Who is entitled to compensation for unused vacation?

When an employee leaves the company, most often he has “non-vacation” days of vacation. The accountant calculates the amount of these conditional vacation pay according to special rules, withholds personal income tax and pays it along with the last salary and severance pay.

No compensation is paid to employees who are simply transferred from one department to another without being fired. It is also not issued to external part-time workers who are transferred to their main place of work. And an employee who was hired less than half a month ago and is now being fired will not receive anything.

Amount of severance pay and payments for the period of employment in 2019

Severance pay is a special type of payment that is due to employees after termination of an employment contract with the employer and other cases of termination of cooperation. Not every employee can receive such payments, since this requires fulfillment of certain conditions. This includes:

- Liquidation of company;

- staff reduction;

- if an employee refuses to be transferred to work in another area;

- the presence of medical conditions that prevent the performance of duties;

- loss of performance;

- refusal to work due to changes in working conditions.

How to calculate average daily earnings

Average daily earnings for the 12 months before dismissal are needed to find out the amount of compensation for the remaining days of vacation. If an employee joined the organization less than a year ago, calculate the average salary from the moment he was hired (Government Decree No. 922 of December 24, 2007).

We add up the amounts of earnings for the required period: this includes income in cash and in kind - salary and additional payments, bonuses, allowances. The amount does not include sick leave, vacation pay and other payments, for the calculation of which average earnings have already been used.

Next, we determine the number of calendar days for the period and consider working months:

- if the employee worked a full month, we take the average number of calendar days in it - 29.3;

- if there were missed working days in a month (vacation or sick leave), then we find the number of days using the formula: (Number of calendar days of the month - Days of vacation or sick leave) * 29.3 / Number of calendar days of the month .

Now let’s find the average daily earnings using the formula: Amount of payments for the billing period / Calendar days for the billing period .

Examples of calculating severance pay and lump sum compensation

Let's consider the procedure for calculating payments due to an employee both when staffing is reduced and when a company is liquidated.

Example 1. Calculation for staff reductions: severance pay

In connection with the reduction in the number of personnel of loader Ermolaeva A.A. fired on August 17, 2020 with severance pay for 1 month of employment. 09.29.2020 Ermolaev A.A. got a new job.

Initial data:

- for August 2019-July 2021, payments in favor of the employee amounted to 322 thousand rubles, incl. the amount of vacation pay is 26 thousand rubles;

- working days in the period - 247 (a chain of food stores, outside the scope of Presidential Decrees), of which 20 working days were worked for annual paid leave.

Let's make the calculations:

| Let's determine the average daily earnings | (322,000 – 26,000) / (247 – 20) = 1,303.96 rubles. |

| Let's find the number of working days falling on the 1st month of job search | From 18.08 to 17.09.2020 – 23 working days |

| We will calculate the payment for 1 month of employment | 1,303.96 x 23 = 29,991.08 rub. |

| 10/02/2020 Ermolaev A.A. applied to the former employer for payment of severance pay for part of the 2nd month of employment (from 09.18 to 28.09.2020 - 7 working days) | 1,303.96 x 7 = 9,127.72 rubles. |

| The result of calculating severance pay in case of staff reduction 2021, paid to the loader by the former employer for the period from the date of dismissal to the day of employment | 29,991.08 + 9,127.72 = 39,118.80 rub. |

The amount of payments upon liquidation of an organization is determined similarly.

Example 2. Calculation upon liquidation: one-time compensation

Due to the liquidation of an organization operating in the Kamchatka Territory (one of the regions of the Far North), all employees are fired on August 24, 2020.

The employer decides to pay one-time compensation in the amount of 5 times the monthly salary to everyone.

Let's carry out calculations using the example of one of the employees:

- for August 2019-July 2021, payments in favor of the employee amounted to 456 thousand rubles;

- working days in the period - 247 (continuously operating enterprise, outside the scope of Presidential Decrees).

Let's calculate the amount of compensation:

| Let's determine the average daily earnings | 456,000 / 247 = 1,846.15 rubles. |

| Let's find the number of working days to calculate the average monthly earnings for 1 month of employment | from 25.08 to 24.09.2020 – 23 working days |

| Let's calculate the average monthly earnings for the first month of employment | 1,846.15 x 23 = 42,461.45 rubles. |

| One-time compensation of 5 times the average monthly salary | 42,461.45 x 5 = 212,307.25 rubles. |

Until the liquidation of the enterprise, the employee will be paid 212,307.25 rubles.

Lump-sum compensation for dismissal due to staff reduction is calculated in a similar manner.

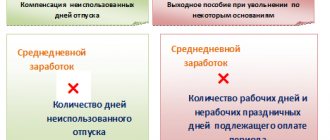

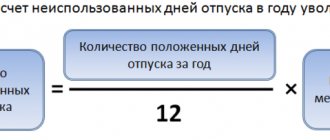

How to calculate compensation for unused vacation

First, understand how many days of the allotted vacation the employee did not take off. We provide a detailed algorithm for calculating this figure here. And in simple cases, when an employee is entitled to 28 vacation days per year, 2.33 vacation days accumulate in a month. If in some months a person worked less than 15 days, we exclude these months from the calculations; if more than 15 days, we round up to a full month. Add the number of months and multiply it by 2.33. From the resulting number, we subtract the days that the employee has already “taken off.”

Calculate the amount of compensation using the formula: Amount of compensation = Average daily earnings * Number of days of unused vacation .

Types of payments and compensations

Labor legislation is complex: it is full of reservations and separate articles for fixed-term contracts, part-time work, seasonal work and activities in the Far North. Therefore, below we have focused only on general cases - they are relevant to the majority of Russians working under an employment contract in the 5/2 schedule.

Remaining salary

This payment is the main one. The employee is required to return the entire amount that he earned before dismissal. In addition to salary, this includes bonuses and additional payments provided for in the employment contract. The specific terms of such payments are determined by the company, but they are required to be paid to the employee strictly on the day of dismissal.

Vacation compensation

By law, every Russian is entitled to a vacation of 28 calendar days, each of which is paid. It happens that before dismissal, an employee does not have time to arrange and spend vacation. In this case, the company pays compensation - strictly for the number of vacation days that were not used.

Sick leave after dismissal

If, within a month after dismissal, an employee took sick leave, but did not find a job in another place, the former employer is obliged to compensate him for sick days. Few people know about this payment, so most often Russians receive treatment using their savings. But the Labor Code stipulates that even the unemployed can receive sick leave if the dismissal occurred recently.

There is a nuance regarding the size of payments. If illness occurs at least a day after dismissal, sick leave will be paid in the amount of 60% of the average salary (regardless of the length of service). If sick leave is opened on the day before dismissal, 100% is paid.

Indexation of average earnings with salary increases

If before or during an employee’s vacation the organization increased salaries (tariff rates), then it is necessary to index the average earnings to calculate vacation pay. This is where the increase factor (KPI) comes in handy: KPV = OH / OS, where OH is the new salary, OS is the old salary. There are three indexing options:

- The salary increased during the pay period. Then all payments taken into account when calculating vacation pay from the beginning of the billing period to the month of salary change are multiplied by the KVP.

- The salary increased after the pay period before the start of the vacation. The entire calculated average earnings are multiplied by the increase factor.

- Salary increased during vacation. Only part of the vacation pay increases, starting from the effective date of the new salaries.

How to calculate wages for laid-off workers in 2021

The salary upon dismissal takes into account:

Accrued funds for days worked.

Monthly bonus proportional to the number of working days.

Overtime (night shifts, overtime, work on weekends or holidays).

Payment for combination.

When calculating the wages due to an employee upon dismissal, an accountant or personnel officer must adhere to a certain algorithm of actions:

The first thing you need to do is draw up an accounting sheet in form T-13. Many accountants recommend creating a separate time sheet for the dismissed employee (from the moment the resignation letter is written).

This document records all working days, days of rest, business trips, vacations and sick leave. The signed time sheet is agreed upon with the employee’s supervisor and endorsed by an employee of the HR department.

The time sheet, drawn up in accordance with the requirements, is transferred to the accounting department of the enterprise.

The amount to be issued is calculated using the following formula:

Salary to be paid = "(salary + bonus, month + other payments) / number of workers. days. per month * no. of work days

This formula is used in standard calculations when the employee did not go on vacation or was on sick leave during the month of dismissal.

Important: voluntary dismissal entails two guaranteed payments: wages for the time actually worked and compensation for unused vacation. Termination of an employment contract by mutual consent of the employee and the employer also provides for the payment of severance pay (provided that this is specified in the text of the employment contract).

Vacation pay

Vacation pay must be paid at least 3 days before the start of the vacation (Article 136 of the Labor Code of the Russian Federation). We take the number of vacation days from the management’s order to provide legal vacation. We pay for all calendar days of vacation except non-working holidays (according to Article 120 of the Labor Code of the Russian Federation).

The situation usually raises questions when vacation starts at the beginning of the month. For example, an employee goes on vacation on July 1, 2018, and vacation pay must be paid on June 27. In this case, the calculation requires the salary for June, which has not yet been accrued.

In this case, the salary calculation for June is first performed: either assuming that the employee will work the last days of the month, or based on the days already worked. Vacation pay is then calculated. If the salary for June changes after calculating vacation pay, you will need to recalculate and pay extra or withhold the difference.

You can calculate your vacation pay in a few minutes using our calculator.

Basic rules for calculating compensation upon dismissal

In accordance with Art. 140 of the Labor Code of the Russian Federation, payment of benefits to a dismissed employee must be made on the last day of his stay in his current position or on the next day after his departure from the enterprise. But the calculation of compensation itself using a single calculator upon dismissal must occur in compliance with certain rules:

- Salary is calculated based on the hourly rate;

- When calculating the salary amount, the employer is obliged to take into account all overtime of the citizen, his bonuses and allowances;

- When calculating compensation for unused vacation, management is obliged to pay the subordinate a period of at least 28 days per 1 working year;

- For disabled people and employees with irregular schedules, as well as workers serving in difficult conditions, the minimum period of legal leave is 30-35 days;

- If in the last two or three years before dismissal the employee has never gone on vacation, then for all this time he is entitled to financial compensation;

- For people who were dismissed from their position earlier than a year after drawing up the employment contract, benefits are calculated by month, not by hour;

- Holidays, absenteeism due to the fault of the employee and unpaid vacations lasting up to 2 weeks are not considered a working period.

Taking into account the listed rules for calculating compensation, the employer will be able to establish the exact amount of payment for a specific subordinate. If an error is discovered in the calculations, the employee has the right to file a lawsuit against the boss in the local judicial authority.

Calculation note upon dismissal (form T-61)

Home / Personnel documents

| Table of contents: 1. Instructions for filling out form T-61 2. Charges when calculating average earnings 3. Other deductions upon dismissal of an employee | Document: Download form T-61 View sample filling T-61 |

A settlement note upon dismissal is a document intended for calculating funds due to an employee for time worked and unused vacation days.

Form T-61 is filled out by different departments of the company:

- 1st – front side – by an employee of the personnel department;

- 2nd – reverse side – by the company’s accounting service.

If there is neither a personnel officer nor an accountant, then the form is completely filled out by the individual entrepreneur / head of the organization or another authorized person.

Form T-61, starting from January 1, 2013, is not mandatory for use. A company can use a document developed independently. But for this it is necessary that it contains the details provided for by the law on accounting and that it be approved by the manager.

Instructions for filling out form T-61

Front side

Name of company

It should be included here in full, without abbreviations. This procedure is established by Decree of the State Standard of the Russian Federation dated March 3, 2003 No. 65-Art. It also clarifies that if the constituent documents contain an abbreviated name of the company, it may be indicated below the full name (or next to it in parentheses).

The above document is valid only until 07/01/2018, and then GOST R 7.0.97-2016 will come into force, but it also contains the same requirement regarding the name as a document requisite.

All the above rules fully apply to individual entrepreneurs.

OKPO code

This is a digital code of an organization according to the all-Russian classifier, which gives a general idea of the industry of its activity. It is assigned to all organizations (eight-digit) and individual entrepreneurs (ten-digit) upon registration with the local statistics office.

In documents for internal use, indicating the OKPO code is not mandatory, so it is often not included (this follows from Rosstat Order No. 221 dated March 29, 2017)

Previously, the code on paper was issued only directly from the statistical authorities. Today, to find out, you can use online services.

For example, at https://kodyrosstat.rf there is an option that allows you not only to see OKPO, but also to print the notification yourself.

Field “Employment contract”

The number indicated in the employment contract between the organization and the dismissed employee, and the day on which it was concluded, is indicated.

Number and date of document preparation

Numbering can be assigned in a serial number throughout the entire period of operation of the organization, individual entrepreneur, or start anew every year. You can also use the number of the dismissal order as the number of the settlement note.

Personnel Number

This number is assigned when applying for a job. It is affixed to all personnel (personnel orders, personal files, time sheets) and accounting (payroll and pay slips, expense reports) documents.

The number is given once for the entire duration of the employee’s work. Since the legislator does not require a personnel number, the field is filled in if available.

Structural subdivision

If there are no such divisions in the organization, then the line is left blank.

Employee position

We put the name of the position, which is indicated in the staffing table and the employment contract.

Line “Employment contract terminated...”

The date of termination of the employment contract is taken from the dismissal order and corresponds to the employee’s last day of work.

But there are cases when the employee was actually absent from the workplace, but, in accordance with the labor code or federal law, his place of work was retained.

So, according to Art. 127 of the Labor Code of the Russian Federation, unused vacations are provided to the employee upon his application with subsequent dismissal. Then the day of dismissal is the last day of vacation.

According to the law of June 12, 2002 No. 67-FZ on guarantees of the rights to participate in a referendum, a member of the commission retains a place of work for the period of elections and their preparation. The day of dismissal in this case will be the last day of work on the commission.

The grounds on which the employment contract was terminated

Termination of an employment contract can be carried out only on the grounds provided in Article 77 of the Labor Code of the Russian Federation. The reason is entered in the dismissal order and in the employee’s work book.

The wording must correspond exactly to that specified in the Labor Code of the Russian Federation, with reference to the article. For example, “The employment contract was terminated due to the transfer of the employee, at his request, to work for another employer, paragraph 5 of part one of Article 77 of the Labor Code of the Russian Federation.”

Next is the date and number of the document according to which the employee was dismissed (order or instruction from management).

Below are marks about how many days of vacation were not used, and whether there were any days that the employee took off in advance. In the second case, such days will be removed from the calculations. If there are no such days, dashes are added.

At the end, the name of the position of the personnel employee (authorized person, individual entrepreneur), his signature and the date of signature are indicated.

Section "Calculation of vacation pay"

To fill out a calculation note regarding the reflection of the resigning employee’s salary, data from the payroll (T-51), payroll (T-53) or payroll (T-49) statements about accrued and paid wages, bonuses, and other funds are used.

| Count | Indicated |

| 1 | The year for which vacation payments are calculated. |

| 2 | 12 months (calendar) preceding dismissal. |

| 3 | The amounts of money that are accrued to the employee monthly are taken into account when calculating average earnings (see the section below “Accruals taken into account and not taken into account...”). |

| 4 | The number of days included in the billing period per year. If the month was worked in full, then the number of days in it for calculating average earnings will be equal to 29.3. Therefore, for the entire period the number of days will be 29.3 x 12 = 351.6. If the month is incomplete, you need to apply the algorithm: (29.3 days: number of days in the month) x number of days worked. |

| 5 | Working hours related to the billing period are indicated when a summarized time recording is established for the employee. |

| 6 | Amounts of average daily or average hourly earnings. To calculate them, you need to divide the total amount of earnings from column 3 by the number of days from column 4 (or hours from column 5). |

| 7 | Vacation days that the employee used in advance. |

| 8 | Vacation days that the employee did not have time to take off. |

| 9 | Payments due to an employee for unused vacation days. They are calculated as follows: Average daily (average hourly) earnings (column 6) x (used vacation days (column - unused (column 7). They are calculated as follows: Average daily (average hourly) earnings (column 6) x (used vacation days (column - unused (column 7). |

Section "Calculation of payments"

| Count | Indicated |

| 10 | The amount of salary accrued for the last working month (column 2). In the sample this is April 2017 |

| 11 | Accrued vacation amounts (column 9). |

| 12 | Other accruals, which include those that do not participate in the calculation of environments. earnings. |

| 13 | The result obtained by adding the sums from columns 10,11,12. |

| 14 | The amount of income tax accrued on the funds indicated in column 13. |

| 15 | Deductions, except for personal income tax deductions (discussed in more detail below in the table). |

| 16 | The total amount of due deductions (column 14 + column 15). |

| 17 | The company's debt to the employee may include, for example, income tax withheld excessively from him, deposited wages not received by him on time, and overexpenditure on the advance report. |

| 18 | Debt owed to the employee is those amounts that are not included in column 15. |

| 19 | The amount to be paid after deductions, consisting of the result of the following calculation: Box 13 – Box 16 + Box 17 – Box 18. |

Under the second table, the amount to be paid is indicated in words and numbers. After the resigned employee receives the money due, the details of the payroll or expense order are indicated.

At the end of the settlement part of the T-61 note, the accountant puts his signature and indicates its decoding.

Accruals taken into account and not taken into account when calculating avg. earnings

When calculating compensation for unused vacation days, it is necessary to take into account only those payments that are provided for by the regulations on the procedure for calculating the average salary (Resolution of the Government of the Russian Federation of December 24, 2007 No. 922).

| Are taken into account | Not taken into account |

|

|

* An exception is payment for breaks provided to the mother for breastfeeding.

Please note: the time for which the payments indicated in the table are not taken into account is excluded from the calculation period when determining the average earnings upon dismissal, and weekends and holidays on which the employee worked are taken into account in the general manner.

Other deductions upon dismissal of an employee

In addition to the considered mandatory withholdings of income tax and vacation pay received in advance, there are other withholdings that are indicated in form T-61 in the calculation of payments in column 15 (Withholdings, except withholdings of personal income tax) and column 18 (Debt due to the employee).

Types of deductions from an employee’s earnings upon dismissal, provided for in columns 15 and 18:

| Kinds | Holds | Percent |

| Mandatory by law | According to executive documents:

| No more than 50% |

| At the initiative of the employer company | Reimbursement of unearned advance payments Unspent and unrefunded travel allowances Overpaid funds due to accounting errors Damage caused by the employee to the organization | No more than 20% |

| According to a statement written by an employee | Voluntary insurance contributions:

Union dues Funds to repay loans, credits and interest on them Amounts intended for charitable foundations | 100% |

Please note: deductions initiated by the employer and related to the repayment of the employee’s debt to the organization can be made only in those cases contained in the Labor Code and other legislative acts.

Did you like the article? Share on social media networks:

- Related Posts

- Order for employment (form T-1 and T-1a)

- Order on sending on a business trip (form T-9 and T-9a)

- Sample of filling out form T-61

- Sample of filling out form T-54

- Employee personal card (form T-2)

- Certification sheet for the case

- Sample of filling out form T-7

- Vacation schedule (form T-7)