Innovations in the P-3 form from 2020

Starting with reporting for January 2021 , it is necessary to fill out and submit Form P-3 “Information on the financial condition of the organization” on a new form.

The new P-3 form was approved by Rosstat order No. 421 dated July 24, 2019 in Appendix No. 6. Instructions for filling out the new P-3 form were introduced by Rosstat order No. 711 dated November 27, 2019. It looks like this:

The new form P-3 2021 can be downloaded for free using the following link (excel):

FORM P-3 IN 2021

The form has not undergone significant changes. But the list of entities who must submit this form has been changed.

Who submits form P-3 in 2020

Statistical reporting forms are quite simple and understandable to use. Respondents and deadlines for submitting forms are usually indicated on their cover pages. Form P-3 is no exception.

For convenience, we will list those who should and who should not submit this report to the diagram:

There is no exemption from submitting the zero form P-3. If a legal entity is included in the list of applicants and there are no indicators, they submit a zero - a completed title page and empty other sections.

Deadlines for submitting form P-3 in 2020

There is a correlation between submitting form P-3 by deadline, depending on who submits this form:

KEEP IN MIND

The form that is submitted at the end of the quarter is essentially the same monthly form on which the “quarterly” sections are completed. 2 more days are allotted for its delivery.

Even if monthly submission of the report is established, some sections of the P-3 form are filled out only based on quarterly results. We will consider the features of filling out form P-3 below.

Report submission deadlines

Organizations must submit these reports within the following deadlines:

- every month until the twenty-eighth day of the month that follows the reporting period (you only need to submit the first section);

- every quarter until the thirtieth day of the month following the expired reporting period (the entire report must be submitted).

You should not forget to submit the P-3 stat form on time, since there are fines for late submission. For the company itself, the fine ranges from twenty to seventy thousand rubles, and for employees responsible for filling out the form - from ten to twenty thousand rubles.

Composition of form P-3

Form P-3 is a generalized form about the financial condition of an enterprise and allows Rosstat to analyze the company’s ability to maintain economic efficiency and manage capital.

It is filled out throughout the organization as a whole. There is no need to submit separate reports for each department.

The form contains the following sections:

And here is the approach to filling out form P-3 in different cases:

- only the title page is filled out by those organizations that are required to submit a report, but do not operate or do not have indicators for filling out form P-3 (in this case, Sections 1-4 are presented blank);

- those who must submit Form P-3 monthly fill out the Cover Sheet and Section 1 monthly, and Sections 2-4 quarterly.

P-3 statistics 2021: form, instructions for filling

In this section, column 1 provides data for the reporting period, and column 2 for the corresponding period of the previous year.

Fill in line by line:

36 - the cost of non-current assets, which, in accordance with accounting rules, include fixed assets, intangible assets, long-term financial investments, unfinished investments in non-current assets, exploration assets, profitable investments in tangible assets, deferred tax assets, etc., recorded in the accounting accounts Section 1 “Non-current assets”. Line 36 corresponds to the total for section 1 “Non-current assets” of the balance sheet.

37 - intangible assets at residual value (except for objects for which depreciation is not charged), recorded in accounts 04, 05. Reflect intangible exploration assets that are recognized as non-current.

Line 38 from line 37 identifies those accounted for as intangible assets, intangible exploration assets, research and development results: negotiable contracts, lease agreements, licenses, business reputation (goodwill) and marketing assets.

39 - fixed assets in operation and under reconstruction, modernization, restoration, conservation or reserve, leased, in trust management, at residual value (except for fixed assets for which depreciation is not charged).

Line 40 from line 39 identifies land plots and environmental management facilities.

41 - costs of construction and installation work, acquisition of buildings, equipment, vehicles, tools, inventory, other durable material objects, other capital works and costs not documented by acceptance certificates of fixed assets and other documents.

42 - inventories at actual cost; VAT on purchased assets; accounts receivable; short-term financial investments, cash and other current assets recorded in accounts 10, 11, 14, 15, 16, 19 - 21, 23, 29, 41, 43 - 46, 50 - 58, 60, 62, 68 - 71, 73, 75, 76, 81, 97.

43 - inventories recorded in accounts 10, 11, 14, 15, 16, 20, 21, 23, 29, 41, 43 - 46, 97. Line 43 corresponds to the “Inventories” indicator in section 2 of the balance sheet.

44 - balances of stocks of raw materials, materials, fuel, purchased semi-finished products, components, structures, parts, containers, spare parts, inventory and household supplies, etc. values of the organization, recorded in accounts 10, 11, 14, 15, 16.

45 - costs of work in progress and unfinished work (services), recorded in accounts 20, 21, 23, 29, 44, 46. If trade and public catering organizations do not recognize the recorded distribution costs in the cost of goods (services) sold in full reporting period as expenses for ordinary activities, then the amount of distribution costs attributable to the balance of unsold goods and raw materials is reflected on line 45.

46 - the actual production cost of the balance in warehouses of finished products that have passed testing and acceptance, complete with all parts in accordance with the terms of contracts with customers and the relevant technical conditions and standards (accounts 43, 16).

47 - the cost of inventory items purchased as goods for sale. Organizations operating in industrial production and other production areas show the cost of products, materials and products purchased specifically for sale, as well as the cost of finished products purchased for assembly, not included in the cost of manufactured products and subject to reimbursement by the buyer separately (accounts 41 , 16).

48 - the amount of VAT on acquired inventories, intangible assets, capital investments made, etc., works and services, subject to assignment in the prescribed manner in the following reporting periods to reduce tax amounts for transfer to the budget or to the appropriate sources of its coverage . Line 48 corresponds to the indicator “Value added tax on acquired assets” in section 2 of the balance sheet.

49 - investments of an organization in securities of other organizations, government securities, etc., loans provided by the organization to other organizations, deposits under a simple partnership agreement, etc. (accounts 58, 59).

50 - balances of funds belonging to the organization, located in the cash register, on settlement, currency and other accounts, etc. (accounts 50, 51, 52, 55, 57).

>Instructions for filling out form P-3

The procedure for completing form P-3 is regulated by Rosstat Order No. 509 dated 08/01/2017, which provides instructions for filling out the form.

Procedure for filling out form P-3

Form P-3 is filled out on the basis of synthetic and analytical accounting accounts. If an organization prepares interim reporting, then data from such reporting must be entered into Form P-3. If the company does not have such an obligation, primary accounting information should be used.

Cost indicators in form P-3 are rounded to the nearest thousand rubles.

No sections of the form are a generalization of its other sections, so you can fill out the sheets in order.

Title page

The title page must be submitted in any case, no matter who submits the P-3 form and at what time. It is necessary to fill in the following information:

- the period for which the reporting is prepared;

- name of the reporting enterprise;

- postal address of the company;

- OKPO.

Section 1

Lines 01-02 show the financial result from the general activities of the enterprise. This includes income from core activities and other income reduced by all expenses. Reflects pre-tax financial results.

Line 01 contains data for the reporting period of the current year, and line 02 contains data for the same period of the previous year.

Lines 03-12 show accounts receivable:

- line 03 – total receivables;

- line 05 identifies the debts of buyers and customers for goods, works and services from the total debt;

- lines 06 and 07 separate from the debt of buyers that which is secured by bills received, as well as debt on government orders;

- line 12 selects short-term receivables from the total amount.

Lines 13-25 show accounts payable:

- line 13 – general creditor;

- Lines 15-25 highlight from the total accounts payable debts to the budget, to state extra-budgetary funds, suppliers and contractors, as well as short-term creditors;

- Line 20 highlights from the debt to suppliers and contractors that which is secured by issued bills of exchange.

Line 26 is responsible for debt on loans and borrowings, line 27 is for short-term loans and borrowings.

In column 2, for each line, it is necessary to highlight the amount of overdue debt, if any.

Debt must be calculated for each counterparty and for each agreement separately. That is, if the counterparty is both a buyer and a supplier or has several contracts at the same time, then it is impossible to summarize the balance for each contract; they must be shown separately.

Section 2

The section is filled out only based on the results of the quarter. There are 2 columns in the section. The first column reflects the data of the reporting period of the current year, the second – the data of the same period for the previous year.

Line 30 shows revenue from main activities. VAT, excise taxes and other similar payments are not included here.

Line 31 is intended to reflect the cost.

Line 32 reflects general production expenses and expenses for maintaining the enterprise.

Line 33 is calculated. The difference is entered into it: line 30 – line 31 – line 32.

Line 34 reflects proceeds from the sale of fixed assets, if such transactions took place during the reporting period.

Line 35 is intended to indicate interest on loans that the organization took into account as expenses in the reporting period.

Section 3

The section is filled out quarterly.

Consists of lines 36-41, intended for information about non-current assets, and lines 42-50, intended for information about current assets.

Line 50a - “Net assets” - is filled out only in the report for the full year as of the end of the year.

In non-current assets the following are highlighted line by line:

- NMA, R&D results; separately - contracts, lease agreements, business reputation, marketing assets;

- OS, profitable investments; separately – land plots and environmental management facilities;

- unfinished capital additions.

In current assets the following are highlighted line by line:

- stocks; separately - production inventories, costs in work in progress, finished products, goods for resale;

- VAT on purchased assets;

- short-term financial investments;

- cash.

Section 4

Another quarterly section P-3.

Section 4 of form P-3 contains information about the organization’s interaction with Russian counterparties (totally on page 51) and with counterparties from other countries. CIS countries are highlighted in separate lines (pp. 53-62). Non-CIS countries are combined in one line 63.

The following information must be filled in:

- volume of goods shipped, including VAT and other similar payments;

- customer debt (separately - overdue);

- debt to suppliers and contractors (separately - overdue);

- debt on received loans and borrowings (separately - overdue).

How to fill

The form includes a title page and four sections.

The title page indicates the basic data of the reporting company.

Section 1

The data in lines 01–02 must be equal to the same indicators indicated in the “Statement of Financial Results”.

Lines 03–12 should show accounts receivable. For each contract with a counterparty, the debt must be looked at separately.

Line 13 should show the total amount of accounts payable.

Lines 15–25 reflect data on types of accounts payable.

Separately, lines 26–27 show debt on loans and borrowings.

Section 2

This section shows the total amount of income and expenses. You only need to fill out the data once a quarter. All indicators correspond to the indicators of the same name from the “Report on Financial Results”.

In line 30 you need to reflect the amount of revenue excluding VAT. This indicator is considered similar to the “Revenue” indicator in the “Income Statement”.

Cost, selling and administrative expenses should be recorded in lines 31 and 32, respectively.

The result of the activity is shown in line 33.

A separate line (34) includes revenue from the sale of fixed assets.

Line 35 takes into account interest on the use of borrowed funds.

Section 3

The third section is completed once a quarter.

This section contains information on the types of current and non-current assets (lines 36–50).

Line 50a is completed on the annual form.

The indicators correspond to similar indicators in section 1 of the balance sheet.

Section 4

To be completed once a quarter.

The section contains information on goods shipped and services provided by country. To fill out the tabular part, you need to take selling prices, including VAT and other similar payments.

Complete instructions for filling out P-3

Please note that as of the January 2021 report, a new form is in effect.

> Information about the financial condition of the organization - form P-3

Form “P-3 statistics”: purpose

Instructions for filling out form P-3

Results

Correspondence of lines of form P-3 to accounting lines

Let's put into the table the correspondence of the lines of form P-3 with the lines of the balance sheet and the financial results statement.

| FORM LINE P-3 | BALANCE SHEET LINES | FINANCIAL STATEMENT LINES |

| Line 01 Section 1 | – | Profit (loss) before tax for the reporting period |

| Line 02 Section 1 | – | Profit (loss) before tax for the same period of the previous year |

| Line 30 Section 2 | – | Revenue |

| Line 31 of Section 2 | – | Cost price |

| Line 32 of Section 2 | – | Selling expenses + Administrative expenses |

| Line 36 Section 3 | Result for section 1 “Non-current assets” | – |

| Line 42 Section 3 | Result for section 2 “Current assets” | – |

Common form filling mistakes

The data presented in Form P-3 may contain errors that lead to unreliable indicators.

| Condition for entering data | Wrong position | Correct position |

| Linking indicators with financial statements and balance sheets | Inconsistency of revenue, expenses, non-current, current assets with the data of form P-3 | The report indicators must coincide with the accounting data of the enterprise’s activities |

| Calculation of numbers determining the need to pass P-3 | Using headcount calculations that do not meet Rosstat requirements | When calculating the number, the requirements established by Instructions No. 498 are taken into account |

| Presentation of reporting by enterprises that have separate divisions on a separate balance sheet | Reporting is submitted at the location of the main body of the enterprise | If there are separate divisions that have an independent balance sheet, reporting is presented for the parent organization and for the division |

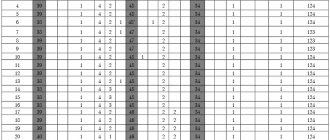

Example of filling out form P-3

Let Principle LLC be one of those legal entities that need to submit Form P-3. The accountant of Princip LLC fills out form P-3 based on the results of the first quarter of 2021. Interim financial statements are not prepared, so Form P-3 is filled out based on primary accounting data.

Based on the results of the first quarter, it is necessary to fill out all sections of the P-3 form. LLC "Princip" has no counterparties abroad.

This is what a sample of a completed P-3 form looks like in 2021: