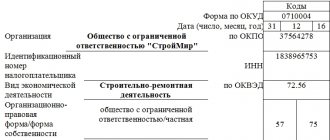

- OKPO code;

- corresponding accounting account (usually account 70, but for the examples given of payments to persons who are not employees of the company, it may be 75 or 76);

- limits of dates during which money must be paid (no more than 5 working days);

- total amount intended for payment (in words and figures);

- serial number of the payroll;

- date of preparation of the payroll;

- the period for which payments are made.

The page is certified by the signatures of the head of the company or individual entrepreneur and the chief accountant (if the company or individual entrepreneur has one).

The next page (or pages) is a table containing information about the recipients of money (personnel number and full name), amounts accrued for payment, as well as space for signatures and notes.

If money is received for someone by power of attorney, then information about the power of attorney is entered in the “Note” column opposite the name of the person to whom the money is intended. In this case, either the original one-time power of attorney or a copy of the power of attorney issued for a period of time, which can be used repeatedly, is attached to the payroll.

In case of failure to receive money within the 5-day period allotted for payment through the cash register, in the column intended for affixing a signature, opposite the name of the person who did not receive it, the entry “Deposited” is made.

The table ends with an indication of the number of sheets in it and the results of payments made. The total amounts of paid and deposited funds are given separately in words and figures. The signatures (with transcript) of the person who made the payment and the accountant who verified the specified data are affixed. The details of the cash disbursement order (number and date) are indicated by which the money actually paid according to this statement is issued from the cash register (clause 6.5 of the Bank of the Russian Federation instructions dated March 11, 2014 No. 3210-U).

A sample of a completed salary slip, as well as the nuances of filling it out, are given in the article .

Director's visa on form T-53

Without the signature of the head of the company, the T-53 payroll will not be considered valid, therefore, after filling out all its points and before transferring it to the cashier for issuing wages, the company’s accountant is obliged to submit it to the director for signature.

And one more signature will need to be placed after all funds have been paid to employees. The chief accountant of the enterprise will have to check the payroll and, if there are no violations, also sign it.

How to fill out the second sheet

The second page details payments for each employee. It contains a table of six columns:

- Sequential number (for the document).

- Employee personnel number (according to internal company records).

- FULL NAME. salary recipient.

- The amount due for his work at the end of the reporting period.

- Receipt or deposit mark.

- Notes (for example, for recipients' identification document numbers).

IMPORTANT!

When the money is issued, each employee must sign the salary payment form: the form without their signatures is invalid. The wording “Deposited” is provided in case the employee has not received the funds. Then the cashier must sign, confirming that he did not give out the money.

Next, you need to calculate the total amount due for payment and transfer it to the first sheet.

The sample payroll slip also contains information on the total amounts paid and deposited. These lines are filled in when the calculations are already completed.

Payroll for payroll

Form

Corrections in payroll

In general, according to the rules for filling out a payroll form T-53, the cashier, before starting to issue funds on the payroll, is obliged to check whether everything in it is drawn up correctly.

If any errors are found, then this document must be returned to the accounting department for revision.

But sometimes situations arise when, for some reason, it is no longer possible to reissue the payroll. In this case, inaccurate information must be carefully crossed out, the correct information must be written on top, and the correction must be certified by the signatures of all the same employees who signed the initial version of the statement. Here you need to indicate the date of correction. If everything is done in accordance with these recommendations, the document will not lose its legal force.

Payment statement. Filling out Sheet No. 2

Next, you need to fill out a table in which you need to fill in the employee data indicated in the table sequentially and line by line: the employee’s personnel number, his last name and initials, the amount of salary due in figures.

Further, when issuing wages to employees, each of them, upon receipt, puts a signature next to his last name, checking the amount received with that indicated on the payroll.

If some employees have not received their salaries, for example, due to absence for three days indicated on the title page, then the money must be handed over to the bank, and in column 5 the deposit of the amount must be noted. The employee will receive it later. (click to expand)

When the entire table is filled out, the employees have received their earnings, under the table you need to write the total amount issued and, if any, the deposited amount. The amount is indicated in words and in numbers in brackets. In the column “paid” the last name, first name and patronymic of the person responsible for issuing the salary are indicated.

Next, the document on the basis of which money was issued to employees from the cash register is indicated; this is an expense cash order: its number and date. That's it, the payroll is completed, you need to submit it for verification to the accounting department and for signature by management.

Next, the payroll must be registered in the payroll register, form T-53a. You can download this journal form from the link below.

| ★ Collection and directory of all personnel documents (forms and documents in word format) > 1200 books purchased |

To organize personnel records in a company, beginner HR officers and accountants are perfectly suited to the author’s course by Olga Likina (accountant M.Video management) ⇓

| ★ Author's course “Automation of personnel records using 1C Enterprise 8” (more than 30 step-by-step video lessons for beginners with instructions) purchased > 2000 practical courses |

How to close a payroll

This stage is the final one. After the payroll has expired (five days), the cashier must formalize its closure. Moreover, this must be done even if wages were not issued to all employees. To close the statement you need:

- Write the word “deposited” opposite the names of those employees who did not receive the money due to them according to this statement;

- Count the funds issued and those that were deposited. Enter this information on the last sheet of the statement;

- Confirm the statement with a signature;

- Write out a cash order. In it you need to write the amount of funds issued, then enter the order number in the statement.

After this entire procedure has been completed, the statement must be submitted again to the accounting department.

What forms to use

Both forms of documents are used if wages are paid in cash. For example, from the cash desk of an institution. If the company transfers money to employees’ bank cards, then T-49 and T-53 are not filled out. In this case, the accounting department draws up a document in form T-51. It is used to reflect accrued wages and other remunerations for labor in a specific billing period.

A payroll statement is prepared only to reflect the fact that money has been issued. The document does not contain any information about charges. But the settlement and payment system is more complex. It combines information about amounts paid (advance and salary) and information about accruals for the billing period. For example, the size of a specialist’s official salary, the number of days worked, incentive and compensation payments, territorial additional payments, etc.

Both documents are signed by the employee. The signature confirms the receipt of money (advance payment, bonus, salary, benefits) and specifies the payment period. Usually it does not exceed 5 working days. The specific deadline is approved by management. If during this period the money is not transferred to the employee, then the salary is returned to the bank. In other words, it is deposited. Receive deposited salary upon special application.

What if there are errors on the statement?

This document is a primary document, and therefore it is necessary not to allow corrections in it. If an error was made at the registration stage, the form is destroyed and a new one is issued.

According to the rules, the cashier must check for errors in the document before starting to issue it. If they are found, the form must be returned back to the accounting department.

However, a situation may arise when an error is detected already in the process of issuing funds according to the document. Accordingly, it will no longer be possible to destroy the form and collect all the necessary signatures on a new one.

In this situation, you need to carefully cross out the incorrect information with one line and write the correct information on top. Crossing out must be done so that the old data is easy to read. The correction is certified by the manager and the chief accountant with their signatures.

Attention! In addition, it is recommended to draw up an accounting statement in which you describe in detail how the error was identified and justify its correction.

First page

The first sheet is the title page - it reflects basic information about the employer, the period of payment of wages and its total amount.

Payroll, first page

The following details should be provided here:

- Name of the organization, as well as the structural unit , if the form is filled out only in relation to its employees. Indicated according to the constituent documents, you can add an abbreviated form.

- OKPO code . The number was assigned by Rosstat and is contained in the information letter.

- Corresponding account . Usually this is account 70 “Settlements with personnel for wages”.

- To the cashier for payment on time . Here you should indicate two dates - the current one and the last one for making the salary payment.

- Sum . The total amount that is transferred to pay wages is indicated. The amount is written first in words and then in numbers.

- Document number and date of its preparation.

- Billing period. These are the first and last days of the period for which wages are accrued.

Also on the first sheet are the signatures of the head of the organization and the chief accountant, if there is one in the organization.