We continue the series of articles that are devoted to the legal and tax issues of concluding a contract. The previous article examined in detail the conditions for concluding a work contract, which have the same meaning for both parties to the contract (read more in No. 1 (January) “BUKH.1S”, p. 37). In the material offered, 1C:ITS specialists talk about what taxes the contractor must pay depending on the conditions contained in the contract.

Contract agreements are widely used in practice. It is concluded between organizations to perform various types of work. Let's consider what tax obligations arise for the contractor, who is one of the parties to this agreement.

Payment for work performed

The terms of the contract may provide for different payment procedures for work performed. These conditions affect the rules for calculating taxes for both the contractor and the customer. The customer can pay the contractor before the work begins or after it is completed.

Tax consequences

VAT

If the terms of the agreement provide for payment before the start of execution of the agreement (a separate stage), then VAT must be calculated and paid from the amount of the advance received (clause 2, clause 1, article 167 of the Tax Code of the Russian Federation). In this case, no later than five calendar days from the date of receipt of the advance payment, the contractor must issue the customer an “advance” invoice for this amount (clause 3 of Article 168 of the Tax Code of the Russian Federation).

After the work is completed (stage of work) and the acceptance certificate is signed, the contractor, on the basis of paragraph 14 of Article 167 of the Tax Code of the Russian Federation, again has the moment of determining the tax base for VAT. Therefore, he must also calculate VAT on the cost of the work performed and issue a “shipping” invoice to the customer. At the same time, he can submit the VAT paid on the advance payment for deduction from the budget (clause 8 of Article 171, clause 6 of Article 172 of the Tax Code of the Russian Federation).

If the customer transfers funds to the contractor after completion of the work, then he calculates VAT in relation to these works once on the date of signing the acceptance certificate for the work performed. Accordingly, he issues an invoice to the customer once.

Income tax

The procedure for reporting funds received from the customer in income for profit tax purposes depends on what method of income recognition the contractor uses.

If the contractor uses the accrual method, then income is recognized on the date of signing the acceptance certificate for the work performed, regardless of whether funds were actually received from the customer on this date or not (clauses 1, 3 of Article 271 of the Tax Code of the Russian Federation). This means that prepayment amounts received from the customer are not included in income until the completion of the work (clause 1, clause 1, article 251 of the Tax Code of the Russian Federation).

If the contractor uses the cash method, then the moment of recognition of revenue in income does not depend on the date of signing the acceptance certificate for the work performed. For such a contractor, revenue is included in income on the date of receipt of funds from the customer (clause 1, clause 1, article 251 of the Tax Code of the Russian Federation, clause 2, article 273 of the Tax Code of the Russian Federation).

Construction of fixed wiring facilities

Manufacturing enterprises, as a rule, carry out the construction of fixed assets (workshops, warehouses for finished products, etc.) in a mixed way: economically and with the involvement of contract construction organizations.

In this case, how is the initial cost of fixed assets formed in accounting and tax accounting? How to calculate VAT on the cost of construction and installation work performed? Let's look at this situation with an example.

Example. The manufacturing enterprise OJSC Zenit built a warehouse for finished products. At the same time, construction and installation work was carried out independently, as well as with the involvement of a construction organization - a contractor.

In January 2004, the company purchased construction materials. One part of them costs 236,000 rubles. (including VAT - 36,000 rubles) were handed over to the contractor to carry out construction and installation work.

Another part worth 177,000 rubles. (including VAT - 27,000 rubles) were used during construction using self-sustaining methods. In June, the contractor completed the work and signed a work acceptance certificate (Form N KS-3) for the total cost of the work - 708,000 rubles.

(including VAT - 108,000 rubles).

In June, wages were accrued to production workers who built the warehouse using self-employed methods - 50,000 rubles. Unified social tax in the amount of 17,800 rubles was accrued for this salary. (including contributions for compulsory pension insurance - 7,000 rubles) and contributions for compulsory accident insurance - 1,000 rubles.

In June, depreciation was accrued on production equipment involved in construction and installation work using self-employed methods - 20,000 rubles.

Construction was completed that same month. An act of acceptance of the completed construction of the facility and the commissioning of the finished product warehouse was signed (Form N KS-11).

Accounting

In accounting, the initial cost of fixed assets during their self-construction is determined based on the organization’s actual costs for their construction and production, with the exception of value added tax and other refundable taxes (except for cases established by the legislation of the Russian Federation). This is stated in paragraph 24 of the Methodological Guidelines for Accounting of Fixed Assets.

According to paragraph 3 of paragraph 1 of Article 146 of the Tax Code of the Russian Federation, the object of income tax is the performance of construction and installation work for one’s own needs. What applies to such work is explained in paragraph 3.

2 Methodological recommendations for the application of Chapter 21 “Value Added Tax” of the Tax Code of the Russian Federation (approved by Order of the Ministry of Taxes of Russia dated December 20, 2000 N BG-3-03/447).

Thus, such work should include only construction and installation work that is carried out in an economic way. Therefore, VAT must be charged on their cost. But there is no need to charge VAT on the cost of construction and installation work that is carried out by contract.

By the way, the courts adhere to a similar position. Look, for example, at the Resolution of the Federal Arbitration Court of the Ural District dated September 10, 2003 N F09-2906/03-AK.

It turns out that in order to correctly calculate the tax base for VAT, it is necessary to separate the costs of construction and installation work by a contractor and the costs of the enterprise for the construction of fixed assets using self-employed methods. Therefore, such expenses must be collected in separate sub-accounts to account 08 “Investments in non-current assets”.

The following entries will be made in the company's accounting records to account for the construction of a fixed asset facility using an economic method.

In January 2004:

Debit 10 subaccount “Construction materials for contract work” Credit 60

- 200,000 rub. — materials have been capitalized for transfer to the contractor;

Debit 19 Credit 60

- 36,000 rub. — the amount of VAT on materials is taken into account;

Debit 10 subaccount “Building materials for household use” Credit 60

- 150,000 rub. — materials were capitalized for use in self-construction;

Debit 19 Credit 60

- 27,000 rub. — the amount of VAT on materials is taken into account;

Debit 60 Credit 51

- 413,000 rub. (236,000 + 177,000) - materials paid to the supplier;

Debit 10 subaccount “Construction materials transferred to third parties” Credit 10 subaccount “Construction materials for contract work”

- 200,000 rub. — materials were transferred to the contractor;

Debit 08 subaccount “Construction of fixed assets/contract” Credit 10 subaccount “Construction materials transferred to third parties”

- 200,000 rub. — the cost of materials transferred to the contractor is included in construction costs.

In June:

Debit 08 subaccount “Construction of fixed assets/contract” Credit 60

- 600,000 rub. — the cost of work performed by the contractor is included in construction costs;

Debit 19 Credit 60

- 108,000 rub. — reflects the amount of VAT on work performed by the contractor;

Debit 60 Credit 51

- 708,000 rub. — the debt to the contractor has been repaid;

Debit 08 sub-account “Construction of fixed assets/economic means” Credit 10 sub-account “Building materials for economic means”

- 150,000 rub. — the cost of materials used during self-construction is included in construction costs;

Debit 08 subaccount “Construction of fixed assets/economic means” Credit 02

- 20,000 rub. — depreciation was accrued on production equipment used during self-construction;

Debit 08 subaccount “Construction of fixed assets/economic means” Credit 70

- 50,000 rub. — the salary of the enterprise’s personnel is included in construction costs;

Debit 08 subaccount “Construction of fixed assets/economic means” Credit 69

- 18,800 rub. (17,800 + 1000) — social tax and contributions for compulsory accident insurance have been accrued;

Debit 01 Credit 08 subaccount “Construction of fixed assets/contract”

- 800,000 rub. (200,000 + 600,000) — the warehouse was put into operation;

Debit 01 Credit 08 subaccount “Construction of fixed assets/economic means”

- RUB 238,800 (150,000 + 50,000 + 18,800 + 20,000) - the warehouse was put into operation.

The initial cost of the finished goods warehouse will be:

800,000 rub. + 238,800 rub. = 1,038,800 rub.

The date of completion of construction and installation work for one’s own consumption is determined as the day the corresponding object is registered (Clause 10, Article 167 of the Tax Code of the Russian Federation). Thus, this is the date of signing the act of acceptance of the completed construction facility (Form N KS-11) and its commissioning.

According to clause 6 of Article 171 of the Tax Code of the Russian Federation, the developer has the right to reduce the accrued amount of tax by the amount of VAT:

- presented to him by contractors when they carried out construction and installation work and paid to these organizations;

- for goods (works, services) purchased for construction and installation work and paid to suppliers;

- accrued on the cost of construction and installation work performed on a self-employed basis and paid to the budget.

The first two deductions are provided from the 1st day of the month following the month in which the constructed fixed asset facility was put into operation (clause 5 of Article 172 of the Tax Code of the Russian Federation).

In addition, if the constructed object belongs to real estate, then the deduction for it is provided from the 1st day of the month following the month of filing documents for state registration of ownership of this real estate.

It is from this moment that real estate is included in one of the depreciation groups in tax accounting in accordance with clause 8 of Article 258 of the Tax Code of the Russian Federation.

As for the third deduction, it can be made only after the VAT accrued on the cost of construction and installation work performed on a self-employed basis has been paid.

Construction of fixed assets. Postings

This follows from clause 5 of Article 172 of the Tax Code of the Russian Federation.

The accountant of OJSC Zenit reflected the VAT deduction with the following entries.

In July:

Debit 68 subaccount “VAT calculations” Credit 19

- 63,000 rub. (36,000 + 27,000) - accepted for deduction of VAT on materials used in construction and installation work;

Debit 68 subaccount “VAT calculations” Credit 19

- 108,000 rub. — accepted for deduction of VAT on construction and installation work performed by the contractor;

Debit 19 Credit 68 subaccount “VAT calculations”

- RUB 42,984 (RUB 238,800 x 18%) - VAT is charged on the cost of construction and installation work performed on a self-employed basis.

In August:

Debit 68 subaccount “VAT calculations” Credit 51

- RUB 42,984 — VAT is transferred to the budget on the cost of construction and installation work according to the submitted declaration for July;

Debit 68 subaccount “VAT calculations” Credit 19

- RUB 42,984 — VAT is accepted for deduction on the cost of construction and installation work performed on a self-employed basis.

The enterprise has established in accounting and tax accounting the useful life of the warehouse as 80 months based on the Classification of fixed assets included in depreciation groups.

The organization uses the straight-line depreciation method in both accounting and tax accounting. To pay off the cost of a fixed asset, you need to determine the annual amount of depreciation.

When determining it, it is necessary to pay special attention to fixed assets that were put into operation during the year. For them, the annual amount of depreciation is calculated only for those months in which the object was operated (with the exception of the month in which the object was put into operation).

Therefore, in our case, the annual amount of depreciation charges in 2004 will be as follows:

RUB 1,038,800 : 80 months x 6 months = 77,910 rub.

And the amount of monthly depreciation deductions:

RUR 77,910 : 6 months = 12,985 rub/month.

In accounting, depreciation is accrued from the 1st day of the month following the month the object was accepted for accounting. This is stated in paragraph 21 of the Accounting Regulations “Accounting for Fixed Assets” PBU 6/01, approved by Order of the Ministry of Finance of Russia dated March 30, 2001 N 26n.

In July 2004, the accountant of OJSC Zenit showed depreciation for the warehouse in accounting as follows:

Debit 20 Credit 02

- RUB 12,985 — depreciation was accrued for the finished goods warehouse for July.

Tax accounting

To determine the initial cost of a fixed asset, the norm of clause 1 of Article 257 of the Tax Code of the Russian Federation is used in tax accounting.

https://www.youtube.com/watch?v=yAFEnTPWKlw

According to this clause, the initial cost of a fixed asset must include all costs associated with its construction and bringing it to a condition suitable for use. But VAT, which can be deducted, is not included in the initial cost.

Also, it is not necessary to include social tax, compulsory pension insurance contributions and accident insurance contributions accrued on the salaries of production personnel in the initial cost of a fixed asset. The fact is that all these contributions, according to paragraph 1 of clause 1 of Article 264 of the Tax Code of the Russian Federation, are included in other expenses.

The initial cost of the finished goods warehouse in tax accounting will be:

RUB 1,038,800 — 17,800 rub. — 1000 rub. = 1,020,000 rub.

Depreciation is calculated on fixed assets in tax accounting according to the depreciation rate determined based on the established useful life. Accrual begins on the 1st day of the month following the month in which the fixed asset was put into operation (clause 2 of Article 259 of the Tax Code of the Russian Federation).

When applying the straight-line method, the monthly depreciation rate will be equal to:

(1: 80 months) x 100% = 1.25%.

And the amount of monthly depreciation charges in 2004:

RUB 1,020,000 x 1.25% = 12,750 rub.

The amount of monthly depreciation deductions in accounting is greater than in tax accounting by 235 rubles. (12,985 - 12,750). This results in a permanent tax liability being recorded. Its value is equal to the product of the difference between accounting and tax depreciation and the income tax rate.

This is stated in paragraph 7 of the Accounting Regulations “Accounting for income tax calculations” PBU 18/02, approved by Order of the Ministry of Finance of Russia dated November 19, 2002 N 114n.

In the accounting in the same months when depreciation on the fixed asset will be calculated, a permanent tax liability must be reflected:

Debit 99 Credit 68 subaccount “Calculations for income tax”

- 56.4 rub. (RUB 235 x 24%) - permanent tax liability is taken into account.

M.A. Vishnevskaya

Auditor

CJSC "Aktiv"

Accounting entries upon receipt of fixed assets

Source: https://buh-experts.ru/stroitelstvo-osnovnyh-sredstv-provodki/

Accounting entries in construction

Due to the specifics of the industry, analytical accounting on this account is carried out in the context of the technological structure of expenses:

- other construction costs.

- design, survey and geodetic work;

- direct construction work;

- equipment, tools, inventory that do not require installation;

- installation of equipment;

One of the main entities involved in the construction process is the contractor - a construction company that performs work under a contract concluded with the developer.

The procedure for concluding such an agreement is regulated by the Civil Code of the Russian Federation, according to which work can be performed either directly by the contractor or by involved persons (subcontractors).

The basis for the delivery and acceptance of work performed under a contract is an act approved and signed by each party. A construction company can carry out

Accounting and taxation of construction and installation works carried out on an economic basis

These do not include:

- individual volumes of work performed by contractors during construction as a whole in an economic way.

- work performed by contractors for their own construction. The scope of such work is included in the scope of work performed by contract;

- work performed by shops of the main activity under contracts and agreements with OKS of the same organization, when payments for work performed are made in the manner established for contractors;

In the course of carrying out work on a self-employed basis, the organization may need to obtain appropriate licenses.

Performing the functions of a customer is not included in the list of works that constitute licensed types of construction activities. According to Article 17 of the Federal Law of 08.08.2001 N 128-FZ “On Licensing of Certain Types of Activities” the design and

How to record contract construction of fixed assets in accounting

The integral parts of such an agreement are:

- technical documentation, which indicates the composition and scope of work, as well as the requirements for these works;

- an estimate that determines the cost of contract work.

This follows from the provisions of Articles 740, 743, 746 of the Civil Code of the Russian Federation.

Fixed assets constructed by contract are accepted for accounting at their original cost (clause 7 of PBU 6/01). Include in the initial price:

- amounts paid to the contractor in accordance with the contract;

- amounts paid for information and consulting services related to the creation of fixed assets;

- the amount of VAT claimed (if the fixed asset will not be used in activities subject to this tax);

- other expenses directly related to the creation (for example, the cost of purchased materials; equipment intended for installation at the facility; costs of examining the safety of the facility, etc.

)

Costs associated with the work

In the process of performing work, the contracting organization bears costs.

Such expenses, in particular, include the cost of purchasing materials necessary to complete the work, paying wages to employees, transportation costs, etc.

Tax consequences

VAT

VAT paid on the purchase of materials, etc., can be deducted by the contractor if the necessary conditions are met, that is, if the materials are purchased for activities subject to VAT, an invoice is received from the supplier of the materials and the materials are registered.

Income tax

Expenses associated with the performance of work are reflected in the contractor's tax records as follows.

A contractor who uses the accrual method and whose expenses are divided into direct and indirect, assigns direct expenses to the current expenses of the reporting (tax) period in which revenue from the work is recognized. In this case, indirect expenses in full relate to the expenses of the reporting (tax) period in which they were incurred (clause 2 of Article 318 of the Tax Code of the Russian Federation).

A contractor using the cash method recognizes costs associated with the performance of work as expenses after their actual payment, regardless of the recognition of revenue from the work (clause 3 of Article 273 of the Tax Code of the Russian Federation).

Construction by contract wiring

To formalize the acceptance of the object, the commission draws up an Acceptance Certificate for the completed construction of the object. The act provides a description of the object to be put into operation. All necessary technical documentation is attached to the act.

Based on the documentation on the acceptance of the object into operation, an Act on the acceptance and transfer of the building (structure) is drawn up (form No. OS-1a). On the basis of this act, objects come under D account 01. Carrying out construction and installation work for one’s own consumption is subject to VAT of 18% (Article 146 of the Tax Code of the Russian Federation).

VAT on the cost of construction and installation work is calculated at the end of each tax period. The VAT amount is calculated at a rate of 18% of the cost of construction and installation work (OD invoice 08 multiplied by 18%). VAT on construction and installation work is deductible in the same quarter.

The amount of VAT is accepted for deduction if the following conditions are met: 1) The object is intended for carrying out operations subject to VAT

Accounting and tax accounting of operations under a construction contract

173.

— act of acceptance of the completed construction of the facility by the acceptance committee (Form N KS-14); — act of suspension of construction (form N KS-17); — act on the suspension of design and survey work for uncompleted construction (Form N KS-18).

The forms used in the organization (including additional details) are usually filed as appendices to the order on accounting policies.

The main document in which records are kept of construction and installation work performed is the general work log (Form N KS-6). This log is maintained throughout the duration of the work.

Account 08 in accounting: entries for accounting for investments in non-current assets

investments cost of building materials transferred for the construction of the warehouse in April 03/08 70 (69) 95 000 The salary (including insurance contributions) of employees involved in the construction of the warehouse in April 01/08 is reflected in capital investments.

03 600 000 Accepted for accounting and put into operation a self-constructed industrial warehouse (250,000.00 + 105,000.00 + 150,000.00 + 95,000.00) Transfer-acceptance certificate (OS-1), Inventory accounting card (OS-6) 19 68 108 000 Reflects accrued VAT on construction work performed in an economic way ((250,000.00 + 105,000.00 + 150,000.00 + 95,000.00) * 18%) Invoice received.

Purchase book 68 19 108 000 Accrued VAT on construction work performed in an economic way has been accepted for deduction. Let's say VESNA LLC entered into an agreement with a contractor for the construction of a facility - an industrial warehouse.

According to the contractor's financial estimates, the costs of constructing an industrial warehouse were: The cost of services for preparing estimates is 59,000 rubles, incl.

How to register and record the construction (manufacturing) of fixed assets using economic methods

Draw up an inventory card on the basis of the act and primary documents.

No. 7. Attention: the absence (failure to submit) of primary documents for accounting of fixed assets is an offense (Article 106 of the Tax Code of the Russian Federation, Article 2.1 of the Code of Administrative Offenses of the Russian Federation), for which it is provided. Fixed assets constructed on an economic basis are accepted for accounting at their original cost (clause

7 PBU 6/01). Include in the initial cost all costs directly related to the manufacture of the object (clause 8 of PBU 6/01, clause 5.1.1 of the Regulations approved by the Ministry of Finance of Russia on December 30, 1993

№ 160)

2.2.1 Accounting for contract construction

invoices.

At the same time, the capital construction project must be used in the future to carry out operations subject to VAT.

The costs of the developer's organization for construction were: the cost of work on drawing up the estimate - 118,000 rubles, including VAT - 18,000 rubles; the cost of construction work according to the contractor's invoices is 1,180,000 rubles.

, including VAT - 180,000 rubles; Costs for the construction of the facility in the developer's accounting are reflected in the following entries: No. of business transactions Correspondence of accounts Amount, rub. Debit Credit Private General 1.

The cost of services of a third-party organization for drawing up an estimate is reflected 08-3 100000 19-18000 2. The cost of construction work is reflected in accordance with the Certificate of the cost of work performed and expenses (form No. KS-3), presented by the contractor 08-3 1000000 19-1 180000 60 1180000 3 .

Submitted to the budget for deduction of VAT on work performed by a third-party organization and contractor; 68 19-1 198000 Example An organization is carrying out capital construction of a workshop by contract.

In April 2010, the contractor completed the next stage of construction work, for which documents were drawn up in form No. KS-2 “Acceptance Certificate of Work Completed” and No. KS-3 “Certificate of the Cost of Work Performed and Expenses” in the amount of 591,143 rubles.

, including VAT -90,174.36 rubles, and an invoice is also provided.

The following entries must be made in the accounting: No. of business transactions Correspondence of accounts Amount, rub.

Debit Credit Private Total 1. Reflects the cost of the stage of work completed by the contractor and accepted 08-3 500 968.64 19-1 60 90174.36 591143 2. Presented to the budget for deduction of VAT on the stage of work completed and accepted by the contractor 68 19-1 90174.36 Page 3 of 8 Adjacent files in an item

- 12/22/2018112.64 Kb

Source: https://konsalt74.ru/stroitelstvo-podrjadnym-sposobom-provodki-67731/

Reimbursement of expenses by the customer

The contract may provide that in addition to paying the cost of the work, the customer compensates the contractor for expenses that do not directly relate to the performance of the work, but without which it is impossible to complete the work. For example, travel expenses to the place of work, living expenses, etc. Are compensation amounts included in the tax base for VAT and income tax for the contractor?

Tax consequences

VAT

Chapter 21 of the Tax Code of the Russian Federation does not contain an answer to this question. However, there are two points of view on this issue.

Thus, in the opinion of the regulatory authorities, the contractor must include the reimbursement amounts received from the customer in the tax base for value added tax, since they are related to payment for work performed.

It does not matter that in contracts these expenses may be indicated separately from the cost of these works. The amounts are included in the tax base in the tax period in which the funds are received, and VAT on them is calculated at the rate of 18/118 (letter of the Ministry of Finance of Russia dated March 2, 2010 No. 03-07-11/37, dated November 9, 2009 No. 03- 07-11/288, etc.).

Some arbitration courts do not agree with this position. They believe that since the amounts of compensation received do not increase the cost of the work performed, then, therefore, they do not relate to the amounts that are associated with payment for these works, and therefore should not be included in the tax base for value added tax (resolutions of the Federal Antimonopoly Service of the North-West District dated 08/25/2008 in case No. A42-7064/2007, FAS Volga-Vyatka District dated 02/19/2007 in case No. A17-1843/5-2006, FAS East Siberian District dated 03/10/2006 No. A33-20073/04- S6-F02-876/05-S1 in case No. A33-20073/04-S6).

Since there is no clear answer to the question, the contractor will have to make the appropriate decision on his own. Moreover, if the contractor will charge VAT on the compensation amount, then he can issue an invoice in one of two ways. In the first case, the invoice is issued in one copy and is not presented to the customer. In the second case, the contractor issues an invoice in two copies, one of which is presented to the customer. Based on this invoice, the customer will be able to deduct VAT. Note that the second option is somewhat risky, since, according to regulatory authorities, the contractor does not have the right to issue an invoice to the customer for the amount of reimbursable expenses. The reason is that there is no sale of goods (works, services).

At the same time, the courts believe that the presentation of an invoice is possible (see decisions of the FAS North Caucasus District dated January 13, 2010 No. A53-9707/2009, dated January 20, 2009 No. A53-10111/2008-C5-44, FAS Moscow District dated 04/27/2010 No. KA-A40/4081-10, Federal Antimonopoly Service of the Ural District dated 05/25/2009 No. F09-3324/09-S3).

If the contractor does not include the reimbursement amounts in the VAT tax base, then he will not be able to deduct the VAT charged to him for these expenses by suppliers for the following reason. As you know, one of the conditions that must be met to deduct VAT is that the purchased goods (work, services) must be used in taxable activities. If these expenses are compensated by the customer, but are not included by the contractor in the VAT tax base, then it turns out that these expenses do not participate in taxable activities. Accordingly, VAT should not be deducted on such expenses.

Income tax

In Chapter 25 of the Tax Code of the Russian Federation there are no rules governing the procedure for recognizing for profit tax purposes the amounts that taxpayers receive as reimbursement of expenses. At the same time, in our opinion, the contractor should reflect them in tax accounting taking into account the following.

If the contractor includes costs that will be reimbursed by the customer as expenses, then he must recognize the received reimbursement amounts in income. If these costs are not included in tax accounting expenses, then the amounts reimbursed by the customer should not be reflected in income.

Implementation of installation work

Proceeds from the sale of work are recognized as income from sales (clause 1 of Article 249 of the Tax Code of the Russian Federation).

The implementation of installation work is reflected in the document Sales (act, invoice) transaction type Services in the section Sales – Sales – Sales (acts, invoices) – Sales – Services (act).

Let's consider the features of filling out the Implementation document (act, invoice) according to this example.

In the Accounting account , you must indicate the Nomenclature group to which the costs of equipment installation are allocated. If you specify the required analytics incorrectly, then account 20.01 “Fixed asset” may not be closed correctly!

Postings according to the document

Income tax return

In the income tax return, income from the sale of work is reflected as follows: PDF

- Sheet 02 Appendix No. 1 page 011 “Proceeds from the sale of goods (works, services) of own production.”

Issuance of SF for sale to the buyer

An invoice for work performed is issued using the Issue an invoice at the bottom of the document Sales (act, invoice) .

The Invoice document issued is automatically filled in with the data from the Sales document (act, invoice) .

- Operation type code : “Sales of goods, works, services.”

The issued invoice is automatically reflected in the Sales Book.

Sales Book report can be generated from the Reports – VAT – Sales Book section. PDF

VAT declaration

The VAT return reflects:

In Section 3 page 010 “Implementation...”: PDF

- sales amount excluding VAT;

- the amount of accrued VAT at a rate of 18%.

In Section 9 “Information from the sales book”:

- invoice issued, transaction type code "".

Elimination of deficiencies in completed work

Sometimes, after completion of the work, the customer identifies shortcomings in the work performed and turns to the contractor with a demand to eliminate them. As a rule, the contractor eliminates these deficiencies free of charge. As a result of performing such work, he is faced with two questions: is it necessary to calculate VAT on the cost of gratuitous work and can the costs associated with the performance of this work be taken into account when taxing profits?

Tax consequences

VAT

In this case, the object of VAT taxation does not arise. The fact is that by eliminating deficiencies free of charge, the contractor, in fact, fulfills the obligations assumed under the contract. In turn, the cost of work under this agreement is already included in the VAT tax base. Therefore, there is no need to charge and pay VAT on the cost of “corrective” work.

Income tax

As for the recognition for profit tax purposes of the costs incurred by the contractor when carrying out work to eliminate deficiencies, they can be included in expenses in tax accounting on the basis of subparagraph 47 of paragraph 1 of Article 264 of the Tax Code of the Russian Federation as losses from defects.

Features of tax accounting

The duration of the contract is taken into account not only in accounting, but also in tax accounting. If we are talking about short-term cooperation between a subcontractor and a customer, work in progress is formed based on direct costs. For tax purposes, indirect costs are taken into account. Proceeds from sales are reflected in tax accounting one-time - after the completion of the project. Expenses incurred during work in progress are recognized in the same way.

For long-term contracts, a different scheme applies. The specifics of legal relations provide for the recognition of revenue from sales based on the results of reporting periods. This norm is enshrined in the Tax Code of the Russian Federation (Articles 271-272). The methodology for calculating revenue is determined by the accounting policy of the subcontracting construction organization.

Theoretically, the methods in accounting and tax accounting may differ. But in practice, such a scheme complicates accounting. If the same methodology is used here and there, work in progress can only be determined in accounting. For tax purposes, all expenses for performing work are recognized.

It is recommended that the subcontractor's accountant pay special attention to VAT. Certain operations may not be taxed (restoration, for example). Accordingly, in such cases, VAT is not charged on sales.

In general, the subcontractor’s accounting and tax records are carried out according to the same rules as in any other company. But knowledge of the specifics of the industry will not harm an accountant.

Is it possible to do without a specialist and keep records yourself? If you want to receive reliable data on financial results, then no. Mistakes made are fraught not only with distortion of operational information, but also with fines for failure to fulfill tax obligations. To minimize risks, collaborate with industry accounting experts.

Source

The customer refused to fulfill the contract

The customer may refuse to fulfill the contract for various reasons. Moreover, this can happen when some of the work has already been completed. The contractor's tax obligations in case of such a refusal depend on whether he received an advance payment for the work performed or not.

Tax consequences

VAT

If the customer refuses to fulfill the contract when part of the work has already been completed, then he must pay the contractor for the work actually performed. The contractor, in turn, must calculate VAT on the cost of these works in the generally established manner. Moreover, if under such an agreement the contractor received an advance payment from the customer and paid VAT on it to the budget, then, when deducting this VAT at the time of calculating the tax on the cost of work performed, he must remember the following.

If the amount of the advance received does not exceed the cost of the work actually performed, then value added tax is deducted in full amount as of the date of tax calculation on the cost of the work actually performed. If the amount of the prepayment exceeds the cost of the work actually performed, the contractor first transfers the corresponding part of the prepayment to the customer, reflects this operation in accounting, and only after that deducts “advance” VAT (clause 5 of Article 171, clause 4 of Article 172 of the Tax Code of the Russian Federation ).

Income tax

The cost of the work actually performed, paid by the customer in the event of refusal to fulfill the contract, is the contractor’s proceeds from the implementation of the work. Under the accrual method, it is included in income for tax purposes in the period in which part of the work is completed and the relevant documents are signed (clause 1, article 39, clause 3, article 271 of the Tax Code of the Russian Federation).

Moreover, if the customer made an advance payment to the contractor, then the income includes an amount corresponding to the cost of the work performed.

A contractor using the cash method includes the advance in income on the date the cash is actually received. Therefore, if the customer refuses the contract, he must exclude from income the amount of the advance payment that exceeds the cost of the work actually performed.

So, we have looked at the tax consequences of entering into a contract for a contractor.

In the next issue we will talk about the tax obligations that arise when concluding an agreement with the customer.

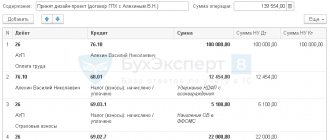

All information provided can be found in the ITS PROF system in the Handbook of Contractual Relations in the “Legal Support” section (see figure).

Rice. 1

How to formalize and record the income and expenses of a general contractor

- 3.

- 1.

- 6.

- 8.

- 2.

- 4.

- 7.

- 5.

If the construction contract does not provide for the contractor’s obligation to perform construction work independently, then the contractor may involve third parties to perform certain construction works. In this case, the contractor is, and the third parties involved by him are. At the same time, the general contractor is responsible to the developer for performing the entire range of works on the construction of the facility, including work performed by subcontractors. The general contractor can:

- carry out some of the work on our own, and some with the involvement of subcontractors;

- completely transfer the execution of construction work to subcontractors.

This is stated in Article 706 of the Civil Code of the Russian Federation. The relationship between the general contractor and the subcontractor is regulated by a construction subcontract agreement, to which the rules of Chapter 37 of the Civil Code of the Russian Federation apply.

The subcontractor is responsible to the general contractor for the quality of work, in particular, for violations of the requirements of technical documentation, building codes and regulations binding on the parties (clause 1 of Article 754 of the Civil Code of the Russian Federation). The general contractor is responsible to the developer for the consequences of non-fulfillment or improper fulfillment of obligations by the subcontractor, and to the subcontractor for the non-fulfillment or improper fulfillment of obligations by the developer under the contract.

At the same time, the developer and the subcontractor do not have the right to present claims to each other related to the violation of contracts concluded by each of them with the general contractor. Such rules are established in paragraph 3 of Article 706 of the Civil Code of the Russian Federation.

Proceed in a similar manner for the delivery and acceptance of work performed by the subcontractor.

The cost of construction and installation work accepted by the general contractor and performed by the subcontractor under a subcontract agreement is included in expenses for ordinary activities (clause 5 of PBU 10/99, clause 10 of PBU 2/2008).

Basis for reflecting the cost

Payment for work performed

The terms of the contract may provide for different payment procedures for work performed. These conditions affect the rules for calculating taxes for both the contractor and the customer. The customer can pay the contractor before the work begins or after it is completed.

Tax consequences

VAT

If the terms of the agreement provide for payment before the start of execution of the agreement (a separate stage), then VAT must be calculated and paid from the amount of the advance received (clause 2, clause 1, article 167 of the Tax Code of the Russian Federation). In this case, no later than five calendar days from the date of receipt of the advance payment, the contractor must issue the customer an “advance” invoice for this amount (clause 3 of Article 168 of the Tax Code of the Russian Federation).

After the work is completed (stage of work) and the acceptance certificate is signed, the contractor, on the basis of paragraph 14 of Article 167 of the Tax Code of the Russian Federation, again has the moment of determining the tax base for VAT. Therefore, he must also calculate VAT on the cost of the work performed and issue a “shipping” invoice to the customer. At the same time, he can submit the VAT paid on the advance payment for deduction from the budget (clause 8 of Article 171, clause 6 of Article 172 of the Tax Code of the Russian Federation).

If the customer transfers funds to the contractor after completion of the work, then he calculates VAT in relation to these works once on the date of signing the acceptance certificate for the work performed. Accordingly, he issues an invoice to the customer once.

Income tax

The procedure for reporting funds received from the customer in income for profit tax purposes depends on what method of income recognition the contractor uses.

If the contractor uses the accrual method, then income is recognized on the date of signing the acceptance certificate for the work performed, regardless of whether funds were actually received from the customer on this date or not (clauses 1, 3 of Article 271 of the Tax Code of the Russian Federation). This means that prepayment amounts received from the customer are not included in income until the completion of the work (clause 1, clause 1, article 251 of the Tax Code of the Russian Federation).

If the contractor uses the cash method, then the moment of recognition of revenue in income does not depend on the date of signing the acceptance certificate for the work performed. For such a contractor, revenue is included in income on the date of receipt of funds from the customer (clause 1, clause 1, article 251 of the Tax Code of the Russian Federation, clause 2, article 273 of the Tax Code of the Russian Federation).

Postings for settlements with suppliers and contractors

The activities of any enterprise are in one way or another connected with the acquisition of goods and services. Suppliers and contractors include enterprises that supply materials, raw materials and other goods and materials, as well as providing various services or performing various types of work. Let's look at typical transactions for settlements with suppliers and contractors in accounting.

Receipt of material assets, works, services from suppliers is carried out on the basis of concluded contracts for supply, contract, assignment, electricity supply, etc. The primary documents for accounting for settlements with contractors include invoices (TORG-12), acts of provision of services, invoices and others documents issued by contractors and suppliers, as well as bank and cash payment documents: To reflect information about settlements made with suppliers, a separate accounting account – 60 is used.

This account is active-passive, so in accounting it can be displayed both in credit and debit turnover:

- The loan takes into account the cost of purchased goods and services. Lending is carried out on the basis of settlement documents received from the supplier.

- The debit of this account displays the amounts of fulfilled obligations - advance payments and full mutual settlement. It should be noted that the amounts of payments made are taken into account separately.

Analytical accounting is carried out in the context of presented invoices. In addition, proper accounting for this account allows you to group suppliers by payment terms, uninvoiced deliveries, bill transactions, etc. Account Dt Account Kt Transaction amount, rub.

Description of the posting Document-basis Postings and transactions reflected in debit 60 of account 60 50 17 500 From the cash desk of the enterprise, payment was made to the supplier for the material received (posting) RKO 60 51 (52) 54 000 Payment was made to the provider of non-cash payment services in national (foreign) currency Payment order, bank statement 60 55-1 37 900 Written off

Costs associated with the work

In the process of performing work, the contracting organization bears costs.

Such expenses, in particular, include the cost of purchasing materials necessary to complete the work, paying wages to employees, transportation costs, etc.

Tax consequences

VAT

VAT paid on the purchase of materials, etc., can be deducted by the contractor if the necessary conditions are met, that is, if the materials are purchased for activities subject to VAT, an invoice is received from the supplier of the materials and the materials are registered.

Income tax

Expenses associated with the performance of work are reflected in the contractor's tax records as follows.

A contractor who uses the accrual method and whose expenses are divided into direct and indirect, assigns direct expenses to the current expenses of the reporting (tax) period in which revenue from the work is recognized. In this case, indirect expenses in full relate to the expenses of the reporting (tax) period in which they were incurred (clause 2 of Article 318 of the Tax Code of the Russian Federation).

A contractor using the cash method recognizes costs associated with the performance of work as expenses after their actual payment, regardless of the recognition of revenue from the work (clause 3 of Article 273 of the Tax Code of the Russian Federation).

Provision of services - accounting entries accounting for the provision of services

» » Accounting entries for services Accounting entries for transport services Accounting entries for sales of services The source of income for an enterprise can be not only the sale of goods, but also the provision of services.

This activity has its own characteristics. And this, naturally, is reflected in the accounting. Accounting entries for services for the customer and the contractor will, naturally, be different. The service provider uses account 90 “Sales” for this purpose. On it, actual expenses are taken into account as a debit, and as a credit, the revenue received is taken into account in accordance with the established tariffs.

From the very specifics of the operation it follows that account 43 “Finished products” is not used in this case. After all, services are always transferred directly to the client. The answer to the question whether account 40 is used in this case (that is, “Output of products (services)”) depends on whether the enterprise uses the planned cost in current accounting.

Accordingly, the accounting entries for services in this case look like this: the amount of revenue from the debit of account 62 is transferred to the credit of account 90 (under subaccount 90-1). This is how the debt for services rendered is reflected.

The actual cost is taken into account by posting Debit 90-2 – Credit 20 “Main production” (or account 23). If the company pays VAT, then it is necessary to reflect the tax accrual - posting Debit 90 (under subaccount 3) - Credit 68 (under the subaccount of the corresponding tax). When the buyer pays for the services, this will be reflected by an entry in which the amount of debt will be written off to the debit of account 51 from the credit of account 62.

Otherwise, the purchase of services from the customer is reflected. The costs of their purchase must be taken into account in accordance with PBU 10/99.

Expenses that are generated for ordinary activities include all costs for the acquisition of services, except those related to the creation or purchase of fixed assets or other non-current assets. As for the accounting entries for services directly, settlements with the contractor are reflected by entries Debit 60 - Credit 51 (this entry is made on the basis of a bank statement).

Reimbursement of expenses by the customer

The contract may provide that in addition to paying the cost of the work, the customer compensates the contractor for expenses that do not directly relate to the performance of the work, but without which it is impossible to complete the work. For example, travel expenses to the place of work, living expenses, etc. Are compensation amounts included in the tax base for VAT and income tax for the contractor?

Tax consequences

VAT

Chapter 21 of the Tax Code of the Russian Federation does not contain an answer to this question. However, there are two points of view on this issue.

Thus, in the opinion of the regulatory authorities, the contractor must include the reimbursement amounts received from the customer in the tax base for value added tax, since they are related to payment for work performed.

It does not matter that in contracts these expenses may be indicated separately from the cost of these works. The amounts are included in the tax base in the tax period in which the funds are received, and VAT on them is calculated at the rate of 18/118 (letter of the Ministry of Finance of Russia dated March 2, 2010 No. 03-07-11/37, dated November 9, 2009 No. 03- 07-11/288, etc.).

Some arbitration courts do not agree with this position. They believe that since the amounts of compensation received do not increase the cost of the work performed, then, therefore, they do not relate to the amounts that are associated with payment for these works, and therefore should not be included in the tax base for value added tax (resolutions of the Federal Antimonopoly Service of the North-West District dated 08/25/2008 in case No. A42-7064/2007, FAS Volga-Vyatka District dated 02/19/2007 in case No. A17-1843/5-2006, FAS East Siberian District dated 03/10/2006 No. A33-20073/04- S6-F02-876/05-S1 in case No. A33-20073/04-S6).

Since there is no clear answer to the question, the contractor will have to make the appropriate decision on his own. Moreover, if the contractor will charge VAT on the compensation amount, then he can issue an invoice in one of two ways. In the first case, the invoice is issued in one copy and is not presented to the customer. In the second case, the contractor issues an invoice in two copies, one of which is presented to the customer. Based on this invoice, the customer will be able to deduct VAT. Note that the second option is somewhat risky, since, according to regulatory authorities, the contractor does not have the right to issue an invoice to the customer for the amount of reimbursable expenses. The reason is that there is no sale of goods (works, services).

At the same time, the courts believe that the presentation of an invoice is possible (see decisions of the FAS North Caucasus District dated January 13, 2010 No. A53-9707/2009, dated January 20, 2009 No. A53-10111/2008-C5-44, FAS Moscow District dated 04/27/2010 No. KA-A40/4081-10, Federal Antimonopoly Service of the Ural District dated 05/25/2009 No. F09-3324/09-S3).

If the contractor does not include the reimbursement amounts in the VAT tax base, then he will not be able to deduct the VAT charged to him for these expenses by suppliers for the following reason. As you know, one of the conditions that must be met to deduct VAT is that the purchased goods (work, services) must be used in taxable activities. If these expenses are compensated by the customer, but are not included by the contractor in the VAT tax base, then it turns out that these expenses do not participate in taxable activities. Accordingly, VAT should not be deducted on such expenses.

Income tax

In Chapter 25 of the Tax Code of the Russian Federation there are no rules governing the procedure for recognizing for profit tax purposes the amounts that taxpayers receive as reimbursement of expenses. At the same time, in our opinion, the contractor should reflect them in tax accounting taking into account the following.

If the contractor includes costs that will be reimbursed by the customer as expenses, then he must recognize the received reimbursement amounts in income. If these costs are not included in tax accounting expenses, then the amounts reimbursed by the customer should not be reflected in income.

Accounting in construction

A construction contract always affects two parties: the customer company and the contractor, that is, the contractor. In the article we will consider the features of accounting when performing construction work.

ConsultantPlus TRY FREE

Get access

The construction of buildings or structures has enormous differences from other types of activities, not only in the stages of implementation and implementation, but also in terms of accounting and tax accounting.

Differences in accounting in construction:

- Documentation. Participants use other documents to reflect the stages and results of construction. For example, certificates of completed work in the KS-2 special form, as well as a special certificate on the cost of construction in the KS-3 form.

- Cost accounting by elements. In other words, the costs incurred are divided into several elements, such as: materials, wages of specialists, operation of equipment, machinery and mechanisms, as well as overhead costs.

- Features of object acceptance. The completed construction project is subject to acceptance according to special rules and special commissions; based on the results of this control event, a transfer and acceptance certificate is drawn up (form No. OS-1a).

- The need to register the object. The constructed building is subject to mandatory registration with the relevant government agencies. Only after registration an object can be included in fixed assets.

Moreover, accounting in the customer’s company also differs from accounting in the contractor’s organization. Let's take a closer look at the accounting features for each party.

Accounting in construction for a contractor

Keeping records of construction activities of organizations is enshrined in PBU 9/99, PBU 10/99, PBU 2/94, PBU for investment accounting. All costs in a construction company are subject to division into the elements mentioned above.

To reflect construction costs in accounting, accounting account 20 “Main production” is used. The debit of account 20 reflects the following expenses:

- for materials with simultaneous reflection of costs on the credit of account 10 “Material inventories”;

- for the salary of construction company personnel under loan 70 “Payroll calculations”;

- for settlements with suppliers on account credit 60.

When receiving step-by-step acceptance, you should use account 46 “Completed stages of work in progress”, forming the posting Dt 46 Kt 90 - the work in progress is reflected.

Accounting in a construction organization: an example

Vesna LLC provides construction services. A contract was concluded for the construction of an office building. Acceptance is carried out in two stages: the first in the amount of 2 million rubles, the second - 2.4 million.

The terms of the contract provide for an advance payment of 90% of the cost of the stage. So, the advance for the first is 1.8 million rubles, for the second - 2.16 million rubles.

The start of work is February 2021, the end of the first part of construction is May, the second is July.

The cost price for the first is 1.72 million rubles, for the second - 1.98 million rubles.

Accounting entries:

| Period | Debit | Credit | Amount (rub.) | Operations |

| 20.02 | 51 | 62-1 | 1 800 000 | Advance payment for stage 1 of work is credited to the current account |

| 20.02 | 62-1 | 68-1 | 274 576 | VAT charged on advance payment |

| 25.03 | 46 | 90-1 | 2 000 000 | Completion of the first stage of construction, KS-2 signed |

| 25.03 | 90-3 | 68-1 | 305 085 | VAT charged |

| 25.03 | 68-1 | 62-1 | 274 576 | VAT on advance has been restored |

| 25.03 | 90-2 | 20 | 1 720 000 | The cost of the first stage of work has been written off |

| 25.03 | 90-9 | 99 | 100 610 | Profit accrued from acceptance of the first stage of work |

| 15.07 | 51 | 62-1 | 2 160 000 | The second advance was credited to the bank account |

| 15.07 | 62-1 | 68-1 | 486 000 | VAT charged on the second prepayment |

| 20.07 | 62 | 46 | 2 000 000 | The cost of construction work of the first stage was written off |

| 20.07 | 62 | 90-1 | 2 400 000 | Revenue reflected |

| 20.07 | 90-3 | 68 | 366 102 | VAT charged |

| 20.07 | 68 | 62-1 | 486 000 | VAT on prepayment has been restored |

| 20.07 | 90-2 | 20 | 1 980 000 | The cost of the second stage is written off |

| 20.07 | 90-9 | 99 | 420 000 | Profit from the second stage of work performed is reflected |

| 20.07 | 62-1 | 62 | 3 960 000 | The amount of the received advance payment is credited |

Construction accounting for the customer

A distinctive feature of accounting for the customer is that the construction of an object for the customer is an investment in non-current assets.

Accounting should be kept on account 08 “Investments in non-current assets” using a special sub-account 3 “Construction of fixed assets”. Thus, when signing a certificate of completion (KS-2), which reflects the costs incurred to pay for contract construction work, the customer makes an entry:

On the debit of account 08-3 on credit 60 “Settlements with the contractor” for the amount of the KS-2 act.

If the contractor has submitted value added tax, then the following entry is made:

Debit 19 “VAT” Credit 60 in the amount of the tax liability issued.

Upon completion of construction, the costs reflected in the debit of account 08-3 are subject to transfer to the debit of account 01 “Fixed assets”.

The constructed building (structure) is subject to mandatory registration with government agencies. Before receiving a certificate of state registration of ownership, the object should be recorded in a special subaccount of account 01.

Depreciation on a constructed building or structure begins on the first day of the month following the month it was taken into account.

Source: https://ppt.ru/art/buh-uchet/v-stroitelstve

Elimination of deficiencies in completed work

Sometimes, after completion of the work, the customer identifies shortcomings in the work performed and turns to the contractor with a demand to eliminate them. As a rule, the contractor eliminates these deficiencies free of charge. As a result of performing such work, he is faced with two questions: is it necessary to calculate VAT on the cost of gratuitous work and can the costs associated with the performance of this work be taken into account when taxing profits?

Tax consequences

VAT

In this case, the object of VAT taxation does not arise. The fact is that by eliminating deficiencies free of charge, the contractor, in fact, fulfills the obligations assumed under the contract. In turn, the cost of work under this agreement is already included in the VAT tax base. Therefore, there is no need to charge and pay VAT on the cost of “corrective” work.

Income tax

As for the recognition for profit tax purposes of the costs incurred by the contractor when carrying out work to eliminate deficiencies, they can be included in expenses in tax accounting on the basis of subparagraph 47 of paragraph 1 of Article 264 of the Tax Code of the Russian Federation as losses from defects.

Features of accounting and taxation for a contractor

02.

10. 2021 | Buhscheta.ru A contract is an agreement under which one party (contractor) undertakes to perform certain work on the instructions of the other party (customer) and deliver the result to the customer, and the customer undertakes to accept the result of the work. The Civil Code of the Russian Federation defines a list of works performed under a contract, which includes: a) manufacturing of a thing; b) processing (processing) of a thing; c) performing other work and transferring its result to the customer.

Under a contract concluded for the manufacture of a thing, the contractor transfers the rights to it to the customer. Accounting Regulations PBU 2/2008 “Accounting for Construction Contracts” ((hereinafter referred to as PBU 2/2008), approved by Order of the Ministry of Finance of the Russian Federation dated October 24, 2008.

No. 116n regulates the specifics of the procedure for the formation in accounting and disclosure in financial statements of information on income, expenses and financial results by organizations (with the exception of credit organizations and state (municipal) institutions) that are legal entities under the legislation of the Russian Federation and acting as contractors or as subcontractors in construction contracts, the duration of which is more than one reporting year or the start and end dates of which fall on different reporting years.

Contract agreements subject to PBU 2/2008 include the following agreements:

- engineering and technical design in construction;

- provision of services in the field of architecture;

- construction contract;

- other services inextricably linked with the facility under construction;

- for the liquidation (dismantling) of buildings, structures, ships, including associated environmental restoration.

- to carry out work on the restoration of buildings, structures, ships;

The contractor can choose one of the accounting methods.

The first method, when costs are added up by object