Payment "for the wrong thing"

Let's look at the most insidious mistakes. For example, the purpose of the payment is incorrect, that is, the name of the goods or services is incorrect. Buyers clearly indicate the wrong name of goods or services on the payment order. For example, instead of “payment for installation” - “rent”. Sometimes instead of “ and vice versa. For example, they transfer money for the transportation of goods, but in the payment slip they indicate “payment for tools.” The larger your company, the higher the risk. And it’s really bad if the name of the goods for which the bank tracks cash withdrawals is mistakenly indicated. For example, a company receives payment for building materials. And he writes off money from the account mainly with the purpose of payment “for food products”, “rent of commercial equipment”. The bank will ask for clarification and may block the client-bank connection. In this case, it will refer to the Methodological Recommendations approved by the Central Bank of the Russian Federation on July 21, 2021 No. 18-MR.

And after comparing payment receipts with the company’s OKVED codes, bankers may be interested in a situation where the main receipts into the account are not related to the company’s activities. Sometimes questions arise from one-time payments, especially for large amounts. For example, if a wholesale company received payment for advertising services. And if deposits with an incorrect payment purpose become regular, suspicions will turn into confidence.

To reduce the likelihood of errors, it is better to include the text in the invoice that must be indicated in the purpose of payment. If your counterparty nevertheless manages to transfer money to you “for the wrong reason,” immediately inform him about it and try to get a written response in which the buyer confirms the correct purpose of the payment. You will forward this correspondence to the bankers if they have any questions.

Errors in the names of goods and services will also interest tax authorities. In this sense, such mistakes are especially risky for “simplifiers” and “imputers”, as well as entrepreneurs on the PSN. If the tax authorities see in the statement receipts for goods or services that do not fall under the special regime, they will demand that taxes be paid according to the general system. You will have to prove that the company or individual entrepreneur conducts only activities that fall under the special regime (Resolution of the Arbitration Court of the Volga District of October 25, 2021 No. F06-26038/2017). Therefore, for large payments, it is safer to agree with the supplier on the correct name of the goods.

But it is best to indicate the specific name of goods, works or services on the payment slip (Appendix No. 1 to the Central Bank Regulations dated June 19, 2012 No. 383-P). Take it from the contract, invoice or specification. If there are a lot of products, you can indicate a generic name, for example, “office supplies.” Or indicate the goods that make up the largest share of the purchase price.

If any errors are made in a payment order, the tax is considered unpaid

There are errors that can be corrected, but tax obligations are considered fulfilled and no penalties will be applied. But there are errors in filling out payment slips, the consequences of which are more serious, and most importantly, the tax is not considered paid (accordingly, fines, penalties or other penalties will appear, especially significant for legal entities).

So, a tax or fee is considered unpaid if:

- Incorrect indication of the payee's account. The money will not be transferred to the budget of the Russian Federation, or it will go to the Federal Treasury account, to which the money was not supposed to be sent;

- Incorrect bank name. The same consequences as if you incorrectly indicate the recipient's account;

- Incorrect indication of the Federal Treasury account or bank name due to the fault of the bank. The consequences are similar to the first two points. Despite the fact that the bank employee is guilty, the taxpayer will be punished for non-payment of tax, and in due time he has the right to make claims against the bank and demand payment of compensation.

The insidiousness of numerology

The next point in our program is the inaccurate contract or account number. It will cause particular suspicion when purchasing goods from suppliers that inspectors consider to be at high risk. However, it is possible to make excuses. If the mere fact of an inaccurate contract or invoice number does not mean that the inspectors will consider the expenses unpaid. Provided that it is possible to determine which expenses the payment actually relates to. Confusion is possible if a company has several agreements with a counterparty. So it’s safer to indicate a specific contract or account number on the payment slip.

For example, a company has two contracts with a buyer. He must transfer payment for goods shipped under one contract. But he indicated the details of another agreement in the payment slip. It is not necessary to specify the purpose of the payment if it can be identified. That is, the receiving company can determine which contract and invoice the payment actually relates to. For example, if the buyer missed a digit in the invoice number.

If buyers often make mistakes in the purpose of payment, you can create a register. Indicate in it which payment purpose is correct. The register will come in handy if the bank requests an agreement or account specified in the payment order.

Is it possible to challenge a payment change?

Sometimes the recipient of the money does not agree with the changes made by the payer. Unfortunately, it is quite difficult to challenge a letter of clarification. This must be done in court. It is advisable to resolve the problem through negotiations.

When making changes to the purpose of payment, you must remember that such transactions are carefully reviewed by regulatory authorities. If the Federal Tax Service sees signs of tax evasion in such letters, then claims may be made: additional taxes and penalties will be assessed. The most common issue that arises is prepayment under a supply agreement, which is later reclassified as a transfer under a loan agreement. This clearly shows a way to avoid paying VAT on the buyer's advance payment, and questions from the tax inspectorate are inevitable.

Drafting for the bank

Also, if errors are detected, a letter is sent to the servicing bank. The message form is arbitrary. The letter is signed by the persons whose autographs were on the incorrect document.

To make changes to the purpose of the payment, the number of copies of the letter must be 4: the first remains with the applicant, the second with the payer's bank, the third with the recipient's bank, and the fourth with the counterparty.

The letter is drawn up by the enterprise that transferred the monetary assets. As a rule, accounting department employees have access to prepare such a document. The letter is subject to mandatory registration.

Example for the Federal Tax Service

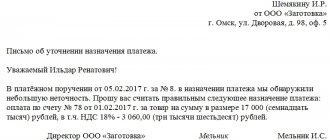

Letter to clarify the purpose of payment

“Smena LLC”, when transferring funds to the supplier Trud LLC under agreement No. 125, in the purpose of payment of payment order No. 56 dated December 10, 2019, the phrase “Including VAT 18%” was incorrectly indicated. Trud LLC applies a simplified taxation system and does not pay VAT. Please make changes to the purpose of payment and replace it with the words “Without VAT”. A copy of the payment document is attached.

Director of Smena LLC Petrov P.P.

15.12.2019

Incorrect VAT rate

Now, during the transition period, due to the increase in VAT, buyers confuse the rate in their payments - they reflect 18% instead of 20% or vice versa. In this case, a letter stating that there is an error in the payment may not be required from the counterparty. The main thing is to calculate VAT at the correct rate. That is, if you shipped goods to the buyer in 2021, apply the new VAT rate - 20%, even if in the payment slip the buyer mistakenly indicated the previous rate and the amount of tax calculated based on 18% (clause 4 of article 5 of the Federal Law of August 3 2021 No. 303-FZ).

note

Recently, bankers, in accordance with the instructions of the Central Bank of the Russian Federation, have taken payment for such goods as cars and spare parts, medicines, tobacco products, vegetables, fruits, confectionery and other food products under close “anti-money laundering” control

If the buyer made a payment for goods shipped in 2018, you should have calculated VAT at a rate of 18%. There is no need to make any recalculations on the payment date. This also applies to the situation where the buyer mistakenly indicated a 20% rate on the payment order.

In general, such an error in the payment order does not entail tax risks for the buyer. But it is worth checking that the supplier has indicated the correct VAT rate on the invoice. If he confuses the rate, the inspectors will refuse the deduction (Clause 2 of Article 169 of the Tax Code of the Russian Federation).

Errors in a payment order: consequences of errors

You need to fill out payment documents extremely carefully, because even if the money does not disappear, you will have to spend a long time processing the return of funds, their offset against future payments, and explanations of the situation to the Federal Tax Service. This means taking your employees and tax officials away from work, unnecessary documents, sometimes paying penalties and fines, or even going to court.

The consequences of incorrectly filled out information in payments may be as follows:

- Recognition of the tax amount transferred at the wrong time (entails the accrual of penalties, the imposition of a fine, and sometimes a second payment of the entire amount);

- Recognition of the amount of tax as unpaid (again, it will not be possible to avoid penalties, fines, or even other serious penalties);

- Receipt of a tax or fee to another budget or fund (offsetting payments between different budgets is not possible; the entire amount is paid anew using the correct details).

It is easier to make a mistake in a tax payment order due to the large number of fields to fill out, but dealing with errors here is easier than with insurance premium payments.

Incorrect VAT amount

The buyer allocated VAT by transferring payment to the “simplified” supplier. The tax authorities will have a question: why did the supplier fail to submit a VAT return? The supplier should inform them that he did not issue a VAT invoice to the buyer. Therefore, you are not required to transfer VAT to the budget and submit a declaration. You can support your position with a reference to the letter of the Ministry of Finance of Russia dated February 15, 2018 No. 03-07-14/9470. And correspondence with the buyer stating that VAT was allocated by mistake would not be out of place.

In general, it is safer to draw up an additional agreement to the contract. Agree with the buyer whether you will reduce the price by the amount of VAT. Indicate in the additional agreement that the supplier does not pay VAT because it uses a simplified procedure. This way, we will at least eliminate the possibility that the buyer, “waking up”, will suddenly request a VAT invoice or demand a price reduction by the amount of tax.

What to do in such a situation and how to fix everything?

If it seems to you that the recipient’s account key is incorrect and it should be with the value “4”, in such a situation it is best to immediately contact the recipient to get the details from him again.

But first try the following algorithm:

- Carefully check the addressee's details and the bank BIC you entered. If you notice typos, correct them - most likely they were the problem;

- Do the same with the recipient’s current and correspondent account number;

- If you checked from beginning to end, but did not find any typos, it is possible that the counterparty himself made a mistake. In such a situation, it is best to contact him immediately and ask him to send the details again. We also advise you to inform your counterparty that you have encountered an error: there may be a situation where the counterparty himself did not notice the typo in the details. As a result, he may send you the same details, believing that there is no error in them;

- If the counterparty double-checked the data and sent the correct details again, but the error did not disappear, contact Sberbank technical support. The hotline number is 88005555777 , the call is free of charge.

“Advance” or “payment”?

The risks in case of confusion in these terms (if the second is indicated instead of the first) are high. And for both the payer and the recipient. It is a risky situation for the supplier when the buyer mistakenly indicated “prepayment” on the payment slip, transferring money after the goods have been shipped. If the tax authorities analyze the extract, they will check whether the supplier has reflected VAT on this advance in the declaration. You will have to explain that the buyer paid for the shipped goods. Therefore, it is safer to agree with the buyer in correspondence that he indicated “advance” in the payment slip by mistake.

Inspectors may refuse to deduct VAT from the advance payment for the payer if the buyer has not indicated in the payment slip that he is making an advance payment (clause 9 of Article 172 of the Tax Code of the Russian Federation). There are chances to defend your case in court, but they are not very high (Resolution of the Federal Antimonopoly Service of the Ural District dated April 4, 2014 No. F09-114/14). In this case, either do not reflect the deduction in the purchase book, or agree on the correct purpose of payment in correspondence with the supplier.

By the way, in addition to “misunderstandings” with government agencies, friction between the partners themselves is also possible. Due to an incorrect purpose of payment, the supplier may offset the payment in a different way than the buyer intended. For example, he may decide that he did not receive an advance payment and, because of this, does not ship the goods. If you notice that you indicated “advance” instead of “payment” or vice versa, it is better to immediately inform the supplier about this.

Types of erroneous bank payments

In general, when making an erroneous payment, the client should promptly contact the financial institution to obtain supporting documents, then request the contact details of the recipient and agree with him on the refund process. The nuances of the procedure depend on the type of payment:

- The payment using erroneous details was made in cash at a bank branch. In this case, the client’s funds remain in the sending bank’s account for several hours, so the amount can be returned by submitting an application or contacting a bank operator. The client can personally go to a bank branch or call the hotline; usually they need to name the place (branch address) and time of making the payment, as well as specify the counterparty and the amount of the transaction.

- A payment using incorrect details was made through a mobile application or on the bank’s website. In this case, the payment is processed within a few minutes; if the money is transferred to an account in another bank, the operation may freeze until the next day. The customer should contact the hotline or in-app chat to request a cancellation of the transaction. The details of the erroneous recipient will remain in the account transaction history, so the sender of the payment can independently contact the organization or individual to request a refund.

- A payment using incorrect details was made to an organization (legal entity). In this case, the chances of returning the money are high; the organization’s accountant can contact the sender himself and transfer the money to avoid problems with regulatory authorities. Russian legislation requires legal entities to confirm each transfer with documents (for example, sales contracts and checks), so companies are not interested in receiving “other people’s” money.

- A payment with an incorrect amount was sent using the correct details. If a client paid a fine, made a budget or utility payment and indicated the wrong amount, they should not request a refund. It is advisable to contact the recipient organization (for example, the local tax office) and ask to offset the funds against future payments. For example, when paying a receipt for housing and communal services, the overpayment will be automatically taken into account, and the client will be provided with a recalculation next month.

- The client's payment was transferred to the details of the credit (loan) account. Many loan users create an auto payment (a regular transaction for a fixed amount) to quickly make monthly loan payments. When making monthly payments, the user may confuse the details and send funds to repay loans. It is not possible to return such amounts, however, the bank will automatically update the payment schedule and recalculate the debt taking into account the transferred funds.

- The client made a mistake when replenishing his mobile operator account. In this case, you should promptly submit a written application to the cellular operator, providing payment documents and a subscription agreement. Mobile operators tend to return money if the client contacts the office no later than 24 hours after making the payment.

- The client mistakenly paid for a purchase in an online store. In this case, the possibility of returning the money is provided for by Russian law FZ-2300-1, which protects consumer rights. The client should submit an application to cancel the order or return the product (service) to the store’s hotline, cancel the order and wait for the refund of the funds paid.

The greatest chance of returning an erroneously made payment is for clients who contact the bank’s office or hotline immediately after the transaction is completed. Transactions are processed with a slight delay, so the client can have time to cancel the transfer and receive the funds back. Russian legislation (FZ-395-1, which regulates banking activities) prohibits banks from independently canceling transfers or returning money based on the applicant’s comments, so the payer must communicate with the recipient of the funds.

Inflated payment amount

The buyer transfers an amount greater than indicated in the contract or invoice. This is by no means a cause for joy. The negative consequences of such “generosity” will not be long in coming, as they say. For example, according to the contract, the buyer must transfer an advance in the amount of 30% of the cost of goods, but in fact transferred 50%. The supplier will have to charge VAT on the entire amount of the advance received, otherwise the inspectors will have claims when they check the bank statement. The overpayment, by the way, may be an advance payment against the next shipments, but this does not change the essence.

If you rely on the clarifications of the Russian Ministry of Finance in letter No. 03-07-11/8323 dated February 12, 2021, the buyer has the right to claim VAT deduction from the advance payment, even if its amount is greater than that provided for in the contract. But inspectors can pretend that they don’t know anything about them (or really don’t know). To avoid disputes with tax authorities, it is better to draw up an additional agreement to the supply agreement, indicating in it the amount of the advance payment transferred upon delivery. By the way, in this case, as in the previous one, disputes between counterparties cannot be ruled out - if the overpayment is incorrectly offset or not returned. Check the terms of the contract.

It may tell you how to offset the overpayment. For example, these amounts are considered an advance against future shipments. Or they are offset against the debt. In this case, apply the rules of the contract, and also inform the buyer how you offset the overpayment.

If there are no such conditions in the contract, judges allow the supplier to offset the overpayment against the debt (clauses 2, 3 of Article 319.1 of the Civil Code of the Russian Federation, Resolution of the Administrative Court of the Ural District of December 21, 2015 No. F09-9691/15). But it is worth agreeing on the offset with the buyer.

If the buyer has no debt, it is safer to return the overpayment to him. If the supplier does not return the overpayment, the buyer has the right to go to court and demand interest at the key rate of the Central Bank of the Russian Federation (Article 395, paragraph 2 of Article 1107 of the Civil Code of the Russian Federation). Companies can also agree that the overpayment is considered an advance towards future shipments.

What are the errors in a payment order?

The payment order may contain the following errors:

| Error | Possibility to fix (no other errors) | What to do? |

| The purpose of payment is incorrectly specified | Eat | — Organize a tax reconciliation with the Federal Tax Service, — draw up a reconciliation report, — sign the document yourself and give it to a Federal Tax Service employee for signature. |

| The payment amount is too high | Eat | Option 1:—Pay the tax or fee again, — leave overpaid funds to offset future payments. Option 2: — Take it into account immediately when making other payments (to the same budget). Option 3: — Issue a refund to the account. |

| Payment amount is too low | No. The tax is considered unpaid and a penalty will be charged. | Pay the missing amount. |

| An out-of-date KBK is entered - incorrect numbers - old KBK. | No. The money will be classified as unclassified payments, and the tax will remain unpaid, which will entail the accrual of penalties. | Fill out an application to the Federal Tax Service, ask to offset the transferred amount, leave a copy of the incorrectly completed document and a bank statement. |

| An erroneous KBK was entered (the KBK is relevant, but relates to another tax of the same fund) | No. The tax that was originally supposed to be paid will be considered unpaid (penalties will be charged), and an overpayment will arise for the tax levy, the BCC of which was mistakenly used. | Option 1: Make a refund to the account. Option 2: Transfer the entire amount again, do nothing regarding the overpayment, and then offset it when paying a similar tax. Option 3: Immediately offset against payment of other taxes to the same budget. |

| The KBK is indicated at the same time as the wrong tax and another fund | No. The tax will be unpaid and a penalty will be charged. | Transfer the entire amount again. (The payment will be accepted by the budget of another level, whose BCC was incorrectly indicated, an overpayment of tax will be created. Offset of funds against taxes cannot be made between funds of different levels.) |

| Column 101 incorrectly indicates the payer status | No. The tax will not be considered paid, since the money will be included in unclassified payments. | Ask the Federal Tax Service by filling out an application to transfer money by credit from an incorrectly designated code to the correct one. |

Errors in a payment order that cannot be corrected

Payment order errors that cannot be corrected:

| Error | A comment |

| The recipient's account is incorrectly specified | Worst mistake of all. Money is not recognized as paid to the budget. You need to send the funds again; for each day of delay in payment, a penalty will be added to the tax amount. |

| The bank name is entered incorrectly | Another irreversible mistake that leads to failure to pay taxes on time and to the accrual of penalties. |

| You entered the wrong BCC | When making insurance payments, you must pay again, as there will be an underpayment. But when paying taxes, an application is submitted to the Federal Tax Service to clarify the codes. |

| A non-existent KBK is indicated | All that remains is to return the funds and make the payment again, because the money simply will not find a recipient. |

Errors in a tax payment order that can be corrected

To correct the mistake, you need to clarify the data by submitting an application to the Federal Tax Service (you will need to present a copy of the payment order).

| Error | Column in the payment order | Correct option |

| Invalid payer status | 101 | 01 - for transferring funds to pay tax on compulsory insurance (medical, pension), recipient - extra-budgetary fund; 02 - calculation of personal income tax; 08 - payments to the social fund. insurance; 09 - individual entrepreneur payments. |

| Incorrect checkpoint or TIN of the recipient | 61 or 103 | The checkpoint consists of nine digits, the Taxpayer Identification Number (TIN) consists of ten digits |

| Invalid KBK | 104 | The correct BCC consists of twenty digits |

| Incorrect OKATO | 105 | Includes eleven digits. If an error is made when paying local taxes (personal income tax, UTII), funds may mistakenly go to the budget of the wrong region. Therefore, in cases with local taxes, it will be safer to transfer the entire tax amount again, and then proceed to return the incorrectly sent money. |

| Incorrect basis for payment | 106 | TP - current payment; ZD - payment of debt of one's own free will; TR - forced payment (requirement of Federal Tax Service employees). |

| Incorrect tax period indication | 107 | MS.(N).2017 - monthly; KV.(N).2017 - quarterly; PL.(N).2017 - for six months; GD.00.2017 - for 2021 |

| Incorrect payment type entered | 110 | NS - tax; VZ - contribution; AB - advance payment; PE - penalty. |

What are the prospects for simplifying the procedure for filling out payment slips for paying taxes and fees?

By Order of the Government of the Russian Federation dated February 10, 2014 No. 162-r, the action plan (“road map”) “Improving tax administration” was approved.

In accordance with clause 8 of section. I “Reducing the time for preparation and submission of tax reports by the taxpayer” is intended to reduce the number of payment order details required to be filled in for the transfer of taxes and fees. To do this, it is planned to analyze and inventory the mandatory details of a payment order for the transfer of taxes and fees (including the type of payment, type, payment period, order of payment, payer status) in order to reduce and eliminate redundant information and reduce the number of errors when transferring tax deductions. Then it is planned to implement proposals and recommendations developed based on the results of the analysis. The executor for this item is the Ministry of Finance with the participation of the Central Bank of the Russian Federation. Deadline: September 2014.