general characteristics

The production of products involves means (structures, buildings, equipment, etc.), as well as objects of labor (fuel, raw materials, etc.). Together they form production assets. A certain group partially or completely retains its natural material form over many cycles. Their cost is transferred to finished products as they wear out in the form of depreciation charges. The specified group is formed by production. They are directly involved in the process of releasing goods. Non-productive funds ensure the formation of social infrastructure.

The concept of fixed assets

Definition 1

Fixed assets are assets used in the economy a large number of times in production in an unchanged natural (material) form. These funds gradually transfer their own value to the product or service being created.

In practice, in accounting and statistics, fixed assets include objects with a service life of more than a year. The cost of fixed assets is an established and periodically revised value depending on changes in prices for products (products) of capital-forming industries.

The classification of fixed assets divides them into 2 types:

- Fixed production assets (FPF), including means of labor that are fully involved in the repeating production process by transferring their value in parts to finished products as they wear out.

- Fixed non-productive assets, which are material goods of long-term use. They do not take part in the production process, but are considered objects of public or personal consumption (residential building, school, hospital, club, cinema, public transport, etc.) This group of fixed assets is financed from the budget.

Finished works on a similar topic

- Course work Production assets in the balance sheet 480 rubles.

- Abstract Production assets in the balance sheet 230 rubles.

- Test work Production assets in the balance sheet 190 rubles.

Receive completed work or specialist advice on your educational project Find out the cost

There is also an active and passive part of fixed assets. The active part includes a set of funds that directly affect objects of labor. Through the action of the passive part of fixed assets, conditions for the normal functioning of the production process are created.

Note 1

The classification of fixed assets into active and passive parts is conditional.

Classification

The main production assets include:

- Buildings are architectural objects designed to create working conditions. These include garages, workshop buildings, warehouses, etc.

- Structures are engineering-construction type objects used to carry out the transportation process. This group includes tunnels, bridges, track construction, water supply systems, and so on.

- Transmission devices - gas and oil pipelines, power lines, etc.

- Equipment and machines 0 presses, machine tools, generators, engines, etc.

- Measuring devices.

- Computers and other equipment.

- Transport - locomotives, cars, cranes, loaders, etc.

- Tools and equipment.

Key quantities

The cost of OPF can be replacement, residual and initial. The latter reflects the costs of obtaining OS. This value is unchanged. The initial cost of funds that come from the capital investments of certain companies can be established by adding up all the costs. These include, among other things, transportation costs, the price of equipment and installation, etc. Replacement cost is the cost of purchasing the OS in current conditions. To determine it, funds are revalued using indexation or the direct recalculation method based on current market prices, confirmed by documents. equal to the recovery value, reduced by the amount of wear. There are also private indicators of OS usage. These include, in particular, the coefficients of intensive, integral, extensive operation of equipment and shifts.

Loss of original properties

The average annual cost of OPF is determined taking into account depreciation and amortization. This is due to the fact that with prolonged use of the products in the technological process, they quickly lose their original properties. The degree of wear can vary and depends on various factors. These include, in particular, the level of operation of the facilities, the qualifications of the personnel, the aggressiveness of the environment, etc. These factors influence various indicators. Thus, to determine capital productivity, an equation is first drawn up, which establishes the average annual cost of the general fund (formula). Capital-labor ratio and profitability depend on revenue and the number of employees.

Obsolescence

It means the depreciation of funds even before the physical loss of properties. can manifest itself in two forms. The first is due to the fact that the production process reduces the cost of products in the areas in which they are produced. This phenomenon does not lead to losses, since it is the result of an increase in savings. The second form of obsolescence arises due to the emergence of such OPFs, which are characterized by high productivity. Another indicator that is taken into account is depreciation (the process of transferring the cost of funds to manufactured products). It is necessary to form a special cash reserve for the complete renovation of facilities.

Average annual cost of OPF: formula for calculating the balance sheet

To determine the indicator, it is necessary to use the data that is present in They must cover transactions not only for the period as a whole, but also separately for each month. How is the average annual cost of open pension fund determined? The balance formula used is as follows:

X = R + (A × M) / 12 - / 12, where:

- R - initial cost;

- A is the value of the introduced funds;

- M is the number of months of operation of the introduced OPF;

- D is the liquidation value;

- L is the number of months of operation of retired funds.

Using the average annual cost of OPF in economic analysis

Let's consider the scope of application of the average annual cost of OPF in the calculation of other economic indicators.

If we take the volume of products produced by an enterprise and divide it by the average annual cost of general production assets, we will obtain a capital productivity ratio, which actually shows how many products produced in monetary terms are per 1 ruble of fixed assets.

If the capital productivity of an enterprise increases over time, this allows us to conclude that the company's capacity is being used efficiently. A decrease in capital productivity, on the contrary, indicates the opposite.

If we take the average annual cost of general production as a dividend, and use the volume of production as a divisor, we get a capital intensity ratio, which allows us to determine what cost of fixed assets is needed to produce a unit of output.

If we divide the average annual cost of OPF by the average number of employees, this will allow us to calculate the capital-labor ratio, which shows the extent to which each of the enterprise’s employees is provided with the necessary means of labor.

If the average annual cost of the general fund is multiplied by the depreciation rate coefficient, which characterizes the operating conditions of the funds, we obtain the amount of depreciation charges for the year. This indicator can be used not only as a retrospective indicator, but also as a forecast indicator when drawing up business plans.

The concept of fixed assets

Definition 1

Fixed assets are assets used in the economy a large number of times in production in an unchanged natural (material) form. These funds gradually transfer their own value to the product or service being created.

In practice, in accounting and statistics, fixed assets include objects with a service life of more than a year. The cost of fixed assets is an established and periodically revised value depending on changes in prices for products (products) of capital-forming industries.

The classification of fixed assets divides them into 2 types:

- Fixed production assets (FPF), including means of labor that are fully involved in the repeating production process by transferring their value in parts to finished products as they wear out.

- Fixed non-productive assets, which are material goods of long-term use. They do not take part in the production process, but are considered objects of public or personal consumption (residential building, school, hospital, club, cinema, public transport, etc.) This group of fixed assets is financed from the budget.

There is also an active and passive part of fixed assets. The active part includes a set of funds that directly affect objects of labor. Through the action of the passive part of fixed assets, conditions for the normal functioning of the production process are created.

Note 1

The classification of fixed assets into active and passive parts is conditional.

OS put into operation

As can be seen from the information above, the equation by which the average annual cost of open pension fund is determined (formula) includes indicators that require separate analysis. First of all, the initial price of the funds is established. To do this, take the amount of the account balance at the beginning of the reporting period. 01 balance sheet. It should then be analyzed whether any fixed assets were introduced during the period. If this was the case, you need to set a specific month. To do this, you should look at the revolutions by db sch. 01 and establish the value of the funds put into operation. After this, the number of months in which these OSs were in use is calculated and multiplied by the cost. Next, the average annual cost of OPF is determined. The formula allows you to determine the cost of the funds put into use. To do this, the figure obtained by multiplying the number of months of use by the initial price of the OS is divided by 12.

Disposal

During the analysis, in addition to the funds put into operation, written-off funds are determined. It is necessary to establish in which month they dropped out. To do this, the revolutions are analyzed according to Kd sch. 01. After this, the value of the disposed funds is determined. When writing off fixed assets during the entire reporting period, the number of months in which they were in use is established. Next, you need to determine the average annual cost of the disposed funds. To do this, their price is multiplied by the difference between the total number of months in the entire reporting period and the number of months of operation. The resulting value is divided by 12. The result is the average annual cost of general purpose assets that have left the enterprise.

Final operations

At the end of the analysis, the total average annual cost of the open pension fund is determined. To do this, you need to add up their initial cost at the beginning of the reporting period and the indicator for the funds put into operation. The average annual cost of fixed assets removed from the enterprise is subtracted from the resulting value. In general, the calculations are not complicated or labor-intensive. When calculating, the main task is to correctly analyze the statement. Accordingly, it must be compiled without errors.

The balance sheet of an enterprise accumulates all information about the availability of property (assets) and the sources of its receipt (liabilities) as of a certain date, i.e., it reflects the financial condition and demonstrates this information to users. The first section of the balance sheet is devoted to non-current assets, a significant proportion of which are fixed assets. Let us recall how fixed assets are reflected in the balance sheet by looking at a specific example.

Residual book value of fixed assets

The requirement of legislators when presenting operating results in the balance sheet is clear - all assets of the company must be reflected in a net valuation, i.e. their initial cost must be reduced by the amount of regulated amounts (for example, accrued depreciation) and reflect a real assessment of the accounting value of assets at the time of preparation of the report. The company's balance sheet reflects the residual value of assets, all without exception, including the organization's fixed assets. That is why we can say that the book value of fixed assets is its residual value.

It is not difficult to determine the residual value of a company's fixed assets. It appears in the first section of the balance sheet “Non-current assets” in line 1150 “OS”. It is made up of data from synthetic accounting registers - order journals for asset accounting. The residual value of fixed assets is the difference between the debit balance of account 01 “Fixed Assets” and accrued depreciation reflected in the credit balance of account 02 “Depreciation of fixed assets” at the end of the same reporting period.

Since all of the company’s fixed assets are classified as production assets, since they participate in the production process (in accordance with the OS Classifier), it makes sense to assert that the residual value of fixed production assets is the same indicator of the availability of assets on the balance sheet, i.e., the full balance sheet residual value of fixed assets. The “full” criterion determines the accounting residual value of the enterprise’s fixed assets after the revaluation, and, in fact, it also represents the value of the residual value of the general fund.

The indicator of the residual value of fixed assets on the balance sheet is involved in the analysis of the company's production activities in the same way as the indicator of the original value (or restored value, if revaluations were carried out).

It is important to understand that book value is a significant financial indicator, but it determines only the accounting price of an enterprise’s assets, i.e., the amount of costs aimed at acquiring or creating this property.

What applies to fixed assets

These assets include property that supports the production and management process of the company - buildings, structures, plots of land, perennial plantings, machine tools, equipment, power machines, vehicles, etc. The cost of recorded fixed assets is formed from the costs aimed at their acquisition (manufacturing), and is gradually repaid by monthly depreciation. This is carried out using one of the methods chosen by the company and enshrined in the accounting policy (clause 48 of PBU dated July 29, 1998 No. 34n):

- reducing balance;

by the sum of numbers of years of SPI (useful life);

in proportion to the volume of output (work, services).

Please note that not all fixed assets are depreciated. For example, land, environmental management facilities, road facilities, museum exhibits, housing stock, mobilization funds in conservation, as well as property owned by non-profit organizations are not subject to traditional depreciation charges.

In terms of liquidity, fixed assets are considered low-liquidity assets, since it is often impossible to immediately turn them into means of payment and quickly sell them if necessary.

What are fixed assets?

In order to increase the efficiency of an enterprise or business, you need to understand how to manage its assets, which include fixed assets. But before moving on to the analysis of ratios and management, it is necessary to understand what fixed assets are, what their structure is and what classifications of fixed assets exist.

To begin with, all the property of the enterprise is represented by fixed assets and inventories.

Fixed assets are means of labor that are repeatedly involved in the production process, while maintaining their natural form, transferring their value to the manufactured products in parts as they wear out in the form of depreciation. These include means of production with a service life of more than 12 months.

Thus, the following conclusions can be drawn.

Firstly, fixed assets last a long time.

Secondly, their cost is gradually included in the cost of products or services. And why? Yes because they are expensive. If you include all the cost at once, the profit will be uneven. And it is likely that if a company has a small turnover, a loss may occur. It is in order to avoid this problem that the depreciation mechanism was invented.

In addition, since fixed assets are usually expensive, additional investment resources are often used to acquire them. At the same time, financing for the acquisition of fixed assets can be carried out from various sources.

Fixed assets on the balance sheet and their valuation

Since fixed assets are a long-term asset (with a service life of more than a year) and tend to gradually wear out during operation, its value changes at each reporting date, that is, the assessment of the recorded fixed assets changes depending on revaluations or due to depreciation charges, unless, of course, it relates to depreciable property. Depreciation is a regulatory indicator that affects the value of fixed assets.

Fixed assets are reflected in the balance sheet at cost reduced by the amount of accrued depreciation (clause 35 of PBU 4/99), i.e. at residual value. In the company's balance sheet, the valuation of fixed assets is indicated at the residual value: the original value minus depreciation.

In accounting, the initial (or replacement after revaluation) cost of fixed assets is taken into account as the debit of account 01 “Fixed assets”, and the amount of accrued depreciation is recorded as a credit of account 02 “Depreciation of fixed assets”. Accordingly, the residual value is calculated as the difference between the amounts of initial cost and depreciation (D/t 01 minus K/t 02).

In the form of the balance sheet, a separate line 1150 “Fixed assets” is provided to reflect the amount of fixed assets valuation as of the reporting date.

Leased fixed assets are subject to separate accounting in account 03 “Income-generating investments in tangible assets”. Depreciation on them is calculated in the same way as on all fixed assets on the account. 02, recorded in the analytical accounting registers, and the residual value of such property occupies line 1160 “Profitable investments in materiel” in the balance sheet.

Example

The company has OS objects presented in the table. Depreciation is calculated using the straight-line method (original cost / number of months of service = depreciation amount per month). The land plot is not subject to depreciation; other objects are depreciated.

| Initial cost as of 01/01/2016 (in rubles) | Accrued depreciation | |||

| Plot of land | ||||

| Equipment | ||||

| Lathe | ||||

| Total | 6 960000 | 413 830 | 413 830 | 413 830 |

In the balance sheet in line “1150” the presence of OS will be reflected as follows:

- at the beginning of 2021 – RUB 6,960,000;

at the end of 2021 – RUB 6,546,170. (6,960,000 – 413,830).

Since January 2021, the company has leased out the lathe. The accountant, based on the order of the manager, opened an analytical accounting register, and the cost of the machine is 308,570 rubles. (360,000 – 51,430) was transferred from account 01 to account 03 and included in the balance line “1160”. At the end of 2021, it includes a machine valuation in the amount of 257,140 rubles. (308,570 – 51,430);

In line “1150” at the end of 2021, the cost of the operating system was 5,875,200 rubles. (6,546,170 – 308,570 – 300,000 – 62,400).

Under the terms of continued rental of the machine in 2021, the following lines are filled in the balance sheet:

- “1150” in the amount of RUB 5,512,800. (5,875,200 – 300,000 – 62,400);

“1160” in the amount of 205,710 rubles. (257,140 – 51,430).

The row data is summed up and ultimately reflected in the first section of the balance sheet (line “1100”). For fixed assets in the balance sheet as of December 31, 2021, the entries look like this:

| Indicator name | ||||||||||||

| ASSETS | ||||||||||||

| I. NON-CURRENT ASSETS | ||||||||||||

| Intangible assets | ||||||||||||

| Research and development results | ||||||||||||

| Intangible search assets | ||||||||||||

| Material prospecting assets | ||||||||||||

| Fixed assets | ||||||||||||

| Profitable investments in material assets | ||||||||||||

| Financial investments | ||||||||||||

| Deferred tax assets | ||||||||||||

| Other noncurrent assets | ||||||||||||

| Total for Section I | 5 718 510 | 6 132 340 | 6 546 170 | |||||||||

There are the following types of valuations of fixed assets: full and residual book value, full and residual replacement value.

Full book value

(a kind of “initial cost”) is formed at the moment the object enters into operation.

Depending on the source of receipt of fixed assets, their initial cost is understood as:

The cost of fixed assets contributed by the founders towards their contribution to the authorized capital of the enterprise by agreement of the parties;

The cost of fixed assets manufactured at the enterprise itself, as well as purchased from other enterprises or persons - in the amount of actual costs, including costs of delivery, installation, installation;

The cost of gratuitously received fixed assets, as well as funds allocated as government subsidies.

Replacement cost

- its essence is as follows: every year buildings, machines, equipment are put into operation, but at each time stage the prices for means of production differ (for example, it is obvious that two buildings of the same type, one of which was built in 1980, and the other - in 1995, have different prices). As a result, the balance sheets of industrial enterprises include fixed production assets acquired at different times and therefore valued at different prices, i.e., in fact, they are expressed in incomparable prices. To evaluate fixed assets at uniform prices, their periodic general revaluation (according to a single methodology and all sectors) is required. Such revaluation was last carried out on January 1, 1995, and the full book value of fixed assets based on inventory results as of January 1, 1992 was taken as the initial basis.

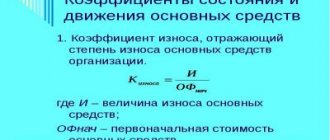

wear out during use

.

The monetary expression of losses by objects of their physical and technical-economic qualities is called depreciation of fixed assets. The original cost minus the amount of depreciation is called the “residual value of fixed assets”

.

The replacement cost of fixed assets minus depreciation is called “residual replacement cost”

. The degree of depreciation (in percentage) of each individual object after revaluation must remain equal to its degree of depreciation before the first assessment according to accounting data.

BALANCE OF FIXED FUNDS

is a statistical table, the data of which characterize the volume, structure, reproduction of fixed assets for the economy as a whole, industries and forms of ownership.

According to the data of this balance, indicators of depreciation, suitability, renewal, disposal, and use of fixed assets are calculated. Data on the availability of fixed assets is used to calculate indicators of capital intensity, capital-labor ratio, capital productivity and other important economic calculations. The balance of fixed assets is compiled by statistical authorities at the federal and regional levels at full and residual (less depreciation) value. Both balances can be compiled according to the balance sheet valuation in current prices, in average annual prices or in constant (base period) prices.

Average annual cost of fixed assets (FPE)

- an indicator that any accountant needs to calculate property taxes. We will explain below how to calculate the indicator and where to get the formula from.

Valuation of fixed assets in accounting

In domestic accounting and statistical practice, several main types of valuation of fixed assets are most often used, among which we can distinguish valuation at historical cost, at original cost taking into account depreciation, at full replacement cost, at replacement cost taking into account depreciation and at book value.

Definition 2

The full initial cost represents the cost of funds in prices that take into account fixed assets at the time of their placement on the balance sheet. Using this cost, you can express the actual cost of constructing a building, structure, including the acquisition, delivery, installation and installation of funds (equipment and machinery). The assessment is carried out at prices that are valid at the time of construction or purchase of these objects.

Do you need proofreading or review of academic work? Ask a question to the teacher and get an answer in 15 minutes! Ask a Question

After acceptance of fixed assets into operation, this cost can be reflected in the balance sheet asset in the “Fixed Assets” account, remaining unchanged until the moment of revaluation.

Residual initial cost includes the cost measured in the prices at which an item of fixed assets was placed on the balance sheet when accounting for depreciation at the time of its determination. This cost is determined by the full initial cost of fixed capital minus the amount of depreciation that has been accumulated in accordance with accounting data:

OPst = PPst – Wear

There are two types of wear and tear: physical wear and tear (depending on the technical condition), obsolescence (reduction of production costs, decrease in the consumer value of existing assets after the introduction of new, more efficient means of labor).

Full replacement cost can be determined by measuring the cost of recreating new items of fixed assets. This cost is taken into account when revaluing fixed assets, based on the actual conditions of their reproduction (contractual prices and estimated prices for construction and installation work, wholesale prices, etc.).

Residual replacement value can be determined as a result of revaluation as the difference between the full replacement cost of fixed assets and the monetary assessment of their depreciation in accordance with accounting information:

OVst = PVst – Wear

Valuation at book value characterizes the value of funds at the time they are registered on the balance sheet. The book value includes a mixed valuation of fixed assets, since part of the inventory objects is on the balance sheet at replacement cost at the time of the last revaluation, and objects that were introduced in subsequent periods are accounted for in accordance with the original cost (acquisition cost).

Formula for calculating the average annual cost of fixed assets

Since the procedure for paying taxes is fixed in the Tax Code, the formula for calculating any tax can be found there. Property tax is no exception.

The tax base for calculating property tax is the average annual cost of fixed assets.

The detailed calculation procedure is described in clause 4 of Art. 376 Tax Code of the Russian Federation.

GHS = (A1 + A2 + A3 + A4 + A5 + A6 + A7 + A8 + A9 + A10 + A11 + A12 + B1) / 13

, Where

SGS - average annual cost;

A2-A12 - the residual value of the property on the 1st day of each month, where the figure is the serial number of the month (for example, A3 - the residual value as of March 1);

The denominator of the formula contains the number 13 - this is the number of months in the tax period increased by one (12 + 1). The numerator ultimately also adds up 13 indicators.

Tax reporting on time and without errors! We are giving access for 3 months to Kontur.Ektern!

Try it

Calculation of the average cost of fixed assets with an example

Average cost differs from average annual cost in that it is used only when calculating advance property tax payments.

An example of a formula for calculating the average cost for six months:

CC = (A1 + A2 + A3 + A4 + A5 + A6 + B1) / 7,

Where

СС - average cost;

A2-A6 - the residual value of the property on the 1st day of each month, where the figure is the serial number of the month (for example, A3 - the residual value as of March 1);

Unlike the formula for calculating the average annual cost, in the above formula all indicators are taken as of the 1st day of the month; data at the end of the month is not used.

Note!

The calculations do not use the residual value of objects that are not subject to property tax or are recorded at cadastral value.

Example

.

Auto-jazz LLC repairs premium cars. Auto-jazz has repair equipment on its balance sheet.

Residual value of fixed assets in rubles:

as of 01/01/2018 - 589,000;

as of 02/01/2018 - 492,000;

as of 03/01/2018 - 689,000;

as of 04/01/2018 - 635,000.

In February, new equipment was purchased, as a result of which the residual value at the beginning of March became higher.

Let's calculate the average cost for January - March:

SS = (589,000 + 492,000 + 689,000 + 635,000) / 4 = 601,250.

How to determine the average annual cost of fixed assets on the balance sheet in thousand rubles.

The balance sheet is an excellent source for determining and analyzing the return on assets.

The average annual value of property is often used for analysis. To do this, you need to take the figures recorded in Section I of the balance sheet under the line “Fixed assets”. For comparison, two years are taken, for example the reporting year and the previous one.

SGS = (Gotch + Gpred) / 2, where

Gotch - the cost of the OS at the end of the current year;

Gpred - the cost of the operating system at the end of the previous year.

Let's consider an example of calculating the GHS from the balance sheet

. Auto-jazz LLC repairs premium cars. Auto-jazz has repair equipment on its balance sheet. The cost of the operating system on the balance sheet as of December 31, 2017 is 983,000 rubles, and as of December 31, 2018 - 852,000 rubles.

To get the GHS, we use the above formula:

GHS = (983,000 + 852,000) / 2 = 917,500 rubles.

Fixed assets in the balance sheet

are reflected in line 1150 of the “Non-current assets” section. Read about the features of data generation for this line in our material.

Conditions for classifying objects as fixed assets

Regulation of accounting for fixed assets is carried out in accordance with the Regulations “Accounting for Assets”, according to which, in order to recognize objects as fixed assets, they must meet several requirements:

- The use of objects must be carried out in production processes or for the management needs of the enterprise, including rental (the price of objects that are purchased for rental is not reflected in the line “fixed assets in the balance sheet”).

- The business must use the facility for more than twelve months.

- The initial price of the object must be at least one hundred thousand rubles.

- When an enterprise purchases a fixed asset, it should not be sold in the near future.

- In the future, the objects can bring profit to the company.

Have questions about this topic? Ask a question to the teacher and get an answer in 15 minutes! Ask a Question

What is considered a fixed asset?

Fixed assets include property assets that can be used as production assets necessary for the manufacture of products (providing services, carrying out work), as well as property used to manage the company. The fixed assets include:

- buildings and constructions;

- land;

- equipment;

- auto, motorcycle and other equipment;

- computing devices;

- measuring instruments;

- household equipment;

- farm livestock;

- perennial plantings;

- on-farm, logistics roads and railways, as well as other similar assets.

Fixed assets also include capital investments in the land fund (carrying out work that significantly improves the quality of agricultural land), environmental management facilities, as well as completed capital investments in leased property.

The cost of registered fixed assets consists of all costs associated with their acquisition and is repaid through depreciation. Depreciation charges are made using one of the methods chosen by the enterprise (clause 48 of the PBU for accounting and accounting, approved by order of the Ministry of Finance of Russia dated July 29, 1998 No. 34n):

- linear;

- reduction of balance;

- by the sum of the numbers of years of useful life;

- in proportion to the volume of production.

NPO property is not depreciated. The cost of land and mining facilities, water and other subsoil is not repaid.

Structure of fixed assets

Fixed assets in the balance sheet are reflected in the group of non-current assets. They are used in production activities and evenly distribute the entire amount of the cost of fixed assets to accrue the calculation of manufactured finished products or services produced.

Fixed assets consist of:

- Real estate (buildings, structures);

- Owned land plots;

- Transport (cars);

- Equipment and inventory for the production process;

- Motor transport and mobile mechanisms;

- Computer technology;

- Measuring instruments;

- Pets;

- Green spaces grown over a long period of time;

- Roads owned by the company;

- Expensive expenses for land enrichment;

- Capital investments in leased real estate fixed assets.

Depreciation charges gradually reduce the original cost of objects. The service life of the OS is calculated according to the new OKOF classifier from 2021.

It is important to take into account that regardless of the results of the company’s financial and economic activities (profitable or unprofitable), the amount of costs for depreciation of fixed assets remains the same.

Cost of fixed assets on the balance sheet: line 1150

In accounting, fixed assets include assets worth more than 40,000 rubles. with a service life of more than a year. In the balance sheet, fixed assets are reflected in the amount of their value reduced by the amount of depreciation (i.e., at the residual value).

To learn how the residual value of fixed assets is determined, read the material

“How to determine the residual value of fixed assets .

In the case of additional equipment (reconstruction, partial write-off) of fixed assets, leading to a change in the initial cost, this information is reflected in the appendices to the balance sheet. The same applies to the case of revaluation of property, carried out by indexing the replacement cost of assets or by direct recalculation to the actual market value. Any differences that arise are credited to additional capital.

The concept of average annual cost of fixed assets

The average annual total accounting value of fixed assets (fixed assets, funds) is calculated by accountants for the following purposes:

- preparation of appropriate accounting and statistical reporting,

- determination of the property tax base;

- achieving internal management and financial goals.

The full accounting value of fixed assets is the original price of the object, which is adjusted by the amount of revaluation (depreciation). Revaluation may be caused by reconstruction, additional equipment, modernization, completion and partial liquidation.

During operation, fixed assets are subject to wear and tear, and they completely or partially lose their original properties. For this reason, the calculation of the average annual value of fixed assets affects the calculation of the residual value.

The residual value is calculated by subtracting the amount of depreciation from the original cost.

Fixed assets, as a rule, transfer their value to finished products over a fairly long period, which may include several cycles. For this reason, accounting is organized in such a way that a one-time reflection and preservation of the original form occurs, including price losses over time.