Bank commission: grounds for its calculation

The basis for charging commissions are agreements for maintaining a current account, servicing a deposit or issuing a loan. Within the framework of these agreements, the terms of the relationship between the organization and the bank are stipulated.

The following list of services for which commissions are paid can be distinguished:

- Ongoing maintenance of the current account with subsequent installation and maintenance of the Client-Bank program.

- Cash collection.

- Transactions of purchase and sale of foreign currency.

- Providing and maintaining a credit line.

- Property management on a trust basis.

- Rent of deposit boxes.

- Use of leased property.

For each type of banking services provided to the client, a separate agreement is drawn up, which details the conditions for the provision of these services, the amount and procedure for paying the bank commission.

Reflection of bank commissions on accounting accounts

In accounting, bank commissions can be displayed in two ways:

- The first method is based on the use of current accounts 60 or 76 with the corresponding sub-account “Settlements with the bank”. Both of these accounts are suitable for accounting for banking services - the procedure for their use can be regulated in the accounting policy of the enterprise.

- The second method is more practical, since the commission is displayed without “intermediate” accounts, but directly to account 91.

Please note, according to the instructions for using the chart of accounts, correspondence of 91 accounts does not provide for payment for the services of credit institutions.

In practice, the second method of accounting for banking services is most often used.

A check sheet for closing an account under Federal Law 115 at the client’s initiative.

Before deciding to close your current account, weigh the pros and cons .

Find out whether the commission will be removed from the account balance when closing the account under Federal Law 115. Or will they charge you at the same rate as for a regular operation?

Estimate the amount that is stuck in your account. If it is very insignificant, then great! If it’s large enough, then think about the possibility of spending it in such a way that the bank will allow it.

To do this, you can try using the following mechanisms:

- paying taxes for yourself. Pay a tax that is not present in your activities, then write an application for a refund from the budget.

- payment of tax for a third party to pay off accounts payable to a counterparty.

- court order, writ of execution.

- return back to the counterparty.

If you can use one of the above methods, then do it and leave. When you close an account with a new bank, you are guaranteed that nothing will come to you.

When deciding to close a bank account agreement with or without deducting a commission, remember that when transferring, the bank may make an entry in list 639-P, which will have to be contested in the future.

Follow the following rules for closing an account under Federal Law 115. Tips for closing an account under Federal Law 115.

- If, when closing an account under Federal Law 115, the bank asks you to sign an agreement to terminate the contract and agree to the commission charged, do not be surprised. In the document, add that you do not agree with the commission, all documents during the audit under 115 Federal Laws were submitted in full and on time. Save this document for legal proceedings.

- When notifying the bank that your account is closed, you are not required to use its form. You can terminate the contract by creating a document yourself, in free form. This way you will avoid unnecessary legal language that could be used against you later.

- A notice of closure of a bank account must be sent either by registered mail with a list of attachments, or by official courier delivery. You can also take the notice to the bank yourself. But then, perhaps, they will not want to accept it and will try to impose their form with formulations that are unnecessary to you. Therefore, sending by mail or courier is most acceptable in this situation.

If the bank nevertheless charged a commission when closing an account for failure to provide documents during an audit under Federal Law 115, and if in your opinion this is unfair, then write a complaint to the bank and the Central Bank.

Despite the fact that such a complaint is unlikely to serve as a basis for a refund, this step is necessary for the further appeal procedure in court. And do not forget to collect from the Bank:

- interest for illegal use of funds;

- losses (in full) incurred by the business due to the fault of the bank: penalties, fines from counterparties;

- costs for lawyers, attorneys, etc.

I really like how some courts argue for the illegality of removing such a commission:

... Law No. 115-FZ, as well as other federal laws, does not contain provisions allowing , as measures to combat money laundering, to establish a special commission in an increased amount . Collection of commissions for transactions with funds related to the legalization (laundering) of proceeds from crime and the financing of terrorism is not a form of control.

At the same time , the commission, when closing an account for the client’s failure to provide or incomplete submission of documents requested by the bank, is withheld not at the time of making controversial transactions and qualifying them as “doubtful” by the bank, but when closing the account at the request of the client and transferring the balance of funds to the plaintiff's current account in another bank. Meanwhile, counteraction to illegal financial transactions should be carried out at the stage of execution by the bank of the client’s order to carry out the corresponding operation .

In this case, the bank’s actions to close the account were not an independent banking service that created any additional benefit for the client within the framework of the disputed agreement. The bank has not proven the incurrence of any expenses and losses in connection with the client’s failure to provide documents requested by the bank, subject to compensation by charging a disputed commission (Article 65 of the Arbitration Procedural Code of the Russian Federation).

Decision of August 7, 2021 in case No. A65-14967/2019 Arbitration Court of the Republic of Tatarstan (AC of the Republic of Tatarstan)

Resolution of the Arbitration Court of the Ural District dated August 6, 2019 in case No. A60-50470/2018

However, there is another position when the client loses in the courts, for example, Resolution dated July 22, 2021 in case No. A40-277186/2018 Arbitration Court of the Moscow District (FAS MO):

...The courts found that based on the results of monitoring transactions on the plaintiff’s current account and interaction with the client bank, a set of signs of the use of the account for dubious transactions was identified, namely: the transit nature of payments, the minimum tax burden, signs of fictitious activity, the presence of negative information giving grounds assume a high risk of servicing the client and the risk of the bank being involved in conducting dubious transactions on behalf of the client.

The courts found that the bank, in order to confirm the validity or refute the assumptions that had arisen about the implementation of dubious transactions on the client’s account, sent a request to the company to provide documents that are the basis for making payments, as well as information relating to the client’s activities and explaining the economic meaning of the transactions being carried out however, the requested package of documents was not submitted by the company , which did not allow the bank to confirm the economic meaning of the operations and their compliance with the declared activities; The client did not apply to the bank to extend the deadline for submitting documents .

Based on the foregoing, the courts came to the conclusion that the fact of unjust enrichment of the defendant at the expense of the plaintiff and the existence of conditions for its recovery from the defendant on the basis of Article 1102 of the Civil Code of the Russian Federation was not confirmed, since, as the courts established, the disputed commission was reasonably collected by the bank for performing a banking transaction. operations and provision of banking services for transferring the balance of funds when closing an account to a client for whom measures have been taken under Law No. 115-FZ.

Accounting entries for bank commissions

| Account Dt | Kt account | Transaction amount, rub. | Wiring Description | A document base |

| Postings to the bank when using an “interim” account 60/76 | ||||

| 60 (76) | 51 | 1 450,00 | A bank commission has been debited from the company's current account (date of debit from the account) | Bank agreement, bank statement |

| 91-2 | 60 (76) | 1 450,00 | Bank commission is included in expenses | Bank agreement, bank statement |

| Bank commission is subject to VAT | ||||

| 60 (76) | 51 | 5 000,00 | Bank commission (including VAT) is written off for credit servicing | Bank agreement, bank statement, invoice |

| 19 | 60 (76) | 762,71 | VAT charged | Check |

| 68 | 19 | 762,71 | VAT displayed | Check |

| 91-2 | 60 (76) | 4 237,29 | Bank commission is included in expenses (excluding VAT) 5000 – 762.71 = 4237.29 | Bank agreement, account |

| Bank commission – “direct” display method | ||||

| 91-2 | 51 | 8 700,00 | Bank commission written off | Bank agreement, bank statement |

| Uniform write-off of bank commissions (within clearly defined time frames) | ||||

| 60 (76) | 51 | 9 450,00 | Bank commission paid (date of transfer) | Bank agreement, bank statement |

| 97 | 60 (76) | 9 450,00 | Inclusion of paid commission into deferred expenses (by date of transfer or evenly) | Banking agreement. Order on the accounting policy of the enterprise |

| 91-2 | 97 | 9 450,00 | Bank commission is included in expenses | Order on the accounting policy of the enterprise |

| If in tax accounting this commission is recognized as an expense at a time, and in accounting - evenly over a specified period, then a deferred tax liability arises | ||||

| 68 | 77 | 1 890,00 | Deferred tax liability accrued9450 * 20% (income tax) = RUB 1890. | Accounting certificate-calculation |

| 77 | 68 | 1 890,00 | Reducing deferred tax liability (we uniformly reduce the amount of bank commission accrued in the current period on account 91-2) | Accounting certificate-calculation |

| Retention of bank proceeds credited through the POS terminal | ||||

| 60 (76) | 90-1 | 35 000,00 | Revenue deposited through the POS terminal is displayed | POS terminal control tape |

| 90-3 | 68-VAT | 5 338,98 | VAT is charged on the sales transaction | POS terminal control tape |

| 91-2 | 60 (76) | 630,00 | There is a fee charged for servicing the POS terminal. | POS terminal control tape, agreement |

| 51 | 60 (76) | 34 370,00 | The proceeds received through the POS terminal (minus bank commission) 35,000 – 630 = 34,370 rubles are credited to the company’s current account. | Electronic journal, bank statement |

Reflection of bank commission in accounting

The basis for recording transactions for the payment and return of bank commissions is the banking services agreement. Funds are debited from the company's account to pay commissions according to Dt 76 “Settlements with various debtors and creditors.”

Let's try using examples to understand typical transactions for paying a commission to a bank.

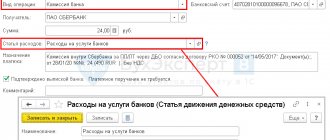

Bank commission for collection services and cash settlement services (RCS)

Imperator LLC entered into agreements with the bank for the provision of the following services:

- installation of the Client-Bank system in the amount of 43,000 rubles. excluding VAT (one-time payment);

- monthly support of the Client-Bank system in the amount of 3,200 rubles. excluding VAT (monthly payment);

- collection of funds in the amount of 6,200 rubles, VAT 945 rubles. (one-time payment);

- RKO in the amount of 800 rubles. excluding VAT (one-time payment).

This is interesting: Income tax benefit for medical institutions 2021

The accountant of Imperator LLC will reflect the following transactions:

Payment of bank commission under a foreign exchange agreement

The following entries will be made in the accounting of Rodina LLC:

Refund of bank commission

LLC "Slava" erroneously wrote off expenses and transferred funds for cash services to the bank in the amount of 850 rubles. After identifying the fact of overpaid funds, the bank returned the money and credited it to the bank account of Slava LLC.

In Slava LLC, transactions were reflected as follows:

| Dt | CT | Description | Sum | Document |

| 76 | 51 | Erroneous transfer of commission for cash settlement services | 850 rub. | Payment order |

| 51 | 76 | Refund by the bank of overpaid funds | 850 rub. | Bank statement |

| 76 | 91 | Adjustment of previously recorded expenses (reversal) | 850 rub. | Accounting information |

The main thing to remember when recording a bank commission transaction in accounting is strict compliance with the terms of the agreement regarding the terms and amount of payment.