Home — Articles

In their activities, taxpayers often resort to the services of intermediaries as a profitable method when paying for goods (works, services). Intermediaries, using their contacts, experience and specializations, ensure wide availability of goods and bring them to a specific consumer. However, in the process of work, a lot of difficulties arise for both parties to the transaction, one of which is the preparation and issuance of invoices . This is the question we will address in this article.

Procedure for issuing invoices

What is common to all intermediaries (commission agent, agent, attorney) is that they act in the interests of the customer and at his expense; everything they receive from third parties is the property of the customer and is subject to transfer to him. Settlements between the customer and third parties can be made either directly with or without the participation of an intermediary. Acting within the framework of a commission agreement, the intermediary (commission agent), on his own behalf, writes out all the necessary documents related to the transaction when selling goods. The intermediary (agent) acts similarly, acting within the framework of the agency agreement on his own behalf and in the interests of the principal. They are required to follow a certain procedure for issuing invoices so that the principal (principal), being a VAT payer, can fulfill his obligations for VAT calculations. When selling goods (work, services), as well as upon receiving payment amounts, partial payment for upcoming deliveries of goods (performance of work, provision of services), appropriate invoices are issued (clause 3 of Article 168 of the Tax Code of the Russian Federation). The procedure for issuing invoices is regulated by the Rules for maintaining logs of received and issued invoices, purchase books and sales books for VAT calculations, approved by Decree of the Government of the Russian Federation of December 2, 2000 N 914 (hereinafter referred to as the Rules).

Introductory information

Modern VAT verification is a cross-check of suppliers and buyers participating in the same transaction.

Tax officials study the information entered in the purchase books and sales books, and in case of intermediary transactions, also in the journal of received and issued invoices (hereinafter referred to as the journal). If the data for all counterparties is consistent, the inspectors admit that there were no violations. Otherwise, the transaction falls into the category of suspicious with all the ensuing consequences (read more about this in the articles “VAT “under the hood”, or a general cameral” and “VAT return for the 3rd quarter: what the tax authorities will check and how to avoid common mistakes when filling out the declaration"). Carry out automatic reconciliation of invoices with counterparties

As part of cross-control, inspectors, among other things, study such details as the type of operation code (KVO). The list of codes was approved by order of the Federal Tax Service of Russia dated March 14, 2016 No. ММВ-7-3 / [email protected] (see “From July 1, new transaction codes will need to be indicated in the books of purchases, sales and the invoice journal”). The commented letter describes what values of the KVO and other “key” details must be indicated during various intermediary operations so that the transaction does not arouse suspicion. The authors of the letter also explained how each participant should register invoices. Let's consider the rules that need to be applied in various types of intermediary transactions.

Sales of goods

To draw up an intermediary invoice, please refer to clause 24 of the Rules. The obligation to draw up an invoice for sales arises with the intermediary (commission agent, agent) when he acts on his own behalf . The commission agent (agent) draws up an invoice on his own behalf upon receipt of an advance payment (prepayment) for upcoming deliveries of goods in two copies. It operates similarly when selling goods. One copy is handed over to the buyer, the second is filed in the journal of issued invoices without registering it in the sales book. In turn, the principal (principal) issues an invoice in the name of the intermediary, registering it in the sales book. This invoice reflects the invoice figures issued by the intermediary to the buyer. The intermediary does not register this invoice in the purchase book. The intermediary issues a separate invoice to the principal (committee, principal) for the amount of his remuneration under the agency agreement (commission, agency agreement). This invoice is registered in the prescribed manner with the attorney (commission agent, agent) in the sales book, and with the principal (committee, principal) in the purchase book.

How to decipher the term “consolidated invoice”

There is no official definition of this concept.

In general, any document compiled on the basis of several primary documents can be considered consolidated. Accordingly, an invoice that combines information from several invoices can be considered consolidated. Consolidated invoice information can be obtained from various sources:

- Art. 158 of the Tax Code of the Russian Federation - this norm provides for the preparation of a consolidated invoice for the sale of the enterprise as a whole as a property complex. It identifies types of property, the amount of receivables, the value of securities and other components of balance sheet assets as separate items.

- Rules for filling out invoices approved by Decree of the Government of the Russian Federation dated December 26, 2011 No. 1137 - they provide for the possibility of issuing consolidated invoices in certain situations and contain general requirements for invoices.

- Explanations from the Ministry of Finance and the Federal Tax Service - officials, in responses to private inquiries, deciphered the procedure for filling out consolidated financial statements in different situations: in shared construction, for commission and agency transactions, in other cases.

Find out how to issue a consolidated invoice if the principal sells the goods through an agent in this material.

We will talk further about the features of the design of consolidated financial statements in certain situations from the position of the Federal Tax Service and the Ministry of Finance.

Preparation of invoices for sales

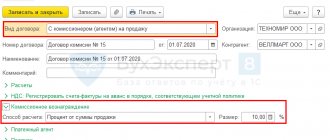

As a rule, intermediaries did not have any questions regarding the preparation of invoices when selling goods. In this case, the general procedure provided for in paragraph 3 of Art. 168, art. 169 of the Tax Code of the Russian Federation and the Rules. In the Letter of the Federal Tax Service of Russia dated 02/04/2010 N ShS-22-3/ [email protected] (hereinafter referred to as Letter N ShS-22-3/ [email protected] ), the tax department indicated it again. The commission agent (agent), upon receipt of an advance payment (prepayment), fills out the invoice as follows : - in line 1 of the invoice, the commission agent (agent) indicates the date of issue and the serial number of the invoice in chronological order; — lines 2, 2a, 2b indicate the name and location of the commission agent (agent) in accordance with the constituent documents, as well as his tax identification number and checkpoint; — lines 3 and 4 contain dashes; — line 5 indicates the details (number and date) of the payment document or cash receipt (when making payments using payment documents or cash receipts to which the invoice is attached) about the buyer’s transfer of advance payment to the commission agent (agent). In case of prepayment in a non-cash form of payment, a dash is placed; — lines 6, 6a and 6b are filled in in the order specified in the Rules; — Column 1 indicates the name of the goods supplied (description of work, services), property rights; - in columns 2 - 6, dashes are placed; — Column 7 indicates the tax rate determined in accordance with clause 4 of Art. 164 Tax Code of the Russian Federation (10/110 or 18/118); — Column 8 indicates the amount of tax determined in accordance with clause 4 of Art. 164 of the Code. — in column 9 enter the amount of the prepayment received, taking into account the amount of VAT; — in columns 10 and 11, dashes are placed. For clarity, let's give an example.

Example. LLC "Commissioner" received a 100% prepayment from LLC "Buyer" by payment order dated December 7, 2010 N 77 in the amount of 118,000 rubles, including VAT - 18,000 rubles. for 10 units of product 1, purchasing it for Komitent LLC. The “commission agent”, having received the advance payment, will issue an invoice in the name of the buyer. When selling goods on December 17, the commission agent will issue an invoice in the name of the buyer. At the same time, he: - in line 1 indicates the date of issue and the serial number of the invoice in chronological order; - in lines 2, 2a, 2b indicates the name and location of the commission agent (agent) in accordance with the constituent documents, as well as his tax identification number and checkpoint; — line 5 is filled in in case of receiving an advance payment. The details (number and date) of the payment and settlement document or cash receipt (when making payments using payment documents or cash receipts to which the invoice is attached) are indicated regarding the transfer by the buyer of the advance payment to the commission agent (agent). In case of prepayment in a non-cash form of payment, a dash is placed; - lines 3, 4, 6, 6a and 6b, columns 1 - 11 are filled out according to the general rules. Invoices that the “Commission Agent” issues to the buyer (advance and upon sale) are signed by his authorized representatives. To illustrate the example of drawing up an invoice by the “Committent”, we will give an option when he issues an invoice in the name of the commission agent upon shipment of goods. As you can see, everything is not so complicated. All difficulties arise when purchasing goods (works, services) through an intermediary.

The principal applies the STS, the commission agent applies the STS

When carrying out operations for the sale of goods, the principal and the commission agent draw up and issue invoices in the same manner as in a situation where both of them are VAT payers. The commission agent keeps a logbook and submits it electronically to the tax office quarterly.

Invoices

Since the principal is a VAT payer, the sale of his goods by the commission agent is subject to this tax. This means that the commission agent must issue an invoice, even if he uses the simplified tax system. The Russian Ministry of Finance adheres to a similar position (letters dated June 25, 2014 No. 03-07-RZ/30534, dated July 1, 2013 No. 03-07-14/25028). The commission agent fills out this invoice in the manner prescribed by clause 1 of the Rules for filling out invoices. The commission agent transfers his data to the principal, who, on their basis, issues his own invoice for the sale of goods.

Thus, the VAT document flow in terms of invoices issued for the sale of goods under a commission agreement in the situation under consideration is similar to the document flow of the principal and the commission agent, who are VAT payers.

Since the commission agent is not a VAT payer, he does not issue an invoice for his remuneration under the commission agreement.

Sales book

According to clause 20 of the Rules for maintaining the sales book, invoices issued by the commission agent when selling the goods of the principal are not recorded in it. Consequently, the commission agent using the simplified tax system does not keep a sales book when carrying out intermediary activities.

The principal registers the invoice issued on the basis of the commission agent's data in his sales book. In column 9, he indicates the name of the commission agent, and in column 10 - his TIN (subparagraph “m”, “n”, paragraph 7 of the Rules for maintaining the sales book).

Journal of received and issued invoices

Since, when carrying out intermediary activities, a commission agent using the simplified tax system issues invoices, he must keep an accounting log (clause 3.1 of Article 169 of the Tax Code of the Russian Federation) in the same manner as a commission agent who pays VAT.

We note that according to clause 5.2 of Art. 174 of the Tax Code of the Russian Federation, persons who are not VAT payers, in the case of issuing and (or) receiving invoices when carrying out business activities in the interests of another person on the basis of commission agreements, are required to submit to the tax authorities at the place of their registration a log of received and issued invoices - invoices in relation to the specified activities in the established format in electronic form via telecommunication channels through an electronic document management operator no later than the 20th day of the month following the expired tax period.

In the letter of the Federal Tax Service of Russia dated 04/08/2015 No. GD-4-3/ [email protected] “On the procedure for submitting a VAT return, as well as a log of received and issued invoices for the first quarter of 2015” it is said that the sending of the log by the above-mentioned persons accounting of received and issued invoices is carried out within the framework of the document flow for the submission of individual documents to the tax authorities (12 subsidiaries), approved by order of the Federal Tax Service of Russia dated November 9, 2010 No. ММВ-7-6/ [email protected] , using the list of documents approved by the order Federal Tax Service of Russia dated June 29, 2012 No. ММВ-7-6/ [email protected]

The principal does not keep a log of received and issued invoices.

Purchasing goods

We have to admit the fact that in the important document on the procedure for accounting and drawing up invoices, the Rules, nothing is said about the procedure for maintaining document flow when purchasing goods under commission agreements and agency agreements. True, from time to time officials devoted their letters to this. Thus, in the Letter of the Ministry of Taxes of Russia dated May 21, 2001 N VG-6-03/404 (hereinafter referred to as the Letter of the Ministry of Taxes of Russia) it is said that when purchasing goods (work, services) through an attorney (agent), the basis for deducting VAT is from the principal (principal) for purchased goods (works, services) is an invoice issued by the seller in the name of the principal (principal). When an invoice is issued by the seller in the name of the commission agent (agent), the basis for the principal (principal) to accept VAT for deduction is the invoice received from the intermediary. In this case, the intermediary issues an invoice to the principal (principal) reflecting the indicators from the invoice issued by the seller to the intermediary. The intermediary does not register these invoices in the sales book. In addition, the later Letter of the Department of Tax Administration of Russia for Moscow dated September 17, 2004 N 21-09/60455 explains that the principal (principal) has the right to apply tax deductions for VAT on the basis of an invoice issued by the agent to the principal, whose indicators correspond to the indicators of the invoice issued by the seller (service provider) to the agent with the allocated VAT amount, as well as in the presence of the agent’s report and supporting documents. The Russian Ministry of Finance has a similar position. In its Letter dated November 14, 2006 N 03-04-09/20, the financial department emphasizes that in the case of the acquisition of goods (work, services) by a commission agent for the principal at the expense of the principal, when issuing invoices to the principal, a procedure similar to the procedure provided for para. 2 clause 24 of the Rules. In this situation, the commission agent issues an invoice for the principal reflecting the indicators of the invoice issued by the seller to the commission agent. However, such invoices are not registered by the commission agent in the purchase book and sales book. Based on the provisions of clause 8 of the Rules, for the purpose of applying tax deductions, the invoice received by the principal from the commission agent is registered by him in the purchase book. In this case, the VAT amounts indicated in the commission agent’s invoice addressed to the principal are subject to deduction from the latter if the conditions of Art. Art. 171, 172 of the Tax Code of the Russian Federation and in the presence of copies of primary accounting and settlement documents received from the commission agent. This emphasizes that an important document for the principal (principal) for the purpose of accepting VAT for deduction is the invoice of the commission agent (agent) in his name reflecting the indicators from the invoice issued by the seller in the name of the intermediary. Up to this point everything seems clear. We come to the most important thing! How are these invoices created?

Invoice from the commission agent for the sale of goods (works, services)

When selling goods (works, services) of a principal who is a VAT payer, you must prepare and issue invoices to buyers on your behalf.

Provide copies of these invoices to the principal. The principal will take from the copy information about the buyer, goods shipped or advances received, issue an invoice on his behalf and give it to you.

Record all invoices that you issue to customers and that you receive from the consignor in the invoice journal. They do not need to be recorded in the sales book or purchase book.

You need to issue invoices and keep logs of invoices even if you are not a VAT payer (clause 3.1 of Article 169 of the Tax Code of the Russian Federation). For example, if you are on the simplified tax system.

If you are a VAT payer, you must also issue invoices to the committing agent for your commission (including those paid to you in advance) or for other income you receive for your services. You record these invoices in the sales ledger. They do not need to be registered in the accounting journal (clause 1(2) of the Rules for maintaining the invoice journal).

How can a commission agent fill out an invoice for a buyer when selling goods (works, services) of the principal

When filling out the invoice, please indicate:

- in line 1 - invoice number and date. Indicate the number that is in your order for outgoing invoices. There is no need to enter special numbering for “commission” invoices (clause “a”, clause 1 of the Rules for filling out invoices);

- lines 2, 2a and 2b - your name, address, tax identification number and checkpoint (Letter of the Ministry of Finance of Russia dated July 19, 2017 N 03-07-09/45747).

Fill out the remaining lines and columns of the invoice as usual.

How can a commission agent issue and register invoices for the sale of goods (works, services) of the principal?

You must prepare and issue an invoice to the buyer no later than five calendar days from the date (clause 3 of Article 168 of the Tax Code of the Russian Federation):

- shipment of goods (works, services) to the buyer;

- receiving an advance from the buyer.

Register the issued invoice in part 1 of the invoice journal (clauses 1, 3, paragraph “a”, clause 7 of the Rules for maintaining the invoice journal). Do not register it in the sales book.

If the invoice simultaneously contains your own goods (works, services) and the principal’s, then this invoice must be registered both in Part 1 of the invoice journal and in the sales book.

Give the consignor a copy of the invoice. There is no need to re-expose it. Based on the copy, the principal will issue you an invoice with the same indicators (paragraphs “i” - “l”, paragraph 1 of the Rules for filling out an invoice).

Register the invoice that you received from the principal in part 2 of the invoice journal (clauses 1, 3, paragraph “a”, clause 11 of the Rules for maintaining the invoice journal).

Preparation of invoices for purchases

Let us turn again to Letter N ШС-22-3/ [email protected] First of all, the tax department refers taxpayers to clause 24 of the Rules and notes that the procedure provided for therein is advisable to apply when purchasing goods, works, services for the principal (principal) , property rights under a commission agreement (agency agreement), providing for the acquisition of goods (work, services), property rights on behalf of the commission agent (agent). An invoice for goods sold to a commission agent (agent) by the seller is drawn up in accordance with the generally established procedure. In turn, the commission agent (agent) must transfer the invoice information received from the seller of the goods to the commission customer (principal). For this purpose, he draws up an invoice to the commission agent (principal) reflecting the indicators from the invoice issued by the seller to the intermediary . The date of issue of the specified documents must match, the serial number of the document drawn up by the commission agent (agent) is indicated in chronological order (line 1 of the invoice). Filling out lines 2, 2a, 2b is strictly prescribed and is surprising. The thing is that in these lines, in accordance with the requirements of the Federal Tax Service of Russia, the name and location of the seller are indicated in accordance with the constituent documents, as well as his tax identification number and checkpoint. That is, the details of the seller of the goods are entered, while he is not connected with the principal (principal) by any contractual relations. Lines 6, 6a, 6b indicate information about the buyer (principal, principal) in accordance with the Rules. And such an invoice must be signed by the manager and chief accountant (or other authorized persons) of the intermediary (commission agent, agent). A strange situation arises. This invoice does not contain a word (data) about the intermediary, and the signatures are affixed by its responsible persons. But the tax authorities insist on their own. This is the procedure for filling out an invoice that must be followed by an intermediary when issuing an invoice to the principal (principal). Otherwise, the latter will not be able to accept the amount of VAT for deduction indicated in the commission agent’s invoice addressed to the principal. The customer (principal, principal), having received the goods, as well as such an invoice, registers this document in the purchase book and in the journal of received invoices. He does the same with the intermediary’s invoice for his remuneration. Please note the special procedure for filling out line 5 of the invoice. It indicates: - details (number and date of preparation) of the payment and settlement document or cash receipt (when paying using payment documents or cash receipts to which the invoice is attached), corresponding to the details specified in the seller's invoice ( i.e. payment and settlement document or cash receipt confirming the transfer by the intermediary to the seller); — details (number and date of preparation) of the payment and settlement document or cash receipt confirming the transfer by the customer-committent (principal) of the advance payment to the intermediary commission agent (agent). We remind you that in case the seller receives payment, partial payment for upcoming deliveries of goods (performance of work, provision of services), transfer of property rights using a non-cash form of payment, a dash is entered in line 5 of the invoice drawn up by the commission agent (agent). To explain this, let’s use the data from the example above. Only with the change that LLC “Commissioner” acquires for LLC “Committent”. The “Commission Agent” made a 100% prepayment according to the payment order dated December 7, 2010 N 71 from the seller for the goods. He, in turn, issued an invoice for prepayment to the “Commission Agent”. The “Commission Agent” issues an invoice to the “Committent”, which reflects the indicators of the invoice issued by LLC “Seller” to the “Commission Agent”. Upon receipt from the SELLER of an invoice dated December 17, 2010 for the shipped goods, Komissioner LLC issues an invoice to Komitent LLC. The example shows all, to put it mildly, the “strangeness” of filling out invoices by an intermediary to the principal (agent). Not every manager, as a person responsible in accordance with the law, will immediately be able to understand that he needs to sign a document that does not contain information (data) about his company. And counter checks on such invoices, as practice has shown, are not so easy to pass. What is the way out of this situation, how can the taxpayer’s situation be alleviated? Let's try to figure it out and give the arguments below.

The commission agent purchases goods for the principal

The essence of the deal is as follows. The principal instructs the commission agent to find a suitable supplier and negotiate with him to ship the goods for the principal. Thus, there are three participants in the transaction. The first is a third-party supplier, the second is the principal (aka the buyer), the third is the commission agent, who is an intermediary between the supplier and the principal.

Document flow of the commission agent

When purchasing goods, the intermediary acts in the interests of the principal. However, according to the agreement concluded between the supplier and the commission agent, all rights and obligations fall on the commission agent (clause 1 of Article 990 of the Civil Code of the Russian Federation). Consequently, in all primary documents, including the invoice, the commission agent is listed as the buyer.

Having received such an invoice from the seller, the intermediary must register it in part 2 of the log of received and issued invoices (clause 11 of the journal rules). There is no need to make an entry in the purchase book, since the goods belong to the consignor, and the commission agent has no right to deduct.

Then the commission agent needs to re-issue the invoice in the name of the principal. The new rules for filling out an invoice describe in detail how to fill out lines 1, 2, 2a, 2b and 5 (see table below). As for the columns of the reissued invoice, they should duplicate the data from the columns of the invoice issued by the supplier in the name of the commission agent.

The reissued invoice must be registered in part 1 of the journal of received and issued invoices (clause 7 of the journal rules). No entry is made in the sales book because the commission agent has no obligation to charge VAT.

What information should be included in the invoice reissued to the principal-buyer?

| Invoice field | What to indicate |

| Line 1 (number and date) | Serial number in accordance with the individual chronology of the commission agent Date of the invoice issued by the seller in the name of the commission agent |

| Line 2 (seller) | Information about the third-party supplier: full or abbreviated name of the organization, or full name of the entrepreneur |

| Line 2a (seller's address) | Location of the third-party supplier: legal address of the organization, or place of residence of the entrepreneur |

| Line 2b (TIN and KPP of the seller) | TIN and PPC of a third-party seller |

| Line 5 (details of the payment document) | Numbers and dates of payment and settlement documents for the transfer of money from the commission agent to a third-party supplier and from the principal to the commission agent |

In addition, the intermediary is obliged to draw up a commission agent’s report (Article 999 of the Civil Code of the Russian Federation). The report must describe what goods and at what price were purchased for the principal, when the payment took place, and what the intermediary’s remuneration is.

Document flow of the principal

The principal receives the invoice re-issued by the commission agent and registers it in part 2 of the journal for recording received and issued invoices (clause 11 of the journal rules).

Then the principal registers the re-issued invoice in the purchase book, and receives the right to accept VAT for deduction.

The principal must keep a copy of the original invoice issued by the supplier in the name of the commission agent for four years. If this document is drawn up in paper form, the intermediary must certify it, and the committent must file it in a folder. If the invoice is issued in electronic form (for example, using the Diadoc system), the commission agent must simply transfer it to the principal via electronic communication channels (subparagraph “a”, paragraph 15 of the journal rules; for the transfer of electronic invoices, see “How will the exchange of electronic invoices take place?”

Please note that the committing party does not need to record a copy of the original invoice in either the journal, purchase ledger, or sales ledger.

If there was an advance payment

When transferring an advance, the supplier issues an invoice in the name of the commission agent. He registers the document in part 2 of the journal, but does not register it in the purchase book.

Then the commission agent reissues the “advance” invoice in the name of the principal, registers it in part 1 of the journal, but does not register it in the sales book.

The principal registers the re-issued invoice for the advance payment in part 2 of the journal, makes an entry in the purchase book and receives the right to deduct VAT from the advance payment. Subsequently, when the products are shipped, the principal will restore the deduction in the usual manner.

Plus, the principal is obliged to file a copy of the “paper” invoice for the advance payment, issued by the supplier in the name of the commission agent and certified by the latter. If the advance invoice is issued in electronic form, the principal must receive it from the commission agent via electronic communication channels. In both cases, the document must be kept for four years.

Commission remuneration

Having completed the transaction, the intermediary receives a reward from the principal. This amount is the commission agent's revenue.

The commission agent issues an invoice for the amount of the remuneration and registers it in part 1 of the log of received and issued invoices. After which the intermediary makes the appropriate entry in the sales book (clause 20 of the rules for maintaining the sales book) and charges VAT for payment to the budget.

The principal registers the same invoice in part 2 of the journal and makes an entry in the purchase book (clause 11 of the rules for maintaining the purchase book). As a result, the principal receives the right to deduct “input” VAT on the services of the commission agent.