Which accounts to use for settlements under the GPC agreement

Sometimes certain types of work (services) are performed for a company by an individual under civil law contracts (GPC).

In this case, the accountant needs to carry out the necessary operations in accounting: to reflect and pay remuneration, calculate insurance premiums, withhold personal income tax, etc. Which accounts should be used for this?

To reflect settlements under the GPC agreement, account 76 “Settlements with various debtors and creditors” is used. This account must be used regardless of whether the work under the GPC contract is performed by an employee of the same company or by a third party who is not in an employment relationship with the employer (customer). In this case, it is incorrect to use account 70 “Settlements with personnel for remuneration” to reflect calculations, since it is not intended to account for this type of transaction.

Which entries should be used in accounting under a GPC agreement? Corresponding accounts are determined depending on the purpose for which the work was performed (service provided): for the needs of the main or auxiliary production, for solving general business problems, etc.

Postings for accrual of remuneration:

The following materials will introduce you to the postings for various business transactions:

- “Transactions on the accrual and payment of UTII”;

- “Wage entries in budget accounting”;

- "Accounting entries for deposits and interest."

How to correctly conclude a GPC agreement with an individual is also described on our website. And ConsultantPlus experts have prepared instructions with which you can check it for tax risks:

To see the recommendations, get a free trial access to K+ and go to the Ready Solution.

Features of tax accounting for the provision of certain types of services, works (contracts)

Sales income for tax purposes is the proceeds from the sale of work (services) (Clause 1, Article 249 of the Tax Code of the Russian Federation). The general contractor accounts for revenue in the general manner provided for tax accounting of income from sales:

- under a construction contract with the developer, based on the total amount of the results of construction and installation work delivered to the developer, including work performed by subcontractors;

- under a subcontract agreement (if it contains a provision for the provision of general contracting services), based on the cost of services provided to the subcontractor.

Situation: what expenses (direct or indirect) include the general contractor’s expenses for paying the subcontractor’s work?

The organization independently determines in its accounting policy for tax purposes a list of direct expenses associated with the production of goods (performance of work, provision of services). To do this, the organization must apply economically sound indicators that are determined by the technological process.

The costs of work performed by subcontractors are directly related to the performance of work on the construction of specific facilities. Consequently, such costs should be classified as direct costs as part of material costs (subclause 6, clause 1, article 254 of the Tax Code of the Russian Federation).

This conclusion follows from paragraph 1 of Article 318 of the Tax Code of the Russian Federation and is confirmed by letter of the Federal Tax Service of Russia dated February 24, 2011 No. KE-4-3/2952.

Direct costs are distributed among the balances of work in progress (Article 319 of the Tax Code of the Russian Federation). When performing construction work under a contract, work in progress includes unfinished work (stages of work), as well as work (stages of work) completed but not accepted by the developer (letter of the Ministry of Finance of Russia dated November 29, 2006 No. 03-03-04/1/ 807).

Thus, the general contractor’s expenses for paying the subcontractor’s work should be classified as direct expenses.

INCOME TAX

The supply of services for tax purposes is any operation that is not the supply of goods, or another operation for the transfer of rights to objects of intellectual property rights and other intangible assets or the provision of other property rights under such objects of intellectual property rights, as well as the provision of services consumed in the process performing a certain action or carrying out a certain activity (clause 14.1.185 of the Tax Code).

In tax accounting, income from the provision of services is recognized as operating income on the basis of clause 135.4.1 of the Tax Code. An enterprise providing services determines income using the accrual method, i.e., revenue from the sale of work and services is reflected in tax accounting at the time of drawing up an act or other document drawn up in accordance with current legislation, which confirms the completion of work or provision of services.

We invite you to familiarize yourself with the Agency Agreement and the Mandate Agreement, which are one and the same.

Expenses incurred by the enterprise for the purpose of providing services (performing work) are reflected as the cost of work and services on the basis of paragraphs. 138.1.1 NKU. According to the rules of clause 138.4 of the Tax Code, expenses that form the cost of goods sold, work performed, services rendered are recognized as expenses of the reporting period in which income from the sale of such goods, work performed, services rendered is recognized (except for non-distributive fixed overhead costs, which are included in cost of goods sold in the period in which they arise).

VALUE ADDED TAX

Operations for the provision of services and performance of work are subject to VAT in accordance with paragraphs. “b” and “e” clause 185.1 of the NKU.

In accordance with clause 188.1 of the Tax Code, the VAT tax base for transactions for the supply of services is determined based on their agreed (contract) value (in the case of controlled transactions - not lower than the usual prices determined in accordance with Article 39 of the Tax Code). In this case, national taxes and fees (except for value added tax) are taken into account.

https://www.youtube.com/watch?v=ytaboutru

a) expenses incurred (accrued) in the reporting period in connection with the purchase from a non-resident of services (work) for consulting, marketing, advertising (except for expenses incurred (accrued) in favor of permanent representative offices of non-residents, which are subject to taxation in accordance with clause 160.8 of the Tax Code) in an amount exceeding 4% of income (revenue) from the sale of products (goods, works, services) (less VAT and excise tax) for the year preceding the reporting year, and for banks - in an amount exceeding 4% of income from operating activities (for excluding VAT) for the year preceding the reporting year;

b) the expenses do not include in full the expenses incurred (accrued) in the reporting period in connection with the purchase from a non-resident of services (work) for consulting, marketing, advertising, if the person in whose favor the corresponding payments are made is a non-resident having offshore status, taking into account the provisions of clause 161.3 of the Tax Code.

Example 4

When concluding an agreement for the supply of goods to a supermarket chain, the question of concluding an additional merchandising agreement almost always arises (according to the terms of the agreement, these are pre-sale preparation services, but in reality we are talking about displaying the goods for review by customers in a prime location in the retail space). Tax authorities scrutinize such agreements too carefully, which results in non-recognition of expenses on them and additional assessment of tax liabilities with penalties. Does the company supplying the goods have the right to expenses under merchandising agreements?

In general, the main problem with such contracts during inspections is the connection with the economic activities of the enterprise that supplies the goods. After all, Ukrainian legislation does not directly define what merchandising is. Translated from English, “merchandising” is the promotion of a product on the market. Merchandising can be considered a separate direction or tool (element) of marketing.

In fact, merchandising is a set of sales technologies that make it possible to present a product to a potential buyer in the most favorable material and psychological conditions. That is, the main task and essence is how to arrange the product in the store so that it is sold more efficiently and without the direct participation of the seller.

At the same time, merchandising services are inherently part of marketing (marketing services) - this position is confirmed by the Generalized Tax Consultation on the classification of expenses for paying for marketing and advertising services as expenses (Order of the State Tax Service of February 15, 2012 No. 123, see “ DK" No. 12/2012).

Conclusion: if the supply agreement or commission agreement between the manufacturer (importer) or the owner of the trademark and the seller (distributor or retailer) provides for payment for advertising, marketing services, including incentive payments, as part of the manufacturer’s (importer’s) expenses or trademark owner, which are taken into account when calculating the object of taxation, include expenses incurred by the manufacturer (importer) or the owner of the trademark to pay for such services and payments in favor of distributors or retailers, subject to the restrictions established by paragraphs. 139.1.13 NKU.

In coming to this conclusion, the tax authorities want to see the connection between the contract for the supply of goods and the contract for the provision of merchandising (marketing) services for such goods. However, judicial practice is not so categorical: the taxpayer carries out financial and economic activities at his own risk, and therefore has the right to independently assess its effectiveness and expediency.

At the same time, the providers of such services can only be business entities that carry out activities that comply with the norms of KVED DK 009:2010 - 73.20 “Research of market conditions and identification of public opinion” (Explanation of the Ministry of Revenue dated July 1, 2013 “Practice of application of the norms of the Tax Code of Ukraine: last changes").

To account for expenses on advertising and marketing services, including incentive payments when calculating the object of taxation, it is necessary to prove the direct connection of such expenses with the economic activities of the taxpayer and confirmation with primary documents, the mandatory maintenance and storage of which is provided for by the accounting rules, and other documents (see clause 139.1.

9 Tax Code and letter of the Ministry of Revenue dated December 5, 2013 No. 6344/І/99-99-19-03-02-14, “DK” No. 11/2014). In this case, we are talking about the availability of primary documents from the supplier company, such as an agreement for the provision of services (marketing, merchandising, promotion of goods in retail chains, etc.), acts of acceptance and transfer of services, tax invoices, documents on payment for these services, meeting the requirements of Article 9 of the Law of Ukraine “On Accounting and Financial Reporting in Ukraine” and containing information necessary for tax purposes on the content of these services and their cost.

Posting in accounting for payment of accrued remuneration

Each of the entries indicated in the previous section forms in the accounting the customer’s obligation to the contractor to pay remuneration for work performed under the GPC agreement (services provided). It arises after the customer accepts the work (service) from the contractor and signs the acceptance certificate. The act will serve as the basis for accounting entries. Then the customer needs to pay the contractor and also reflect this operation in accounting.

To reflect settlements under GPC agreements, the following posting is used:

The basis for such an entry in accounting (in addition to the agreement and act) will be a bank statement if the money is transferred in non-cash form, or a cash order when paying the contractor money from the cash register.

This material will introduce you to the postings for accounting cash transactions.

You can find out how a customer can calculate income tax, pay personal income tax and insurance premiums when paying for services to an individual in ConsultantPlus by getting trial access to the system for free.

An example of registration, accrual, payment and reflection in accounting of the amounts of GPC agreements

Let's consider an example of registering amounts under a GPC agreement in 1C 8.3 ZUP.

From October 1, 2021, a GPC agreement was concluded for two months with an employee who is already working in the organization under an employment contract for a total amount of 30,000 rubles.

According to the terms of the agreement, accruals will be made on the basis of acts of completed work. The following acts were signed: October 31, 2019 in the amount of 10,000 rubles. and November 25, 2021 – in the amount of RUB 20,000.

All payments are made within the organization’s salary payment deadlines – the 5th of each month. At the same time, income under both the employment contract and the GPC agreement is paid in one Statement...

The employee's salary is set at 33,000 rubles.

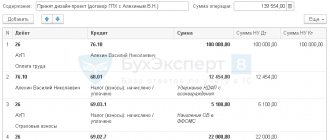

All amounts under the concluded GPC agreement when creating credit entries must be credited to account 76.10. In October, expenses under the GPC agreement (when generating transactions, this is a debit account) must be attributed to the same Method of reflecting wages in accounting as specified for an employee under an employment contract - General production expenses (Dt 25). In November - costs should be reflected as General production expenses (Dt 25).

Because It is planned to pay amounts for an employee under an employment contract and a civil process agreement in one Statement... , then according to the contract there is no need to create a separate element in the Employees .

To register the terms of the concluded GPC agreement, we will enter the document Agreement (work, services) , indicating in it the period of validity of the agreement from October 1 to November 30, 2021 and selecting the Payment method - according to certificates of work performed for a total amount of 30,000 rubles:

Since the amounts under the GPC agreement should be accounted for in the credit account on account 76.10, then in the Account as , select the value Settlements with counterparties :

Based on the document Agreement (work, services), we will create a document Acceptance Certificate for Work Completed , indicating in it as the Date of the document the date of its signing (10/31/2019) and the Month of accrual - October 2021.

The October amount under the act will be 10,000 rubles, and the payment date will coincide with the date of salary payment in the organization - November 5, 2019:

Since in October the amount under the GPC agreement should be attributed to the same cost account as for the amounts under the employee’s employment contract, the Account, subaccount empty:

When filling out the document Calculation of salaries and contributions for October 2021, the amount according to the Work Acceptance Certificate - 10,000 rubles - Contracts

In this case, under the employment contract, on the Accruals , the salary payment in the amount of 33,000 rubles will be calculated

The total personal income tax for October for an employee will be 5,590 rubles: 4,290 rubles. - according to salary and 1,300 rubles. – under the GPC agreement:

In the Statement to the Cashier for October 2021, in the Pay , we indicate the method of payment of wages - Monthly salary :

When automatically filling out a document for an employee, the following amounts will be due for payment under the employment contract and the GPC agreement:

- 33,000 (Payment based on salary) + 10,000 (amount under the GPC agreement) – 5,590 (personal income tax) = 37,410 rubles.

When generating the document Reflection of salary in accounting for October 2021, the Method of reflection by Type of transaction - Contract (work, services) will be loaded Method of reflection of salary in accounting is the same as for an employee under an employment contract - General business expenses (Dt 26). KA value will be loaded in the Expense Item :

After synchronization with 1C:Accounting 3, the following transactions will appear in it:

In November 2021, based on the Agreement (work, services) , we will create the document Certificates of Work Completed dated November 25, 2019:

The amount under the act will be 20,000 rubles. with payment date – 12/05/2019:

Since in November expenses the amount under the GPC agreement should relate to the Method of reflecting wages in accounting - General production expenses (Dt 25), then in the Account, subconto we will indicate this method:

Accrual under the GPC agreement in 1C 8.3 ZUP will be made in the document Accrual of salaries and contributions in November 2019 on the Agreements :

salary payment amount will be 33,000 rubles. and the total personal income tax will be calculated as 6,890 rubles.

In the Sheet... for November 2021. to be paid will be equal to:

- 33,000 (Payment based on salary) + 20,000 (amount under the GPC agreement) – 6,890 (personal income tax) = 46,110 rubles.

In the Reflection of salaries in accounting for November 2019 by Type of operation - Contract (work, services) the following will be loaded:

- Method of reflection - General production expenses (Dt 25)

- Cost item – spacecraft

After synchronization with 1C:Accounting 3, the following transactions will appear in it:

If you are a subscriber to the BukhExpert8: Rubricator 1C ZUP system, then watch

In what account should personal income tax be reflected on payments to the contractor?

When paying remuneration, the source of payments is obliged to withhold personal income tax from the amount accrued to the individual (subclause 6, clause 1, article 208 of the Tax Code of the Russian Federation). The customer does not have to perform the duties of a tax agent for personal income tax only if the GPC agreement is concluded with an individual entrepreneur, a private notary or a lawyer. These categories of performers pay the tax themselves (clause 2 of Article 227 of the Tax Code of the Russian Federation).

Operations for calculating tax and transferring it to the budget are carried out according to the following scheme:

The responsibilities of the tax agent when making payments under the GPC agreement are not limited to withholding tax, transferring it and reflecting payments in Form 6-NDFL. At the end of the year, you need to issue a 2-NDFL certificate or inform the tax authorities and the recipient of the income about the impossibility of withholding tax if the remuneration is issued in kind (clause 5 of Article 226 of the Tax Code of the Russian Federation).

How to show insurance premiums under an agreement with an individual in accounting

Insurance premiums are charged on the remuneration amounts under the GPC agreement: for compulsory pension and medical insurance. Contributions to the Social Insurance Fund for compulsory social insurance in case of temporary disability and in connection with maternity do not need to be accrued (subclause 2, clause 3, article 422 of the Tax Code of the Russian Federation).

Contributions for accident insurance are accrued only if this is provided for in the GPC agreement (paragraph 4, paragraph 1, article 5, paragraph 1, article 20.1 of the law “On compulsory social insurance ...” dated July 24, 1998 No. 125- Federal Law).

The accrual and payment of insurance premiums are reflected by entries in the accounting accounts in the following order:

On account 69, you need to organize analytical accounting for the types of insurance premiums paid (sub-account “Settlements with the Pension Fund”, sub-account “Settlements with the Federal Compulsory Medical Insurance Fund”, etc.).

How to reflect payments under GPC agreements in the DAM is described in this publication.

Cost accounting using your own materials

It happens that to carry out construction work, the customer provides materials on a toll basis. However, by default, the contract is drawn up as dependent on the contractor. That is, construction is carried out from the materials of the contractor, with his forces and means. This is provided for in paragraph 1 of Article 704 of the Civil Code of the Russian Federation.

Such material costs are taken into account as direct costs. Often the amount of such costs is clear in advance based on the estimate. Therefore, they are included in the expected direct costs.

The purchase of materials is reflected in the general order.

Next, the property is transferred to production. Why draw up one of the documents:

- limit-fence card, for example, in form No. M-8. This document is used when there are approved standards and plans for the consumption of materials;

- requirement-invoice (form M-11) or warehouse registration card (form M-17). They are used when there are no standards and plans and there is no need to transfer materials to a remote unit;

- an invoice for the release of materials to the third party (form M-15) is drawn up when materials are transferred to a geographically remote unit.

This is established by paragraphs 100, 109 and 126 of the Methodological Instructions, approved by Order of the Ministry of Finance of Russia dated December 28, 2001 No. 119n.

Debit 20 Credit 10 (16) – materials written off for production (construction).

This procedure is provided for in the Instructions for the chart of accounts (accounts 10, 16, 20).

If expenses are expected, they can be written off against a special reserve.

We invite you to read Time off for work on a holiday according to the Labor Code of the Russian Federation: payment or day off, how to arrange it? || How to provide days off for work on holidays with single pay

In this case, the cost of materials is written off as the cost of work in accordance with the cost estimation methodology approved in the accounting policy.

If this is expressly provided for in the contract, then for construction work the customer can provide the contractor with materials on a toll basis.

Debit 003 – materials received for construction work.

Organize internal movements of the customer's materials on subaccounts of off-balance sheet account 003. When transferring materials to production, their cost does not affect the cost of your work.

Debit 20 Credit 02, 10, 23, 25, 26, 60, 68, 69, 70, 76… – the expenses of the performing organization for processing materials are taken into account.

Credit 003 – materials transferred to production are written off.

https://www.youtube.com/watch?v=ytpolicyandsafetyru

Credit 003 – unused materials were transferred to the customer.

This order follows from the Instructions for the chart of accounts (accounts 02, 10, 20, 23, 26, 60, 68, 69, 70, 76... 003).

The basis for such an entry will be a report on the consumption of materials and an invoice in form No. M-15.

Indirect costs include the part of the organization's general business expenses that falls on a specific contract. Set the procedure for distributing indirect costs between contracts yourself in your accounting policy for accounting purposes. For example, you can distribute indirect costs in proportion to the revenue for each of the contracts or in proportion to direct costs.

Debit 20 Credit 26 (25, 23) – indirect expenses are taken into account.

This procedure is provided for in paragraph 13 of PBU 2/2008.

Results

Postings under a GPC agreement with an individual affect different accounting accounts.

The accrual of remuneration is reflected in account 76 “Settlements with various debtors and creditors”. The customer makes the payment by debiting account 76 in correspondence with the cash accounts. Insurance premiums are charged on the amount of remuneration and reflected in account 69 “Calculations for social insurance and security”. The deduction and transfer of personal income tax from the remuneration received is carried out using account 68 “Calculations for taxes and fees”. You can find more complete information on the topic in ConsultantPlus. Free trial access to the system for 2 days.