Payment of dividends at the end of the year: general principles

The decision on the distribution of net profit is made by persons who participate in the authorized capital of the organization.

Their composition depends on the organizational and legal form of the legal entity and the number of participants. The dividend payment schedule in 2021 can be set at the discretion of the owners. Part of the profit can be paid:

- quarterly,

- semiannually,

- once a year.

Distribution of profits between participants is not allowed if:

- the company has signs of insolvency (bankruptcy),

- the value of net assets is less than the value of the authorized capital, or will become so as a result of the distribution and transfer of profits.

When transferring part of the profit to a participant, a payment order is issued in accordance with the general procedure. The recipient of the funds transfer and his bank details are indicated. It is necessary to correctly specify the purpose of the payment when paying dividends to the founder so that the transfer can be clearly qualified by the bank and regulatory authorities. For example, like this:

“Transfer of part of the net profit to the participant in accordance with the Minutes of the meeting of shareholders No. 1 dated May 11, 2018.”

Please note that to confirm the legality of the money transfer, the bank has the right to request a copy of the specified Protocol.

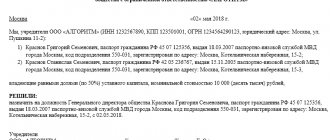

Registration of the participants’ decision on profit distribution

Sample minutes of the general meeting of company participants, if the number of participants is more than one

general meeting of participants

Limited Liability Company “OUR FIRM”

Moscow April 28, 2012

members of the Society:

Ivanov I.I. (date of birth, passport details, registration address; share in the authorized capital - 60%),

Petrov P.P. (date of birth, passport details, registration address; share in the authorized capital - 40%),

General Director Sidorov S.S.

The meeting has a quorum of 100%.

Agenda:

1. Recognition of the validity of expenses incurred in 2011 at the expense of net profit (not subject to accounting for profit tax purposes).

2. Recognition of the validity of the formation of funds in 2011.

3. Approval of financial statements for 2011.

4. Distribution of profits received in 2011.

5. Approval of the timing and procedure for payment of participation income (dividends).

Performances:

General Director Sidorov S.S. on the results of work for 2011, the amount and structure of expenses incurred from net profit (not subject to accounting for profit tax purposes), the formation of funds in 2011.

Solutions:

1. Recognize as justified the expenses incurred in 2011, which are not subject to accounting for profit tax purposes, in the amount of .

2. Recognize the formation of the Reserve Fund in 2011 as justified in the amount in accordance with the Charter.

3. Approve the annual report for the 2011 financial year in the following composition:

— annual balance sheet;

- Profits and Losses Report;

— appendices to them, provided for by regulations;

— calculation of net asset value.

4. Based on the results of economic activity in 2011, the profit remaining after taxation should be used to pay dividends in the amount of .

5. The declared dividends in total shall be distributed among the founders in proportion to their shares in the authorized capital:

6. Dividends should be paid in cash through the cash desk no later than June 26, 2012.

The decisions were made unanimously.

1. Certificate of the amount and structure of expenses incurred that are not subject to accounting for profit tax purposes.

This is interesting: Sample power of attorney for an accountant for tax purposes

2. Certificate from an accountant about the availability and amount of net profit that can be used to pay dividends

3. Certificate of no restrictions on the distribution of profits between the founders (Clause 1, Article 29 of the Federal Law of 02/08/1998 N 14-FZ “On Limited Liability Companies”)

Chairman of the meeting, founder Ivanov I.I. signature

Secretary of the meeting, founder Petrov P.P. signature

If the LLC has a single founder, then instead of the minutes of the general meeting, a Resolution is drawn up.

Moscow April 28, 2012

The sole founder of the Limited Liability Company "OUR FIRM" is a citizen of the Russian Federation Ivanov Ivan Ivanovich, having a passport ..., issued by ..., date of issue: ..., subdivision code: ..., living at the address: ...,

1. Recognize as justified the expenses incurred in 2011, which are not subject to accounting for profit tax purposes, in the amount of .

2. Recognize the formation of the Reserve Fund in 2011 as justified in the amount in accordance with the Charter of the Company.

3. Approve the annual report for the 2011 financial year in the following composition:

— annual balance sheet;

- Profits and Losses Report;

— appendices to them, provided for by regulations;

— calculation of net asset value.

4. Based on the results of economic activities in 2011, the profit remaining after taxation should be used to pay dividends to the Sole Founder of the Company in the amount

5. Dividends should be paid in cash through the cash register no later than June 26, 2012.

1. Certificate of the amount and structure of expenses incurred that are not subject to accounting for profit tax purposes.

2. Certificate from an accountant about the availability and amount of net profit that can be used to pay dividends

3. Certificate of no restrictions on the distribution of profits between the founders (Clause 1, Article 29 of the Federal Law of 02/08/1998 N 14-FZ “On Limited Liability Companies”)

founder of OUR FIRM LLC ______________ / I.I. Ivanov /

The period within which the payment of dividends must be made may be specified in the Articles of Association or in the Minutes/Decision, however, it cannot exceed 60 days from the date of the decision. If the period is not specified, it is also considered equal to 60 days (clause 3 of Article 28 of Law No. 14-FZ).

Payments of dividends on shares in 2021

The decision to pay dividends to a joint stock company is made by the general meeting of shareholders. To do this, it is necessary to initiate a meeting. This can be done by the board of directors or another person determined by the charter.

The board of directors submits a proposal on the amount and procedure for distribution of profits for consideration by the general meeting of shareholders. Based on the results of the consideration and voting of shareholders, a Protocol on the results of the meeting is drawn up, which reflects the decision to transfer income to shareholders. This document is the basis for the transfer.

Part of the profit can only be paid to the shareholder by bank transfer. There is no need to issue a separate transfer order. The previously listed documents are sufficient. But if it is provided for by the organization’s document flow, then its preparation is not prohibited.

Order for payment of dividends, sample

How to draw up a dividend payment protocol - sample?

The payment of income to the founders can be either the main topic of the general meeting or part of the general agenda. In any case, based on the results of the event, a protocol is drawn up, which must contain the required details:

This is interesting: Sample car purchase and sale agreement

list of founders and the ratio of their shares in the capital;

a list of issues discussed and the content of decisions on them.

To decide on dividend payment,

It is necessary that the meeting participants come to agreement on the following points:

the period for which profit is subject to distribution;

whether the profit will be used in whole or in part;

when and in what form the participants’ income will be paid.

The object of distribution can be amounts received for a quarter or a year, both for the current and the previous one. In this case, the share of payments to each participant in the company is determined in accordance with his share in the capital or on other grounds specified in the charter. The protocol may contain already recalculated amounts to be paid. Although it is most likely to transfer income in cash, other forms of receiving it are also possible.

The deadline for transferring dividends is established by the charter or a decision of the meeting of founders, but according to clause 2 of Art. 28 of Law No. 14-FZ, it should not exceed 60 calendar days.

Sample decision on payment of dividends

presented at the link below.

Payment of dividends in LLC

In a limited liability company, to make a decision on the distribution of profits, it is necessary to hold a general meeting of participants. Part of the profit is distributed on the basis of the Minutes of such a meeting in proportion to the owners’ shares in the authorized capital (unless the Charter of the organization provides for a different procedure).

The deadline for paying dividends to an LLC after a decision is made cannot exceed 60 calendar days. But at the same time, the Protocol or Charter may provide for other deadlines not exceeding this date.

conclusions

Dividends are the profit that the owners of the enterprise receive. What taxes and their amount depend on the status of the income recipient.

At the legislative level, the obligation to pay tax is assigned to the organization paying dividends. The tax is transferred within 1 day from the date of payment of dividends (not from the date of the decision).

If payment is not made, then a fine of 20% of the total amount is provided for unscrupulous taxpayers. The tax rate for a resident is 13%, for a non-resident citizen - 15%.

When taxing legal entities, the tax is paid on a general basis (13%), the taxation regime of the organization does not matter.

Tax exemptions are granted to companies whose share in the authorized capital exceeds or equals 0.5 million rubles.

The procedure for paying dividends to the sole founder of an LLC

When the owner of the company is a single person, there is no need to hold a meeting. To make a decision, the sole order of the owner is required.

Founder's decision to pay dividends, sample

In pursuance of the decision, the General Director may issue a Transfer Order, which will become an order to the Chief Accountant to make the transfer. But this is not mandatory and is not requested by regulatory authorities. In principle, the decision of the sole owner is sufficient for transfer.

Order on payment of dividends to the sole founder, sample

Accrual and payment of dividends, postings

The organization conducts settlements with the founders on account 75 of accounting.

Postings for payment of dividends to the founder

| Operation | Debit | Credit |

| The amount to be transferred to the participant has been accrued | 84 | 75 |

| Withholding tax on income (personal income tax or profit) | 75 | 68 |

| Transfer made to the founder | 75 | 51, 50 |

| Withheld taxes transferred to the budget | 68 | 51 |

If your organization is the founder of another company and received income from participation, then you need to reflect this operation as follows:

| Operation | Debit | Credit |

| Income received from participation | 51 | 76 |

| Funds received from participation in the authorized capital are reflected in income | 76 | 91 |

Dividend tax 2021

Taxes on dividends to the founder in 2021 are calculated depending on who is paid to: an individual or an organization.

Payment of dividends to the founder - organization is subject to income tax. Moreover, the payer acts as a tax agent, that is, he must withhold and transfer the tax to the budget. As a general rule, the rate is 13% (clause 2, clause 3, Article 284 of the Tax Code of the Russian Federation). But if the owner owns at least half of the authorized capital for at least one year, then the rate is set at 0% (clause 1, clause 3, article 284 of the Tax Code of the Russian Federation).

Income paid to the founder - an individual - is subject to personal income tax at a rate of 13% if he is a resident of the Russian Federation. If the owner is a non-resident, then the transfer of part of the net financial result to him will be taxed at a rate of 15% (paragraph 2, paragraph 3, article 224 of the Tax Code of the Russian Federation).

The tax calculation does not depend on the dividend payment calendar for 2021. For each transfer, the tax is calculated separately, and not on an accrual basis from the beginning of the year. To calculate, use the formula:

If your company itself receives income from participation in affiliated companies, then they must be taken into account when calculating the tax on amounts paid to the founders:

When dividends cannot be distributed

Profit cannot be distributed in the following cases:

- the authorized capital of the LLC has not been fully paid;

- the company has signs of bankruptcy or will meet such signs after paying dividends;

- the value of net assets is less than the authorized capital and reserve fund, or will become less as a result of the distribution of profits;

- the actual value of the participant’s share (part of the share) has not been paid;

- The company has an uncovered loss according to its financial statements.

Net assets and reserve fund

Net assets are the difference between assets and liabilities, which is determined according to accounting data. Assets include all of the company's property (fixed assets, inventories, cash, accounts receivable, etc.). Liabilities include the LLC's debts (accounts payable).

The reserve fund is a kind of “insurance” for the company in case of compensation for losses from business activities. It is created at the request of the LLC participants, in the amount provided for by the company’s charter, but not less than 5% of the value of the authorized capital.

If, at the end of the financial year, the value of net assets has become less than the authorized capital and reserve fund (if any), within six months after the end of the year it is necessary to take measures to increase net assets (at least to the size of the authorized capital) or reduce the authorized capital or even liquidate OOO.

How to reflect dividend payments on the balance sheet

The decision to transfer part of the profit to participants affects line 1370 “Retained earnings” of the balance sheet. When deciding on the distribution of the net financial result, the amount reflected in it is reduced.

In addition, the amount of income paid to the founders must be reflected in the Statement of Changes in Capital in the appropriate line.

The company that receives income from participation in the authorized capital reflects the amount received in the Statement of Financial Results. For this purpose, in this form of financial statements there is a separate line 2310 “Income from participation in other organizations.”

Receiving dividends when the founder leaves the LLC

Distribution of the company's net profit is carried out until the participants leave the founders.

Important

In order to prevent the emergence of controversial situations in such a case, it is necessary to provide for the procedure for accruing cash to participants who have expressed a desire to leave the company in the charter.

If one of the participants is going to leave the company, then the standard procedure for making a decision on bonifications is applied, but it should be remembered that the distribution of dividends cannot occur more often than once every three months.

Thus, if a participant plans to leave the company, it is advisable to exit immediately after the meeting at which the issue of distribution of assets was considered. In order to simplify bureaucratic issues, you can include the question of his withdrawal in the minutes of the same meeting.

What is more profitable for business: is it better to open an individual entrepreneur or an LLC?

We draw up a standard charter for an LLC: find out more

How to make changes to the charter of an LLC: https://bsnss.net/predprinimatelstvo/docs/izmeneniya-v-ustav.html